- Food Ingredients & Additives

- Fillings & toppings market Size, Share, and Growth Forecast 2026 - 2033

Fillings & toppings market Size, Share, and Growth Forecast 2026 - 2033

Fillings & toppings market by Product Type (Creams, Fruits & Nuts, Fondants, Syrups, Others), Form (Solid, Liquid, Gel, Foam), Application (Bakery Products, Confectionery, Dairy & Frozen Desserts, Beverages, Others), and Regional Analysis for 2026 - 2033

Fillings & toppings market Share and Trends Analysis

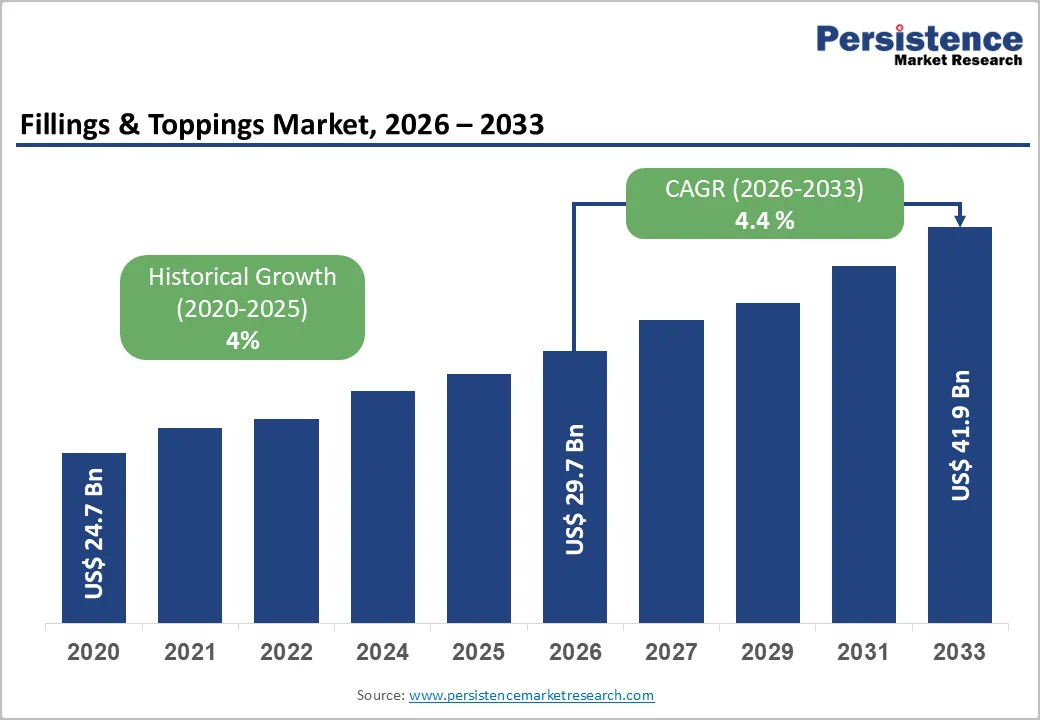

The global fillings & toppings market size is likely to be valued at US$ 31.2 billion in 2026, and is projected to reach US$ 41.9 billion by 2033, growing at a CAGR of 4.3% during the forecast period 2026-2033.

This growth reflects increasing demand for bakery, confectionery, dairy, and dessert products, driven by shifting consumer tastes, growing urbanization, and rising disposable incomes. Manufacturers’ innovation in texture, formulation, and convenience formats supports broader adoption across applications. The market’s steady expansion also suggests robust long-term potential in both developed and emerging economies.

Key Industry Highlights

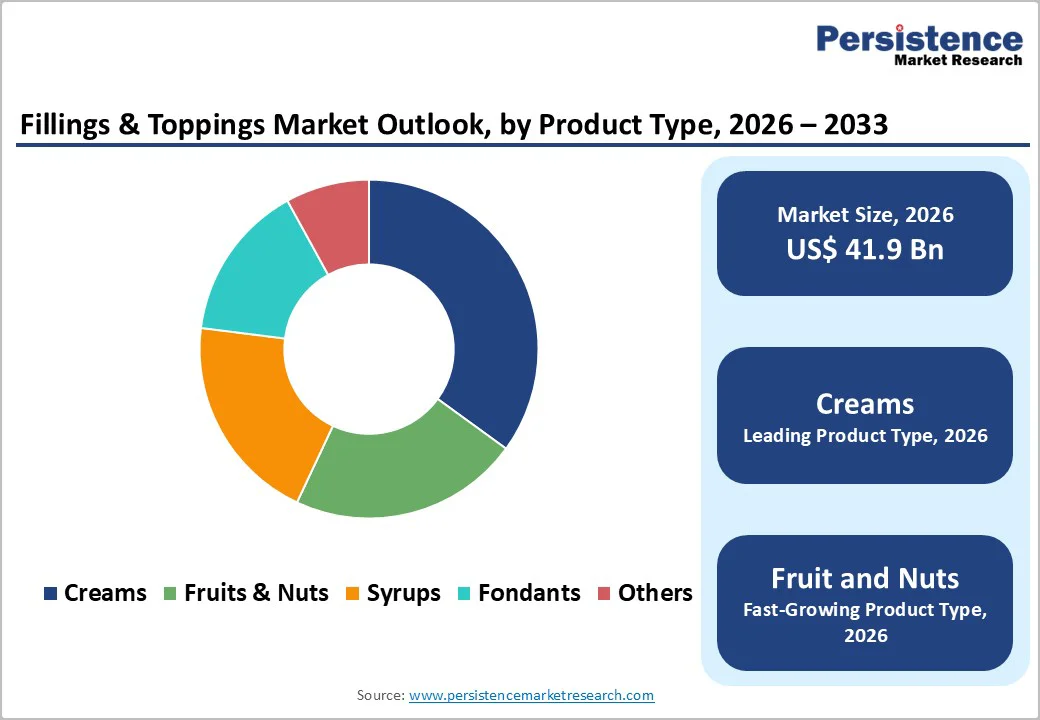

- Leading Product Type: Creams are expected to hold the largest market share in 2026, driven by their extensive use across bakery, confectionery, and dessert products.

- Fastest-Growing Product Type: Fruits & nuts are projected to grow the fastest through 2033, supported by rising clean-label, natural, and premium ingredient demand.

- Leading Form: Liquid fillings and toppings are expected to hold the largest share in 2026, supported by their widespread preference.

- Dominant Application: Bakery products are anticipated to account for around 42% revenue share in 2026, reflecting strong utilization in pastries, cakes, and commercial bakery production.

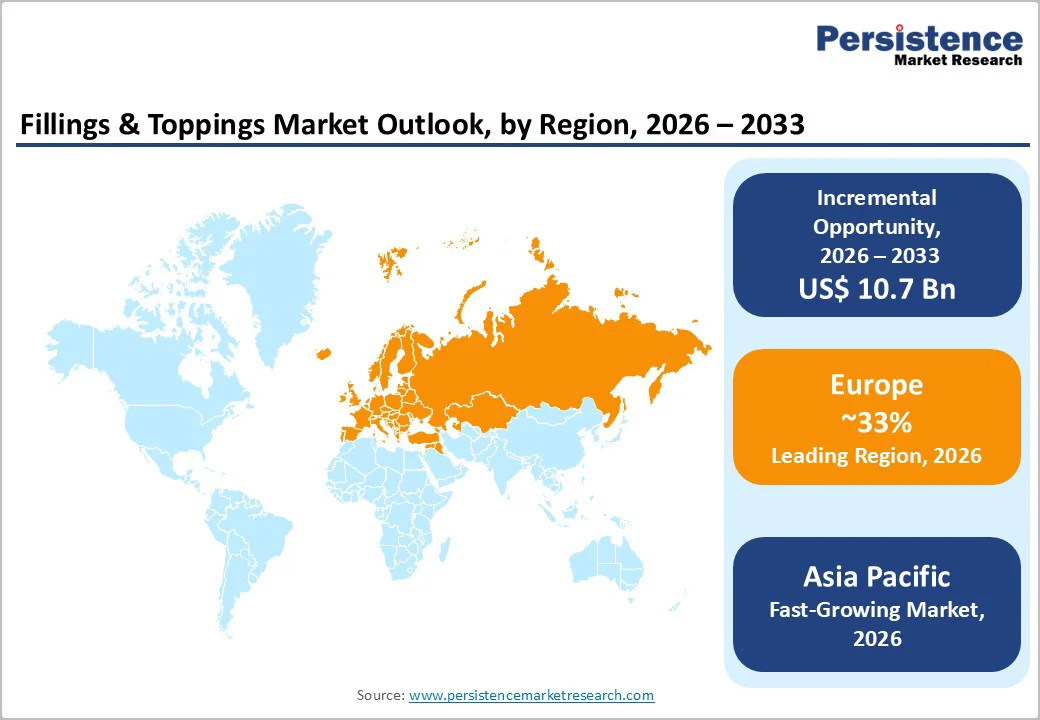

- Dominant Region: Europe is projected to lead in 2026 due to its mature bakery sector and strong confectionery consumption, while Asia Pacific is expected to grow the fastest.

- Key Market Trends: The market is being propelled forward by the rising demand for plant-based, reduced-sugar fillings, expanded use of gel and foam formulations, and accelerated supplier expansion into Asia Pacific.

| Key Insights | Details |

|---|---|

|

Fillings & toppings market Size (2026E) |

US$ 31.2 Bn |

|

Market Value Forecast (2033F) |

US$ 41.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.3 % |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.0 % |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growing Demand for Convenient, Clean-Label, and Innovative Bakery & Dessert Solutions

Consumer preferences are shifting toward healthier, clean-label, and plant-based bakery and dessert products, increasing demand for fillings and toppings made with natural ingredients and reduced sugar. This trend reflects rising health awareness and a preference for convenient, ready-to-use formats that simplify preparation while maintaining consistent quality across bakery, confectionery, and dessert applications.

Organized retail, foodservice, and e-commerce channels are also expanding, creating wider access to standardized fillings and toppings and supporting higher-volume procurement. Manufacturers are also advancing formulation technology, developing stable textures, improved shelf life, and innovative ingredient systems that meet regulatory expectations and evolving consumer taste. These combined factors are strengthening global adoption and widening application across frozen desserts, dairy alternatives, and modern convenience foods.

Raw Material Volatility and Rising Health-Driven Regulatory Pressures

Fluctuating prices of key raw materials such as sugar, cocoa, dairy fats, nuts, and fruit purées create cost instability for manufacturers, often compressing margins or prompting product price increases. These shifts can reduce demand, especially for chocolate and nut-based formulations that are more sensitive to commodity swings. A notable share of consumers is increasingly cautious about high-sugar fillings, further constraining traditional product categories.

At the same time, growing health awareness and stricter regulations targeting sugar content and calorie density are placing added pressure on established formulations. Markets with strong nutritional oversight face sharper declines in demand for high-sugar and high-fat toppings, requiring investments in reformulation and cleaner alternatives. This dual challenge limits growth potential and raises operational complexity for producers.

Strengthening Preference for Plant-based Ingredients

Consumer demand for fillings and toppings is experiencing significant growth across North America, Europe, and Asia Pacific, driven by shifting preferences toward natural, plant-based, clean-label, and functional ingredients. Industry research from 2025 confirms that consumers prioritize label transparency and actively seek products with functional benefits. This trend reflects a broader movement toward health-conscious consumption, where shoppers scrutinize ingredient lists and favor recognizable, minimally processed components. Manufacturers who respond to these preferences gain competitive advantage by aligning their product portfolios with consumer values. The shift presents a strategic opportunity for companies to reformulate existing offerings and develop new products that meet these elevated expectations while maintaining taste, texture, and shelf stability.

The applicability of fillings and toppings is expanding beyond traditional bakery and confectionery categories into dairy products, frozen desserts, beverages, and convenience foods. Recent advances in formulation science and processing technologies enable manufacturers to create stable, high-quality ingredients that perform consistently across diverse applications. This technological progress allows companies to diversify their revenue streams and reduce dependence on seasonal product cycles that historically characterized bakery and confectionery markets. Success in this evolving market requires investment in R&D, close collaboration with food manufacturers, and agility to adapt formulations as consumer preferences continue to evolve across global markets.

Category-wise

Product Type Insights

The creams segment is likely to remain the market leader in 2026, holding an estimated 35% share globally. This dominance stems from creams’ high versatility as they have smooth texture, stable consistency, and reliable flavor and visual appeal. Because creams work well in a wide variety of bakery, confectionery, and dessert applications, from cakes and pastries to filled breads and donuts, manufacturers continue to favour them for both industrial-scale bakeries and artisanal bakeries alike. Their adaptability across dairy-based, non-dairy, whipped, and plant-based cream variants further strengthens their broad appeal and market penetration.

The fruits & nuts segment is poised for the fastest growth, projected to expand at a CAGR of around 6.3% during the 2026-2033 forecast period. This acceleration is driven by rising consumer demand for clean-label, natural, and authentic ingredient profiles, especially in health-conscious and emerging markets. Inclusion of visible fruit pieces or nuts provides perceived freshness and premium value, aligning with shifting dietary trends. Advances in processing and preservation techniques now enable fruit and nut-based fillings to maintain texture and flavor while delivering shelf stability, enhancing their appeal to both manufacturers and consumers.

Product Form Insights

The solid segment is expected to hold approximately 25% of the fillings & toppings market revenue share in 2026. This category includes nut or fruit inclusions, sprinkles, and textured toppings, widely preferred for their stability, ease of storage, and versatility across bakery, confectionery, frozen desserts, and snack applications. Solids provide consistent texture, visual appeal, and compatibility with both industrial-scale and artisanal production processes, making them the backbone of the fillings & toppings market.

Gel-based fillings and toppings are projected to grow at an estimated CAGR of 6.5% through 2033, making them the fastest-growing form. Gel enables layered desserts, mousse cakes, and specialty pastries by providing smooth texture, stable structure, and premium presentation. Advances in stabilizers, preservation, and formulation technologies enhance shelf life and stability, supporting wider adoption in retail, foodservice, and frozen dessert applications. Foam toppings continue to grow steadily but at a slightly lower rate, complementing premium dessert trends without surpassing the growth trajectory of the gel segment.

Application Insights

Bakery products are projected to continue to dominate as the primary application for fillings and toppings in 2026, capturing roughly 42% of the total market demand. Baked goods including cakes, pastries, breads, donuts, and specialty bakery items consistently rely on creams, syrups, fruit-based fillings, and decorative toppings to enhance taste, appearance, and perceived value. The wide variety of bakery formats, from industrial-scale to artisanal and the steady demand for both every day and celebratory baked goods makes bakery the largest and most stable application segment.

On the growth front, dairy and frozen desserts are most likely to stand out as the fastest-growing application segment, with an expected CAGR of around 6% between 2026 and 2033. The massive global popularity of ice creams, frozen pastries, packaged dairy desserts, and convenience snacks, particularly in emerging markets, is driving this trend. Technological advances in formulation and preservation enable fillings and toppings to remain stable under freezing or refrigerated conditions, facilitating wider adoption even where cold-chain infrastructure is limited.

Regional Insights

North America Fillings & Toppings Market Trends

North America occupies a prime position, capturing around 27% of the fillings & toppings market share in 2026. High spending capacity, mature bakery and confectionery sectors, and strong consumer preference for indulgent, premium bakery and dessert products maintain steady demand. The U.S. drives the regional market, particularly for ready-to-eat bakery items, artisanal pastries, seasonal specialties, and frozen desserts. Well-established retail networks, convenience stores, supermarkets, and a broad foodservice ecosystem, including quick-service restaurants (QSRs) and cafes, ensure widespread product availability and consistent market penetration across urban and suburban areas.

Regional manufacturers are investing in innovation to develop clean-label, low-sugar, plant-based, and functional fillings in response to evolving consumer preferences and health trends. Expansion of manufacturing capacity, automation, and cold-chain logistics enables companies to serve domestic and export markets efficiently. The competitive landscape is moderately consolidated, with leading ingredient and filling suppliers emphasizing product quality, differentiation, and consistency.

Europe Fillings & Toppings Market Trends

Europe is expected to capture the largest share of the global fillings and toppings market in 2026, at an estimated 33%. This leadership is supported by strong consumer preferences, high per capita bakery consumption, and large urban populations. Mature bakery and confectionery markets in countries such as Germany, the United Kingdom, France, and Spain drive consistent demand for indulgent yet health-conscious products. Harmonized European Union (EU) regulations on food safety, labeling, and sugar reduction foster innovation, encouraging manufacturers to develop healthier, transparent, and functional fillings and toppings that meet evolving consumer expectations.

The expansion of modern retail, e-commerce, and foodservice channels in the region has broadened market reach, benefiting both premium and mass-market products. Sustainability trends, eco-conscious packaging, and ethical sourcing are also shaping product development strategies. Stable consumer demand, clear regulatory frameworks, and a willingness to pay for high-quality, innovative offerings position Europe as a strategic growth hub for the fillings and toppings industry. These factors attract both established companies and new market entrants seeking long-term opportunities in a dynamic and competitive landscape.

Asia Pacific Fillings & Toppings Market Trends

Asia Pacific is forecasted to achieve the fastest growth in the market for fillings & toppings, set to exhibit a CAGR of nearly 9% from 2026 to 2033, while capturing 30% market share in 2026. Rapid urbanization, increasing disposable incomes, shifting lifestyles, and greater acceptance of bakery, confectionery, dairy, and frozen dessert products fuel this expansion. Nations such as China, India, and ASEAN member-states demonstrate a rising demand for Western-style desserts, artisanal baked goods, and convenient snacks. The growth of modern retail outlets, supermarkets, convenience stores, and e-commerce platforms enables manufacturers to access urban and semi-urban consumers effectively. This distribution evolution can accelerate the adoption of premium and indulgent fillings and toppings across diverse demographics.

Local production benefits, including reduced labor expenses, plentiful raw materials, and expanding food processing facilities, draw both international and domestic manufacturers to the region. Strengthening food safety standards, labeling requirements, and quality controls promote investments in transparent and sustainable manufacturing processes. The competitive market structure supports development of customized, innovative, and health-oriented fillings tailored to various food categories. Companies that leverage these dynamics can secure strong positions by prioritizing localized formulations, agile supply chains, and partnerships with retail partners to meet evolving regional preferences.

Competitive Landscape

The global fillings & toppings market landscape is expected to be led by major players such as Cargill, Ingredion, Kerry Group, Puratos, Döhler, Barry Callebaut, and Bunge. These companies maintain strong market positions through extensive ingredient portfolios, advanced food processing capabilities, and established relationships with bakery, confectionery, and dairy manufacturers. Leadership is reinforced by product quality, consistent supply, and innovation in clean-label, plant-based, and functional fillings, catering to premium, health-conscious, and indulgent dessert segments.

Competition is increasingly influenced by regional and niche suppliers offering specialized, natural, and cost-effective formulations tailored to local tastes. Companies differentiate through innovation in texture, flavor, shelf stability, and formulation technologies, including gel, foam, and reduced-sugar products. Expansion of production in Asia Pacific, rising demand in emerging markets, and adoption of convenience and frozen dessert products drive continuous R&D and market expansion. This has enabled key players to meet evolving global consumer preferences and maintain competitiveness across bakery, confectionery, dairy, and convenience food sectors.

Key Industry Developments

- In June 2025, Fix Dessert Chocolatier launched “Time to Mango,” a white chocolate Dubai Chocolate bar filled with mango, passion fruit, and popping candy, positioned as a multi-sensory, nostalgia-infused experience in the UAE. The brand is leveraging strong regional enthusiasm for mango-flavoured, social media-friendly treats and its existing viral success with pistachio and kunafa-inspired chocolates to sustain momentum in premium, locally rooted confectionery innovation.

- In February 2025, Nestlé launched new KitKat tablets in Europe, featuring double chocolate, hazelnut, and salted caramel flavors with creamy fillings and marbled designs, to meet surging demand for indulgent, shareable chocolate. The launch was backed by a € 44.2 million investment in its Sofia factory producing 10,000-20,000 extra tons annually for 29 countries.

- In February 2025, Flowers Foods finalized the acquisition of Simple Mills for US$ 795 million, expanding its presence in the fast-growing “better-for-you” (BFY) snack segment. Simple Mills will continue to operate independently, allowing Flowers Foods to leverage its expertise in natural and plant-based ingredients while enhancing its portfolio of health-conscious bakery and dessert products.

Companies Covered in Fillings & toppings market Size, Share, and Growth Forecast 2026 - 2033

- Cargill

- Barry Callebaut

- Archer Daniels Midland Company

- Tate & Lyle

- AGRANA Beteiligungs‑AG

- Associated British Foods

- Ingredion Incorporated

- Puratos Group

- Olam International

- Sensient Technologies

- AAK AB

- Ashland Inc.

Frequently Asked Questions

The global fillings & toppings market is projected to reach US$ 31.2 billion in 2026.

Growing consumer preference for healthier, clean-label, and plant-based products, and expansion of retail channels are driving the market.

The market is poised to witness a CAGR of 4.3% from 2026 to 2033.

Plant-based and clean-label innovations, diversification into dairy and frozen desserts, and localized flavor development are key market opportunities.

Few of the key market players include Cargill, Ingredion, Kerry Group, Puratos, and Döhler.