- Specialty & Fine Chemicals

- Ferric Hydroxide Market

Ferric Hydroxide Market Size, Share, and Growth Forecast 2025 - 2032

Ferric Hydroxide Market by Product Form (Solid, Slurry), Application (Adsorbent, Coloring Agent, Flocculant, Other), Industry (Paints & Coatings, Construction, Wastewater treatment, Cosmetics, Pharmaceuticals, Other), and Regional Analysis for 2025 - 2032

Ferric Hydroxide Market Size and Trend Analysis

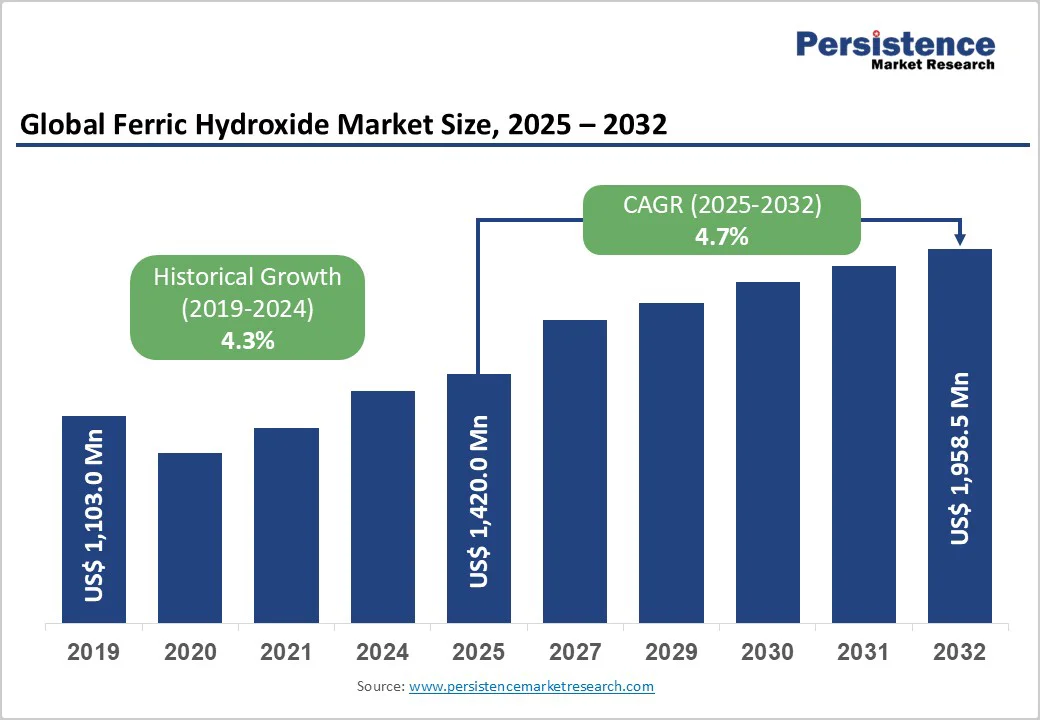

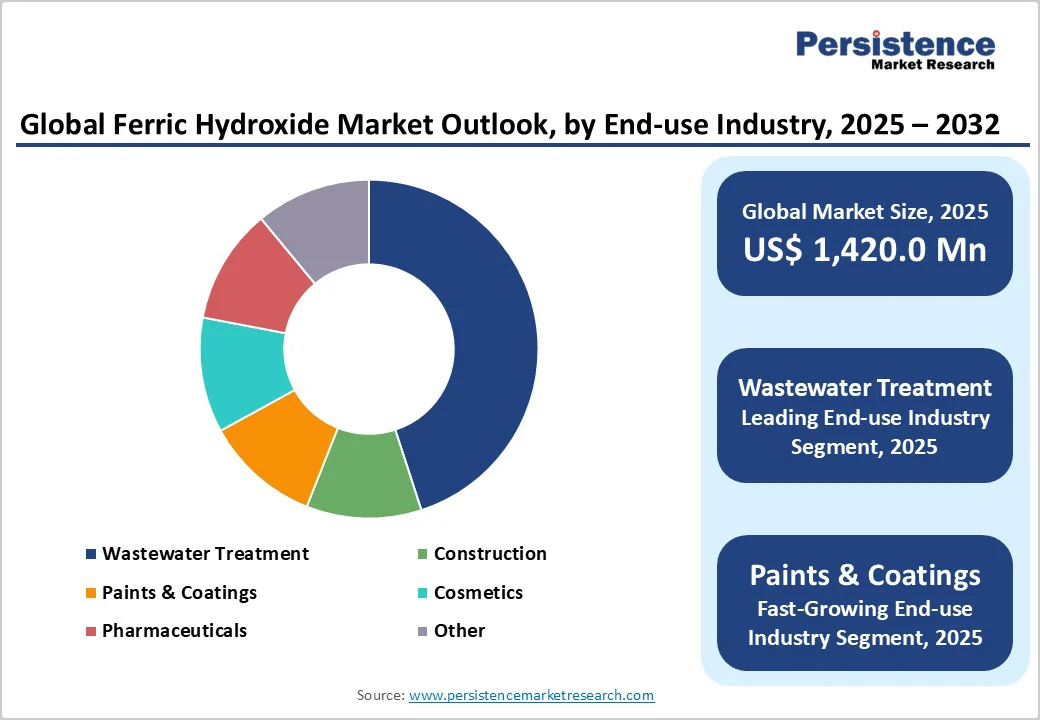

The global ferric hydroxide market size is likely to value at US$ 1,420.0 million in 2025 and is projected to reach US$ 1,958.5 million by 2032, growing at a CAGR of 4.7% between 2025 and 2032. This growth is primarily driven by increasing demand in water treatment and industrial applications, supported by stringent environmental regulations worldwide. Rising infrastructure development and the need for effective wastewater management further bolster the market, as ferric hydroxide's adsorption properties make it essential for removing contaminants like arsenic and heavy metals.

Key Market Highlights:

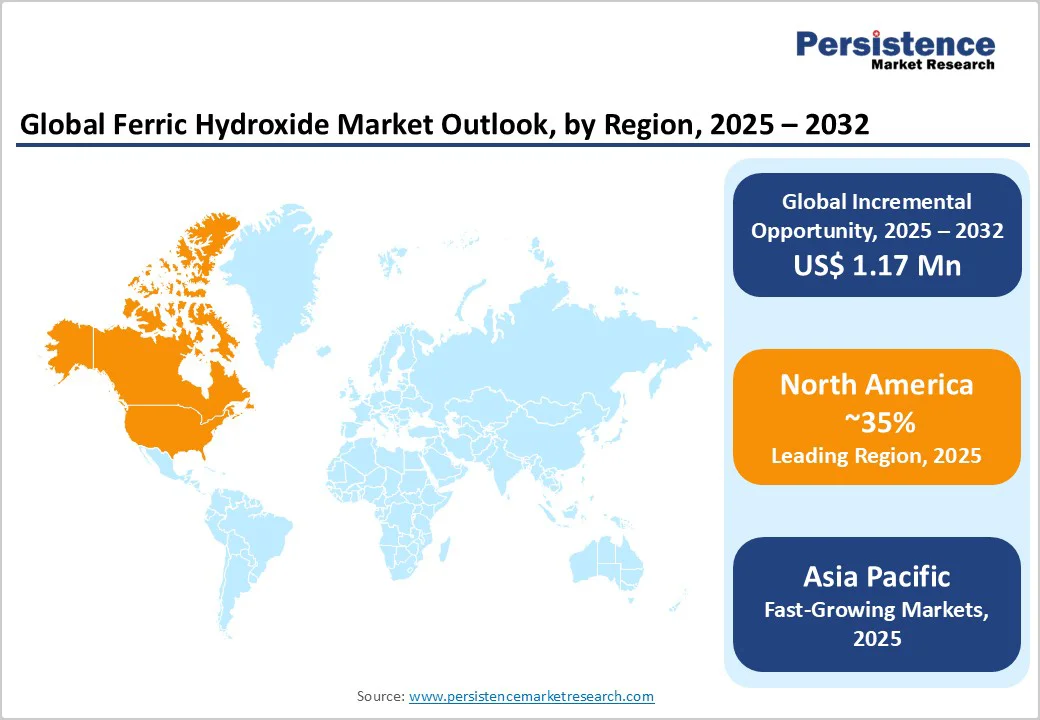

- Regional Leader: North America dominates the Ferric Hydroxide Market, with around 35% market share, due to stringent EPA regulations and advanced water infrastructure, ensuring high adoption in treatment and pigments.

- Fastest Growing Region: Asia Pacific emerges as the fastest-growing region, fueled by China's manufacturing scale and India's urbanization, projecting 7% annual expansion.

- Leading Segment: The Solid product form leads segments with 60% share, preferred for stability and logistics in global supply chains across industrial applications.

- Fastest Growing Segment: Slurry form grows fastest, driven by on-site dosing needs in large wastewater plants for efficient contaminant removal.

- Growth Opportunities: Sustainable water purification offers key opportunities, with innovations in adsorbents tapping into global scarcity challenges.

| Key Insights | Details |

|---|---|

|

Ferric Hydroxide Market Size (2025E) |

US$ 1,420.0 Mn |

|

Market Value Forecast (2032F) |

US$ 1,958.5 Mn |

|

Projected Growth CAGR (2025-2032) |

4.7% |

|

Historical Market Growth (2019-2024) |

4.3% |

Market Dynamics

Driver - Increasing Demand for Wastewater Treatment

The demand for ferric hydroxide in wastewater treatment is surging due to global efforts to combat water pollution, with governments enforcing stricter discharge standards. For instance, the U.S. Environmental Protection Agency (EPA) reports that over 40% of the U.S. rivers and streams fail to meet water quality standards, necessitating the use of advanced coagulants, such as ferric hydroxide, for removing phosphates and heavy metals. This driver's impact is evident in the Water & Wastewater Treatment Chemicals Market, where ferric hydroxide's high adsorption capacity reduces arsenic levels below 5 μg/L in drinking water, as demonstrated in EPA-approved filtration systems.

According to the World Health Organization (WHO), approximately two billion people lack access to safely managed drinking water, amplifying the urgency for advanced treatment solutions. The industrial sectors, such as chemicals and pharmaceuticals, are increasingly adopting it, ensuring cleaner effluents and compliance with regulations like the Clean Water Act. This not only mitigates environmental risks but also supports sustainable development, positively influencing market expansion.

Rising Applications in Paints and Coatings

Ferric hydroxide's use as a pigment in paints and coatings is accelerating market growth, driven by the construction boom in emerging economies. The Paints and Coatings Market benefits from its properties for producing durable, UV-resistant earthy tones, with global construction output expected to rise by 3.5% annually through 2030, according to the International Council on Clean Transportation. In applications like concrete and roofing, it enhances color fastness and corrosion resistance, reducing maintenance costs by up to 20%.

Data from the United Nations indicates that urban populations will rise by 2.5 billion by 2050, driving investments in building materials. Ferric hydroxide's cost-effectiveness compared to organic alternatives ensures its preference in large-scale projects, particularly in the Asia Pacific, where construction output is projected to grow robustly. This versatility across residential and industrial coatings fosters innovation, directly boosting demand and reinforcing ferric hydroxide's role in the expanding architectural sector.

Restraint - Volatility in Raw Material Prices

Fluctuations in iron ore and chemical precursor prices pose a significant challenge to the ferric hydroxide market, impacting production costs and profitability. Iron ore prices surged by 25% in 2024 due to supply chain disruptions from geopolitical tensions, as noted by the World Steel Association, making it difficult for manufacturers to maintain stable pricing. This volatility discourages investment in large-scale production, particularly in developing regions where input costs can rise by 15-20% annually. Consequently, smaller players face margin erosion, limiting market penetration and slowing overall growth.

Stringent Health and Safety Regulations

Health concerns related to improper handling of ferric hydroxide, such as potential skin irritation and inhalation risks, hinder market adoption. The Occupational Safety and Health Administration (OSHA) mandates strict protocols, with fines up to $14,502 per violation in 2025, increasing operational burdens for end-users in pharmaceuticals and cosmetics. Reports from the National Institute for Occupational Safety and Health (NIOSH) indicate that prolonged exposure can lead to respiratory issues, prompting cautious procurement and higher compliance costs, which negatively affect market dynamics.

Opportunity - Advancements in Sustainable Water Purification Technologies

Market participants can capitalize on innovations in eco-friendly water treatment, where ferric hydroxide-based granular adsorbents offer high efficiency in removing contaminants. The EPA has approved granular ferric hydroxide for arsenic remediation, achieving removal rates over 95% in pilot projects across the U.S., as per 2024 field trials. With global water scarcity affecting 2.4 Bn people according to the United Nations, demand for such technologies is projected to grow at 6% annually, particularly in the Water & Wastewater Treatment Chemicals Market. Companies investing in nanotechnology-enhanced formulations can tap into government grants, like the EU Green Deal funding of €1 billion for clean water initiatives, creating significant revenue potential through exports to Asia and Africa.

Expansion in Emerging Construction Markets

Opportunities abound in the construction sector of Asia, where ferric hydroxide is increasingly used for pigment production in infrastructure projects. For instance, China's Belt and Road Initiative has spurred $1 trillion in investments by 2030, driving demand for durable coatings, as reported by the Asian Development Bank.

In India, urban development plans aim to build 100 smart cities, boosting pigment needs by 8% yearly, according to the Ministry of Housing and Urban Affairs. Firms focusing on slurry forms for on-site applications can leverage low-cost manufacturing in the region, aligning with policies like India's Make in India for local sourcing, thus unlocking substantial growth in end-uses such as construction and paints.

Category-wise Insights

Product Form Analysis

The Solid segment leads the product form category in the Ferric Hydroxide Market, commanding approximately 60% market share. This dominance stems from its stability, ease of storage, and transportation advantages over slurry forms, making it ideal for global supply chains. According to industry data from the European Chemical Industry Council (CEFIC), solid ferric hydroxide reduces logistics costs by 15-20% due to lower moisture content, facilitating widespread use in paints and wastewater applications. Its longer shelf life and minimal spillage risks further justify its preference, as evidenced by adoption rates in U.S. manufacturing facilities where solid variants handle 70% of pigment production needs.

Application Analysis

The Flocculant segment dominates the application category, holding about 35% market share in the Ferric Hydroxide Market. This leadership is driven by its critical role in wastewater treatment, where it effectively aggregates suspended particles for sedimentation, achieving up to 90% removal efficiency as per EPA guidelines on coagulation processes.

In industrial settings, flocculants based on ferric hydroxide are preferred for their cost-effectiveness and compliance with discharge norms, supporting applications in over 50% of municipal plants globally. Data from the International Water Association underscores its superiority in handling high-turbidity waters, solidifying its position amid rising pollution controls.

Industry Analysis

The Wastewater Treatment segment leads the Industry category, capturing roughly 45% market share in the Ferric Hydroxide Market. Its prominence arises from the compound's exceptional adsorption capabilities for heavy metals and phosphates, essential for meeting global standards like the EU Water Framework Directive.

The World Health Organization (WHO) reports that untreated wastewater affects 80% of the global supply, driving adoption in treatment facilities where ferric hydroxide reduces contaminant levels by 95%. This segment's growth is further supported by investments in sustainable infrastructure, positioning it as a cornerstone for environmental compliance across industries.

Regional Insights

North America Ferric Hydroxide Trends

North America exhibits robust trends in the Ferric Hydroxide Market, led by the U.S.'s advanced regulatory framework under the EPA, which mandates arsenic removal below 10 μg/L in drinking water. Innovations in granular ferric hydroxide filters have enabled utilities to treat over 1,000 million gallons daily, as per 2024 EPA assessments, fostering an ecosystem of R&D collaborations with universities. The region's focus on sustainable practices, including the Infrastructure Investment and Jobs Act, which allocates $55 billion for water systems, enhances market dynamics by promoting ferric hydroxide in remediation projects.

Market growth is further propelled by pharmaceutical applications, where ferric hydroxide supports iron supplementation therapies amid rising anemia cases, affecting 20% of the population according to the Centers for Disease Control and Prevention (CDC). Expansion in the Water & Wastewater Treatment Chemicals Market underscores this, with companies investing in automated dosing systems for efficiency.

Europe Ferric Hydroxide Trends

Europe's Ferric Hydroxide Market is characterized by strong performance in Germany, the U.K., France, and Spain, harmonized under REACH regulations ensuring chemical safety and environmental protection. Germany's leadership in wastewater infrastructure, treating 95% of urban sewage per the European Environment Agency (EEA), relies on ferric hydroxide for phosphate removal, aligning with the Urban Wastewater Treatment Directive. Recent developments include France's €2 billion investment in green chemicals, boosting pigment use in coatings.

Regulatory harmonization facilitates cross-border trade, with the U.K. post-Brexit adopting similar standards to maintain supply chains. The Paints and Coatings Market in Spain benefits from ferric hydroxide's eco-profile, supporting EU goals to reduce emissions by 55% by 2030, driving consistent regional demand.

Asia Pacific Ferric Hydroxide Trends

Asia Pacific's Ferric Hydroxide Market is experiencing dynamic growth, with China dominating through manufacturing advantages and large-scale water projects under the South-North Water Transfer Project, treating 30 billion cubic meters annually, as reported by the Ministry of Ecology and Environment. India's rapid urbanization, adding 300 million city dwellers by 2030 per the United Nations, fuels demand in construction pigments, leveraging low production costs.

Japan and ASEAN nations like Indonesia emphasize ASEAN growth dynamics, with Japan's Ministry of the Environment promoting ferric hydroxide in advanced filtration amid aging infrastructure. China's export surge of iron-based chemicals by 5% in 2024 supports regional hubs, enhancing affordability and market penetration in the Ferric Chloride Market-related applications.

Competitive Landscape

The Ferric Hydroxide Market exhibits a moderately consolidated structure, with top players like Lanxess, BASF SE, and Huntsman Corporation controlling through integrated supply chains and R&D investments. Expansion strategies focus on capacity enhancements and partnerships for sustainable production, such as bio-based precursors to meet EU Green Deal standards. Key differentiators include high-purity formulations for pharmaceuticals and customized slurry dosing for water treatment. Emerging trends involve circular economy models, recycling spent adsorbents, and digital twins for process optimization, enabling leaders to capture premium segments while mid-tier firms target regional niches.

Key Market Developments:

- September 2024: LANXESS wins ICIS Innovation Award for innovative LFP battery materials using high-quality iron oxides derived from ferric hydroxide processes.

- January 2024: LANXESS partners with IBU-tec to develop iron oxides for lithium iron phosphate (LFP) cathodes, enhancing sustainable battery production.

- April 2023: Cathay Industries completes acquisition of Venator's iron oxide pigments business, expanding global pigment capacity by 20%.

Top Companies in Ferric Hydroxide Market

Lanxess (Germany) leads with a diverse portfolio in inorganic chemicals, emphasizing sustainable iron-based pigments and water treatment solutions. In 2024, advancements in LFP materials are enhancing market influence, with R&D investments surpassing 5% of sales.

BASF SE (Germany) excels in high-volume production of ferric compounds for coatings and pharmaceuticals, leveraging global facilities for cost efficiency. Its focus on eco-friendly processes positions it as a mature player in regulatory-compliant applications.

Huntsman Corporation (USA) specializes in performance additives, using ferric hydroxide in advanced flocculants for industrial uses. Its portfolio strength and U.S.-centric operations emphasize acquisitions for expanded end-use reach.

Companies Covered in Ferric Hydroxide Market

- Lanxess

- Huntsman Corporation

- Ferro Corporation

- BASF SE

- Xiamen Hisunny Chemical Co., LTD

- Yipin Pigments

- Cathay Industries

- Shenghua Group Deqing Huayuan Pigment Co.Ltd

- Harold Scholz & Co. GmbH

- Kings International

- SIOF s.p.a.

- Jinhe Enterprise Co.,Limited

- Jiangsu Yuxing Industry and Trade Co.,Ltd

- DuPont

- American Elements

Frequently Asked Questions

The Ferric Hydroxide Market is valued at US$ 1,420.0 Mn in 2025 and expected to reach US$ 1,958.5 Mn by 2032, growing at 4.7% CAGR.

Key drivers include stringent wastewater regulations and rising paints demand, with EPA standards boosting adsorption uses by 20%.

The Solid form leads with 60% share, favored for stability in storage and transport across global applications.

North America leads due to robust EPA regulations and infrastructure investments supporting water treatment dominance.

Sustainable water technologies offer growth, with granular adsorbents targeting arsenic removal in emerging markets at 95% efficiency.

Major players include Lanxess, BASF SE, and Huntsman Corporation, driving innovation in pigments and treatment solutions.