- Medical Devices

- Defibrillator Market

Defibrillator Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Global Defibrillator Market by Product (Implantable Cardioverter Defibrillators (ICDs) and External Defibrillators), by Patient (Adult Patients, and Pediatric Patients), by End User (Hospitals, Cardiac Centers, Ambulatory Surgery Centers, and Others), and Regional Analysis from 2026 to 2033

Defibrillator Market Share and Trend Analysis

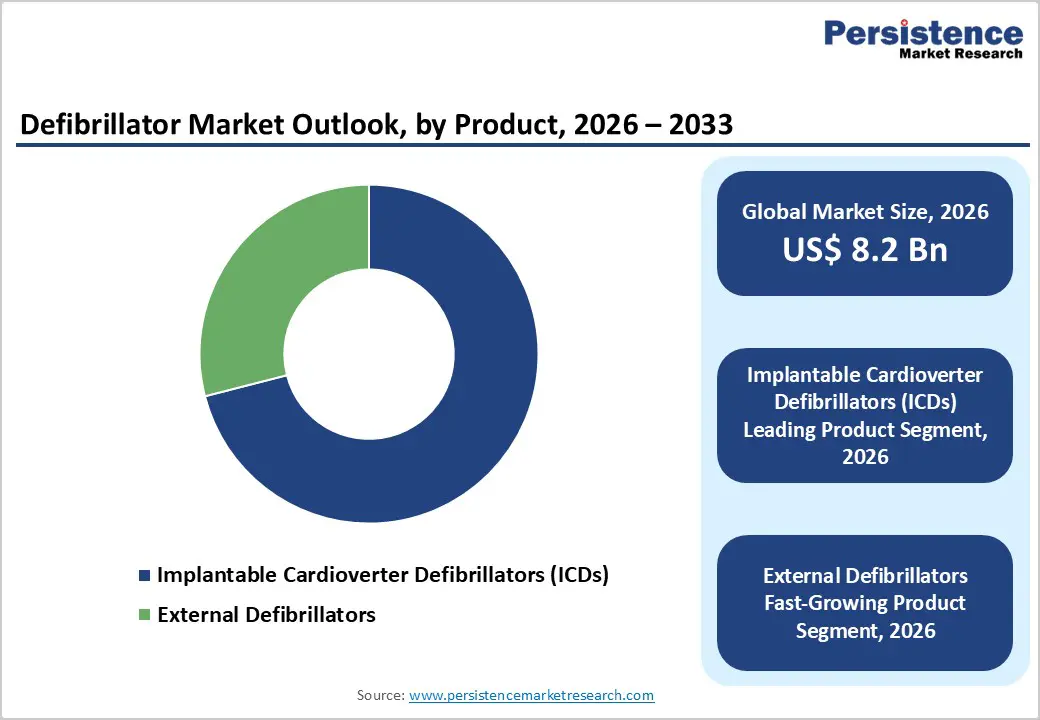

The global defibrillator market size is estimated to grow from US$ 8.2 Bn in 2026 to US$ 13.5 Bn by 2033. The market is projected to record a CAGR of 5.3% during the forecast period from 2026 to 2033.

Global demand for defibrillators is increasing steadily, driven by the rising prevalence of cardiovascular diseases, including arrhythmias, heart failure, and sudden cardiac arrest, along with growing awareness of early cardiac intervention and emergency response. Aging populations, sedentary lifestyles, obesity, diabetes, and hypertension are significantly expanding the at-risk patient pool, thereby supporting sustained demand for both implantable and external defibrillation solutions. Defibrillators are widely used across hospitals, cardiac centers, emergency medical services, and public access locations to restore normal heart rhythm and improve survival outcomes during life-threatening cardiac events.

Growing emphasis on preventive cardiology, early diagnosis of rhythm disorders, and rapid response to out-of-hospital cardiac arrest is further accelerating adoption. Expansion of emergency care infrastructure, increasing deployment of automated external defibrillators in public spaces, and rising penetration of cardiac specialty centers are strengthening market growth globally. Technological advancements, including improved shock delivery algorithms, remote monitoring capabilities, longer battery life, and device miniaturization, are enhancing clinical effectiveness and usability. Additionally, expanding healthcare infrastructure in emerging markets and increasing investments in cardiac care and emergency preparedness are reinforcing long-term demand for defibrillators worldwide.

Key Industry Highlights

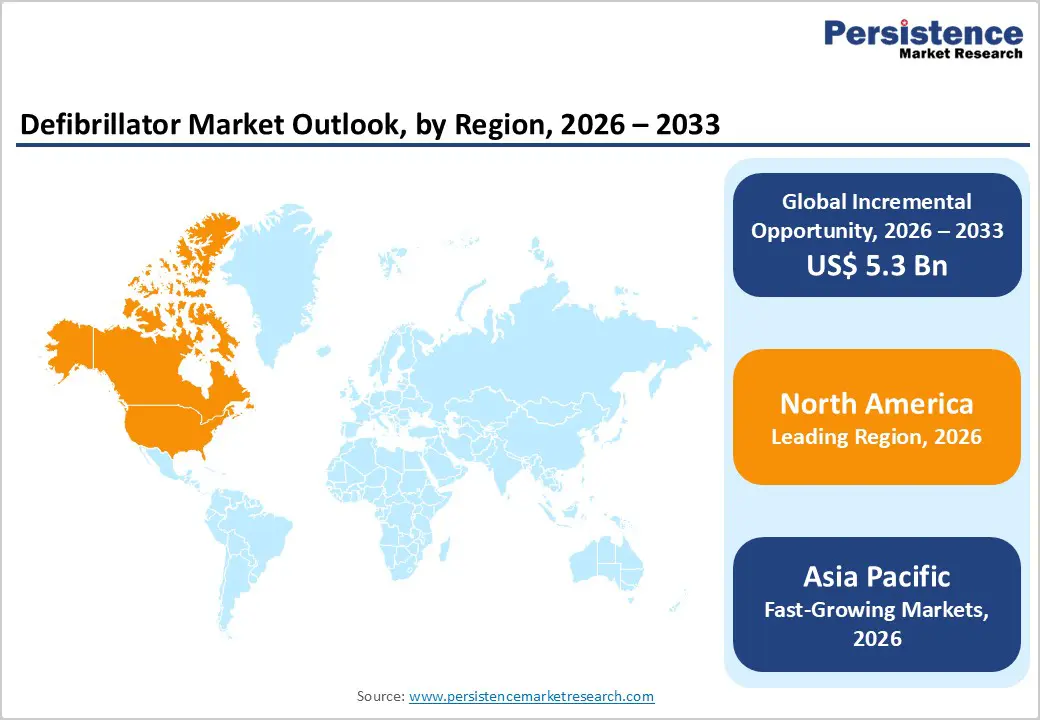

- Leading Region: North America holds the largest share at 47.3%, supported by a high prevalence of cardiovascular diseases, strong healthcare spending, advanced cardiac care infrastructure, favorable reimbursement frameworks, widespread availability of emergency medical services, and high adoption of both implantable and external defibrillators across hospitals and public access settings.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to rising cardiovascular disease burden, increasing aging population, improving healthcare access, rapid urbanization, growing investments in emergency response systems, government initiatives to improve cardiac arrest survival rates, and expanding private cardiac care facilities.

- Leading Product Segment: Implantable cardioverter defibrillators (ICDs) dominate the market due to their proven clinical effectiveness in preventing sudden cardiac death, long-term cardiac rhythm management capability, strong guideline support, and high adoption across hospitals and cardiac specialty centers.

- Fastest-Growing Product Segment: External defibrillators are growing rapidly as healthcare systems and public authorities prioritize early intervention, public access defibrillation programs, ease of use, portability, and deployment in high-footfall public and pre-hospital environments.

- Leading End User Segment: Hospitals remain the top segment, driven by high volumes of acute cardiac cases, availability of advanced cardiac intervention facilities, and strong demand for ICD implantation and in-hospital emergency defibrillation.

- Fastest-Growing End User Segment: Cardiac centers are scaling quickly as demand rises for specialized electrophysiology services, advanced rhythm management, and comprehensive cardiac care pathways.

| Global Market Attributes | Key Insights |

|---|---|

| Defibrillator Market Size (2026E) | US$ 8.2 Bn |

| Market Value Forecast (2033F) | US$ 13.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.2% |

Market Dynamics

Driver – Rising Burden of Cardiovascular Diseases, Increasing Sudden Cardiac Arrest Incidence, and Wider Access to Emergency Care

Growth is strongly supported by the increasing global burden of cardiovascular diseases, which remain a leading cause of mortality worldwide. Rising incidence of arrhythmias, heart failure, ischemic heart disease, and sudden cardiac arrest has significantly expanded the patient population requiring both implantable and external defibrillation solutions. Aging populations, sedentary lifestyles, obesity, diabetes, and hypertension are key contributors to this trend, particularly in developed and rapidly urbanizing economies. Defibrillators play a critical role in both acute emergency response and long-term cardiac rhythm management, making them indispensable across hospitals, cardiac centers, and pre-hospital settings.

Additionally, growing emphasis on improving survival rates from out-of-hospital cardiac arrest is driving wider deployment of automated external defibrillators (AEDs) in public spaces such as airports, workplaces, schools, and transportation hubs. Expansion of emergency medical services and improved response protocols further reinforce demand. Technological advancements, including remote monitoring, improved battery longevity, miniaturization of implantable devices, and enhanced shock accuracy, are strengthening clinical confidence and adoption. Increased awareness of cardiac health, early diagnosis, and guideline-driven treatment approaches continue to fuel consistent demand across both developed and emerging healthcare systems.

Restraints – High Device Costs, Invasive Nature of ICDs, and Infrastructure Limitations

The market growth is constrained by the high cost associated with advanced defibrillator systems, particularly implantable cardioverter defibrillators. ICD implantation involves not only device costs but also procedural expenses, follow-up care, and long-term monitoring, which can limit accessibility in cost-sensitive healthcare systems. Budget constraints in public hospitals and limited insurance coverage in certain regions further restrict adoption.

The invasive nature of ICD implantation can also act as a barrier, as it requires specialized surgical expertise, electrophysiology infrastructure, and post-implantation management. In lower-income and rural settings, lack of trained cardiologists, catheterization laboratories, and diagnostic facilities reduces the feasibility of advanced cardiac interventions. For external defibrillators, underutilization due to limited public training, fear of device misuse, and lack of awareness can restrict effectiveness despite availability. Additionally, maintenance requirements, periodic battery and electrode replacement, and compliance with regulatory and safety standards increase the total cost of ownership. Lengthy approval processes and varying regulatory frameworks across countries may delay product launches. Collectively, these factors slow penetration, particularly in emerging markets where affordability and infrastructure gaps remain significant challenges.

Opportunity – Public Access Defibrillation, Emerging Markets Expansion, and Digital Connectivity

Significant growth opportunities are emerging from the expansion of public access defibrillation programs and increasing investments in emergency preparedness worldwide. Governments, municipalities, and private organizations are prioritizing AED deployment in high-footfall public locations to improve cardiac arrest survival rates, creating sustained demand for external defibrillators and related accessories. Increased focus on workplace safety regulations and community-level cardiac response initiatives further supports adoption.

Emerging markets across Asia Pacific, Latin America, and parts of the Middle East and Africa represent substantial untapped potential. Improving healthcare infrastructure, rising healthcare expenditure, and growing awareness of cardiac emergencies are enabling broader access to defibrillation technologies. Expansion of private hospitals and cardiac specialty centers is accelerating ICD adoption in urban areas. Technological innovation presents another key opportunity, particularly through remote monitoring, wireless data transmission, and integration with digital health platforms. These features enhance long-term patient management, reduce hospital visits, and improve clinical outcomes. Development of cost-optimized devices, portable AEDs, and simplified user interfaces can further expand reach in resource-limited settings. Strategic partnerships between manufacturers, healthcare providers, and emergency service organizations are expected to unlock long-term growth opportunities.

Category-wise Analysis

By Product, Implantable Cardioverter Defibrillators (ICDs) Lead Due to Clinical Effectiveness and Long-Term Patient Management

Implantable Cardioverter Defibrillators (ICDs) are projected to dominate the global defibrillator market in 2026, accounting for a revenue share of 71.0%. Their leadership is driven by their proven clinical efficacy in preventing sudden cardiac death among high-risk patients with life-threatening arrhythmias. ICDs provide continuous cardiac monitoring and automatic shock delivery, making them a standard of care in cardiology. Strong adoption across hospitals and specialized cardiac centers, combined with favorable clinical guidelines and reimbursement support in developed markets, continues to reinforce demand. Technological advancements such as remote monitoring, longer battery life, and minimally invasive implantation techniques further enhance adoption. Additionally, the growing prevalence of cardiovascular diseases and increasing survival rates post-cardiac events support sustained utilization. High device value and recurring revenues from replacements and follow-ups contribute significantly to overall market dominance.

By Patient, Adult Patients Lead Due to Higher Incidence of Cardiac Disorders

The adult patients segment is expected to dominate the global defibrillator market in 2026, capturing a revenue share of 63.1%. This dominance is primarily attributed to the higher prevalence of cardiovascular diseases, arrhythmias, and sudden cardiac arrest among adult and elderly populations. Lifestyle-related risk factors such as obesity, hypertension, diabetes, smoking, and physical inactivity significantly increase cardiac risk in adults, driving demand for both implantable and external defibrillation solutions. Adults represent the largest population undergoing cardiac diagnostics, interventional procedures, and long-term rhythm management, resulting in higher ICD implantation rates. Increasing awareness of preventive cardiac care, routine cardiac screening, and early diagnosis further supports growth. Additionally, expanding access to emergency response systems and public access defibrillation programs predominantly targets adult populations. As global life expectancy rises, the adult segment is expected to remain the primary driver of defibrillator demand.

By End User, Hospitals Lead Due to High Cardiac Case Volume and Advanced Infrastructure

Hospitals are projected to dominate the global defibrillator market in 2026, accounting for a revenue share of 77.6%. This leadership is driven by high patient footfall for emergency cardiac care, availability of advanced diagnostic and interventional facilities, and the presence of trained cardiologists and electrophysiologists. Hospitals are the primary centers for ICD implantation, acute cardiac arrest management, and post-event monitoring, making them the largest purchasers of defibrillator systems. Integration of defibrillators within intensive care units, emergency departments, operating rooms, and cardiac catheterization labs supports consistent utilization. Higher procurement budgets allow hospitals to invest in technologically advanced devices and regular equipment upgrades. Additionally, strong clinical trust, standardized treatment protocols, and reimbursement support reinforce hospital-based usage. While ambulatory and outpatient settings are expanding, hospitals continue to dominate due to comprehensive cardiac care capabilities.

Region-wise Insights

North America Defibrillator Market Trends

North America is expected to dominate the global defibrillator market with a value share of 47.3% in 2026, led primarily by the United States. The region benefits from a well-established cardiovascular care ecosystem, high awareness of sudden cardiac arrest, and widespread access to advanced emergency medical services. High prevalence of cardiovascular diseases, an aging population, and sedentary lifestyles continue to drive demand for both implantable and external defibrillators.

Strong presence of leading manufacturers such as Medtronic, Abbott, Boston Scientific Corporation, Stryker, and Zoll Medical Corporation ensures rapid adoption of technologically advanced devices. Favorable reimbursement frameworks, strong regulatory oversight, and well-defined clinical guidelines support ICD implantation volumes. Additionally, extensive public access defibrillation programs across airports, schools, workplaces, and public venues significantly boost external defibrillator demand. Early adoption of remote monitoring technologies and regular device replacement cycles further sustain market leadership across the forecast period.

Europe Defibrillator Market Trends

The Europe defibrillator market is expected to grow steadily, supported by strong cardiovascular care standards and rising emphasis on early intervention and preventive cardiology across countries such as Germany, the U.K., France, Italy, and Spain. The region benefits from robust healthcare infrastructure, universal healthcare coverage in many countries, and high adherence to clinical and regulatory standards. An aging population and increasing incidence of cardiac rhythm disorders are driving demand for ICDs and in-hospital defibrillation systems.

Hospitals and specialized cardiac centers continue to invest in reliable and clinically validated devices to maintain patient safety and treatment efficiency. Expansion of emergency response networks and growing availability of automated external defibrillators in public spaces further support growth. Additionally, increasing focus on reducing out-of-hospital cardiac arrest mortality through public awareness campaigns contributes to adoption. Preference for high-quality, durable devices and consistent healthcare funding ensures long-term market stability in Europe.

Asia Pacific Defibrillator Market Trends

The Asia Pacific defibrillator market is expected to register a relatively higher CAGR of around 7.2% between 2026 and 2033, driven by expanding healthcare infrastructure, rising cardiovascular disease burden, and increasing awareness of emergency cardiac care. Countries such as China, India, Japan, South Korea, and Australia are witnessing a rapid rise in cardiac disorders due to urbanization, aging populations, dietary changes, and lifestyle-related risk factors. Improving access to hospital-based cardiac care and growing investments in emergency medical services are significantly boosting defibrillator adoption. Expansion of private hospitals, cardiac specialty centers, and public access defibrillation programs is increasing device penetration.

Government initiatives focused on strengthening emergency response systems and improving survival rates from sudden cardiac arrest further support growth. Additionally, local manufacturing, cost-effective device availability, and entry of global players are improving affordability. With rising healthcare expenditure and awareness, Asia Pacific is positioned as the fastest-growing regional market.

Market Competitive Landscape

The global defibrillator market is highly competitive, with strong participation from companies such as Medtronic, Abbott, Boston Scientific Corporation, Stryker, and Zoll Medical Corporation. These players leverage extensive global distribution networks, strong brand recognition, and broad cardiovascular and emergency care product portfolios to address the rising demand for effective cardiac rhythm management and sudden cardiac arrest interventions.

Their offerings focus on advanced shock delivery technologies, device reliability, real-time monitoring and connectivity, ease of use in emergency settings, and compatibility across hospital, pre-hospital, and public access environments. Continuous technological innovation, regulatory compliance, product safety, and adherence to international quality and manufacturing standards remain critical to sustaining competitive positioning in the global defibrillator market.

Key Industry Developments:

- In January 2026, Abbott announced a collaboration with AtaCor Medical to develop a next-generation implantable cardioverter defibrillator (ICD) aimed at treating life-threatening cardiac arrhythmias without placing leads inside the heart or veins. The partnership combines Abbott’s investigational extravascular ICD system with AtaCor’s investigational parasternal EV-ICD lead, known as Atala.

- In May 2025, the US Food and Drug Administration (FDA) approved Element Science’s premarket approval application for its Jewel Patch Wearable Cardioverter Defibrillator (Patch-WCD), expanding its use in cardiac care for patients with a temporary elevated risk of sudden cardiac arrest in the United States. Prior to this, the device received CE mark certification along with UK Conformity Assessed (UKCA) approval in January of the previous year, enabling its commercialization across European and UK markets.

- In October 2023, Medtronic plc received U.S. FDA approval for its Aurora EV-ICD™ MRI SureScan™ system and Epsila EV™ MRI SureScan™ defibrillation lead for treating life-threatening rapid heart rhythms associated with sudden cardiac arrest. The Aurora EV-ICD is the first extravascular ICD to deliver defibrillation, anti-tachycardia pacing, and backup pacing through a lead placed beneath the breastbone, outside the heart and veins, while offering size, durability, and performance comparable to traditional transvenous ICDs.

Companies Covered in Defibrillator Market

- Medtronic

- Abbott

- Boston Scientific Corporation

- Stryker

- Zoll Medical Corporation

- Biotronik

- Nihon Kohden Corporation

- METRAWATT International

- Datrend Systems

- Fluke

- BC Group International

- Netech

- Others

Frequently Asked Questions

The global defibrillator market is projected to be valued at US$ 8.2 Bn in 2026.

The market is driven by the rising prevalence of cardiovascular diseases and sudden cardiac arrests globally, coupled with technological advancements in defibrillator devices.

The global defibrillator market is poised to witness a CAGR of 5.3% between 2026 and 2033.

Key opportunities include expanding public access defibrillator programs and growth in emerging markets with increasing healthcare infrastructure investments.

Medtronic, Abbott, Boston Scientific Corporation, Stryker, and Zoll Medical Corporation. are some of the key players in the defibrillator market.