- Industrial Goods & Service

- Dewatering Pump Market

Dewatering Pump Market Size, Share, and Growth Forecast for 2025 - 2032

Dewatering Pump Market by Flow Rate (Up to 250 GPM, 250 to 1000 GPM, 1000 to 5000 GPM, and Above 5000 GPM), Head Capacity (Up to 30m, 30 to 100m, and Above 100m), Technology (Centrifugal, Positive Displacement, and Diaphragm), Drive Type, Industry, and Regional Analysis from 2025 to 2032

Dewatering Pump Market Size and Share Analysis

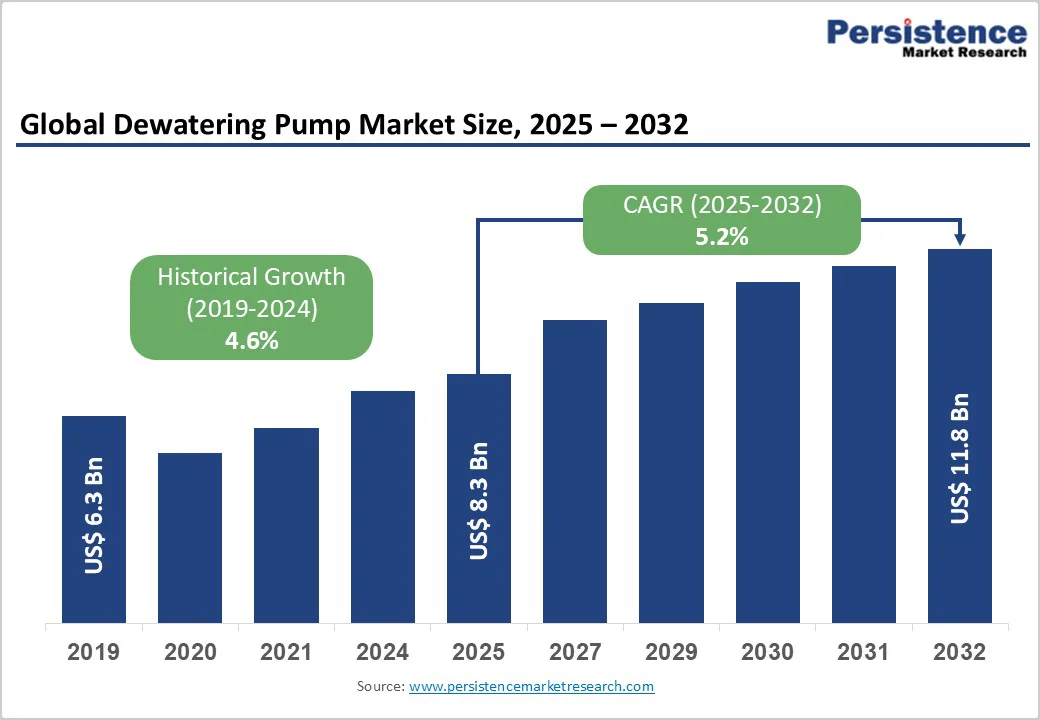

The global dewatering pump market size was valued at US$ 8.3 billion in 2025 and is projected to reach US$ 11.8 billion, growing at a CAGR of 5.2% between 2025 and 2032. Rise in global construction activities and continued expansion of the mining industry, particularly in the Asia Pacific are some of the key factors driving the sales of the dewatering pumps. Development of energy-efficient pump systems and integration of smart controls, IoT, remote monitoring, and automation in dewatering equipment further stimulates market growth.

Key Industry Highlights:

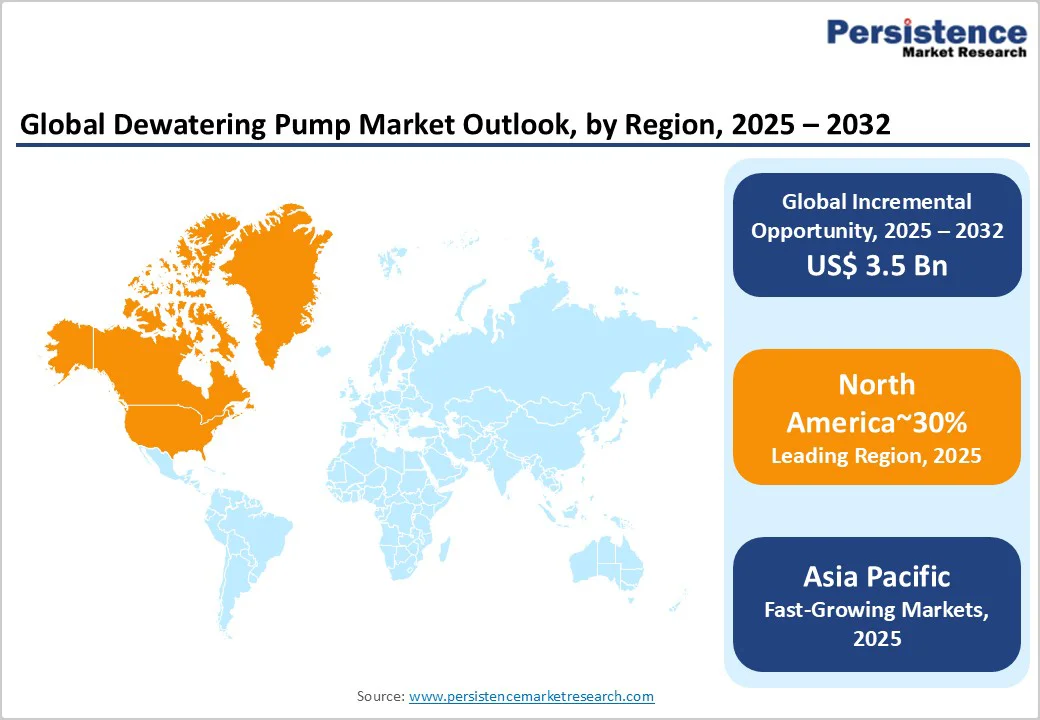

- Regional Leaders: North America maintains regional market leadership with mature construction infrastructure, robust regulatory frameworks emphasizing environmental compliance, and the established presence of technology leaders.

- Fastest-Growing Region: Asia Pacific represents fastest growth at 5.6% CAGR, driven by China and India construction expansion, mining sector development, and urbanization.

- Leading Flow Rate Segments: 1000 to 5000 GPM flow rate dominates at 38% market share, serving mid-to-large scale applications across construction and mining with optimal capacity-cost balance supporting diverse global dewatering requirements.

- Head Capacity Segment: 30 to 100m head capacity leads market at 44% share, representing optimal performance range for standard infrastructure applications with proven reliability and cost-effectiveness supporting widespread commercial adoption across construction projects globally.

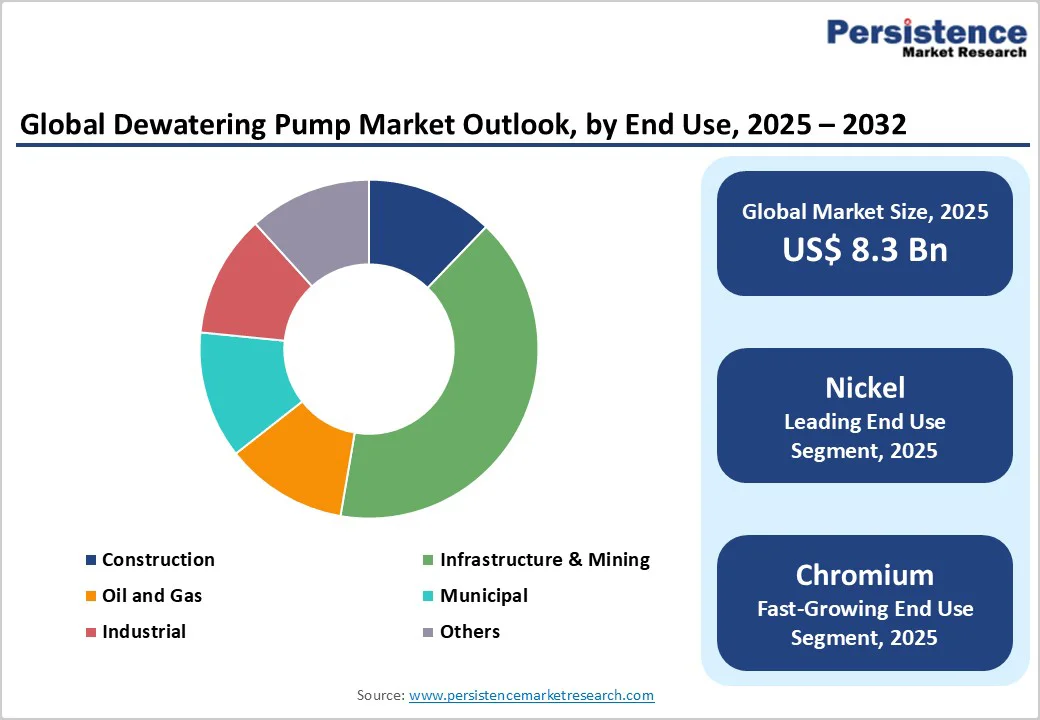

- Application Segment: Infrastructure & Mining applications dominate dewatering pump utilization with approximately 37% market share, representing critical water management requirements.

- Market Opportunity: Rapid agricultural modernization across emerging economies creates substantial opportunities for dewatering pumps for irrigation system development.

| Key Insights | Details |

|---|---|

| Dewatering Pump Market Size (2025E) | US$ 8.3 Bn |

| Projected Market Value (2032F) | US$ 11.8 Bn |

| Global Market Growth Rate (CAGR 2025 to 2032) | 5.2% |

| Historical Market Growth Rate (CAGR 2019 to 2024) | 4.6% |

Market Dynamics

Drivers - Accelerating Global Infrastructure and Construction Development Programs

Global infrastructure investments demonstrate unprecedented momentum, with governments prioritizing transportation, water management, and urban development projects requiring comprehensive dewatering solutions. The United States construction sector alone shows robust growth driven by Interstate Highway System modernization, bridge reconstruction, and residential complex development, necessitating sophisticated groundwater control systems. Construction activity projections indicate that China, India, the United States, and Indonesia will account for 60% of global construction growth through 2030, directly correlating with dewatering pump demand expansion.

Groundwater management during excavation represents a critical foundation stability requirement, with dewatering preventing seepage-related failures and ensuring structural integrity across complex construction environments. Government infrastructure stimulus programs, including the US Infrastructure Investment and Jobs Act (IIJA), which allocates $110 billion toward transportation and water infrastructure, directly translate to sustained dewatering equipment procurement across federal, state, and municipal projects supporting consistent market expansion through 2032.

Rising Investments in Wastewater Treatment and Urban Infrastructure Fuel Market Growth

Expanding wastewater treatment infrastructure and rapid urban development strongly drive the global dewatering pump market. Governments and private sectors worldwide are investing heavily in modernizing sewage networks, stormwater systems, and industrial effluent treatment facilities to meet environmental regulations and urban population needs. Dewatering pumps play a critical role in these projects by managing sludge, removing excess water, and ensuring the smooth operation of treatment plants. Cities in Asia Pacific, Europe, and North America are upgrading drainage and sanitation systems to handle increasing wastewater volumes, creating strong recurring demand for reliable and energy-efficient pumps.

The robust expansion of smart city initiatives and industrial parks requires efficient groundwater control and drainage management solutions. The growing emphasis on sustainable water management and regulatory compliance accelerates pump adoption, as industries and municipalities seek advanced, automated dewatering technologies to improve efficiency, reduce downtime, and maintain environmental safety standards.

Restraint - High Maintenance and Operational Costs Limit Market Growth

High maintenance and operational costs restrain the growth of the global dewatering pump market. Dewatering pumps operate in demanding environments such as mining, construction, and wastewater treatment, where they handle abrasive materials, sediments, and fluctuating water levels. These harsh conditions increase wear on impellers, seals, and bearings, forcing operators to conduct frequent repairs and replacements. Energy consumption adds further costs, especially for high-capacity electric and diesel-driven pumps that run continuously.

When technicians neglect regular servicing or use substandard components, performance drops and downtime rise, leading to productivity losses. In developing regions, limited access to spare parts and trained personnel makes maintenance even more expensive and time-consuming. Many small and medium contractors, therefore, avoid investing in advanced pump systems, choosing cheaper short-term options instead. This cost burden directly reduces market adoption, creating a major barrier to widespread deployment of efficient dewatering technologies worldwide.

Opportunity - Mining Sector Expansion and Critical Water Management Requirements

The global mining industry faces escalating water management demands driven by deeper extraction, environmental remediation requirements, and operational safety imperatives, creating exceptional growth opportunities for advanced dewatering solutions. Coal production sustaining global energy systems, with China accounting for 65% of global coal production, followed by the United States, Russia, India, and Germany, demands sophisticated underground water management to prevent flooded tunnels, unstable ground conditions, and catastrophic safety incidents.

Mining segment dewatering pump demand projects a 6.8% CAGR through 2032, representing approximately US$ 4.8 billion annual market value driven by mineral extraction expansion, deep underground mining development, and environmental compliance requirements. Strategic investments in sustainable mining practices incorporating advanced water recycling and treatment technologies create premium market opportunities for manufacturers offering environmentally compliant, high-reliability dewatering systems supporting operational continuity while meeting regulatory discharge standards and corporate sustainability commitments aligned with emerging market environmental policies.

Agricultural Sector Mechanization and Irrigation Infrastructure Development

Rapid agricultural modernization across emerging economies, including India, Southeast Asia, and Latin America, creates substantial dewatering pump demand for irrigation system development, excess water drainage from flooded fields, and agricultural productivity enhancement. Global urbanization and rising food security pressures drive investments in agricultural infrastructure and irrigation systems using dewatering pumps for groundwater management and field drainage optimization.

Agricultural application dewatering pumps project 5.2% CAGR through 2032, representing expanding opportunities for manufacturers offering cost-effective, energy-efficient solutions optimized for agricultural field conditions. Government irrigation subsidies and agricultural development programs in India, targeting 80 million hectares by 2032, directly support pump procurement across emerging agricultural sectors, creating distributed growth opportunities across diverse geographic markets, supporting market expansion through cumulative agricultural end-user demand.

Category-wise Analysis

Flow Rate Insights

The 1000 to 5000 GPM flow rate segment commands approximately 38% market share, serving mid-to-large scale dewatering applications across construction sites, mining operations, and municipal water management projects requiring balanced capacity and operational flexibility. This segment demonstrates optimal performance across diverse application requirements, delivering sufficient pumping capacity for substantial water removal while maintaining operational efficiency and cost-effectiveness relative to larger-capacity alternatives. Standard construction sites generating approximately 500-2000 GPM dewatering requirements align with this segment's capabilities, supporting routine excavation, foundation preparation, and groundwater control applications across global construction projects.

Above 5000 GPM ultra-high-capacity systems represent the fastest-growing segment at 5.8% CAGR, driven by massive mining operations, large-scale infrastructure projects, and emergency flood response scenarios demanding extreme-volume water removal capabilities. Companies including Sulzer, Xylem, and Grundfos maintain substantial market share within this premium segment through specialized engineering expertise and proven high-volume system reliability supporting mission-critical applications where operational continuity represents paramount concern.

Technology Analysis

Centrifugal pump technology dominates the dewatering market with approximately 62% market share, driven by widespread applicability across diverse dewatering requirements, operational simplicity, high-volume capacity handling, and proven reliability across construction and municipal applications. Centrifugal pumps utilize rotating impellers generating centrifugal force enabling efficient water movement, cost-effective manufacturing, and straightforward maintenance accessibility supporting user adoption across equipment operators with varying technical expertise.

Positive displacement pumps command 23% market share, serving applications requiring precise flow control, ability to handle abrasive slurries, and operational performance in challenging contaminated water environments typical of mining and industrial dewatering scenarios.

Industry Analysis

Infrastructure & mining applications dominate dewatering pump utilization with approximately 37% market share, representing critical water management requirements for operational safety, structural stability, and productivity optimization across mining pit dewatering, underground tunnel operations, and large-scale infrastructure excavation.

Construction applications account for 29% market share, encompassing building foundation dewatering, site preparation, groundwater control, and emergency water removal, supporting project timeline adherence and worker safety across diverse construction environments.

Regional Insights

North America Dewatering Pump Market Trends

North America represents a mature, well-established dewatering pump market driven by substantial construction activity, robust regulatory frameworks emphasizing environmental compliance, and sophisticated technical requirements demanding advanced pump solutions. The United States construction sector, valued at approximately US$ 1.9 trillion annually, generates consistent dewatering pump demand through infrastructure modernization, residential development, and commercial facility expansion, particularly concentrated in Texas, California, Florida, and New York, experiencing significant water management requirements.

EPA regulatory frameworks and environmental discharge standards mandate the adoption of environmentally compliant dewatering systems, supporting premium market positioning for advanced solutions incorporating real-time monitoring, efficient filtration, and sustainable water management practices. Infrastructure investments through the Bipartisan Infrastructure Law allocate substantial federal funding toward transportation, water infrastructure, and climate resilience projects, creating multi-year dewatering equipment procurement cycles supporting equipment manufacturer revenue stability through 2032.

Europe Dewatering Pump Market Trends

Europe demonstrates steady dewatering pump demand driven by mature infrastructure networks requiring modernization, stringent EU environmental regulations mandating sustainable water management practices, and regulatory harmonization across member states supporting consistent technical standards. German automotive and manufacturing sectors, combined with significant construction activities across France, Spain, and the United Kingdom generate commercial dewatering requirements supporting equipment utilization across diverse industrial applications and construction projects.

EU Water Framework Directive requirements and REACH chemical regulations enforce the adoption of environmentally compliant dewatering systems with advanced filtration, wastewater treatment capabilities, and emissions reduction features supporting premium product positioning. Germany leads European dewatering pump demand at approximately US$ 2.8 billion annually, benefiting from a sophisticated industrial base, stringent engineering standards, and environmental compliance emphasis supporting advanced technology adoption.

Asia Pacific Dewatering Pump Market Trends

Asia Pacific represents the fastest-growing regional dewatering pump market, commanding approximately 35.9% global market share in 2024, driven by massive construction activities across China, India, Southeast Asia, and mining sector expansion supporting industrial water management requirements. China's construction sector, valued at approximately US$ 5.8 trillion annually, represents the world's largest construction market, generating substantial dewatering pump demand through high-rise building development, infrastructure modernization, and mining operations, supporting consistent market expansion through 2032.

India demonstrates exceptional growth at 6.8% CAGR through 2032, driven by rapid urbanization with projected urban population reaching 40% by 2032, government infrastructure development initiatives, and agricultural sector modernization, creating sustained dewatering equipment demand. Mining sector expansion across Southeast Asia, India, and Australia, targeting mineral and coal extraction, drives 37% market share concentration within infrastructure & mining applications, supporting specialized high-capacity dewatering system demand.

Competitive Landscape for the Dewatering Pump Market

The global dewatering pump market demonstrates moderately consolidated characteristics with approximately 15-20 competitors controlling substantial market segments, where the top three companies (Xylem, Grundfos, Sulzer) control approximately 20-25% global market share through established technology platforms and extensive industrial relationships. High barriers to entry reflecting significant R&D investments, regulatory compliance expertise, manufacturing scale requirements, and specialized technical knowledge concentrate competitive advantages among well-capitalized multinational corporations and technology specialists.

Market leaders compete through comprehensive pump solution portfolios, advanced technology differentiation, including IoT integration and AI-powered predictive analytics, and established customer relationships rather than commodity-based pricing competition. Regional competitors, including Ebara Corporation, KSB SE & Co. KGaA, and emerging manufacturers from the Asia Pacific, compete through specialized solutions, strong regional presence, and cost-effective technologies, capturing price-sensitive market segments.

Recent Industry Developments

- In March 2025, Xylem Inc. announced the acquisition of Weir Minerals dewatering solutions division, expanding Xylem's portfolio with specialized high-capacity and mining-focused dewatering systems, positioning the company for enhanced mining sector market penetration and technology cross-pollination.

- In August 2024, Grundfos launched SCALA Series submersible dewatering pumps incorporating IoT connectivity and predictive maintenance capabilities, enabling real-time monitoring of pump performance, energy consumption, and component health, reducing downtime by approximately 35% through proactive maintenance alerts.

- In November, 2023, Sulzer completed a partnership with AT&S to develop energy-optimized dewatering plating technology, reducing power consumption by 25% while maintaining pumping performance through advanced impeller design and variable frequency drive integration, supporting sustainable operational practices.

Companies Covered in Dewatering Pump Market

- Grundfos Holding A/S

- Sulzer Ltd.

- Xylem Inc.

- Ebara Corporation

- KSB SE & Co. KGaA

- Weir Group PLC

- Tsurumi Manufacturing Co., Ltd.

- Pioneer Pump Inc.

- Atlas Copco

- Flowserve Corporation

- Wacker Neuson

- Gorman-Rupp Company

- Zoeller Pumps

- Merrick Industries

- C.R.I. Pumps

- Verder Scientific

- Nanfang Pump Industry

Frequently Asked Questions

The global Dewatering Pump market was valued at US$ 8.3 billion in 2025 and is projected to reach US$ 11.8 billion by 2032, growing at 4.3% CAGR during the forecast period.

Key demand drivers include accelerating global construction activities, mining industry expansion, climate change-induced weather volatility necessitating emergency flood response capabilities, and robust urbanization and infrastructure development.

The 1000 to 5000 GPM flow rate segment dominates with 38% market share, serving mid-to-large scale construction and mining applications.

Asia Pacific commands the largest regional share at 35.9% in 2024, driven by China and India construction dominance, mining sector expansion, and rapid urbanization.

Major opportunities include mining sector expansion creating 6.8% CAGR demand growth representing US$ 4.8 billion annual market value.

Key market players include Xylem Inc., Grundfos Holding A/S, Sulzer Ltd., Ebara Corporation, KSB SE & Co. KGaA, Weir Group PLC, Tsurumi Manufacturing Co., Ltd., and Atlas Copco.