- Specialty & Fine Chemicals

- Ferric Chloride Market

Ferric Chloride Market Size, Share, and Growth Forecast, 2026 - 2033

Ferric Chloride Market by Grade (Liquid, Anhydrous, Hexahydrate Lumps), Application (Wastewater Treatment, Metal Surface Treatment, Others), End-use Industry (Municipal Wastewater Treatment, Pharmaceuticals, and Others), and Regional Analysis for 2026 - 2033

Ferric Chloride Market Size and Trends Analysis

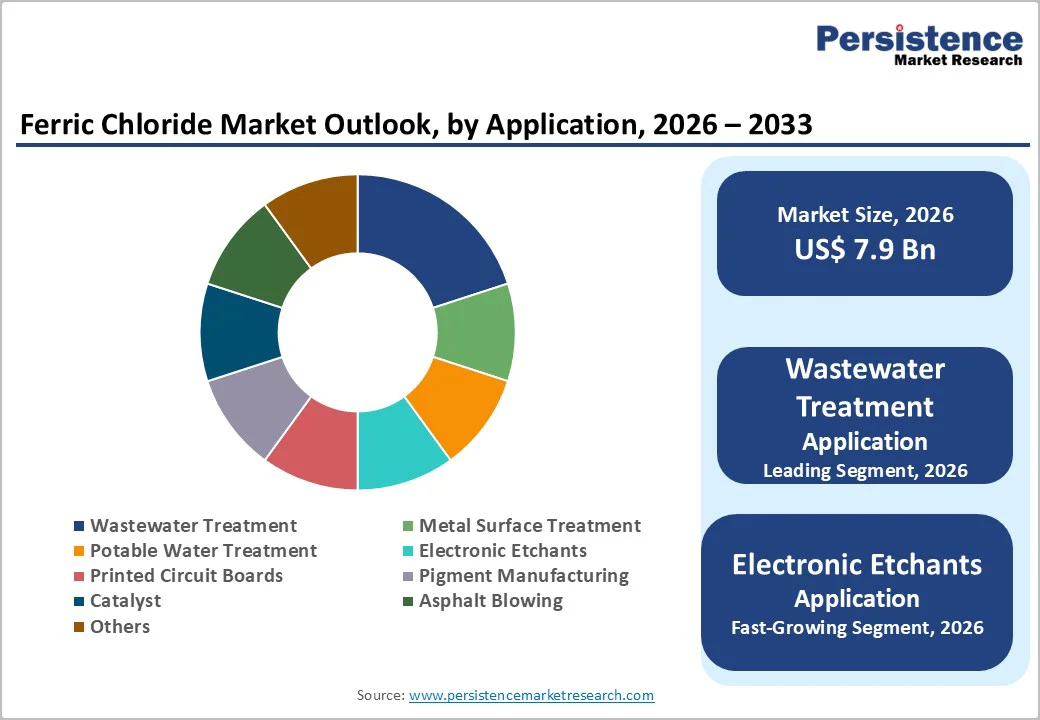

The global ferric chloride market size is likely to be valued at US$7.9 billion in 2026, and is expected to reach US$10.8 billion by 2033, growing at a CAGR of 4.5% during the forecast period from 2026 and 2033, driven by the increasing prevalence of water purification needs, rising demand for coagulants in wastewater treatment, and advancements in high-purity etching solutions.

Rising demand for stable, eco-friendly ferric chloride in electronics and pharmaceuticals, coupled with advances in liquid and hexahydrate formulations and its role in sustainable industrial processes in emerging regions, is driving rapid market growth.

Key Industry Highlights:

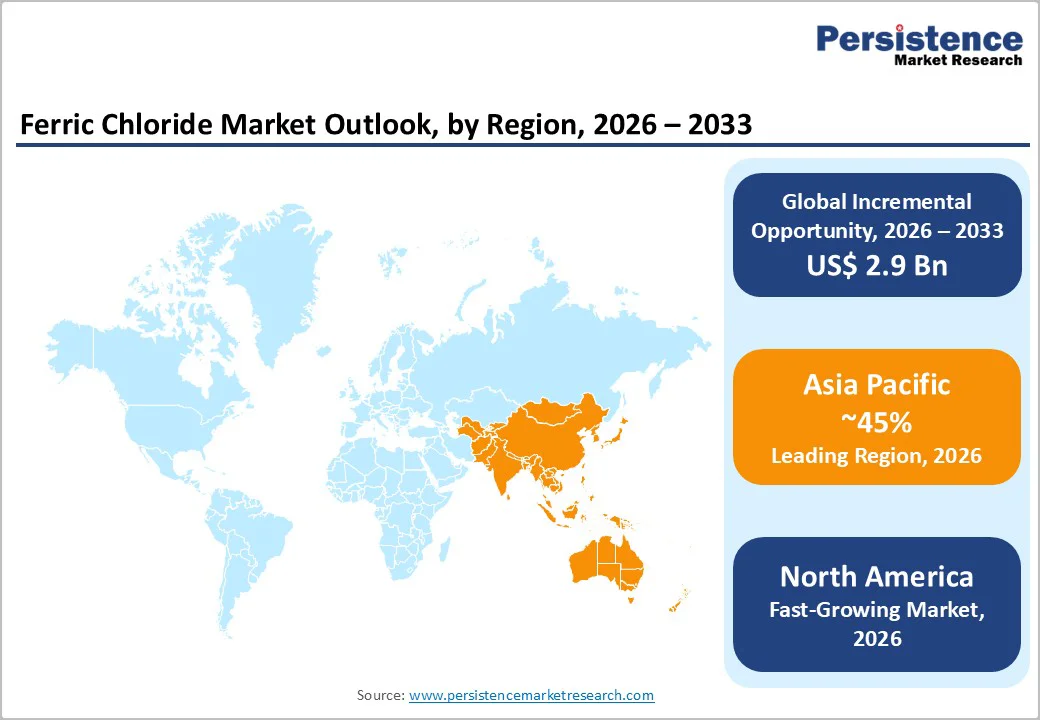

- Leading Region: Asia Pacific, anticipated to account for a 45% market share in 2026, driven by rapid industrialization, expanding water infrastructure, and robust electronics manufacturing in China and India.

- Fastest-growing Region: North America is likely to be the fastest-growing region between 2026 and 2033, due to accelerating digital adoption, strong investments in advanced technologies, and rapid enterprise shifts toward cloud-native, AI-driven security architectures.

- Dominant Grade: Liquid is anticipated to hold approximately 60% of the market share in 2026, as it generates strong solubility and ease of dosing by closely mimicking fluid handling needs.

- Leading Application: Wastewater treatment is expected to account for over 20% of the market revenue, due to coagulation efficiency, regulatory mandates, and widespread use in effluent purification.

- Leading End-use Industry: Municipal wastewater treatment is projected to contribute nearly 40% of the market revenue in 2026, due to its scalable infrastructure, trained operators, and capacity to handle urban effluents.

| Key Insights | Details |

|---|---|

|

Ferric Chloride Market Size (2026E) |

US$7.9 Bn |

|

Market Value Forecast (2033F) |

US$10.8 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Demand for Ferric Chloride Coagulants in Water and Wastewater Treatment

The rising preference for water purification needs is quickly becoming a major opportunity for chemical suppliers, driven by growing regulatory demand for clean effluents and reduced contamination. Traditional flocculants often create sludge buildup, especially in municipal plants, leading to higher disposal costs and lower efficiency. Coagulant technologies, including ferric chloride liquids, anhydrous powders, hexahydrate lumps, pH-adjusted solutions, and chelated variants, address these concerns by offering a robust, multi-valent alternative. These formats simplify dosing, reduce the need for secondary polymers, and are particularly effective during peak flows or industrial surges where rapid clarification is critical.

Ferric chloride significantly lowers the risk of turbidity breakthrough, heavy metal leaching, and odor formation, which remain major concerns in treatment settings. They also support improved settling and easier dewatering, especially for liquid and lump grades, making them ideal for urban or remote facilities. As global environmental organizations push for wider effluent coverage and user-friendly chemicals, demand continues to expand across potable treatment, electronics etching, and pigment manufacturing.

High Development and Purification Costs

High development and purification costs present a significant barrier for companies advancing next-generation ferric chloride and novel coagulant systems. Developing innovative grades such as ultra-pure liquids, anhydrous crystals, or hexahydrate blends requires extensive research, specialized electrolysis, and advanced filtration technologies that are far more expensive than technical ferric chloride. Purity is an even greater challenge: many refined variants, trace-impurity reduced lots, and stabilizer-enhanced products are sensitive to hydrolysis, temperature, and oxidation, requiring rigorous optimization to ensure they remain stable throughout storage and application. Achieving regulatory compliance often involves costly bioassays, sophisticated ICP-MS testing, and the use of high-grade precipitants, which significantly increase R&D expenditures.

Meeting stringent regulatory expectations for arsenic limits, microbial controls, and batch uniformity requires multiple stability studies under various conditions and across several production batches. This adds both time and financial burden to development timelines. Scaling up manufacturing requires controlled reactors, specialized dryers, and quality-assurance systems, further driving up overall costs. For smaller processors, these challenges can limit grade expansion or delay commercialization.

Advancements in Eco-Friendly and High-Purity Delivery Platforms

Advancements in eco-friendly and high-purity ferric chloride delivery platforms are transforming the global treatment landscape by addressing two major challenges, sludge generation and impurity risks. Eco-friendly ferric chloride is engineered to achieve low-dose efficacy, reducing reliance on over-application and enabling sludge-minimized operations in wastewater plants. Innovations, such as polymer-augmented liquids, bio-derived precipitants, crystal engineering, and hybrid coagulants, significantly improve settling rates and reduce residuals, lowering disposal costs for municipalities and industrial campaigns.

Progress in high-purity platforms, including electronic-grade etchants, pharma-buffered solutions, solid lumps, and catalyst precursors, supports more precise reactions by stimulating ion exchange, the process’s first line of defense against defects and byproducts. These formats eliminate contaminants, enhance yield, and allow automated dosing without skilled operators, making them highly suitable for mass purification programs. New technologies such as nano-encapsulated chlorides, mucoadhesive polymers, and VLP-based flocculants further enhance coagulation and etching response.

Category-wise Analysis

Grade Insights

The liquid segment is anticipated to dominate, accounting for approximately 60% of the market share in 2026. Its dominance is driven by superior flowability, dosing precision, and stability, making it preferred for wastewater coagulation. Liquid ferric chloride provides rapid flocculation, ensures efficacy, and contributes to sludge reduction, making it suitable for large-scale treatment campaigns. For example, the EPA notes that ferric chloride is commonly used as a coagulant in municipal wastewater treatment processes to react with phosphate and suspended solids, forming insoluble compounds that settle out of the water during primary and secondary treatment stages. This chemical dosing step helps improve clarification and reduce pollutant loads before discharge or further biological treatment.

Hexahydrate lumps are likely to be the fastest-growing segment due to their compact form and increasing use in electronics etching. Their crystalline structure allows for precise dissolution, minimizing waste, while ongoing advancements in lump purification are enhancing their quality and boosting adoption across North America and Europe, where demand for dry, transportable grades is rising. For instance, the U.S. National Institutes of Health (NIH)/PubChem notes ferric chloride’s role as an etching agent in PCB manufacturing, where solid hexahydrate lumps are dissolved to accurately remove copper without excessive application.

Application Insights

Wastewater treatment is anticipated to lead the market, driven by persistent effluent challenges, large municipal programs, and strong global demand for coagulants. Their dominance continues as operators expand treatment for industrial discharges and urban runoff. Rising adoption of metal surface treatments and expanded potable campaigns highlight the growing focus on comprehensive purification. For example, the U.S. Environmental Protection Agency (EPA) states that ferric chloride is the most common inorganic coagulant used in the wastewater treatment industry and is widely applied for phosphate removal in municipal wastewater effluent, especially under regulations such as the Clean Water Act aimed at protecting sensitive waters (Great Lakes, Chesapeake Bay). This reflects its dominant role in large municipal wastewater programs and compliance-driven treatment upgrades.

Electronic etchants are likely to be the fastest-growing segment between 2026 and 2033, due to strong momentum in PCB fabrication and expanding inclusion of high-purity ferric chloride in semiconductors. The growing shift toward compact, defect-free platforms, along with better copper selectivity, accelerates the adoption. Advancements in anhydrous etchants and the continued progress of lump-based solutions entering pilot trials drive market growth. For example, Ferric chloride is used for electronic and photographic etching, metal surface treatment, and as a catalyst in chemical reactions for products such as vinyl chloride, confirming that its role in electronics manufacturing is recognized at the regulatory level as a key industrial application beyond water treatment.

End-use Industry Insights

Municipal wastewater treatment is likely to dominate the market, with approximately 40% share in 2026, due to the high volume of urban effluents and strong global emphasis on discharge compliance. Regular coagulation schedules, regulatory requirements, and widespread access to dosing systems drive consistent demand. Rising focus on chemical processing and electronics further strengthens municipal leadership. For example, the U.S. EPA states that ferric chloride is widely used as a coagulant in municipal wastewater treatment to remove suspended solids and precipitate contaminants, making it a core chemical in urban effluent processing and clarifying wastewater before discharge. Water treatment is cited as the primary commercial use of ferric chloride in the U.S., with most consumption going toward wastewater applications driven by regulatory standards.

The pharmaceuticals segment is expected to be the fastest-growing sector, driven by the increasing demand for pure buffers, sensitivity to impurities, and the rising adoption of chelated agents. Enhanced safety profiles, precise concentration options, and improved solubility for oral applications support rapid market uptake. Expanding use in potable treatments, catalysts, and other health-focused applications further fuels growth. For instance, ferric chloride hexahydrate is recognized as a pharmaceutical raw material with official quality standards in major pharmacopeias, including the British Pharmacopoeia (BP), European Pharmacopoeia (Ph. Eur.), and United States Pharmacopeia (USP), which provide detailed monographs and specifications to ensure high-purity grades suitable for pharmaceutical synthesis and medicinal uses.

Regional Insights

North America Ferric Chloride Market Trends

North America is projected to be the fastest-growing region, driven by accelerating digital adoption, strong investments in advanced technologies, and rapid enterprise shifts toward cloud-native, AI-driven security architectures. Treatment systems in the U.S. and Canada provide extensive support for coagulation programs, ensuring wide accessibility of ferric chloride across wastewater, potable, and electronics populations. Increasing demand for liquid, convenient, and easy-to-dose forms is further accelerating the adoption, as these formats improve efficiency and reduce barriers associated with solids.

Innovation in ferric chloride technology, including stable purities, improved flocculation delivery, and targeted impurity removal, is attracting significant investments from both public and private sectors. Government initiatives and clean water campaigns continue to promote use against industrial discharges, algal blooms, and emerging contaminant threats, creating sustained market demand. The growing focus on anhydrous grades and metal treatments, particularly for chemicals and metallurgy, is expanding the target applications for ferric chloride. For example, the New York City DEP uses ferric chloride in its wastewater treatment plants to reduce phosphorus levels and meet effluent discharge requirements, directly illustrating municipal wastewater operations leveraging ferric chloride for regulatory compliance and environmental protection.

Europe Ferric Chloride Market Trends

Europe is projected to lead with a market share of 20% in 2026, driven by increasing awareness of treatment benefits, strong infrastructure systems, and government-led purification programs. Countries such as Germany, France, and the U.K. have well-established environmental frameworks that support routine coagulation and encourage the adoption of innovative ferric chloride delivery methods. These reliable formulations are particularly appealing for municipal populations, cost-averse operators, and electronics users, improving compliance and coverage rates.

Technological advancements in ferric chloride development, such as enhanced stability, etchant-targeted delivery, and improved eco-grades, are further boosting market potential. European authorities are increasingly supporting research and trials for chemicals against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, automated dosing options is aligned with the region’s focus on preventive treatment and reducing sludge volumes. Public awareness campaigns and effluent drives are expanding reach in both urban and rural areas, while suppliers are investing in catalysts and novel purities to increase efficacy.

Asia Pacific Ferric Chloride Market Trends

Asia Pacific is anticipated to lead, accounting for approximately 45% of the share in 2026, driven by rising purification awareness, increasing government initiatives, and expanding application programs across the region. Countries such as India, China, Japan, and Southeast Asian nations are actively promoting treatment campaigns to address industrial effluents and emerging potable needs. Ferric chloride is particularly attractive in these regions due to its cost-effective dosing, ease of scaling, and suitability for large-scale coagulation drives in both urban and rural populations.

Technological advancements are supporting the development of stable, effective, and easy-to-handle ferric chloride, which can withstand challenging climatic conditions and minimize sludge dependence. These innovations are critical for reaching remote plants and improving overall effluent coverage. Growing demand for wastewater, electronics, and metallurgy applications is contributing to market expansion. Public-private partnerships, increased chemical expenditure, and rising investment in purification research and manufacturing capacity are further accelerating growth. The convenience of ferric chloride delivery, combined with improved flocculation and reduced risk of overflows, positions ferric chloride as a preferred choice.

Competitive Landscape

The global ferric chloride market features competition between established chemical leaders and emerging regional producers. In North America and Europe, Kemira Oyj and BASF SE lead through strong R&D, distribution networks, and treatment ties, bolstered by innovative grades and purification programs. In Asia Pacific, Feralco AB advances with localized solutions, enhancing accessibility. Coagulant delivery boosts efficiency, cuts sludge risks, and enables mass treatments across regions. Strategic partnerships, collaborations, and acquisitions merge expertise, expand capacities, and speed commercialization. High-purity formulations solve compliance issues, aiding penetration in regulated areas.

Key Industry Developments

- In July 2024, Kemira Oyj announced an investment in expanding its ferric chloride capacity in Tarragona, Spain, to enable production of specific biogas products, BDP (Biogas Digestion Product). This investment will enable Kemira to respond to the growing market demand for biogas applications in Europe. Ferric chloride is also the most used coagulant for phosphorus reduction in wastewater treatment.

Companies Covered in Ferric Chloride Market

- Kemira Oyj

- BASF SE

- Feralco AB

- PVS Chemicals Inc.

- Kem One

- Gulbrandsen AS

- Malay-Sino Chemical Industries Sdn Bhd

- Tessenderlo Group NV

- Feracid S.A.

- BorsodChem MCHZ Ltd.

- BPS Products Pvt Ltd.

- Asia Chemicals

- Sidra Wasserchemie

- Chemifloc Ltd.

- AkzoNobel Industrial Chemicals B.V.

- National Biochemicals

Frequently Asked Questions

The global ferric chloride market is projected to reach US$7.9 billion in 2026.

The rising prevalence of water purification needs and demand for coagulants in wastewater treatment are key drivers.

The ferric chloride market is poised to witness a CAGR of 4.5% from 2026 to 2033.

Advancements in eco-friendly and high-purity delivery platforms are the key opportunities.

Kemira Oyj, BASF SE, Feralco AB, PVS Chemicals Inc., and Tessenderlo Group NV are the key players.