- Testing, Inspection, & Certification

- File Integrity Monitoring Market

File Integrity Monitoring Market Size, Share, and Growth Forecast, 2026 - 2033

File Integrity Monitoring Market by Offering (Software, Services), Deployment (Cloud-based, On-premises), Enterprise Size (Large Enterprises, Small & Medium-sized Enterprises), Industry (BFSI, Healthcare, IT & Telecom, Retail & E-commerce, Manufacturing, Energy & Utilities, Government & Defense, Others), and Regional Analysis for 2026 - 2033

File Integrity Monitoring Market Size and Trends Analysis

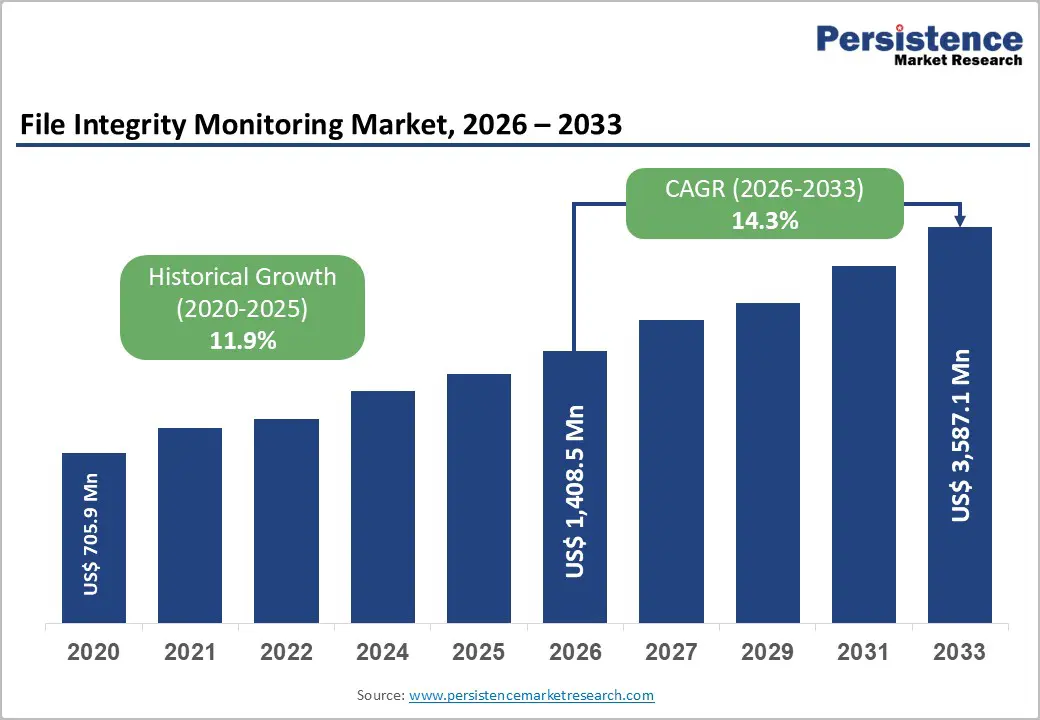

The global file integrity monitoring (FIM) market size is projected to rise from US$1,408.5 Mn in 2026 to US$3,587.1 Mn by 2033. We anticipate a 14.3% CAGR over the forecast period from 2026 to 2033, as organizations increasingly prioritize real-time detection of unauthorized changes to critical files, configurations, and sensitive data.

Escalating cybersecurity threats, including ransomware, malware, and insider attacks, are driving the demand for continuous monitoring solutions to prevent data breaches and ensure compliance. The growing adoption of cloud services, hybrid IT environments, and complex IT infrastructures has intensified the need for scalable and automated FIM solutions.

Key Industry Highlights:

- Leading Offering: Software dominates with over 68% market share in 2026, valued at more than US$ 957.8 Mn, driven by demand for scalable, automated monitoring, real-time alerts, ML-driven anomaly detection, and built-in compliance reporting. Services are the fastest-growing at 15.6% CAGR, fueled by the need for expert deployment, policy optimization, false-positive reduction, and 24/7 monitoring across hybrid and cloud environments.

- Leading Deployment: On-premises holds over 43% market share in 2026, valued at over US$605.7M, and is preferred for sensitive systems, regulatory compliance, and legacy infrastructure monitoring. Cloud-based deployment is growing fastest at a 18.7% CAGR, driven by scalability, reduced operational overhead, simplified onboarding, and seamless monitoring of containerized and serverless workloads.

- Leading Enterprise Size: Large enterprises hold more than 70% share in 2026, valued at over US$ 986 Mn, supported by sizable security budgets, regulatory mandates, and complex IT environments requiring comprehensive monitoring. SMEs are the fastest-growing segment at a 18.1% CAGR, adopting lightweight, automated FIM tools to address ransomware, insider threats, and compliance pressures.

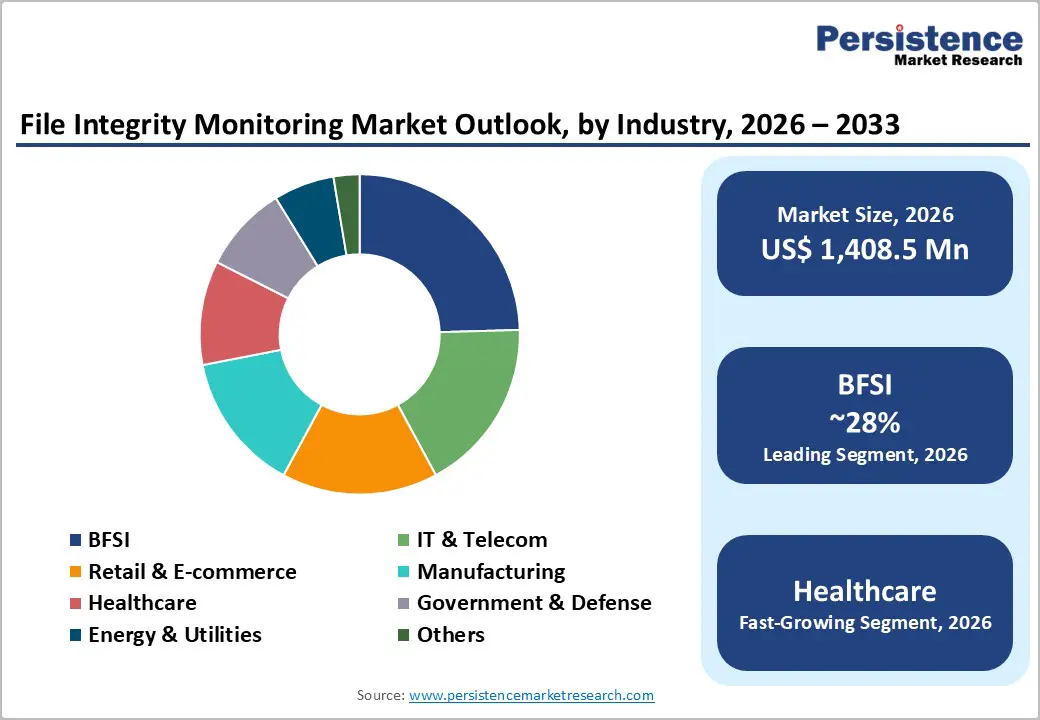

- Leading Industry: BFSI commands the largest market share at over 28% in 2026, valued at US$ 394.4 Mn, due to the need for protecting sensitive financial data and meeting strict compliance mandates like PCI-DSS and SOX. Healthcare grows fastest at 17.4% CAGR, driven by regulatory requirements, electronic health records protection, and rising ransomware and insider threat risks.

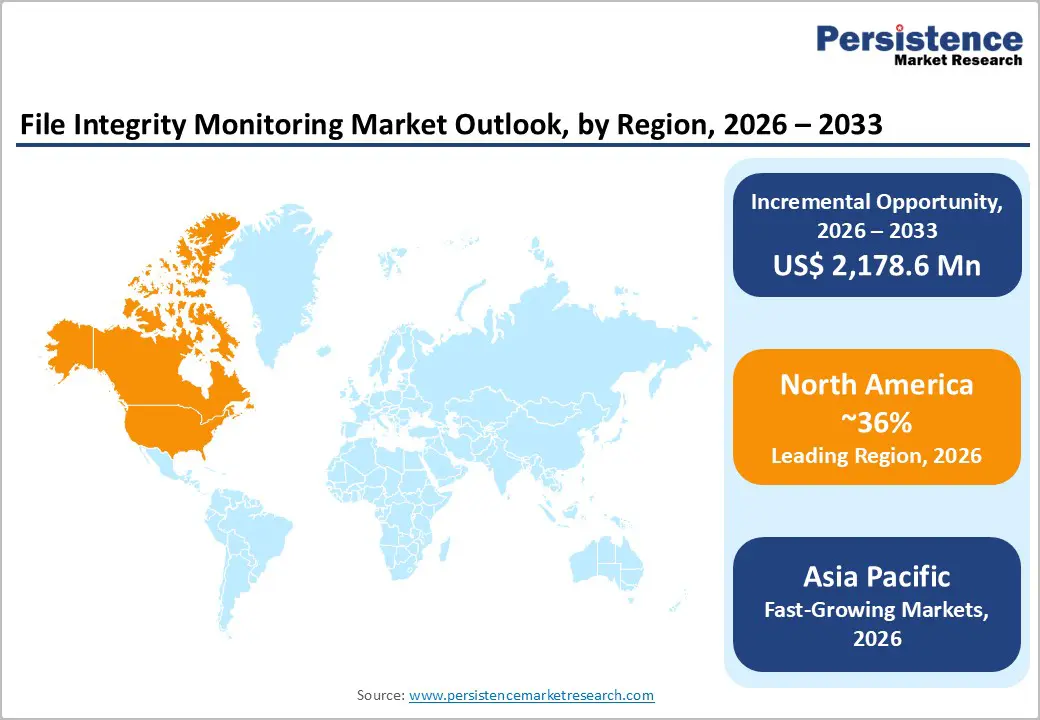

- Leading Region: North America leads with over 36% share in 2026, valued at US$ 507.1 Mn, driven by mature cybersecurity spending, regulatory mandates, and high ransomware incidents. Asia Pacific is growing fastest at 18.2% CAGR, fueled by digital transformation in China, India, Japan, and ASEAN economies. Europe holds over 24% share, supported by GDPR, NIS 2 Directive, and DORA compliance mandates.

| Global Market Attribute | Key Insights |

|---|---|

| File Integrity Monitoring Market Size (2026E) | US$1,408.5 Mn |

| Market Value Forecast (2033F) | US$3,587.1 Mn |

| Projected Growth (CAGR 2026 to 2033) | 14.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 11.9% |

Market Dynamics

Driver - Rise in Cybersecurity Threats and Rising Data Breach Incidents

The sharp rise in ransomware, malware, and advanced persistent threats (APTs) has exposed the limitations of perimeter-based security, thereby increasing reliance on continuous file-integrity monitoring. Growing insider threats, both malicious and accidental, further elevate the need for real-time detection of unauthorized changes to system files, configurations, and sensitive data. With average data breach costs running into several million dollars per incident, for example, IBM estimates that the global average cost of a data breach in 2025 reached approximately US$4.44 million. Enterprises are increasingly investing in FIM as a preventive control to support rapid forensic investigation, compliance, and executive-level risk mitigation.

Stringent Regulatory Compliance and Data Protection Mandates

Global regulations such as PCI-DSS, HIPAA, GDPR, SOX, and CCPA mandate continuous monitoring, tamper detection, and auditable change logs to protect sensitive data. For example, PCI DSS requires real-time monitoring of cardholder data systems, whereas HIPAA’s Security Rule mandates safeguards to detect unauthorized modification of ePHI. GDPR enforces accountability through DPIAs, with penalties of up to €20 million or 4% of global annual revenue for non-compliance. These mandates directly drive FIM adoption, as organizations require real-time change detection, forensic audit trails, and automated compliance reporting to demonstrate ongoing regulatory adherence.

Restraint - Implementation Complexity and Integration Challenges

File integrity monitoring deployments require deep technical expertise to define accurate baselines, configure policy rules, and integrate with SIEM and SOAR platforms across heterogeneous IT environments. Organizations frequently face integration friction when embedding FIM into existing security workflows, alongside high false-positive rates that generate alert fatigue and increase SOC workload. Configuration complexity often extends onboarding timelines and drives elevated professional services costs. These challenges are amplified in containerized and cloud-native environments, where traditional agent-based FIM models lack visibility, creating adoption barriers for mid-market enterprises with limited cloud security expertise.

Cost Constraints and Resource Limitations for SMEs

High upfront costs associated with FIM software licensing, professional deployment, and continuous tuning pose a significant barrier to adoption for SMEs with limited cybersecurity budgets. Unlike large enterprises, SMEs often lack in-house expertise to manage policy configuration, alert tuning, and SIEM integration, increasing reliance on costly managed services. According to a study, SMEs are significantly slower in adopting advanced security controls due to cost complexity trade-offs. This challenge is amplified in emerging markets, where shortages of skilled cybersecurity professionals further limit effective FIM implementation and operationalization.

Opportunity - Cloud-Native & Container-Focused FIM

Cloud-native and containerized environments are driving demand for modern file integrity monitoring solutions. With over 60% of enterprises deploying Kubernetes in 2024 and adoption expected to exceed 90% by 2027, traditional FIM tools built for static infrastructure are insufficient for ephemeral, immutable, and dynamically scaled containers. Purpose-built solutions now offer container image scanning, runtime integrity monitoring, and infrastructure-as-code policy enforcement across microservices and serverless architectures. Advanced technologies such as eBPF and agentless discovery enable real-time, low-overhead monitoring, addressing the unique challenges of modern, distributed cloud environments.

AI-Driven Anomaly Detection and Automated Response Capabilities

Integration of AI and machine learning into FIM solutions enhances detection accuracy, significantly reduces false positives, and automates response orchestration. By 2024, more than 40% of enterprises had adopted AI-enabled FIM capabilities for anomaly detection, materially reducing false positives and alert fatigue. Machine learning establishes behavioral baselines, identifies anomalies, and correlates file changes with user and network activity to distinguish malicious modifications. Automated response capabilities such as file quarantine, system isolation, and workflow triggering cut mean time to respond from hours to minutes, with detection-response times under five minutes reported across large IT infrastructures.

Category-wise Analysis

Offering Insights

Software dominates the global market, capturing more than 68% of the market share in 2026, with a value exceeding US$ 957.8 million, driven by enterprises' preference for scalable, automated, and feature-rich monitoring platforms over manual auditing. These solutions enable comprehensive change detection across distributed environments, provide real-time alerts, offer customizable baselines, and facilitate seamless SIEM integration for correlating file changes with security events and user activity. Advanced platforms further deliver built-in compliance reporting, automated remediation, and ML-driven anomaly detection, significantly reducing analyst workload and accelerating incident response.

Services are expected to grow at a 15.6% CAGR due to organizations' increasing need for expert-led deployment, configuration, and ongoing tuning of complex FIM environments. Enterprises require managed services to handle baseline creation, policy optimization, false-positive reduction, and integration with SIEM, SOAR, and cloud platforms. The rise of hybrid, multi-cloud, and containerized infrastructures is driving demand for continuous monitoring, compliance reporting, and 24/7 threat response support.

Deployment Insights

On-premises holds over 43% share in 2026, with a value exceeding US$605.7M, driven by enterprises’ need for direct control over sensitive systems and data. Highly regulated sectors require strict compliance, data sovereignty, and audit readiness, which on-prem solutions support more effectively. Organizations with legacy infrastructure and mission-critical workloads prefer on-prem FIM for deeper system visibility and low-latency monitoring. It aligns with internal security policies that restrict external data transmission and cloud dependency.

Cloud-based is expected to grow at the highest rate, with a 18.7% CAGR, as organizations prioritize deployment models that eliminate infrastructure overhead, provide instant scalability, and enable consistent monitoring across multi-cloud environments. It offers immediate value through simplified onboarding, automatic security updates, reduced operational complexity, and seamless integration with cloud-native workloads, including containerized applications and serverless functions. Cost-effectiveness advantages, including eliminating hardware investments, reducing physical security footprints, and transferring operational technology to managed service providers, continue to accelerate adoption.

Enterprise Size Insights

Large enterprises are expected to account for more than 70% in 2026, with a value exceeding US$986M, driven by large security budgets, strict regulatory compliance mandates, and highly distributed IT environments spanning multiple geographies. Their complex ecosystems, often involving thousands of servers, applications, and users, face elevated ransomware, insider threat, and audit risks, making comprehensive FIM solutions business-critical. Mature security operations centers and dedicated cybersecurity teams enable effective deployment, continuous monitoring, and incident response.

Small & medium-sized enterprises (SMEs) are expected to achieve a 18.1% CAGR, as they increasingly face ransomware, insider threats, and supply-chain-driven cyber risks that were previously concentrated among large enterprises. SMEs need affordable, automated FIM solutions to meet basic compliance requirements, protect critical business data, and detect unauthorized file changes without maintaining large security teams. Rising cloud adoption and remote work further increase the need for lightweight, easy-to-deploy monitoring tools. Growing regulatory pressure and customer security expectations are prompting SMEs to invest in foundational security controls, such as FIM.

Industry Insights

BFSI commands the largest market share at over 28% in 2026 with a value exceeding US$ 394.4 Mn, as financial institutions manage vast volumes of highly sensitive customer and transaction data that must be continuously protected against breaches and unauthorized changes. FIM is essential for meeting strict regulatory and compliance mandates, such as PCI DSS, SOX, and GDPR, which require robust monitoring and audit trails. The high frequency and sophistication of cyberattacks targeting financial systems make real-time integrity checks critical for risk mitigation and operational trust.

Healthcare is expected to grow at a 17.4% CAGR, driven by the urgent need to protect sensitive patient data and ensure uninterrupted clinical operations. Hospitals and healthcare providers manage electronic health records (EHRs), medical imaging files, and connected medical devices that are frequent targets of ransomware and insider threats. Strict regulatory requirements, such as HIPAA, and increasing data privacy mandates drive demand for continuous visibility into file changes and audit readiness. The rapid digitization of healthcare systems and the expansion of cloud-based health platforms heighten the need for real-time detection of unauthorized file modifications.

Regional Insights

North America File Integrity Monitoring Market Trends

North America holds over 36% share in 2026, reaching US$ 507.1 Mn value, driven by stringent regulatory mandates, mature enterprise security spending, and a large installed IT base. The U.S. leads adoption due to heightened cybersecurity awareness and compliance requirements under PCI DSS, HIPAA, FISMA, GLBA, along with evolving frameworks such as the FTC Safeguards Rule and SEC cybersecurity disclosures. According to CompTIA 2025 report, 81% of organizations prioritize cybersecurity, directly supporting sustained investment in core controls like FIM. The ~9% rise in ransomware complaints against U.S. critical infrastructure in 2024, noted by the FBI, reinforces demand for real-time file integrity detection. A strong innovation ecosystem, supported by venture capital access and concentrated security talent, further accelerates FIM product evolution and early enterprise adoption.

Asia Pacific File Integrity Monitoring Market Trends

Asia Pacific is expected to grow at the highest rate with a CAGR of 18.2%, driven by digital transformation across China, Japan, India, and ASEAN economies. Expanding IT infrastructure from semiconductor manufacturing, electronics assembly, and technology services increases demand for continuous file integrity monitoring and regulatory compliance. India’s growing tech sector and focus on data protection, China’s domestic and international FIM solutions addressing local regulations, and Japan’s mature infrastructure and strict compliance culture fuel adoption in government, healthcare, and financial services. ASEAN nations such as Malaysia, Singapore, Vietnam, and Thailand benefit from manufacturing relocation from China, creating new IT monitoring needs aligned with global OEM security standards.

Europe File Integrity Monitoring Market Trends

Europe is expected to hold more than 24% share by 2026, due to stringent regulatory frameworks such as GDPR, which mandates robust data protection measures, audit trails, and breach response procedures. The NIS 2 Directive, effective October 2024, expands cybersecurity obligations to medium and large organizations across essential sectors, enforcing incident reporting within 72 hours, supply chain security, and CEO-level accountability, with penalties up to €7 million or 1.4% of revenue. In the financial sector, DORA imposes ICT risk management, resilience controls, third-party vetting, and frequent vulnerability assessments, with fines up to 1% of daily revenue. The UK market, led by finance, government, and critical infrastructure, sees companies like Darktrace and Sophos embedding AI-driven FIM within broader security platforms.

Competitive Landscape

The file integrity monitoring market is moderately fragmented, with several established vendors and niche players competing to offer advanced security and compliance solutions, but in an increasingly consolidating competitive environment. Companies are focusing on differentiating through AI-augmented detection, real-time monitoring, and integration with broader cybersecurity platforms. Strategic partnerships, like collaborations with system integrators and cloud service providers, are leveraged to expand market reach and adoption. Vendors emphasize regulatory compliance support, scalability for large enterprises, and customization for industry-specific needs to gain a competitive edge. Continuous innovation and targeted marketing are central to sustaining growth in this evolving market.

Key Industry Developments

- In November 2025, Trend Micro is launching the Trend Vision One™ AI Security Package at AWS reInvent, offering proactive, AI-powered security across the entire AI application stack, including cloud, containers, and code. The package features File Integrity Monitoring (FIM) for Kubernetes and eBPF, real-time threat detection, risk insights, and zero-trust AI access to enhance runtime protection and compliance.

- In April 2025, Cimcor Inc. partnered with Al Moammar Information Systems Co. (MIS) to expand cybersecurity offerings in Saudi Arabia and the Middle East. The collaboration aims to deliver advanced system integrity monitoring and compliance solutions to government, financial, and enterprise sectors across the region.

Companies Covered in File Integrity Monitoring Market

- Tripwire, Inc.

- Qualys, Inc.

- Trend Micro Incorporated

- SolarWinds Worldwide, LLC

- LogRhythm, Inc.

- Splunk Inc.

- Cimcor, Inc.

- AT&T

- Trustwave Holdings, Inc.

- Zoho Corporation Pvt. Ltd.

- Netwrix Corporation

- BeyondTrust Corp.

- Ionx Solutions LLP

- Others

Frequently Asked Questions

The global file integrity monitoring market is projected to be valued at US$1,408.5 Mn in 2026.

The need for organizations to detect unauthorized file changes, ensure regulatory compliance, and protect sensitive data from cyber threats and insider risks is a key driver of the market.

The market is expected to witness a CAGR of 14.3% from 2026 to 2033.

Growing adoption of cloud-native environments, containerized applications, and AI-driven FIM solutions is creating strong growth opportunities.

Tripwire, Inc., Qualys, Inc., Trend Micro Incorporated, SolarWinds Worldwide, LLC, LogRhythm, Inc., Splunk Inc., Cimcor, Inc. are among the leading key players.