- Smart Packaging

- EPE Foam Packaging Market

EPE Foam Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

EPE Foam Packaging Market by Product (Low-Density EPE Foam, High-Density EPE Foam, Others), Application (Protective Packaging, Electronics & Electricals, Others), End-user, and Regional Analysis for 2026 - 2033

EPE Foam Packaging Market Size and Trends Analysis

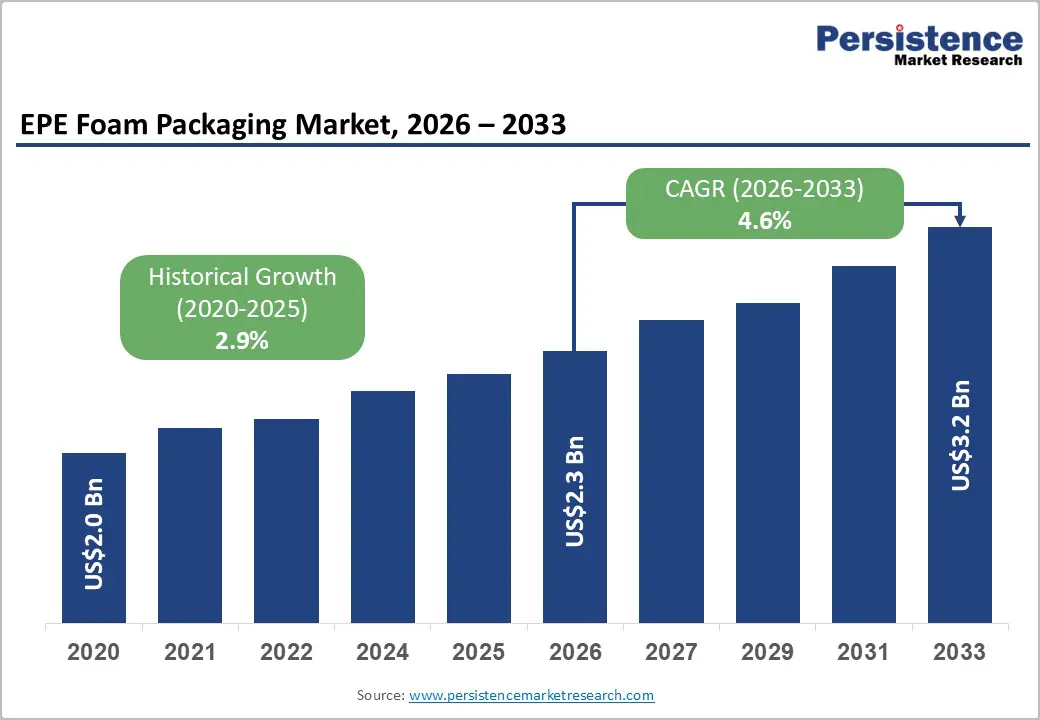

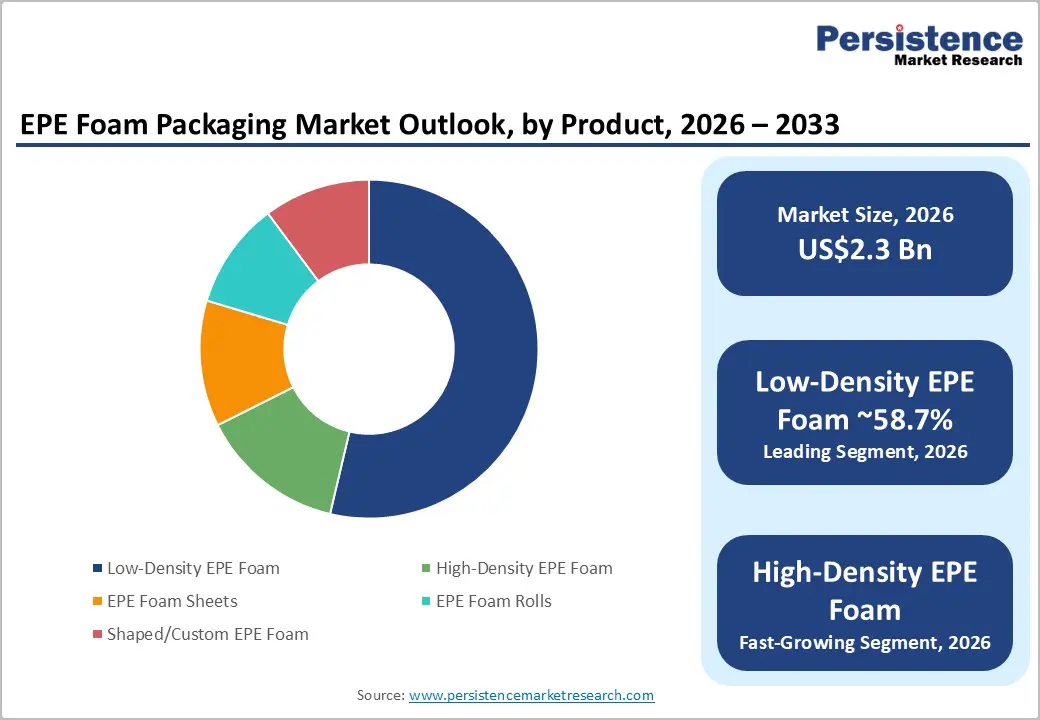

The global EPE foam packaging market size is likely to be valued at US$2.3 billion in 2026 and is expected to reach US$3.2 billion by 2033, growing at a CAGR of 4.6% between 2026 and 2033, driven by the steady expansion of e-commerce logistics, rising shipments of consumer electronics, and sustained demand for lightweight protective materials in automotive and appliance supply chains.

The market structure remains volume-driven, with low-density EPE accounting for the majority of demand, while higher-density and customized formats capture value in industrial applications. Companies that balance scale-oriented production with engineered, higher-margin solutions and recyclable formulations are best positioned to capture long-term growth and manage regulatory risks.

Key Industry Highlights

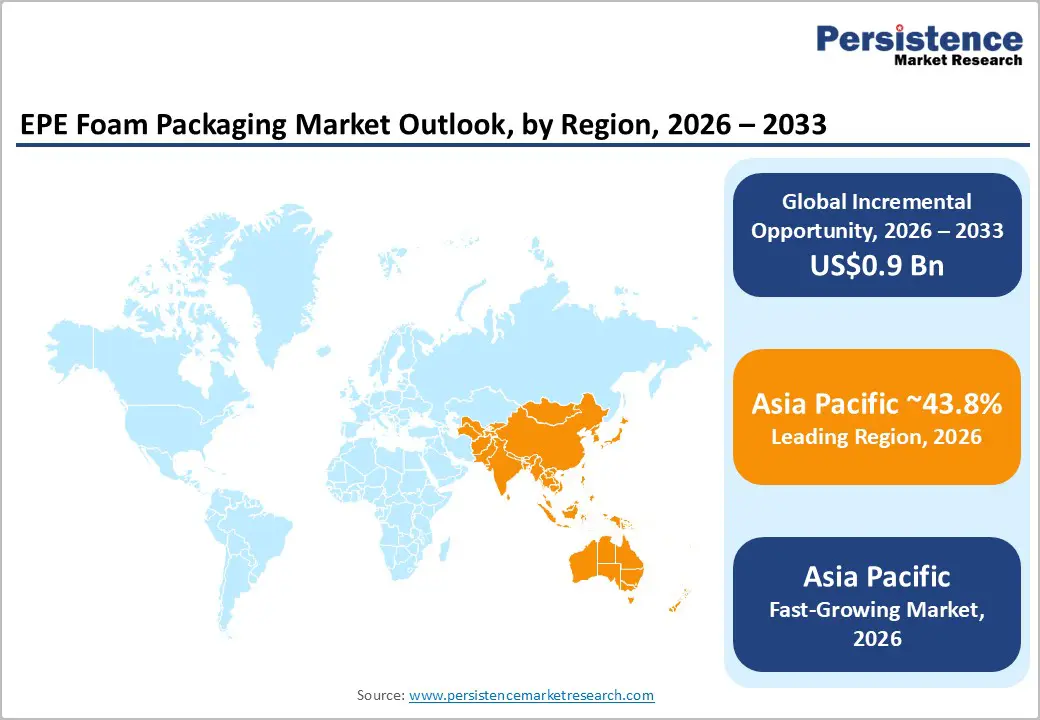

- Leading Region: Asia Pacific is projected to account for over 43.8% of the market share, driven by dense electronics manufacturing clusters in China, expanding production in India and ASEAN, and strong export-oriented supply chains.

- Fastest-growing Region: Asia Pacific is also the fastest-growing region, supported by rapid e-commerce penetration, manufacturing scale-up initiatives, and increasing investments in localized foam extrusion and converting capacity.

- Investment Plans: Manufacturers are expanding extrusion and die-cutting capacities in China, India, and Mexico, while investing in recyclable and recycled-content EPE formulations. Capital allocation is focused on automation, engineered inserts, and reusable dunnage systems to address sustainability and margin optimization goals.

- Dominant Product: Low-density EPE foam is anticipated to lead with approximately 58.7% market share, owing to its cost efficiency, lightweight properties, and widespread use in high-volume protective packaging applications across e-commerce and consumer electronics.

- Leading Application: Protective packaging is estimated to account for over 49.2% of the market, reflecting strong demand for cushioning, corner protection, and void-fill solutions in the transportation of electronics, appliances, and industrial goods.

| Key Insights | Details |

|---|---|

| EPE Foam Packaging Market Size (2026E) | US$2.3 Bn |

| Market Value Forecast (2033F) | US$3.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 2.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Surge in E-Commerce and Parcel Volumes

Global e-commerce expansion continues to reshape packaging consumption patterns. The rise in direct-to-consumer shipping has increased parcel volumes, thereby increasing demand for cushioning, void-fill, and surface-protection materials. Each shipped unit requires protective packaging that can withstand handling, vibration, and drop risks in last-mile logistics. EPE foam, due to its lightweight and shock-absorbing properties, aligns well with dimensional weight pricing structures used by courier networks. As parcel density grows across electronics, apparel, and home goods categories, packaging intensity per shipment increases. This structural shift contributes significantly to the projected CAGR by expanding addressable volume and reinforcing recurring demand across fulfillment networks.

Electronics and Consumer Device Shipments

The proliferation of consumer electronics and high-value industrial components supports increasing demand for precision protective packaging. Miniaturized devices and higher average selling prices have elevated protection standards, including drop-test compliance and electrostatic discharge (ESD) control. Manufacturers require custom-shaped EPE inserts that secure products during transit while maintaining dimensional stability. This shift toward engineered solutions increases revenue per kilogram of foam and strengthens supplier relationships through design integration. As device complexity rises and cross-border shipments expand, packaging reliability becomes a strategic procurement priority. The result is sustained demand for high-performance EPE formats across electronics, telecommunications equipment, and precision instruments.

Lightweighting and Transport Cost Optimization

Freight pricing models increasingly emphasize weight and volumetric efficiency. Packaging materials that reduce shipping weight while maintaining protective integrity offer measurable cost savings. EPE foam’s low density and high energy absorption enable shippers to optimize cushioning without increasing dimensional weight charges. Logistics operators and OEMs actively pursue packaging redesign initiatives to reduce overall shipping costs and carbon footprint intensity. This focus encourages adoption of thinner profiles, multilayer laminates, and custom inserts engineered for performance efficiency. Consequently, EPE foam benefits from both cost-reduction strategies and sustainability objectives centered on material minimization.

Barrier Analysis - Raw Material Price Volatility

EPE foam production depends on polyethylene resin derived from petrochemical feedstocks. Resin prices fluctuate in response to crude oil dynamics and ethylene supply conditions, creating cost uncertainty for manufacturers. Companies operating in high-volume, price-sensitive segments often have limited ability to pass through cost increases immediately. Short-term volatility can compress margins and delay procurement decisions by cost-conscious buyers. Historical swings in resin prices have affected gross margins across polymer-based packaging segments. To mitigate risk, producers rely on long-term supply contracts, inventory management strategies, and selective price adjustments tied to feedstock indices.

Sustainability and Regulatory Pressure

Packaging regulations in several markets increasingly emphasize recyclability, waste reduction, and extended producer responsibility frameworks. Polymeric foams, including EPE, face scrutiny where recycling infrastructure is limited. Compliance may require investment in recycled-content formulations, take-back systems, or material traceability mechanisms. These changes can raise capital expenditure and operating costs. Customers, particularly multinational retailers and electronics OEMs, are integrating sustainability criteria into procurement decisions. Suppliers that fail to demonstrate environmental performance improvements risk losing business. Addressing regulatory complexity while maintaining cost competitiveness remains a structural challenge.

Opportunity Analysis - Premium Engineered Inserts and Industry-Specific Solutions

Custom-shaped EPE inserts designed for electronics, automotive components, and medical devices command higher margins compared to commodity sheets and rolls. Precision fabrication, design prototyping, and low-volume production services create differentiation and long-term OEM partnerships. A strategic shift of 5-8% of total market volume toward engineered solutions can generate mid-single-digit revenue uplift, given higher unit pricing and service bundling. Investment in CNC routing, die-cutting technology, and collaborative packaging design capabilities enhances competitive positioning. Companies that integrate engineering expertise into sales offerings can transition from commodity supply to value-added partnerships.

Asia Pacific Manufacturing and Export Scale-Up

Asia-Pacific is the largest and fastest-growing regional market. The region’s manufacturing density, export orientation, and expanding domestic e-commerce networks provide scale advantages. Establishing regional extrusion and converting facilities in China, India, and Southeast Asia reduces transportation costs and shortens delivery cycles. Even a modest 2-3 percentage-point gain in regional market share can significantly impact overall revenue due to the region’s size. Operational efficiency, localized raw material sourcing, and strong distribution partnerships are critical success factors.

Category-wise Analysis

Product Insights

Low-density EPE foam is expected to account for nearly 58.7% of the market over the forecast period. Its dominance stems from cost efficiency, strong cushioning performance, and compatibility with high-volume packaging formats. The material is widely used in electronic inserts for smartphones and laptops, appliance corner protectors for brands such as Whirlpool and LG, and protective mailers across major e-commerce platforms.

Continuous extrusion technology enables mass production of sheets and rolls at optimized cost structures, supporting large-scale distribution networks. Its lightweight profile reduces dimensional shipping charges, making it highly suitable for fulfillment centers and third-party logistics providers. As parcel shipments and consumer electronics volumes continue to grow, low-density EPE remains the preferred choice for standardized, cost-sensitive protective packaging.

High-density EPE foam is projected to grow the fastest, driven by rising adoption in automotive, heavy equipment, and industrial machinery packaging. This segment benefits from demand for higher compressive strength, vibration dampening, and long-term durability. Automotive OEMs such as Toyota and BMW are increasingly deploying reusable, high-density EPE dunnage trays for component transport between Tier 1 suppliers and assembly plants. Industrial exporters of precision machinery and HVAC systems also rely on thicker foam grades for secure international shipments.

Compared to low-density variants, high-density formulations generate higher revenue per unit due to specialized performance characteristics. Ongoing investment in cross-linking processes and surface lamination technologies enhances moisture and abrasion resistance, strengthening product differentiation and contract-based supply agreements.

Application Insights

Protective packaging is anticipated to account for over 49.2% of the market share in 2026. The segment includes cushioning inserts, edge protectors, foam wraps, and void-fill materials used in the transportation of electronics, furniture, medical equipment, and industrial tools. E-commerce platforms and global courier services rely on such formats to reduce product damage rates during last-mile delivery. For example, consumer electronics manufacturers frequently integrate die-cut EPE inserts into retail-ready packaging to ensure drop-test compliance.

The material’s shock absorption, flexibility, and lightweight structure support both cost optimization and product safety. Stable demand from large manufacturing clusters ensures consistent production volumes for extruders and converters operating in this segment.

Electronics and electrical packaging are projected to grow the fastest in the application landscape, driven by increasing device sophistication and stricter performance standards. High-value components such as semiconductors, printed circuit boards, and telecommunications modules require precision-fit inserts with anti-static and electrostatic discharge protection. Manufacturers of smartphones, networking equipment, and industrial automation systems utilize custom-molded EPE solutions to minimize vibration and transit damage.

Rising exports of consumer electronics from the Asia Pacific and growing investments in semiconductor fabrication facilities reinforce packaging demand. As device miniaturization continues and global trade volumes expand, engineered EPE cushioning solutions are expected to gain greater adoption across electronics supply chains.

Regional Insights

North America EPE Foam Packaging Market Trends - Automation-Driven, Sustainability-Led Industrial and E-Commerce Demand

North America represents a value-intensive EPE foam packaging market supported by advanced converting infrastructure, automation adoption, and strong demand from electronics, medical devices, and industrial equipment manufacturers. The U.S. accounts for the majority of regional consumption, driven by one of the world’s highest e-commerce penetration rates. Major electronics and appliance brands such as Apple, HP, and Whirlpool rely on engineered foam inserts to meet drop-test and transit protection standards, sustaining consistent industrial-scale procurement.

Sustainability and regulatory compliance increasingly shape purchasing decisions. Several U.S.-based packaging leaders, including Sealed Air and Pregis, have expanded their recyclable and recycled-content foam portfolios as part of corporate sustainability commitments aligned with the U.S. Plastics Pact. For example, Pregis has invested in foam recycling infrastructure and introduced polyethylene foam solutions designed for circular recovery streams, strengthening domestic recycling loops. Automation investments in states such as Ohio and Texas have enhanced die-cutting precision and throughput, lowering conversion costs and supporting customized insert production.

Automotive OEMs and electronics assemblers relocating production from Asia to Mexico increase cross-border component shipments, which elevates demand for reusable EPE dunnage systems. Companies operating manufacturing hubs in Monterrey and Querétaro increasingly deploy high-density EPE trays for returnable packaging, improving cost efficiency in regional supply chains. These developments collectively reinforce North America’s positioning as a technologically advanced and compliance-focused market.

Europe EPE Foam Packaging Market Trends - Regulation-intensive, Automotive-Anchored Protective Packaging Market

Europe demonstrates steady, regulation-driven demand for EPE foam packaging, supported by strong automotive exports, advanced machinery manufacturing, and mature consumer goods markets. Germany leads regional industrial consumption, driven by its automotive and engineering base, with OEMs such as Volkswagen Group and BMW requiring protective foam packaging for precision components and export shipments. The U.K. and France contribute significantly through retail and e-commerce-driven packaging demand, supported by large distribution networks and omnichannel retail models.

Regulatory harmonization across the European Union significantly influences material selection and innovation. The EU Packaging and Packaging Waste Directive and ongoing revisions under the European Green Deal have intensified scrutiny on recyclability and extended producer responsibility. As a result, packaging suppliers are integrating higher recycled-content polyethylene and developing mono-material solutions to simplify recovery processes. Companies such as Storopack and JSP have expanded recyclable polyethylene foam product lines and invested in closed-loop take-back programs across Germany and France.

Automotive electrification trends also support demand for precision protective packaging. European battery manufacturers and EV component suppliers require vibration-resistant, anti-static foam solutions for lithium-ion battery modules and power electronics. In Spain and Eastern Europe, new EV manufacturing investments stimulate localized packaging conversion capacity. Capital flows increasingly support recycling technology upgrades and digital traceability systems, enabling suppliers to meet compliance documentation requirements. These structural shifts sustain Europe’s stable yet compliance-intensive growth trajectory.

Asia Pacific EPE Foam Packaging Market Trends-Manufacturing-Scale-Driven, Cost-Efficient, and Fast-Growing Supply Hub

Asia Pacific is expected to be the leading and fastest-growing region in the market, accounting for over 43.8% of the market share in 2026. The region benefits from dense electronics manufacturing clusters, integrated supply chains, and cost-competitive resin production. China dominates both production and consumption, supported by large-scale electronics assembly operations serving global brands such as Huawei, Xiaomi, Lenovo, and international contract manufacturers.

The concentration of export-oriented manufacturing hubs in Guangdong, Jiangsu, and Zhejiang provinces generates sustained demand for protective foam sheets, rolls, and custom-molded inserts. Japan emphasizes high-performance technical foam applications, particularly for automotive and precision electronics sectors. Automotive OEMs, including Toyota and Honda, utilize engineered EPE dunnage for component logistics within domestic and export supply chains. Japanese manufacturers such as JSP have advanced lightweight polyethylene foam technologies with enhanced impact resistance, strengthening the region’s innovation profile.

India and Southeast Asia exhibit accelerating growth momentum driven by expanding domestic manufacturing and rapid e-commerce penetration. India’s Production Linked Incentive schemes for electronics and mobile manufacturing have attracted global brands to establish assembly operations, which increases demand for protective packaging materials. In Southeast Asia, countries such as Vietnam and Thailand continue to attract electronics assembly and automotive investments, creating new converting facilities for foam packaging.

Regional players have expanded extrusion capacity and automated die-cutting lines to meet export quality standards. Localized resin sourcing, improved logistics infrastructure, and automation investments further strengthen Asia Pacific’s role as a global supply base. The region’s combination of manufacturing scale, technological adoption, and cost efficiency underpins its leadership position in both production and consumption of EPE foam packaging solutions.

Competitive Landscape

The global EPE foam packaging market is moderately fragmented, comprising multinational producers and numerous regional converters. High-volume roll and sheet segments face competitive pricing pressure, whereas engineered inserts and specialty grades exhibit higher concentration and greater margin stability. Vertical integration and feedstock partnerships help mitigate risks associated with raw materials.

Leading companies prioritize engineered product differentiation, regional capacity expansion, and integration of sustainability. Service-based offerings combining packaging design, prototyping, and logistics support enhance customer retention and competitive positioning.

Key Industry Developments

- In June 2025, Sealed Air Corporation launched a new recyclable cushioning foam alternative, EcoFoam Shield, designed to meet rising demand for sustainable protective packaging in the electronics and consumer goods sectors.

Companies Covered in EPE Foam Packaging Market

- Sealed Air Corporation

- Pregis LLC

- JSP Corporation

- Storopack Hans Reichenecker GmbH

- BASF SE

- Kaneka Corporation

- Mitsubishi Chemical Group Corporation

- Kuraray Co., Ltd.

- Zotefoams plc

- Armacell International S.A.

- Recticel NV/SA

- Signode Industrial Group LLC

- FoamPartner Group

- Plastifoam Company, Inc.

- Wisconsin Foam Products

- UFP Technologies, Inc.

- Dongshin Industry Inc.

- Sanchez Packaging Industries

Frequently Asked Questions

The global EPE foam packaging market is likely to be valued at US$2.3 billion in 2026.

The EPE foam packaging market is expected to reach US$3.2 billion by 2033.

Key trends include the rapid expansion of e-commerce-driven protective packaging demand, increasing adoption of engineered and anti-static foam inserts for electronics, growth in reusable dunnage systems for automotive supply chains, and rising investments in recyclable and recycled-content polyethylene foam solutions aligned with sustainability regulations.

Low-density EPE foam is the leading product segment, accounting for approximately 58.7% of the total market share, driven by its cost efficiency, lightweight profile, and suitability for high-volume protective packaging applications.

The EPE foam packaging market is projected to grow at a CAGR of 4.6% between 2026 and 2033.

Major players include Sealed Air Corporation, JSP Corporation, Storopack Hans Reichenecker GmbH, Pregis LLC, and BASF SE.