- Industrial Goods & Service

- Door Frame Market

Door Frame Market Size, Share, and Growth Forecast, 2026 – 2033

Door Frame Market by Frame Type (Wood, Aluminum, Hollow Steel, Vinyl, Fiberglass), End-User (Residential, Commercial, Industrial), Distribution Channel (Offline Retail, Online Retail, Direct Sales), and Regional Analysis for 2026-2033

Door Frame Market Share and Trends Analysis

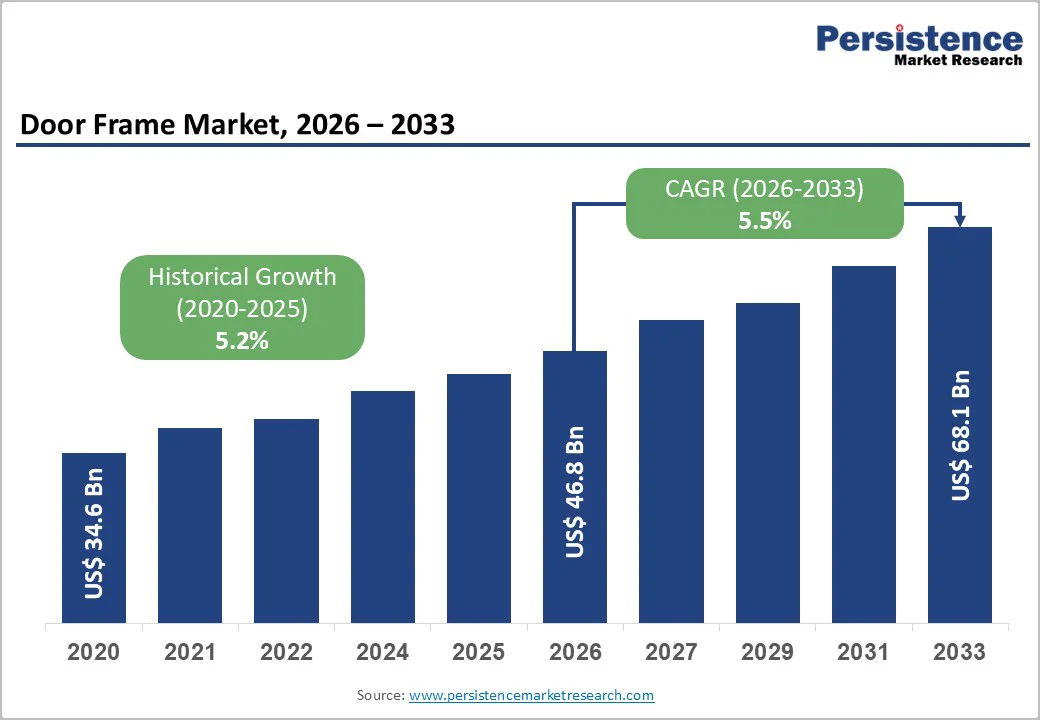

The global door frame market size is likely to be valued at US$ 46.8 billion in 2026, and is projected to reach US$ 68.1 billion by 2033, growing at a CAGR of 5.5% during the forecast period 2026−2033. Rising demand for door frames reflects growth in residential construction, large commercial projects, and use of durable, standardized materials. Government housing programs and urban redevelopment initiatives boost consumption across developed and emerging markets. Aluminum, hollow steel, and fiberglass frames improve durability and reduce maintenance, encouraging replacement activity. Fire safety, energy efficiency, and structural compliance regulations increase adoption in commercial and industrial buildings. Expanded availability through direct sales and online retail enhances accessibility and cost-effectiveness, allowing efficient procurement for both new construction and renovation projects.

Key Industry Highlights

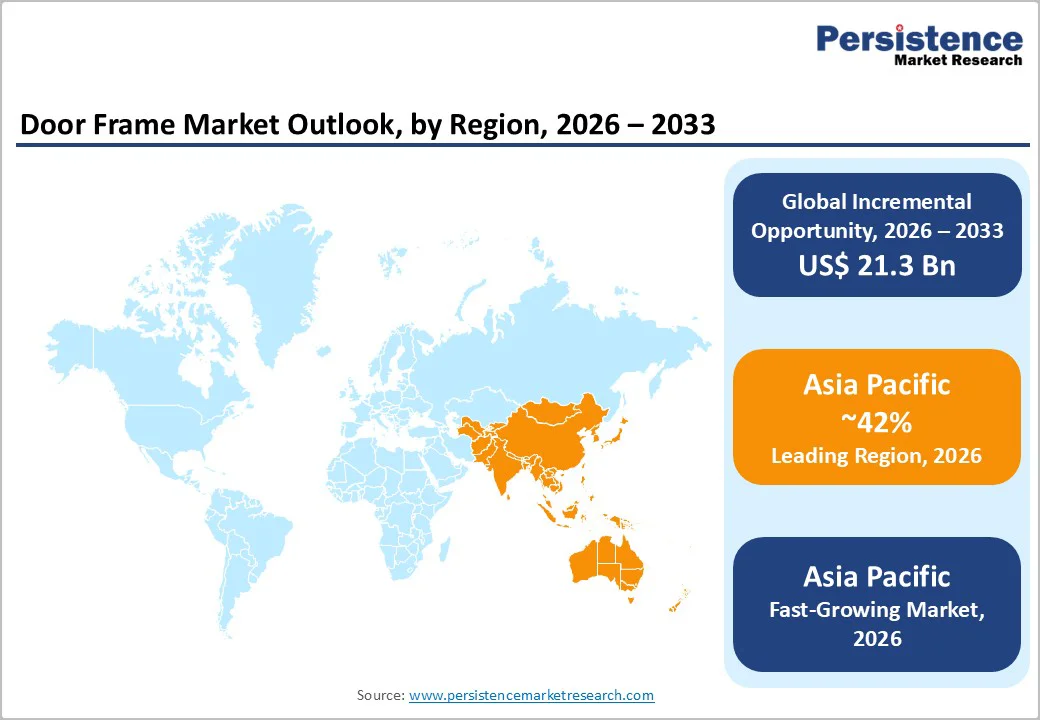

- Dominant Region: Asia Pacific is set to dominate with approximately 42% market share in 2026, supported by strong industrial growth and high regional demand for durable materials.

- Fastest-growing Market: The Asia Pacific door frame market is expected to expand the fastest through 2033, driven by growing adoption of durable, cost-effective construction materials.

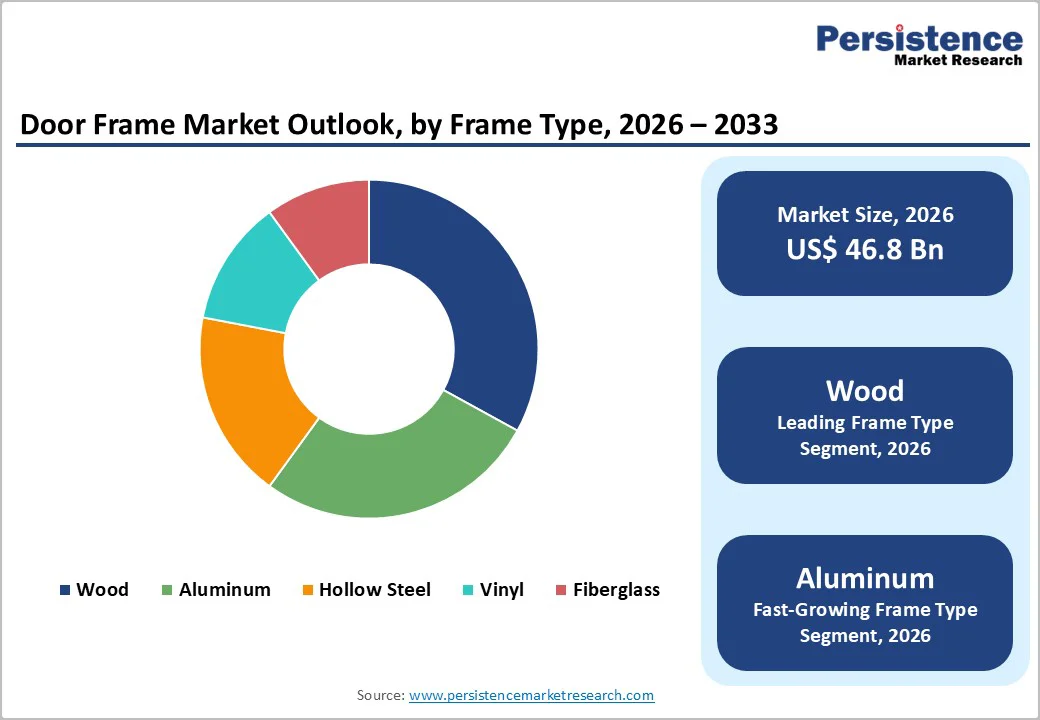

- Leading Frame Types: Wood frames are forecasted to capture 33% of the market in 2026, valued for their versatility, affordability, durability, and design adaptability.

- Fastest-growing Frame Types: Aluminum frames are projected to grow fastest from 2026 to 2033, preferred for their lightweight, durable, and corrosion-resistant design.

- November 2025: ASSA ABLOY acquired International Door Products (IDP), a US-based manufacturer of standard and custom fire-rated steel door frames, strengthening its North American offerings.

| Key Insights | Details |

|---|---|

| Door Frame Market Size (2026E) | US$ 46.8 Bn |

| Market Value Forecast (2033F) | US$ 68.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growing Demand for Energy-Efficient and Sustainable Materials

Rising focus on energy efficiency and sustainability in construction has become a critical factor influencing demand for advanced door frame materials. Regulatory frameworks targeting thermal performance, insulation, and carbon reduction are guiding material selection for residential and commercial projects. Builders increasingly adopt recycled aluminum, engineered wood, and composite solutions that enhance durability, reduce maintenance, and align with environmental standards. Consumer interest in environmentally responsible construction further accelerates adoption.

The economic advantages of energy-efficient and sustainable frames strengthen market growth. High-performance frames can lower energy consumption by up to 20%, reflecting measurable reductions in heating and cooling costs. Innovations in lightweight, corrosion-resistant, and recyclable materials provide performance without compromising design versatility. Manufacturers focus on integrating sustainable practices in production, optimizing supply chains, and promoting eco-friendly credentials to appeal to architects, contractors, and developers. As urbanization and regulatory pressures intensify, energy-efficient and sustainable door frame solutions continue to drive both adoption and market expansion.

Volatility in Raw Material Prices

Fluctuating costs of essential materials create a critical challenge for the door frame industry. Metals such as steel and aluminum, timber, and composite materials constitute major production inputs, and sudden price shifts directly affect manufacturing expenses. Escalating costs can compress profit margins, forcing manufacturers to adjust pricing strategies or absorb the increase, potentially slowing demand. In February 2025, prices for key steel products, including hot-rolled coil, declined by approximately 18% compared with the previous year, highlighting significant exposure to market instability. Such unpredictability complicates project budgeting and long-term planning for both producers and contractors.

Inventory and supply chain management are also impacted by material cost volatility. Manufacturers face risks of production delays and procurement inefficiencies, particularly smaller firms with limited capital to hedge against sudden price swings. Contracts may include price adjustment clauses, yet unanticipated market movements can still disrupt operations. To mitigate risks, companies explore alternative materials, strategic sourcing, and long-term agreements with suppliers. These measures aim to stabilize costs, maintain production schedules, and meet delivery expectations, ensuring smooth operations in an environment where raw material prices remain unpredictable.

Adoption of Sustainable and Smart Technologies

Integration of sustainable and smart technologies represents a significant growth opportunity in the door frame market, supported by evolving construction trends and regulatory standards. Use of recycled aluminum, engineered wood, and low-emission composites lowers environmental impact while meeting energy efficiency requirements. Smart systems such as automated locking, access control, and sensor-enabled frames enhance security and operational efficiency. Builders and developers increasingly adopt solutions that provide long-term performance, reduce maintenance needs, and comply with green building certifications. These technologies address the rising demand for environmentally responsible and high-performance building components.

Smart and sustainable innovations also differentiate offerings in a competitive environment. Customizable, technology-enabled frames allow seamless integration with modern architectural designs and intelligent building management systems. Rapid urbanization and increased focus on energy conservation elevate the demand for durable, efficient, and environmentally responsible materials. Manufacturers incorporating these technologies improve lifecycle performance, operational efficiency, and regulatory compliance, positioning products as advanced solutions for evolving construction and infrastructure requirements.

Category-wise Analysis

Frame Type Insights

Wood frames are poised to dominate, with a forecasted market share of 33% in 2026. Leadership arises from versatility, cost-effectiveness, and widespread adoption in residential construction. Wood frames provide aesthetic flexibility, enabling seamless integration with diverse architectural styles, while offering durability and ease of installation. Strong demand in both emerging and mature markets, including Asia Pacific and Latin America, continues to drive volume. Ongoing improvements in manufacturing techniques and surface treatments are expected to further enhance performance and appeal across residential and commercial projects.

Aluminum frames are estimated to be the fastest-growing segment from 2026 to 2033, due to their increasing adoption in commercial and institutional projects. Their lightweight nature, corrosion resistance, and alignment with energy-efficiency and fire-safety regulations enhance attractiveness in modern construction. Rising infrastructure investment and preference for low-maintenance, long-lasting frames support expansion. Growth is further reinforced by urban development in high-demand regions and technological improvements in extrusion and fabrication processes.

End-User Insights

Residential applications are anticipated to secure around 45% of the door frame market revenue share in 2026, driven by high installation rates per housing project and increasing activity in urban and suburban residential construction. Leadership in the residential segment is maintained. Affordable housing initiatives and rising urban migration support steady consumption of wood, vinyl, and composite frames. Residential projects prioritize aesthetic appeal, durability, and ease of installation, prompting manufacturers to offer customizable and pre-finished solutions. Continued innovation in materials and finishes is expected to sustain demand and strengthen the segment across diverse regions.

Commercial applications are likely to be the fastest-growing during the 2026-2033 forecast period, powered by expansion of office complexes, healthcare facilities, and educational institutions. Adoption focuses on fire-rated, reinforced, and energy-efficient frames to comply with regulatory standards and ensure long-term durability. Growth is further supported by modernization of commercial infrastructure, integration of smart and modular solutions, and increasing investment in urban development. Manufacturers emphasize design versatility, compliance certifications, and rapid deployment capabilities to capture evolving demand in the commercial sector.

Distribution Channel Insights

Offline retail is forecasted to maintain a dominant position, with an anticipated 55% of the door frame material market revenue share in 2026. The leadership of this segment is supported by the prevalent reliance on physical inspection, bulk procurement, and immediate availability of wood, aluminum, and steel frames. Contractors and developers favor offline outlets for quality verification, customization, and efficient bulk purchasing. Extensive dealer networks and regional showrooms enhance accessibility. Continuous improvements in supply chain efficiency and service quality are expected to further strengthen channel performance across key markets.

Direct sales are set to register the highest CAGR between 2026 and 2033, stimulated by increasing engagement of large construction firms with manufacturers. Direct procurement provides pricing stability, tailored specifications, and reliable supply for commercial and institutional projects. Growth is further reinforced by urban infrastructure expansion, modernization of office and healthcare facilities, and demand for customized solutions. Online ordering among small contractors and renovation projects complements this trend. Manufacturers leverage direct sales to strengthen relationships, streamline logistics, and deliver integrated solutions, establishing it as a high-growth distribution channel.

Regional Insights

North America Door Frame Market Trends

The North America door frame market is poised to experience steady growth driven by robust residential construction and commercial infrastructure projects. Regional demand is focused on wood, steel, fiberglass, and aluminum frames that balance strength, aesthetics, and energy efficiency. Compliance with building codes and fire safety standards shapes material and design choices, while smart home integration and advanced security features increasingly influence product development. Prefabricated and modular door frame solutions gain popularity for faster installation and reduced labor costs. Expansion in suburban housing and urban commercial developments further supports adoption, with manufacturers targeting both new construction and renovation projects to sustain consistent market demand.

Innovation in materials and finishes plays a critical role in the North America door frame industry. Automated production techniques, quality control measures, and sustainable manufacturing practices enhance efficiency and competitiveness. Strategic collaborations with distributors and construction companies expand market reach, while investment in lightweight, low-maintenance frames meets evolving consumer preferences. Renovation of older housing stock increases demand for replacement frames, and commercial developments require high-performance, durable door systems. Companies focus on product differentiation, superior service, and after-sales support to maintain strong positioning and address diverse market needs.

Europe Door Frame Market Trends

The Europe door frame market growth is fueled by advanced construction standards, strict building regulations, and strong emphasis on energy efficiency and safety. Residential and commercial construction projects increasingly require high-performance materials such as aluminum, steel, and engineered wood to meet sustainability and fire-resistance standards. Urban renovation projects and retrofitting of historical buildings have also bolstered demand for customized door frame solutions. Manufacturers in Europe emphasize durability, design flexibility, and compliance with environmental norms. Technological integration, including smart locking systems and modular designs, further differentiates products, catering to premium segments and sophisticated architectural requirements.

Key players in Europe focus on innovation, premium materials, and regulatory certifications to maintain competitiveness. Companies invest in R&D for lightweight and corrosion-resistant aluminum frames, sustainable composites, and enhanced thermal performance. Regional manufacturers leverage strong supply chains, local raw material access, and advanced fabrication techniques to reduce production costs and lead times. Strategic collaborations and acquisitions help expand product portfolios and reach niche markets. The European market balances high-quality, performance-oriented door frame offerings with growing sustainability trends, positioning manufacturers to serve both residential and commercial sectors effectively.

Asia Pacific Door Frame Market Trends

Asia Pacific is anticipated to be the leading and fastest-growing market through 2033, projected to capture an estimated 42% of the door frame market share in 2026, fueled by rapid urbanization, industrial expansion, and sustained demand in residential and commercial construction. High-density urban centers drive extensive housing requirements, while large-scale infrastructure projects, including airports, commercial complexes, and public facilities, are driven by demand for high-performance door frame solutions. Cost-effective, durable materials such as steel, aluminum, and unplasticized polyvinyl chloride (uPVC) align with regional construction economics, enabling manufacturers to scale efficiently. Proximity to raw material sources and expanding local fabrication facilities reduces lead times and production costs relative to other regions, strengthening competitive positioning.

Growth is further reinforced by increasing adoption of architectural standards prioritizing energy efficiency, fire safety, and aesthetic integration with building envelopes. Rising preference for modular and prefabricated construction enhances installation efficiency, stimulating demand for ready-to-install systems. Industrial output in China, India, and Southeast Asia supports deployment of innovative materials, including composite and lightweight metal frames. Government incentives for sustainable construction and industrial policies encouraging manufacturing investments amplify market expansion, ensuring the dominant position of Asia Pacific and attracting global and domestic players.

Competitive Landscape

The global door frame market structure remains moderately fragmented, with leading companies collectively controlling around 40% of the market share. International manufacturers operate alongside regional specialists to serve diverse end-use applications. Competition is driven by material innovation, fire and safety certifications, energy efficiency, and design aesthetics. Companies focus on supply chain reliability, customization capabilities, and sustainable production practices to differentiate their offerings. Emerging markets and urbanization trends continue to attract investments, while technological integration, such as smart locking systems, enhances competitive positioning.

Key players, including ASSA ABLOY, ensun GmbH, Therma-Tru Corp., Pella Corporation, and Owens Corning, dominate premium segments while smaller regional players target niche and cost-sensitive applications. ASSA ABLOY emphasizes security and durability, ensun GmbH focuses on precision steel systems, Therma-Tru offers integrated residential solutions, Pella Corporation leads in energy-efficient designs, and Owens Corning specializes in composite and fiberglass frames. Strategic mergers, acquisitions, and R&D investments remain central to maintaining market leadership and expanding geographical reach.

Key Industry Developments

- In December 2025, CDF Distributors invested US$ 26?million to expand its manufacturing and distribution hub in Gallatin, Tennessee, creating 85 new jobs and strengthening production capacity for commercial doors and frames.

- In November 2025, SBM Gold, known for HDPE pipes and water tanks, expanded into premium uPVC doors and windows tailored for Indian climates, offering better insulation, durability and low maintenance for modern homes.

- In September 2025, Fleetwood Windows & Doors launched the 4400 Wood Pivot Door, its first wood-panel pivot entry, combining natural wood aesthetics with aluminum framing and customizable designs for luxury residential projects.

Frequently Asked Questions

The global door frame market is projected to reach US$ 46.8 billion in 2026.

Growth in residential and commercial construction, infrastructure development, and strong demand for durable, energy-efficient, and high-performance materials are factors driving the market.

The market is poised to witness a CAGR of 5.5% from 2026 to 2033.

Adoption of sustainable materials, smart technologies, and high-performance, low-maintenance door frame solutions across residential and commercial sectors are creating market opportunities.

Some of the key market players include ASSA ABLOY, ensun GmbH, Therma-Tru Corp., Pella Corporation, and JELD-WEN, Inc.