- Nutraceuticals & Functional Foods

- General Well-Being Dietary Supplements Market

General Well-Being Dietary Supplements Market Size, Share, and Growth Forecast 2026 - 2033

General Well-Being Dietary Supplements Market by Supplement Type (Vitamins, Minerals, Herbal Supplements, Proteins & Omega-3, Probiotics), by Form (Tablets, Capsules, Powders, Gummies, Liquids), by Distribution Channel (Pharmacies & Drug Stores, Health & Beauty Stores, Specialty Stores, Online Sales, Others), and Regional Analysis, 2026 - 2033

General Well-being Dietary Supplements Market Share and Trends Analysis

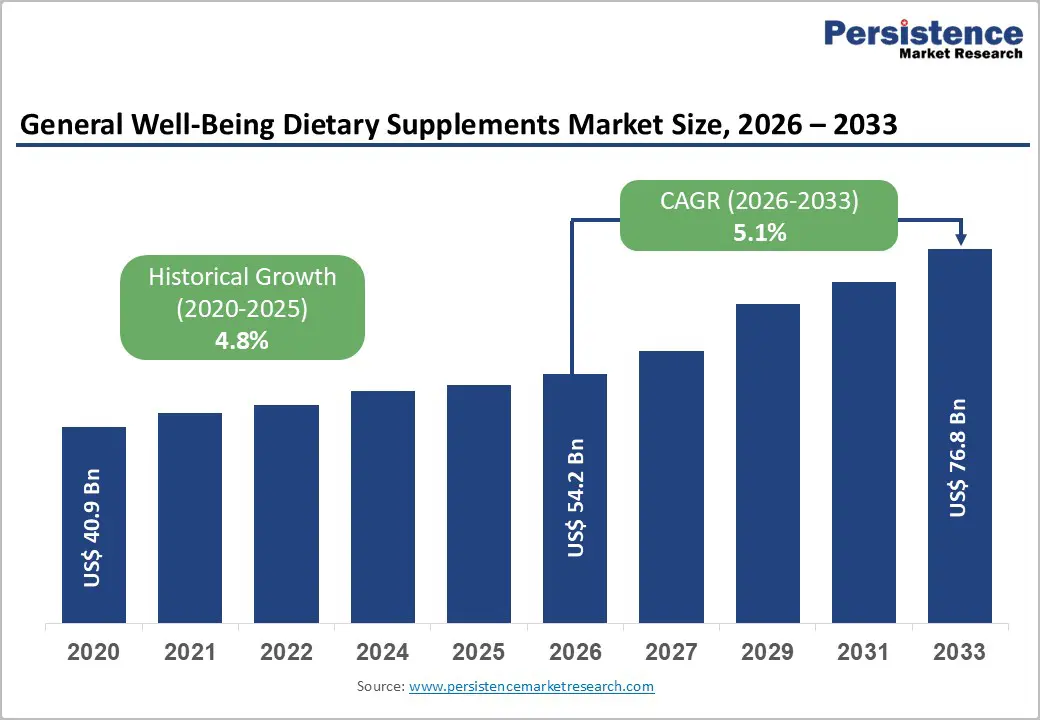

The global general well-being dietary supplements market size is expected to be valued at US$ 54.2 billion in 2026 and projected to reach US$ 76.8 billion by 2033, growing at a CAGR of 5.1% between 2026 and 2033.

Robust expansion is supported by rising adoption of preventive health practices, widespread use of supplements across age groups, and the normalization of multivitamin and specialty supplement intake as part of daily wellness routines. Growing evidence that general dietary supplements help close micronutrient gaps, combined with heightened health awareness after the COVID-19 pandemic, is encouraging consumers to invest in general well-being products for immunity, energy, stress management, and healthy ageing. The market also benefits from broader access through e-commerce, subscription models, and omnichannel retail formats, making supplements more convenient and affordable.

Key Industry Highlights:

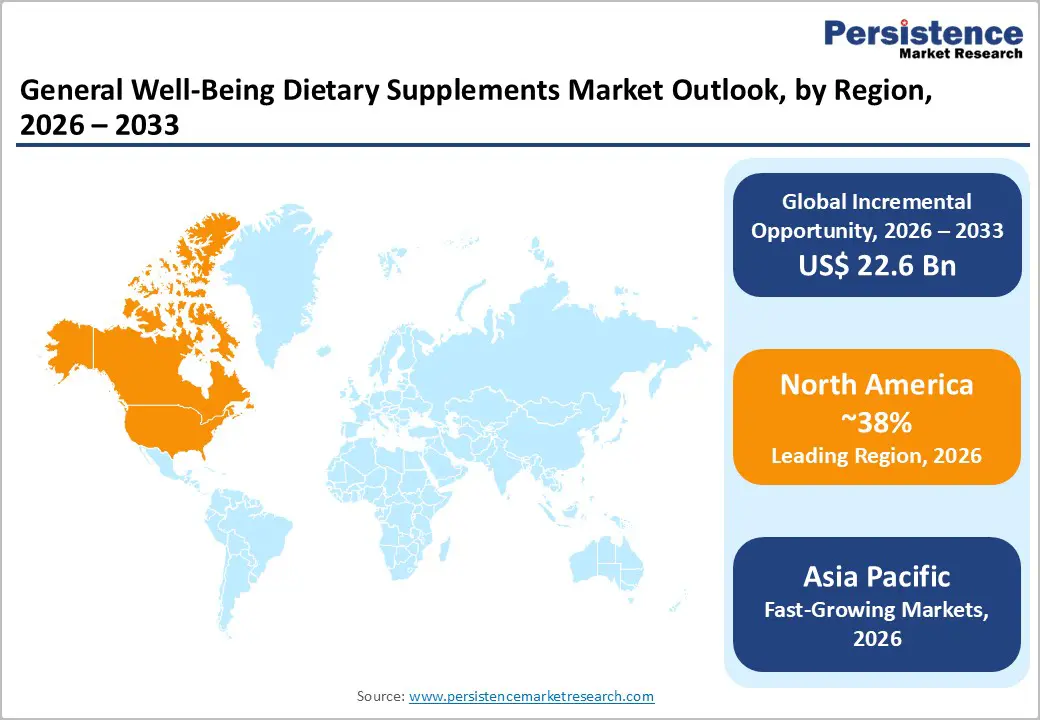

- North America remains the leading region in the general well-being dietary supplements market, with an estimated 38% share of global revenues in 2025, driven by high supplement penetration, strong purchasing power, and a mature regulatory and retail ecosystem supporting innovation and trust.

- Asia Pacific is projected to be the fastest-growing region between 2026 and 2033, fueled by rising incomes, rapid adoption of e-commerce and social commerce, where over 50% of supplement transactions are already online in some markets, and a longstanding cultural affinity for nutraceutical and herbal products.

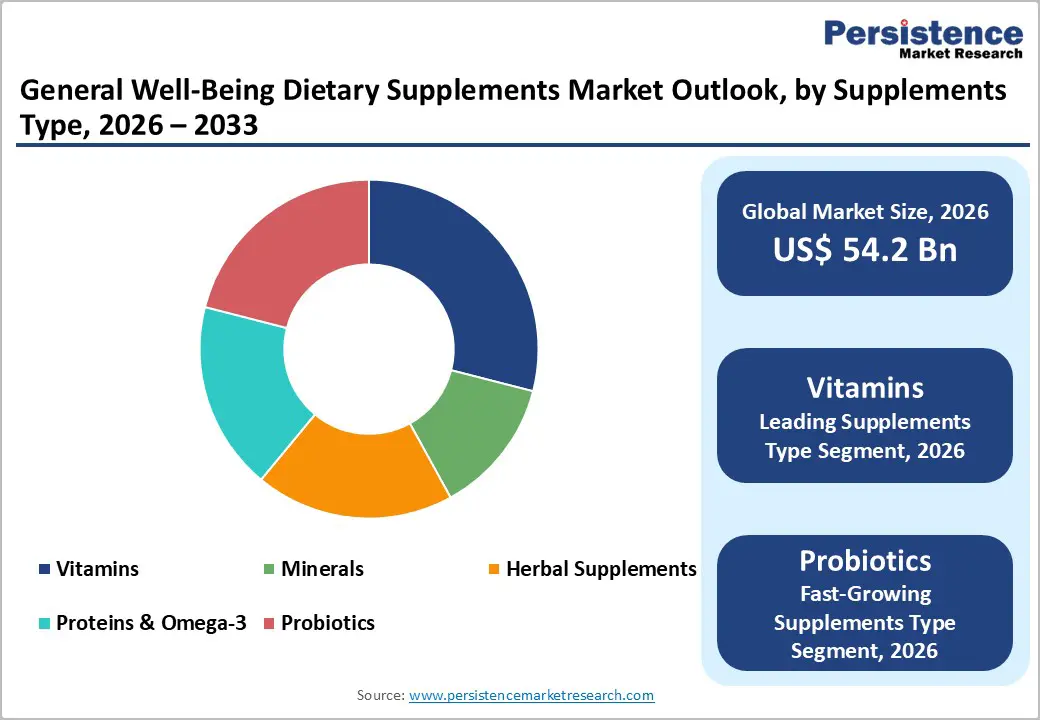

- Within supplement types, vitamins form the dominant segment, holding about 29% share in 2025, supported by strong evidence that multivitamin-mineral products are the most commonly used supplements among adults in both North America and Europe and are widely recommended for addressing micronutrient gaps.

- Among emerging categories, probiotics and gut-health-focused formulations are among the fastest-growing, supported by expanding research on the gut-immune and gut-brain axes, increasing consumer interest in digestive comfort, and the positioning of microbiome support as central to overall well-being.

- A key market opportunity lies in personalized, digital-first wellness ecosystems that combine science-backed supplement portfolios with online assessments, biomarker integration, subscription models, and omnichannel fulfillment to deliver tailored general well-being regimens across diverse demographic and lifestyle segments.

| Key Insights | Details |

|---|---|

| General Well-Being Dietary Supplements Market Size (2026E) | US$ 54.2 billion |

| Market Value Forecast (2033F) | US$ 76.8 billion |

| Projected Growth CAGR (2026 - 2033) | 5.1% |

| Historical Market Growth (2020 - 2025) | 4.8% |

Market Dynamics

Drivers - Rising preventive health focus and everyday supplement use

A structural shift toward preventive healthcare is a primary growth engine for the general well-being dietary supplements market. In the United States, analysis of NHANES 2017-2018 data by the Centers for Disease Control and Prevention (CDC) showed that 57.6% of adults aged 20 and over used at least one dietary supplement in the past 30 days, with usage rising to 80.2% among women aged 60 and above. More recent federal monitoring confirms that nearly 3 in 5 U.S. adults consumed dietary supplements during 2017-March 2020, indicating that supplements are now firmly mainstream. In Europe, harmonized reviews of national nutrition surveys report that adult dietary supplement use exceeds 40% in several countries, including Finland, Denmark, Switzerland, and the Netherlands, reflecting normalization of vitamins, minerals, omega-3 fatty acids, and probiotics as part of daily wellness routines. This sustained, high baseline of usage directly supports demand for general well-being formulations focused on immunity, vitality, and stress resilience.

Aging population and widening nutrient gaps

Global demographic aging is another powerful catalyst for general well-being dietary supplements. A comprehensive international review highlights that older adults are among the heaviest users of vitamins, minerals, and other supplements, motivated by concerns about bone density, cardiovascular health, cognitive performance, and overall vitality. U.S. federal monitoring through NHANES and the National Center for Health Statistics shows that supplement use increases steadily with age and income, and that multivitamin-mineral products are the most commonly consumed category among adults. In Europe, national surveys across Finland, Denmark, Belgium, Germany, and other countries show that more than 50% of adults use dietary supplements, with particularly high adoption among older cohorts. As life expectancy rises and lifestyle-related conditions such as obesity, type 2 diabetes, and cardiovascular disease become more prevalent, general well-being supplements that support healthy aging, metabolic health, and micronutrient sufficiency are expected to see sustained, long-term demand.

Restraints - Regulatory complexity and inconsistent global oversight

Regulatory fragmentation across countries remains a key barrier to seamless market expansion for general well-being dietary supplements. A global review of regulations shows that supplements are variously classified as foods, a distinct category between foods and medicines, or quasi-pharmaceuticals, leading to divergent requirements for safety evaluation, pre-market notification, and health claims. For example, in the United States, the Dietary Supplement Health and Education Act (DSHEA) framework permits broad market access and structure-function claims under post-market oversight by the Food and Drug Administration (FDA) and the Federal Trade Commission (FTC), whereas in the European Union, nutrition and health claims on supplements must undergo scientific evaluation by the European Food Safety Authority (EFSA) and comply with strict labeling rules. These inconsistencies increase compliance costs, delay cross-border launches, and complicate global brand harmonization, particularly for products positioned around general well-being benefits.

Safety concerns, adulteration risks, and misinformation

Persistent concerns about product safety, adulteration, and misleading marketing also restrain market growth. Regulatory and scientific reviews document instances in which supplements contain nutrients at levels above tolerable upper intake levels, undeclared pharmacologically active substances, or contaminants when good manufacturing practices are not rigorously followed. U.S. national statistics show that multivitamin/mineral and vitamin D supplements often provide 100% or more of the recommended daily intake, underscoring the need for responsible formulation and clear consumer guidance. At the same time, some online marketing overstates benefits or implies disease treatment, contravening regulatory standards and eroding consumer trust. These issues can trigger heightened regulatory scrutiny, foster skepticism among healthcare professionals, and increase demand for third-party testing, certifications, and transparent labeling, raising entry barriers for smaller or less sophisticated players.

Opportunities - Personalized nutrition, digital health, and data-driven supplementation

The convergence of nutrition science, digital health, and data analytics is creating substantial opportunities in general well-being dietary supplements. Global leaders are investing in personalized supplement platforms that use online questionnaires, biometric data, and subscription models to tailor multivitamin, mineral, and specialty formulas to individual needs. Bayer AG’s acquisition of a majority stake in Care/of, a direct-to-consumer personalized nutrition company, has strengthened its presence in customized vitamin packs and provided access to rich consumer-behavior data for product development and targeting. In parallel, Nestlé Health Science launched a dedicated GLP-1 nutrition support platform in 2024 to provide nutritional guidance and product bundles, including supplements, for individuals on weight-management therapies, illustrating how companion solutions around metabolic and weight health can expand the general well-being space. As consumers increasingly seek tailored regimens for stress, sleep, energy, and metabolic support, companies that combine robust clinical evidence with digital tools, coaching, and adaptive recommendations are positioned for above-average growth in this segment.

E-commerce acceleration and omnichannel distribution models

Rapid expansion of e-commerce and direct-to-consumer (DTC) models is reshaping distribution strategies for general well-being dietary supplements. Analyses of global supplement channels indicate that DTC now accounts for roughly 29% of supplement sales in North America, up from about 16% in 2020, while in parts of Asia-Pacific, more than 50% of supplement transactions already occur online via platforms such as Tmall, JD.com, Shopee, and Lazada. Research on purchasing behavior finds that about 50% of U.S. vitamin and mineral supplement users reported shopping more online during the COVID-19 pandemic, firmly establishing digital as a core purchasing channel for everyday wellness products. At the same time, specialty retailers, mass-market pharmacies, and supermarkets are evolving into omnichannel hubs, integrating in-store counseling with click-and-collect, subscription refills, and loyalty apps for supplements. This diversification of channels expands reach, supports premiumization, and enables rapid testing of novel formats such as gummies, shots, and sachets specifically positioned for general well-being use cases.

Category-wise Analysis

Supplements Type Insights

Vitamins are expected to remain the leading supplement type in the general well-being dietary supplements market, accounting for an estimated 29% share of global revenues in 2025. Multiple surveillance reports from the CDC, the National Health and Nutrition Examination Survey (NHANES), and the National Institutes of Health (NIH) Office of Dietary Supplements (ODS) consistently identify multivitamin-mineral products as the most commonly used dietary supplements among U.S. adults, ahead of botanicals or single nutrients. In Europe, national surveys compiled across Finland, Denmark, Switzerland, the Netherlands, and Belgium also report high use of vitamin- and mineral-based supplements relative to other categories, often exceeding 30-40% of adults. This strong evidence base for addressing micronutrient gaps, together with simple, high-awareness positioning around immunity, energy, and fatigue reduction, underpins the category’s leadership, while probiotics emerge as the fastest-growing segment focused on gut and holistic well-being.

Distribution Channel Insights

Pharmacies and drug stores are anticipated to remain the leading distribution channel, with an estimated 36% share of global general well-being dietary supplement sales in 2025, even as online channels grow faster. Analyses of the retail pharmacy sector indicate that chain pharmacies and mass retailers collectively account for a large share of health-and-wellness transactions, benefiting from high foot traffic, pharmacist counseling, and strong private-label and branded supplement portfolios. Historical channel data show that natural and specialty brick-and-mortar outlets once dominated dietary supplement sales, but e-commerce and mass-market channels have rapidly caught up; projections for 2025 suggest rough parity among natural/specialty retail, online, and mass channels for supplements. Consumer surveys further reveal that nearly 30% of shoppers intend to increase online purchasing for drug-store needs, indicating that pharmacies and drug stores will increasingly function as part of an omnichannel journey that includes online marketplaces, brand websites, and subscription models, with online sales recognized as the fastest-growing distribution segment.

Regional Insights

North America General Well-Being Dietary Supplements Market Trends and Insights

North America is the leading regional market, representing an estimated 38% share of global general well-being dietary supplements revenue in 2025, underpinned by high supplement penetration, purchasing power, and a mature regulatory framework. U.S. federal statistics show that nearly 60% of adults use at least one dietary supplement, with prevalence rising to over 70-80% among older adults, confirming deep integration of supplements into daily health routines. Longitudinal NHANES analyses demonstrate that overall dietary supplement use in the U.S. increased from about 50% of the population in 2007 to 56% in 2018, with multivitamin-mineral products consistently the leading category. The DSHEA framework places responsibility for safety and labeling on manufacturers while enabling the FDA and FTC to oversee post-market safety and claims, creating a dynamic innovation ecosystem for general well-being products.

Within this environment, companies such as Amway Corporation, Herbalife Ltd., Abbott Laboratories, Bayer AG, Haleon plc, and Nestlé Health Science emphasize science-backed formulations, high-quality manufacturing, and consumer education to reinforce trust. Bayer’s majority stake in personalized nutrition player Care/of exemplifies the region’s leadership in tailored supplement regimens, while Nestlé Health Science’s GLP-1 nutrition support platform demonstrates the integration of supplements into broader metabolic and weight-management journeys. E-commerce penetration is also high, with research showing that around 50% of U.S. vitamin and mineral supplement users reported shifting more purchases online during the COVID-19 pandemic, strengthening omnichannel models that combine retail pharmacy strengths with digital convenience and subscriptions.

Asia Pacific General Well-Being Dietary Supplements Market Trends and Insights

Asia Pacific is expected to be the fastest-growing region for general well-being dietary supplements through 2033, propelled by rapid urbanization, rising disposable incomes, and strong cultural acceptance of herbal and traditional remedies. Regional analyses show a pronounced rise in supplement use driven by greater awareness of nutritional deficiencies, the growing incidence of lifestyle diseases, and the popularity of functional foods and nutraceuticals among middle-class and younger consumers in China, Japan, India, and key ASEAN markets. Consumers increasingly adopt vitamins, minerals, herbal tonics, and probiotics for day-to-day goals such as stress management, immunity, and energy, often complementing conventional diets with both Western-style and traditional formulations.

The region also benefits from strong manufacturing bases in China, India, and parts of Southeast Asia, which supply domestic needs and export markets for a wide range of general well-being supplements. E-commerce is a standout growth driver: analyses of global supplement channels suggest that in parts of Asia, more than 50% of supplement transactions already take place online, with platforms like Tmall, JD.com, Shopee, and Lazada as well as social-commerce formats enabling rapid scaling of new brands and cross-border offerings. This digital-first environment supports fast experimentation with novel formats and targeted formulations for immunity, digestive comfort, and energy. As regulators tighten quality and labeling standards and large multinationals deepen partnerships with local champions, Asia Pacific is set to deliver the highest regional CAGR for general well-being dietary supplements over the forecast period.

Competitive Landscape

The general well-being dietary supplements market is highly fragmented and competitive, characterized by the presence of global pharmaceutical, nutrition, and FMCG players alongside regional and niche brands. Leading companies focus on product innovation, clean-label formulations, and personalized nutrition to differentiate themselves. Strong distribution networks, especially e-commerce and direct selling, play a crucial role in market penetration. Companies are increasingly investing in scientific validation and branding to build consumer trust.

Key Market Developments

- In February 2026, Vitux expanded its Concordix chewable emulsion delivery technology by securing an extension of a key U.S. patent, strengthening its intellectual property position and partner confidence. The company also introduced over 60 launch-ready nutraceutical concepts across areas such as immunity, longevity, children’s health, and general well-being.

- In July 2025, Herbalife announced the launch of MultiBurn™, a next-generation weight management dietary supplement formulated with clinically studied botanical extracts to support metabolic health, weight loss, healthy fat reduction, and energy expenditure.

Companies Covered in General Well-Being Dietary Supplements Market

- Amway Corporation

- Herbalife Ltd.

- Nestlé S.A.

- Bayer AG

- Abbott Laboratories

- Haleon plc

- Glanbia plc

- Otsuka Holdings Co. Ltd.

- Suntory Holdings Ltd.

- Now Health Group Inc.

- Vitabiotics Ltd.

- Reckitt Benckiser Group plc

- Pfizer Inc.

- Nature’s Bounty (The Bountiful Company)

- Church & Dwight Co., Inc., Blackmores Limited

Frequently Asked Questions

The global general well-being dietary supplements market is projected to reach around US$ 54.2 billion in 2026, reflecting steady growth driven by entrenched preventive health behaviors, high supplement usage across demographics, and broad access via retail pharmacies and digital channels.

A key demand driver is rising preventive health awareness, as consumers increasingly use vitamins, minerals, probiotics, and herbal products to address micronutrient gaps, support immunity, enhance energy, and manage stress as part of everyday wellness routines.

North America currently leads the global general well-being dietary supplements market, with an estimated 38% share of worldwide revenues in 2025, supported by high supplement penetration, strong purchasing power, and a well-established regulatory and retail infrastructure.

A major opportunity lies in personalized, digital-first wellness ecosystems that use online assessments, data analytics, and subscription models to deliver tailored supplement regimens, integrating general well-being products with coaching, tracking, and omnichannel fulfillment for higher engagement and lifetime value.

Key players include Amway Corporation, Herbalife Ltd., Nestlé S.A., Bayer AG, Abbott Laboratories, Haleon plc, Glanbia plc, Otsuka Holdings Co. Ltd., Suntory Holdings Ltd., Now Health Group Inc., Vitabiotics Ltd., and Reckitt Benckiser Group plc, alongside several regional specialists and emerging digital-native brands.