- Communication Infrastructure & Services

- Fixed Satellite Services (FSS) Market

Fixed Satellite Services (FSS) Market Size, Share, and Growth Forecast, 2025 - 2032

Fixed Satellite Services (FSS) Market By Services Type (TV Channel Broadcast, Telecom Backhaul, Others), Enterprise Size (Small Offices and Home Offices (SOHO), Others), End-user, and Regional Analysis for 2025 - 2032

Fixed Satellite Services (FSS) Market Size and Trends Analysis

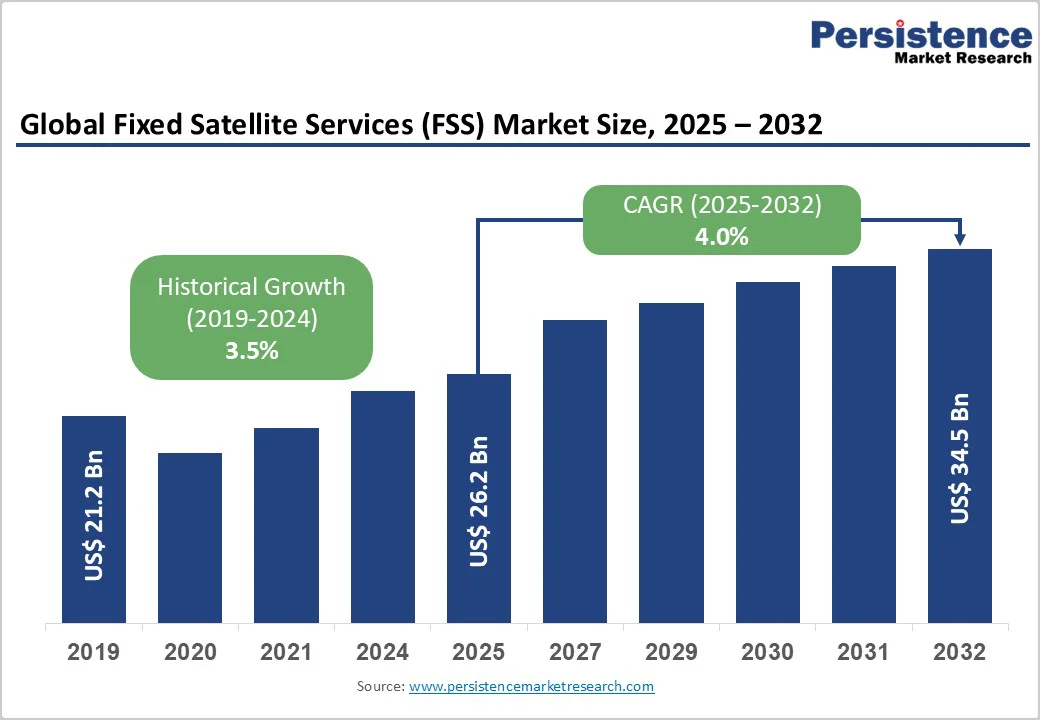

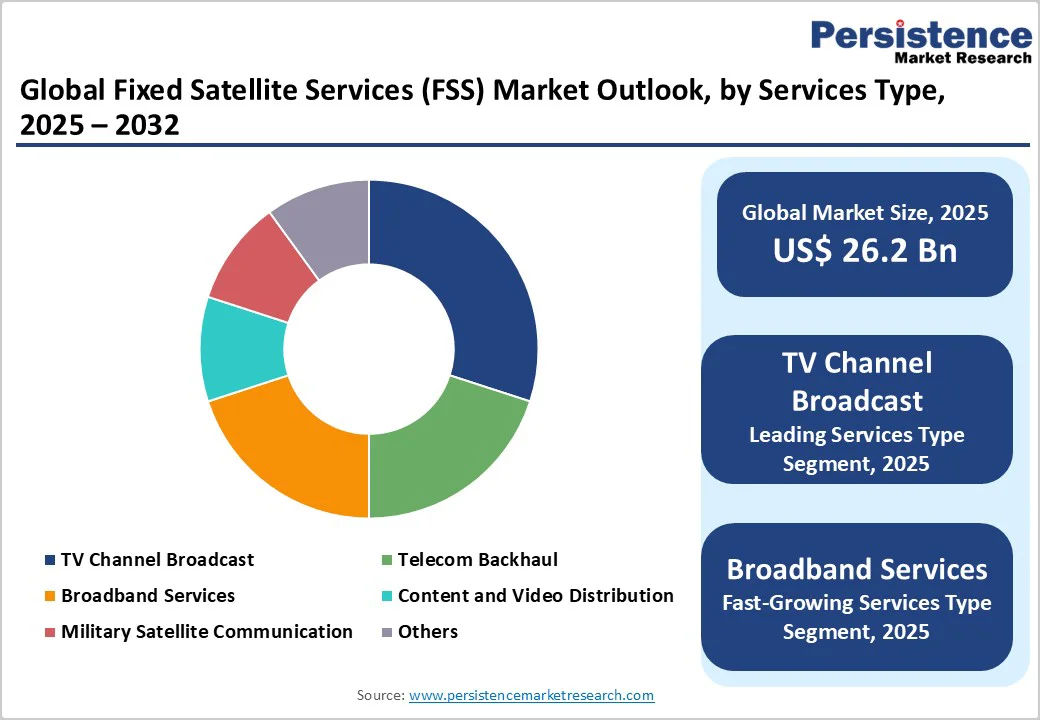

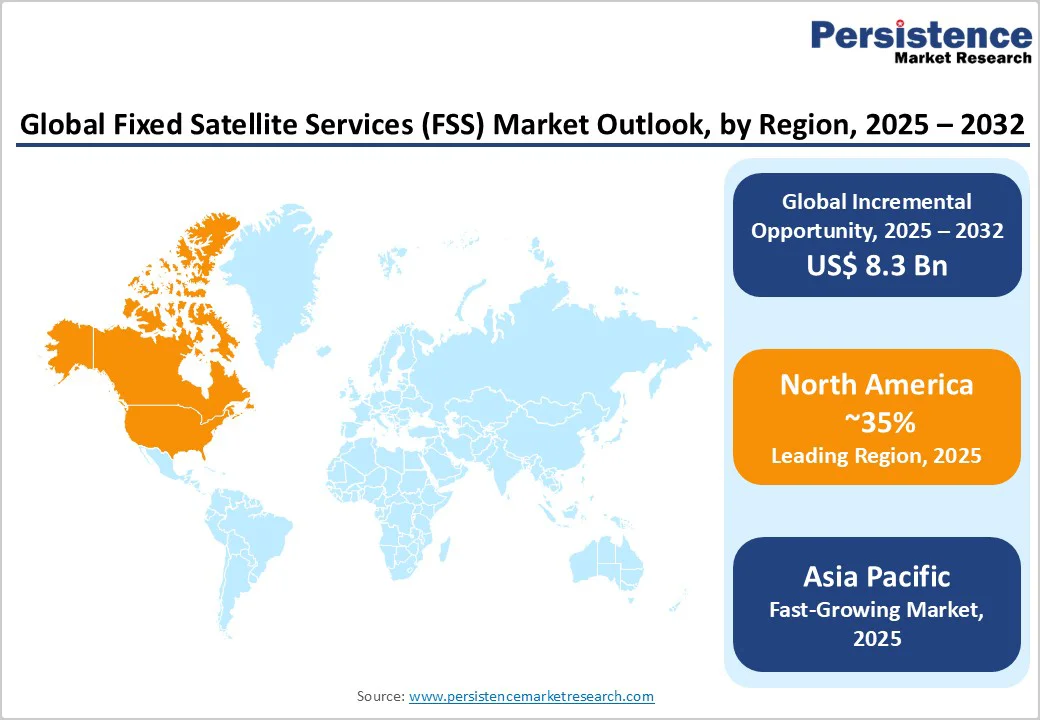

The global fixed satellite services (FSS) market size is likely to be valued at US$26.2 Billion in 2025 and is expected to reach US$34.5 Billion by 2032 growing at a CAGR of 4.0% during the forecast period from 2025 to 2032, driven by the increasing prevalence of remote connectivity needs, rising demand for high-bandwidth communication in telecom backhaul, and advancements in satellite technologies.

Reliable broadcasting and data distribution needs, especially in media, are driving the adoption of fixed satellite services (FSS). Innovations in broadband and military communications further support growth, while rising reliance on FSS for global, secure coverage, particularly in aerospace, continues to propel market expansion.

Key Industry Highlights:

- Leading Region: North America, commanding a 35% market share in 2025, driven by advanced telecom infrastructure, high prevalence of broadcasting, and strong R&D activities in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by increasing digitalization, rising awareness of satellite connectivity, and growing investments in broadband in countries such as China and India.

- Dominant Services Type: TV channel broadcast, holding approximately 30% of the market share, due to media distribution needs.

- Leading Enterprise Size: Large Enterprises, accounting for over 45% of market revenue, driven by global operations.

Leading End-user: Media and Entertainment, contributing nearly 35% of market revenue, due to content delivery demands.

- Key Market Driver: It reduces latency by dynamically routing data between space and ground systems. This convergence supports 5G, IoT, and enterprise applications, driving wider adoption across industries.

- Market Opportunity: Expanding digital connectivity in underserved regions by integrating FSS with 5G and IoT networks presents a major opportunity, enabling advanced communication services, global broadband access, and innovative satellite-based business models across diverse industries.

| Key Insights | Details |

|---|---|

|

Fixed Satellite Services (FSS) Market Size (2025E) |

US$26.2 Bn |

|

Market Value Forecast (2032F) |

US$34.5 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

4.0% |

|

Historical Market Growth (CAGR 2019 to 2024) |

3.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Remote Connectivity Needs and Demand for High-Bandwidth Services

The increasing global demand for remote connectivity is a primary driver of the fixed satellite services (FSS) Market. With the expansion of digitalization, industries such as telecommunications, defense, energy, and maritime require seamless connectivity in remote and hard-to-reach areas where terrestrial networks are limited. FSS bridges this gap by providing reliable communication links across continents, oceans, and isolated regions. The rapid surge in data consumption, fueled by cloud computing, video streaming, IoT applications, and enterprise networks, is further increasing the demand for high-bandwidth satellite services.

Governments and private organizations are also investing in satellite infrastructure to enhance connectivity for rural communities, disaster management, and mobile backhaul. High-throughput satellites (HTS) and Low Earth Orbit (LEO) constellations are meeting these bandwidth demands by offering faster data transfer rates, lower latency, and scalable capacity. As businesses and consumers increasingly depend on digital services, FSS providers are expanding offerings to ensure uninterrupted, high-performance broadband connectivity worldwide, reinforcing their role in bridging the global digital divide.

High Satellite Launch and Spectrum Allocation Costs

The high costs associated with satellite launch and spectrum allocation for fixed satellite services (FSS) pose a significant restraint on market growth. The development, manufacturing, and deployment of communication satellites require billions of dollars in investment, including launch vehicle costs, insurance, and ground infrastructure. Despite advancements in reusable rockets, costs for large satellites remain high, particularly for geostationary systems that demand precision placement and long operational lifespans.

Spectrum allocation poses regulatory and financial challenges. Securing orbital slots and frequency bands requires complex coordination with international regulatory bodies, such as the International Telecommunication Union (ITU), often resulting in delays and additional costs. Competition for limited spectrum resources is intensifying as Low Earth Orbit (LEO) constellations, terrestrial 5G networks, and other wireless services proliferate. These constraints can slow deployment timelines and restrict scalability for FSS providers.

Advancements in HTS Satellites and LEO Integrations

Advancements in High Throughput Satellites (HTS) and LEO integrations present significant growth opportunities for the fixed satellite services (FSS) Market. HTS technology significantly increases data throughput through spot-beam architectures, optimizing bandwidth utilization and reducing per-bit costs. This enables operators to deliver high-speed broadband services, supporting growing demands from enterprises, governments, and consumers. The deployment of LEO constellations, operating closer to Earth, minimizes latency and improves real-time communication performance, which is crucial for applications such as video conferencing, IoT, and cloud services.

The integration of HTS and LEO systems is creating hybrid networks that combine the wide coverage of geostationary satellites with the low latency of LEO satellites. These advancements are particularly impactful in remote and underserved regions, offering seamless, resilient connectivity where terrestrial infrastructure is limited. Partnerships between FSS providers and space technology companies are accelerating innovation, leading to more flexible, scalable, and cost-efficient satellite communication ecosystems that can support next-generation data-intensive applications globally.

Category-wise Analysis

Services Type Insights

TV channel broadcast dominates the market, accounting for a 30% share in 2025. Its dominance is driven by content delivery, reliability, and global reach, making it preferred for media. TV channel broadcast services, such as those from SKY Perfect JSAT Corporation, provide HD transmission, ensuring quality. Its bandwidth and coverage make it preferred for operators.

Broadband services are the fastest-growing segment, driven by efforts to close internet gaps and by rising adoption in rural regions. Offering high-speed and reliable connectivity, broadband via satellite meets the needs of remote users. Advancements in High-Throughput Satellites (HTS) are accelerating adoption, particularly across the Asia Pacific and Africa.

Enterprise Size Insights

Large enterprises lead the market, holding a 45% share in 2025, driven by their extensive global operations and need for reliable backhaul connectivity. These organizations rely on FSS for secure, high-capacity communication across dispersed locations. Rising data demands and network expansion further strengthen their dominance in satellite-based connectivity solutions.

The Small and Medium Businesses (SMB) segment is the fastest-growing, driven by affordable VSAT solutions and expanding e-commerce. Satellite connectivity offers reliable communication in remote areas, enabling seamless operations. Its convenience, scalability, and declining service costs make it an attractive choice for emerging digital enterprises and startups.

End-user Insights

The media and entertainment segment dominates the market, contributing 35% in 2025. Its leadership stems from widespread satellite use in television broadcasting and live event coverage, as well as rising video streaming demand. FSS enables efficient content distribution to vast audiences, making it the preferred medium for reliable, high-quality global media transmission.

The IT and telecommunications segment is the fastest-growing, driven by rising data traffic, 5G expansion, and growing backhaul requirements in remote regions. FSS offers versatile, high-capacity solutions that ensure reliable connectivity, supporting network resilience, bandwidth demand, and seamless communication across enterprises and mobile network operators.

Regional Insights

North America Fixed Satellite Services (FSS) Market Trends

North America dominates, accounting for 35% in 2025, driven by increasing demand for high-speed broadband connectivity, expanding 5G infrastructure, and growing applications across the defense, media, and enterprise sectors. The region’s strong technological base and presence of major satellite operators, such as Intelsat, SES S.A., and EchoStar Corporation, support continuous innovation in service delivery.

Advancements in high-throughput satellites (HTS) and low Earth orbit (LEO) constellations are enhancing data transmission capacity and coverage, catering to remote and underserved areas. The U.S. leads the market, propelled by government and commercial investments in space-based communications and resilient network solutions. The growing need for reliable connectivity across the maritime, aviation, and oil & gas sectors is fueling adoption. High capital expenditure and competition from fiber and 5G terrestrial networks pose challenges.

Europe Fixed Satellite Services (FSS) Market Trends

Advancements in satellite technology, high demand for broadband connectivity, and strong adoption across broadcasting, defense, and enterprise communication sectors drive Europe. The region benefits from a mature satellite infrastructure and the presence of major players such as SES S.A., Eutelsat Communications, and Intelsat Corporation, which provide extensive coverage and high-capacity bandwidth across Europe, the Middle East & and Africa.

The market is further supported by the European Union’s initiatives to promote digital connectivity and space innovation, including the EU Space Programme and Copernicus. The increasing demand for High-Throughput Satellites (HTS) and their integration with Low Earth Orbit (LEO) constellations are enhancing data transfer speeds and reducing latency, enabling improved internet access in underserved areas. The growing adoption of cloud-based services, maritime communication, and in-flight connectivity is expanding commercial opportunities. Europe’s strong emphasis on sustainability and energy efficiency is also driving investments in next-generation satellite systems.

Asia Pacific Fixed Satellite Services (FSS) Market Trends

Asia Pacific is the fastest-growing region, with a 25% share in 2025, driven by rapid digitalization, expanding broadband demand, and the increasing adoption of satellite-based connectivity across remote and rural regions. Countries such as China, India, Japan, and Thailand are leading developments, supported by government initiatives promoting space technology, communication infrastructure, and digital inclusion. The region’s rising need for high-speed data, direct-to-home (DTH) broadcasting, and enterprise connectivity is fueling investment in both geostationary and High-Throughput Satellites (HTS).

Key players such as Thaicom Public Company Ltd., China Satcom, and SKY Perfect JSAT Corporation are focusing on localized service models, affordable bandwidth solutions, and partnerships with telecom operators to bridge connectivity gaps. The emergence of Low Earth Orbit (LEO) satellite networks is further transforming service capabilities by reducing latency and improving broadband performance. The growing adoption of cloud-based communication and maritime and aviation connectivity is expanding application opportunities.

Competitive Landscape

The global fixed satellite services (FSS) market is highly competitive, comprising a mix of satellite operators, communication providers, and network solution companies striving to enhance connectivity and bandwidth efficiency. In developed regions such as North America and Europe, leading players such as SES S.A. and Intelsat Corporation dominate the market through strong R&D capabilities, extensive satellite fleets, and established global networks. Their focus on service reliability and data capacity expansion drives adoption across broadcasting, defense, and enterprise communication sectors.

In the Asia Pacific region, companies such as Thaicom Public Company Ltd. leverage localized solutions and cost-effective services to cater to growing demand from emerging economies. The market is experiencing rapid transformation through the integration of High-Throughput Satellites (HTS), which offer higher bandwidth and improved spectral efficiency. Partnerships, mergers, and the integration of Low Earth Orbit (LEO) satellite constellations are intensifying competition and expanding service capabilities.

Key Industry Developments

- In March 2024, Arabsat, the satellite service provider in the Middle East region, signed an MoU with Telesat to establish a long-term strategic partnership. The partnership aims to work together on the commercialization of the Telesat Lightspeed constellation in the Middle East and North Africa region, as well as regulatory issues and orbital resources.

- In September 2023, SpaceX announced an agreement to provide the Telesat Lightspeed constellation to Low Earth Orbit (LEO).

Companies Covered in Fixed Satellite Services (FSS) Market

- Embratel Star One

- Eutelsat Communications

- Telesat Holdings

- SKY Perfect JSAT Corporation

- Thaicom Public Company Ltd

- Nigerian Communications Satellites Ltd

- Telenor Satellite AS

- Singapore Telecommunications Ltd (Singtel)

- SES S.A

- Arabsat

- Hispasat

- Intelsat Corporation

Frequently Asked Questions

The global fixed satellite services (FSS) market is projected to reach US$26.2 Billion in 2025.

The rising prevalence of remote connectivity needs and the demand for high-bandwidth services are the key drivers.

The fixed satellite services (FSS) market is poised to witness a CAGR of 4.0% from 2025 to 2032.

Advancements in HTS satellites and LEO integrations are the key opportunities.

Embratel Star One, Eutelsat Communications, Telesat Holdings, SES S.A., and Intelsat Corporation are the key players.