- Semiconductor Materials & Components

- Fixed Inductor Market

Fixed Inductor Market Size, Share, and Growth Forecast, 2025 - 2032

Fixed Inductor Market by Inductor Type (Wire-Wound Inductors, Multilayer Inductors, Thin-Film Inductors, Others), Core (Air Core, Ferrite Core, Iron Core, Ceramic Core, Others), Application (Consumer Electronics, Automotive, Industrial, Telecommunications, Others), and Regional Analysis for 2025 - 2032

Fixed inductor market size and analysis

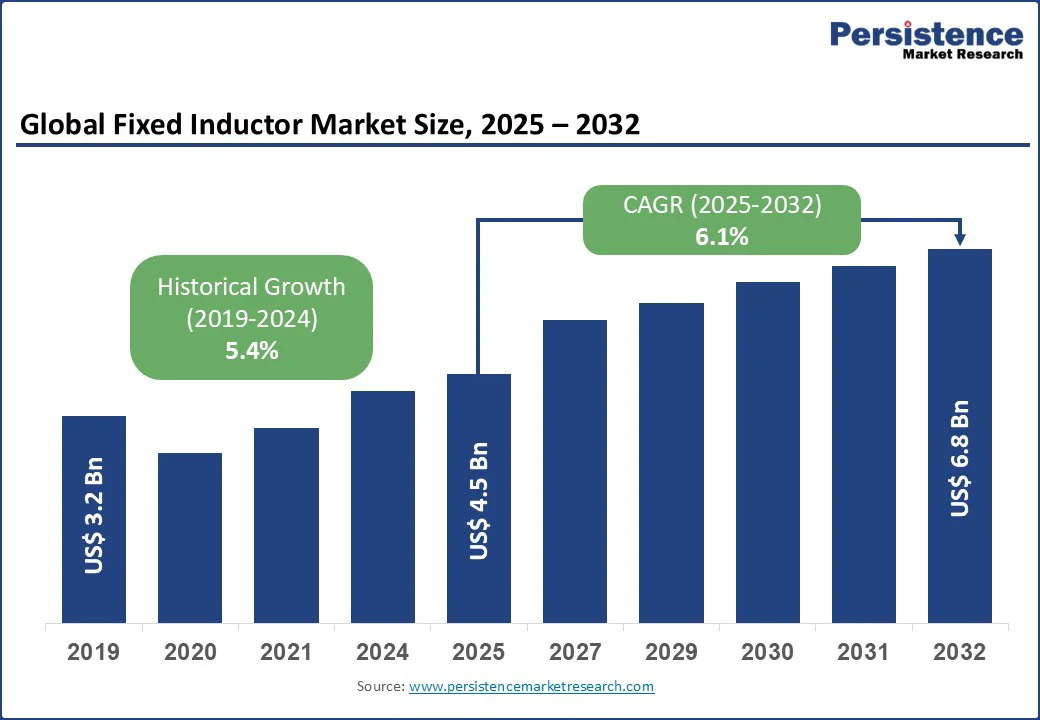

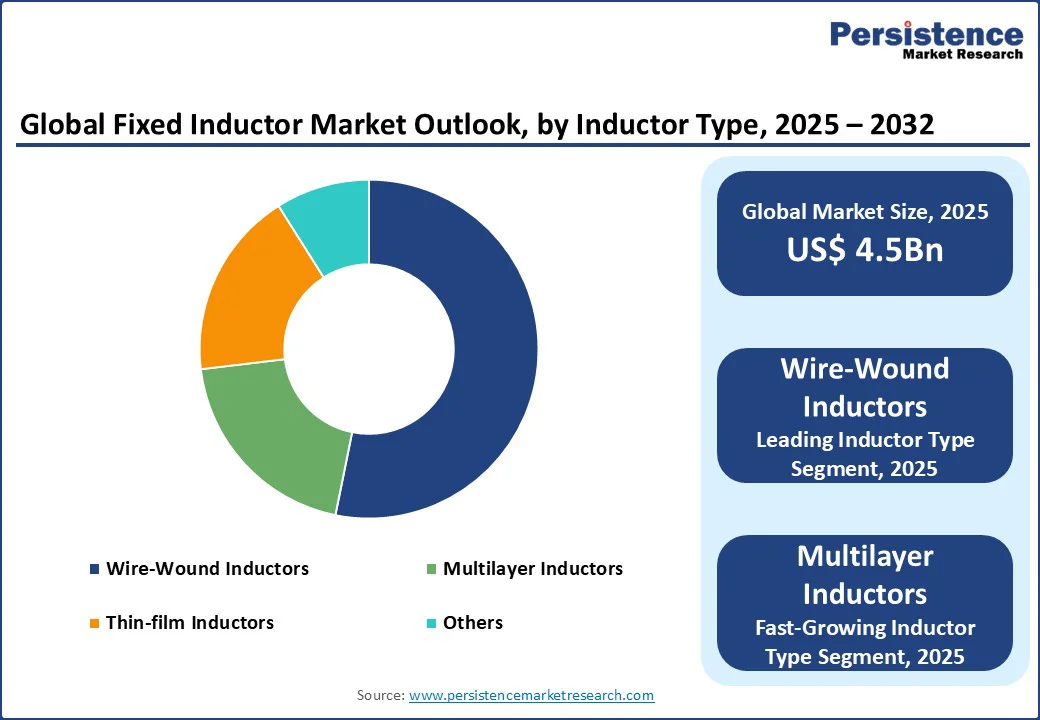

The global fixed inductor market size is likely to be valued at US$4.5 Bn in 2025 and reach US$6.8 Bn by 2032, growing at a CAGR of 6.1% during the forecast period from 2025 to 2032.

The fixed inductor market is experiencing robust growth, driven by increasing demand from consumer electronics, automotive, and telecommunications industries, where compact, efficient, and high-performance components are critical.

Fixed inductors, essential for power management, signal filtering, and energy storage in electronic circuits, benefit from advancements in miniaturization and material technologies. The rise in global demand for smart devices, electric vehicles (EVs), and 5G infrastructure supports market expansion.

Key Industry Highlights:

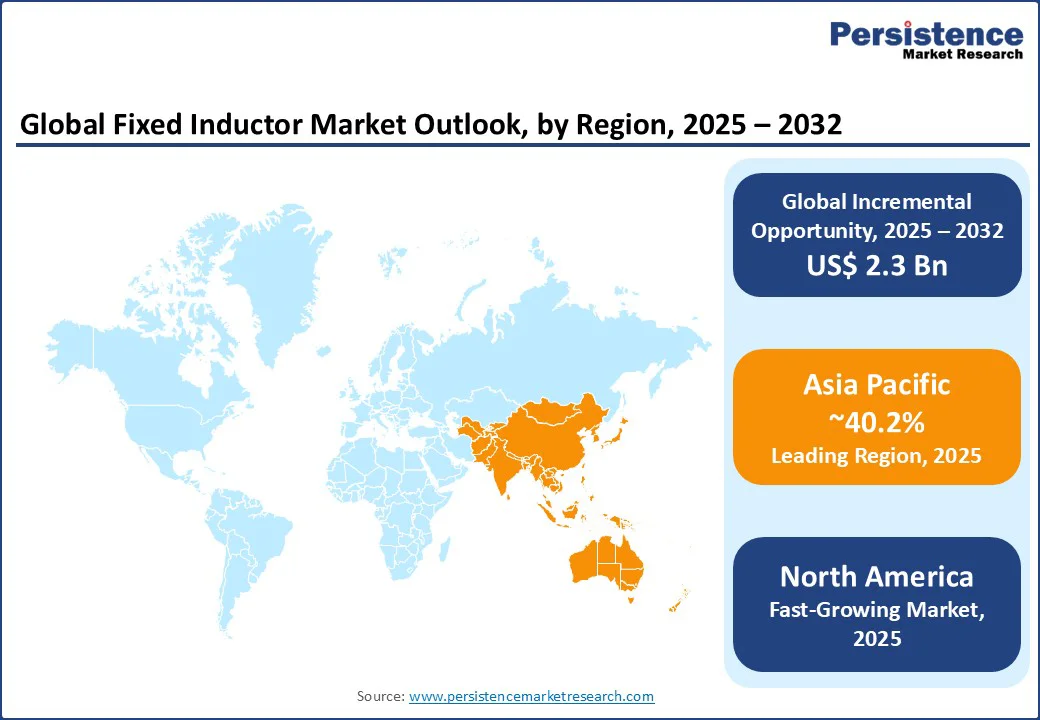

- Leading Region: Asia Pacific holds a 40.2% market share in 2025, driven by high electronics production and rapid industrialization in countries such as China, Japan, and South Korea.

- Fastest-Growing Region: North America is the fastest-growing region, propelled by advancements in automotive electronics and telecommunications in the U.S. and Canada.

- Investment Plans: China’s 14th Five-Year Plan (2021-2025) emphasizes electronics manufacturing, boosting demand for fixed inductors in consumer and industrial applications.

- Dominant Inductor Type: Wire-Wound Inductors account for 53.4% of the market share, due to their high efficiency and suitability for power-intensive applications.

- Leading Application: Consumer Electronics contributes over 42.3% of market revenue, fueled by global demand for smartphones, wearables, and IoT devices.

| Global Market Attribute | Key Insights |

| Fixed Inductor Market Size (2025E) | US$ 4.5Bn |

| Market Value Forecast (2032F) | US$ 6.8Bn |

| Projected Growth (CAGR 2025 to 2032) | 6.1% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.4% |

Market Dynamics

Driver: Surging Demand for Consumer Electronics and IoT Devices

The global fixed inductor market is witnessing significant growth due to the rising demand for consumer electronics and Internet of Things (IoT) devices. Fixed inductors are critical components in power management and signal processing for smartphones, wearables, smart home devices, and IoT sensors. According to the International Data Corporation (IDC), global smartphone shipments are expected to reach 1.24 billion units by 2025, driving demand for compact and efficient inductors.

Companies such as TDK Corporation and Murata Manufacturing reported a surge in inductor sales for IoT applications in 2024. Government initiatives promoting smart cities, such as India’s Smart Cities Mission, and increasing consumer spending on electronics in emerging economies ensure sustained demand, positioning consumer electronics as a key driver for market growth through 2032.

Restraint: Price Volatility of Raw Materials and Supply Chain Disruptions

The fixed inductor market faces challenges due to fluctuating raw material prices and supply chain disruptions. Key materials such as ferrite, copper, and ceramic are subject to price volatility due to global supply constraints and geopolitical factors. In 2023, copper prices fluctuated significantly, impacting production costs for manufacturers, as reported by the London Metal Exchange. This volatility creates pricing pressures, particularly for smaller players, limiting their competitiveness.

Additionally, global supply chain disruptions, such as semiconductor shortages and logistics delays, hinder timely production and delivery. Competition from alternative technologies, such as integrated circuits with embedded inductors, also poses a challenge in cost-sensitive markets, restraining overall market growth.

Opportunity: Growing Adoption in Electric Vehicles and 5G Infrastructure

The increasing adoption of electric vehicles (EVs) and 5G infrastructure presents significant opportunities for the fixed inductor market. Fixed inductors are essential in EV powertrains, battery management systems, and charging infrastructure for efficient energy conversion and storage.

The International Energy Agency (IEA) projects global EV sales to reach 45 million units annually by 2030, driving demand for high-performance inductors. In telecommunications, 5G network expansion requires inductors for base stations and RF modules. Companies such as Vishay Intertechnology and Taiyo Yuden are innovating with compact, high-frequency inductors for 5G applications.

Government incentives, such as the U.S. CHIPS Act and the EU’s Digital Decade initiative, support investments in 5G and automotive electronics, creating opportunities for manufacturers to develop advanced, energy-efficient inductors to meet evolving industry needs through 2032.

Category-wise Insights

Inductor Type Insights

- Wire-wound inductors hold the largest market share, approximately 53.4% in 2025, due to their high efficiency and suitability for power-intensive applications. Widely used in consumer electronics and automotive systems, these inductors offer superior performance in power supplies and DC-DC converters. Companies such as TDK Corporation and Murata Manufacturing lead with extensive portfolios, catering to demand in smartphones, EVs, and industrial equipment across North America and the Asia Pacific.

- Multilayer inductors are the fastest-growing segment, driven by their compact size and suitability for high-frequency applications in 5G devices and IoT systems. Their adoption is rising in telecommunications and wearables, with brands such as Taiyo Yuden and Coilcraft expanding offerings in Europe and the Asia Pacific, supported by growing demand for miniaturized, high-performance components.

Core Insights

- Ferrite core inductors account for the largest market share, approximately 49.8% in 2025, due to their high magnetic permeability and cost-effectiveness. Widely used in consumer electronics and industrial applications, ferrite core inductors are favored for their efficiency in power management. Companies such as Vishay Intertechnology and Panasonic Corporation lead with robust portfolios, serving markets in the Asia Pacific and North America.

- Ceramic core inductors are the fastest-growing segment, driven by their suitability for high-frequency applications in telecommunications and automotive electronics. Their adoption is rising in 5G base stations and EV charging systems, with players such as AVX Corporation and KEMET Corporation expanding offerings in Europe and North America to meet demand for high-performance, compact inductors.

Application Insights

- The consumer electronics sector accounts for over 42.3% of market revenue in 2025, driven by global demand for smartphones, wearables, and IoT devices. Fixed inductors are critical for power management and signal filtering in these devices. Major players such as Murata Manufacturing and TDK Corporation supply high-performance inductors for projects in China and the U.S., where consumer spending on electronics fuels demand.

- The automotive sector is the fastest-growing application, propelled by rising investments in electric vehicles and advanced driver-assistance systems (ADAS). Fixed inductors are used in battery management and powertrain systems, with companies such as Vishay Intertechnology innovating for high-efficiency applications. Growth in Asia Pacific and North America, driven by EV adoption, supports this segment’s rapid expansion.

Regional Insights

Asia Pacific Fixed Inductor Market Trends

Asia Pacific dominates the fixed inductor market, accounting for 40.2% share in 2025, fueled by rapid industrialization, high electronics production, and government initiatives in countries such as China, Japan, and South Korea. China, the world’s largest electronics manufacturer, contributes significantly to global inductor demand, per the China Electronics Industry Association.

Japan’s automotive sector and South Korea’s 5G infrastructure drive demand for high-performance inductors. India’s Make in India initiative boosts electronics manufacturing, increasing the need for fixed inductors in consumer and industrial applications. The region’s telecommunications and automotive industries, supported by companies such as Murata Manufacturing and Taiyo Yuden, ensure Asia Pacific’s market dominance through 2032.

North America Fixed Inductor Market Trends

North America is the fastest-growing region, driven by robust demand from the automotive and telecommunications sectors in the U.S. and Canada, supported by advanced technological infrastructure. The U.S. automotive industry relies heavily on fixed inductors for EVs and ADAS. Consumer electronics, including smartphones, wearables, and IoT devices, require compact and efficient inductors.

Manufacturers are focusing on miniaturizing inductors without compromising performance, catering to the demand for smaller and more powerful devices. Canada’s telecommunications sector drives demand for high-frequency inductors in 5G networks, per the Canadian Wireless Telecommunications Association.

Major players such as Vishay Intertechnology and Coilcraft dominate with extensive distribution networks, catering to automotive and telecom projects. Consumer preference for energy-efficient, compact inductors strengthens North America’s market position.

Europe Fixed Inductor Market Trends

Europe is the second fastest-growing region, driven by stringent regulatory standards, rising demand in automotive and telecommunications, and infrastructure development in countries such as Germany and France. In 2022, approximately 17.1 million motor vehicles were produced in the European Union, with a significant portion being passenger cars.

Per the European Automobile Manufacturers’ Association (ACEA), supports demand for inductors in EVs and ADAS. Germany’s telecommunications sector benefits from players such as TDK Corporation and AVX Corporation. The EU’s Digital Decade initiative promotes 5G infrastructure, increasing demand for high-frequency inductors in telecom applications. Europe’s focus on sustainability and high-quality standards drives market growth, with companies innovating to meet regulatory and consumer demands.

Competitive Landscape

The global fixed inductor market is highly competitive and fragmented, with numerous domestic and international players. Leading companies such as TDK Corporation, Murata Manufacturing, and Vishay Intertechnology dominate through extensive product portfolios and global distribution networks.

Regional players such as Chilisin Electronics focus on localized offerings in the Asia Pacific. Companies are investing in advanced manufacturing technologies and high-frequency inductors to enhance market share, driven by demand for compact, efficient components in consumer electronics and automotive sectors.

Key Industry Developments:

- February 2025: TDK introduced wire-wound inductors for high-current automotive PoC applications, designed to support simultaneous power and data transmission over a single coaxial cable for vehicle systems such as ADAS. These components operate across a wide temperature range (-55 °C to +155 °C), provide high impedance across a broad frequency spectrum, and can handle high currents up to 1650 mA, contributing to reduced vehicle weight and improved efficiency.

- July 2025: TDK Corporation expanded its ADL4524VL series of wire-wound inductors for automotive Power-over-Coax (PoC) applications, entering mass production in July 2025. These inductors are designed to support high-frequency signal handling with a wide frequency range from 10 MHz to 1 GHz, enabling high impedance characteristics. This feature allows for the reduction of the number of inductors used in PoC filter circuits, thereby saving space and simplifying design.

Companies Covered in Fixed Inductor Market

- TDK Corporation

- Murata Manufacturing Co., Ltd.

- Vishay Intertechnology, Inc.

- Taiyo Yuden Co., Ltd.

- AVX Corporation

- KEMET Corporation

- Coilcraft, Inc.

- Delta Electronics, Inc.

- Panasonic Corporation

- Samsung Electro-Mechanics Co., Ltd.

- Bourns, Inc.

- Sumida Corporation

- Chilisin Electronics Corp.

- Others

Frequently Asked Questions

The Fixed Inductor market is projected to reach US$4.5 Bn in 2025.

Growing demand for consumer electronics, IoT devices, and expanding applications in electric vehicles and 5G infrastructure are the key market drivers.

The Fixed Inductor market is poised to witness a CAGR of 6.1% from 2025 to 2032.

The rising adoption of electric vehicles and 5G infrastructure is the key market opportunity.

TDK Corporation, Murata Manufacturing, Vishay Intertechnology, and Taiyo Yuden are key market players.