- Inks, Coatings, Adhesives & Sealants (ICAS)

- Exterior Architectural Coating Market

Exterior Architectural Coating Market Size, Share and Growth Forecast, 2026-2033

Exterior Architectural Coating Market by Resin Type (Acrylic, Epoxy, Polyester, Alkyd, Polyurethane), Technology (Solvent-Borne, Waterborne), Product Type (Primer, Emulsion, Enamel), Application (Residential, Non-Residential), and Regional Analysis for 2026-2033

Exterior Architectural Coating Market Share and Trends Analysis

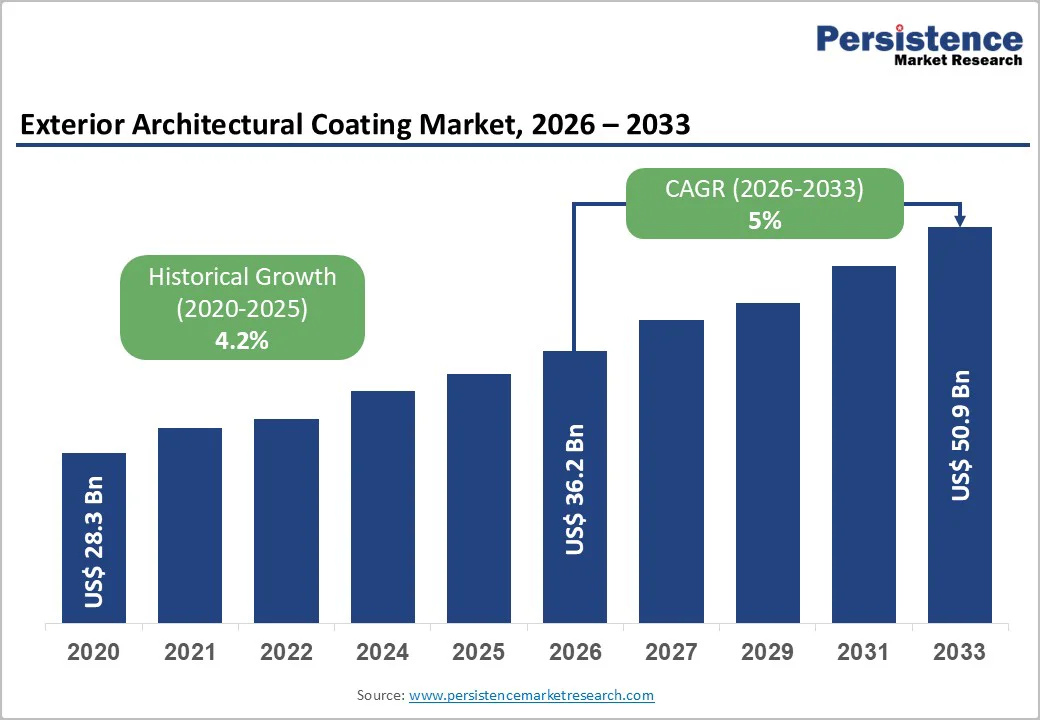

The global exterior architectural coating market size is likely to be valued at US$ 36.2 billion in 2026 and is projected to reach US$ 50.9 billion by 2033, growing at a CAGR of 5% during the forecast period 2026 - 2033. Market expansion is primarily supported by sustained residential construction activity, large-scale renovation cycles in mature economies, and tightening environmental regulations, accelerating the shift toward waterborne exterior coatings. Public infrastructure investments, urban housing demand across Asia Pacific, and advancements in acrylic-based weather-resistant formulations continue to reinforce long-term growth visibility. Increasing adoption of durable, UV-stable, and low-VOC exterior paints is structurally reshaping product portfolios across global manufacturers.

Key Industry Highlights

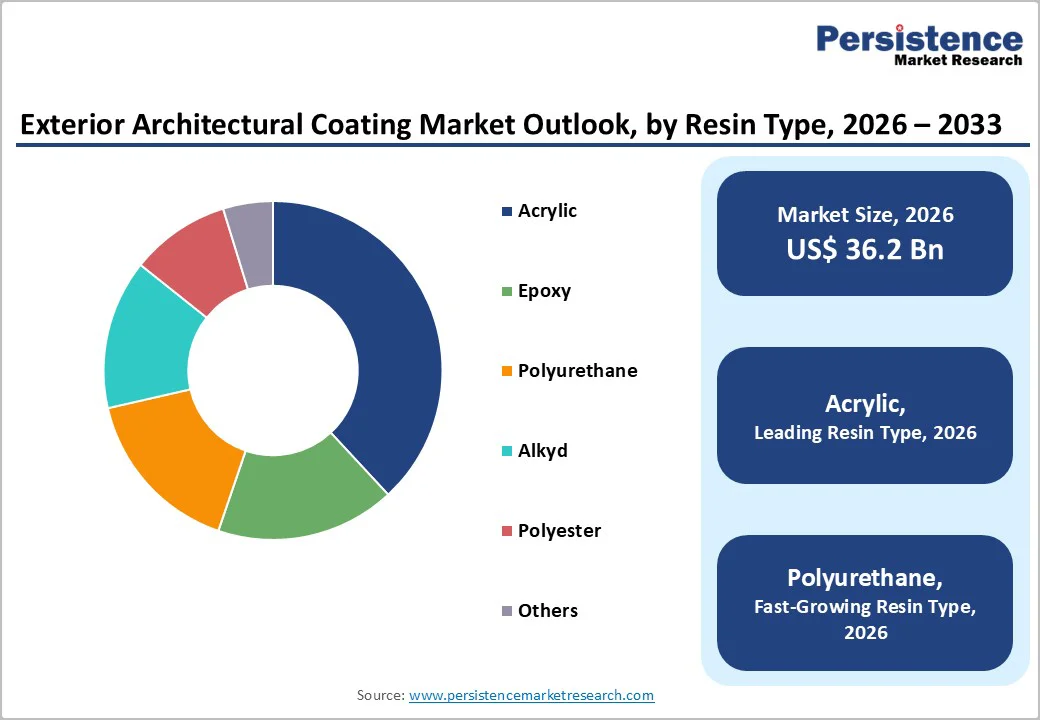

- Dominant Resin Type: Acrylic resins are expected to command around 40% of the revenue share in 2026, while polyurethane-based coatings are likely to grow at an estimated 6.2% CAGR during 2026–2033, supported by rising demand for high-durability finishes.

- Leading Technology: Waterborne coatings are anticipated to dominate the market with approximately 65% share in 2026, driven by formulation advancements and accelerated penetration across Asia Pacific and other emerging economies.

- Product Type Dynamics: Emulsion coatings are projected to lead with an estimated 48% in 2026, whereas primer coatings are expected to grow the fastest at 6% CAGR from 2026 to 2033, driven by the growing emphasis on longer coating lifecycles.

- Application Dynamics: Residential applications are projected to account for nearly 60% of total volume in 2026, while non-residential applications are poised to register the highest CAGR through 2033, owing to a large housing stock and massive commercial construction projects.

- Regional Leadership: Asia Pacific is slated to dominate with an estimated 38% share in 2026, fueled by government housing programs in urban clusters across China, India, and Southeast Asia.

- October 2025: AkzoNobel launched the world’s first hydrophilic?resin self-cleaning façade coating that significantly reduces maintenance needs by letting rainwater carry away dirt and pollutants.

| Key Insights | Details |

|---|---|

| Exterior Architectural Coating Market Size (2026E) | US$ 36.2 Bn |

| Market Value Forecast (2033F) | US$ 50.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Housing Activity Expansion and Sustainability-Focused Product Innovation

Residential construction and renovation remain the primary demand drivers for exterior architectural coatings, supported by sustained housing investment, recurring repainting cycles, and urban infrastructure development. Large urban populations in Asia and steady refurbishment in mature markets ensure consistent consumption, as exterior surfaces require periodic renewal to maintain protection and aesthetics. Government-backed housing programs and urban development initiatives further boost demand for emulsions, primers, and other exterior coatings, enabling stable, volume-led growth across both new construction and renovation sectors.

Rising environmental regulations and consumer preference for sustainable solutions are driving the adoption of low-VOC and bio-based coatings. For example, Vermont Natural Coatings PolyWhey Exterior Stain is a bio-based product that uses whey protein technology derived from dairy industry by-products, providing a renewable and environmentally friendly alternative to conventional binders. The stain forms a durable, waterproof barrier while offering UV protection for outdoor wood surfaces. Combined with advanced acrylic and polyurethane formulations, such innovations enhance surface durability, reduce maintenance cycles, and lower ownership costs. Regulatory alignment and eco-friendly product development are thus transforming compliance into a long-term growth catalyst.

Cost Volatility and Regulatory Compliance Pressure on Manufacturers

Exterior architectural coating manufacturers face structural cost pressure due to reliance on petrochemical-based raw materials. Inputs such as resins, solvents, and performance additives are closely linked to crude oil price movements, creating frequent cost fluctuations. Since raw materials form a substantial portion of total production expenses, sudden price increases directly compress margins and reduce pricing flexibility. Mid-sized and regional producers are particularly exposed, as limited hedging capacity and long procurement cycles restrict their ability to absorb or pass on cost increases during volatile market periods.

Tightening environmental and chemical safety regulations add to operational complexity and expense. Continuous reformulation, product testing, and certification are required to remain compliant with evolving emission and labeling standards, increasing fixed compliance costs. Smaller manufacturers often struggle to justify these investments, raising the risk of market exit or forced consolidation. In the short term, this can limit product availability in price-sensitive regions and slow innovation rollout, particularly where regulatory enforcement accelerates faster than local industry readiness.

Waterborne Innovation and Premium Functional Coatings Fuel Exterior Infrastructure Growth

Emerging economies offer significant growth potential for exterior architectural coating manufacturers as markets increasingly shift from solvent-based products to waterborne formulations. This transition is fueled by rapid urbanization, heightened regulatory awareness, and evolving consumer preferences, with Asia Pacific playing a central role due to its substantial contribution to global construction activity. The relatively low adoption rate of waterborne coatings in developing regions compared to mature markets signals considerable room for expansion. Manufacturers can capitalize on this trend by providing compliant, cost-effective solutions designed for local climatic and regulatory requirements, thus establishing scalable growth pathways.

Premiumization and infrastructure expansion are further enhancing value creation opportunities in the sector. There is growing demand for functional exterior coatings that deliver durability, self-cleaning capabilities, and aesthetic versatility, especially in densely populated urban and coastal areas where energy efficiency and long-term performance are essential. For example, at the 2025 American Institute of Architects (AIA) Conference, PPG introduced Coraflon® Platinum and Duranar® liquid coatings, which provide extended weather resistance, excellent color retention, and a wide range of design options for both residential and commercial applications. These advanced solutions enable higher profit margins, strengthen brand differentiation, and align with increasing infrastructure investment, thereby driving sustained growth across commercial and institutional construction segments.

Category-wise Analysis

Resin Type Insights

Acrylic resins are likely to account for approximately 40% of the exterior architectural coating market revenue share in 2026 due to their strong weather resistance, UV stability, and color retention. These properties make acrylic coatings highly suitable for exterior wall applications exposed to harsh climatic conditions. Compatibility with waterborne systems further strengthens their adoption under tightening environmental regulations. Residential construction remains the primary demand base for acrylic coatings globally. Broad availability and cost efficiency also support large-scale usage. Together, these factors reinforce acrylic resins as the dominant material choice.

Polyurethane (PU) resins are projected to be the fastest-growing segment, expanding at an estimated 6.2% CAGR between 2026 and 2033. Growth is driven by increasing demand for enhanced abrasion resistance and longer service life in commercial and institutional buildings. Adoption is particularly strong in premium façades due to superior protection against moisture, chemicals, and mechanical wear. Innovations from 2025, such as Allnex’s UCECOAT® 7997 bio-carbon certified waterborne polyurethane dispersion, low-bake powder coating resins, and formaldehyde-free crosslinkers, enhance sustainability and performance while maintaining low VOC emissions. These high-performance, eco-friendly solutions reinforce polyurethane’s value-driven penetration, offsetting higher upfront costs with lower maintenance and long-term durability.

Technology Insights

Waterborne coatings are anticipated to dominate the technology segment, holding nearly 65% revenue share in 2026, as environmental compliance becomes a priority across global markets. Low volatile organic compound (VOC) emissions, improved safety during application, and regulatory acceptance support widespread adoption. Performance improvements in adhesion, drying time, and chemical resistance have enhanced their suitability for exterior use. Residential projects remain the largest end-use base for waterborne technologies, while public infrastructure projects increasingly specify these systems. Innovations such as Tnemec’s Series 288 Enviro?Pox and Series 289 Enviro?Pox, waterborne epoxy coatings engineered for superior durability, enhanced chemical resistance, and easier application, exemplify advancements that broaden waterborne adoption in both architectural and industrial applications.

Waterborne coatings are also set to grow the fastest at a 5.8% CAGR from 2026 to 2033. Ongoing innovation in binder chemistry and product performance, including enhanced durability and weather resistance, has accelerated conversion from solvent-borne products, particularly in emerging economies. Rising enforcement of environmental standards further supports this transition. Manufacturers continue to expand waterborne product portfolios, ensuring that growth momentum remains structurally strong.

Product Type Insights

Emulsion coatings will likely lead the product category in 2026, reaching about 48% in terms of revenue share, since they balance performance with straightforward application across a wide range of projects. Builders and homeowners use them extensively on residential exterior walls for both new builds and refurbishments, and the broad shade range helps maintain visual consistency over time. Formulators also benefit because emulsions align well with waterborne technology, which supports compliance and simpler on-site handling in many markets. To capture this volume, suppliers should prioritize easy-to-spec products, dependable tinting performance, and strong availability through retail outlets and contractor channels.

Primers should deliver the fastest expansion, rising at an estimated 6% CAGR through 2033, as manufacturers place greater emphasis on surface preparation and long-term substrate protection. A well-chosen primer improves adhesion and extends the service life of the full coating system, which becomes more valuable in harsh settings such as humid zones, coastal belts, and high-pollution corridors. Non-residential buyers increasingly request higher-performance systems, which pushes demand toward specialized primer chemistries and clearer application guidance. Coating manufacturers can turn this shift into margin growth by offering substrate-specific primer selections, contractor training, and warranties tied to full system use.

Application Insights

Residential applications are predicted to dominate the exterior architectural coating market landscape, accounting for approximately 60% of the total volume in 2026 due to an expanding global housing stock and consistent repainting cycles. Home improvement projects drive consumption in mature economies, where homeowners prioritize aesthetic maintenance and property value protection. Manufacturers sustain this leadership position by fostering brand loyalty through targeted marketing and ensuring widespread product availability in retail channels. Exterior emulsions serve as the primary choice for these projects because they offer a balance of durability, cost-effectiveness, and ease of use. Suppliers can further capitalize on this segment by offering broad color palettes and user-friendly application tools that appeal to both do-it-yourself (DIY) enthusiasts and professional residential contractors.

Non-residential applications are projected to expand more rapidly, registering an estimated 5.9% CAGR between 2026 and 2033. Rising investment in commercial buildings, public infrastructure, and institutional facilities fuels this demand, as these structures require coatings that meet rigorous durability and regulatory compliance standards. Stakeholders in this sector increasingly prioritize lifecycle cost over initial price, which accelerates the adoption of advanced resin systems and high-performance primers designed for longevity. As governments and private developers increase infrastructure spending, coating manufacturers should focus on technical specifications, warranty programs, and specialized solutions such as anti-graffiti or self-cleaning technologies to secure contracts in this high-growth vertical.

Regional Insights

North America Exterior Architectural Coating Market Trends

North America represents a mature, high-value market for exterior architectural coatings, expected to contribute an estimated 28% of global revenue in 2026, with the United States as the primary driver of regional demand. Recurring residential renovation cycles, façade refurbishment across aging housing stock, and ongoing non-residential maintenance programs collectively sustain a large installed base that requires regular coating upgrades. Stringent environmental regulations continue to accelerate the shift toward low VOC and waterborne technologies, prompting manufacturers to modernize product portfolios and strengthen compliance positioning. In 2025, for instance, BASF broadened its biomass-balanced offerings in North America, which lowered product carbon intensity and indirectly encouraged greater adoption of more sustainable exterior coating systems.

Regional exterior architectural coating market growth is expected to remain moderate through 2033, which reflects market maturity rather than a rapid increase in coating volumes. Investments in energy-efficient buildings, supported by federal and state-level infrastructure initiatives, are shifting demand toward premium exterior solutions that deliver extended durability, improved weather resistance, and better building envelope performance. A well-established contractor base and deep retail penetration ensure reliable specification, distribution, and application, which reinforces steady replacement and upgrade cycles. These dynamics position North America as a stable, high-value region where sustainability requirements and performance expectations guide purchasing decisions and create opportunities for differentiated, higher-margin coating technologies.

Europe Exterior Architectural Coating Market Trends

Europe is poised to command nearly 24% of the exterior architectural coating market share in 2026, with Germany, France, the United Kingdom, and Spain leading regional consumption. Strict environmental compliance defines the landscape, as harmonized chemical and emission standards propel waterborne technologies to the forefront of product adoption across diverse applications. Renovation and refurbishment projects generate the primary demand, especially in Western Europe, where aging structures require periodic upgrades to maintain performance and visual appeal. Coating suppliers can leverage this stability by aligning formulations with regional norms, such as low-emission profiles and enhanced substrate compatibility, to secure long-term contracts in maintenance-heavy segments.

The Europe market anticipates moderate expansion between 2026 and 2033, fueled by energy retrofitting programs, façade insulation enhancements, and efforts to preserve historic buildings. Intense competition spurs ongoing innovation in areas such as extended durability, refined aesthetics, and eco-friendly attributes, which meet escalating performance expectations. Regulatory pressures and replacement cycles create a predictable demand environment, where manufacturers who invest in compliant, high-value solutions gain a decisive edge.

Asia Pacific Exterior Architectural Coating Market Trends

Asia Pacific is set to lead the exterior architectural coating market in 2026, securing roughly 38% of global revenue and achieving the fastest expansion rate during the 2026-2033 forecast period. China, India, and ASEAN nations are envisaged to spearhead this surge through swift urbanization, expanding middle-class homeownership, and large-scale government construction initiatives. Vietnam illustrates this trend with its affordable housing program, encompassing about 692 projects and 633,559 units. Thái Bình Province scheduled 24 projects in 2025, contributing to Vietnam's national goal of 1 million social housing units by 2030 for workers and low-income households. These extensive developments generate continuous coating consumption for new builds and refurbishment work.

The regional market’s projected CAGR of 6.5% through 2033 establishes it as the main driver of global market expansion. Waterborne coating uptake is slated to quicken, aided by growing local production capacity and progressively higher quality benchmarks. The Asia Pacific market also gains from economical manufacturing, the rise of capable domestic brands, and heightened investment from international producers setting up regional facilities. Public-sector residential building efforts supply a reliable consumption base, cementing the region's preeminence in the worldwide exterior architectural coatings arena.

Competitive Landscape

The global exterior architectural coating market structure is moderately consolidated, with leading multinational players such as Sherwin-Williams, PPG Industries, AkzoNobel, Nippon Paint Holdings, and RPM International accounting for a significant share of global revenue. These companies benefit from strong brand equity, extensive retail and contractor distribution networks, and diversified portfolios across acrylic, polyurethane, and waterborne exterior coatings. Continuous investment in product innovation, sustainability-driven reformulation, and performance-enhancing technologies enables these players to maintain competitive positioning while meeting increasingly stringent environmental regulations.

Regional and mid-sized manufacturers across Asia Pacific, Europe, and the Middle East hold strong positions by tailoring products to local climate conditions, pricing structures, and regulatory requirements. Companies such as Asian Paints, Berger Paints, Kansai Paint, and Jotun leverage localized manufacturing, dense dealer networks, and cost efficiencies to compete effectively in high-growth markets. While high entry barriers related to compliance, raw material sourcing, and brand trust limit new entrants, ongoing market consolidation through acquisitions and partnerships is expected as global leaders expand geographically and strengthen premium and sustainable coating offerings.

Key Industry Developments

- In October 2025, Sherwin-Williams completed the acquisition of BASF’s Suvinil brand for approximately US$ 1.15 billion, strengthening its footprint in Brazil and Latin America. This strategic move expands their architectural coatings portfolio, enhances market share in decorative paints, and leverages Suvinil’s established brand presence across the region.

- In June 2025, PPG Industries highlighted innovations at its Global Coatings Innovation Center in Allison Park, PA, including low-temperature electrocoats, overspray-free systems, and energy-efficient protective coatings. These developments enhance productivity, reduce emissions, and reinforce PPG’s strategic focus on sustainable, high-performance coatings for architectural and industrial applications.

- In May 2025, AkzoNobel launched a "sunscreen" thermal insulation exterior coating system in China, designed to reduce building surface temperatures and improve energy efficiency by reflecting solar radiation and emitting heat, acting like a sunscreen for buildings and lowering surface temperatures by up to 10%.

Companies Covered in Exterior Architectural Coating Market

- Sherwin-Williams

- PPG Industries

- AkzoNobel

- Nippon Paint Holdings

- RPM International

- Asian Paints

- BASF Coatings

- Kansai Paint

- Jotun Group

- Axalta Coating Systems

- Hempel Group

- Berger Paints

Frequently Asked Questions

The global exterior architectural coating market is projected to reach US$ 36.2 billion in 2026.

Expanding residential and infrastructure construction, increasing renovation and repainting cycles, regulatory enforcement favoring low-VOC and waterborne coatings, and advancements in coating durability and weather resistance are driving the market.

The market is poised to witness a CAGR of 5% between 2026 and 2033.

Major opportunities include rising penetration of waterborne exterior coatings in emerging economies, growing demand for high-performance and functional exterior coatings, and increased infrastructure investment across Asia Pacific and the Middle East.

Some of the most prominent players in the market include Sherwin-Williams, PPG Industries, AkzoNobel, Nippon Paint Holdings, RPM International, and Asian Paints.