- Advanced Materials

- Crude Sulfate Turpentine Market

Crude Sulfate Turpentine Market Size, Share, and Growth Forecast, 2026 - 2033

Crude Sulfate Turpentine Market by Product Derivative (Alpha-Pinene, Terpineol, Others), Application (Aroma Chemicals, Fragrance Chemicals, Others), and Regional Analysis for 2026 - 2033

Crude Sulfate Turpentine Market Size and Trends Analysis

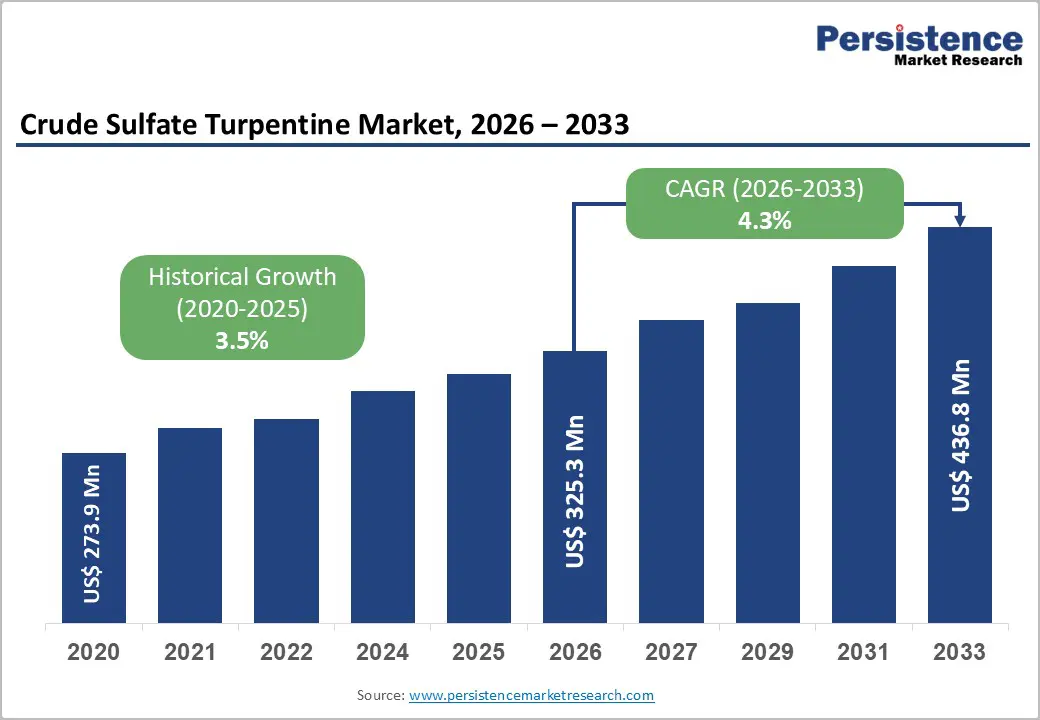

The global crude sulfate turpentine market size is likely to be valued at US$325.3 million in 2026 and is expected to reach US$436.8 million by 2033, growing at a CAGR of 4.3% between 2026 and 2033, driven by increasing demand for bio-based chemicals, wider use of terpene derivatives across fragrance and industrial applications, and stricter environmental regulations governing volatile organic compound (VOC) emissions. The value chain is progressively shifting toward higher-value derivative processing, with refined terpene products emerging as key contributors to overall profitability.

Key Industry Highlights:

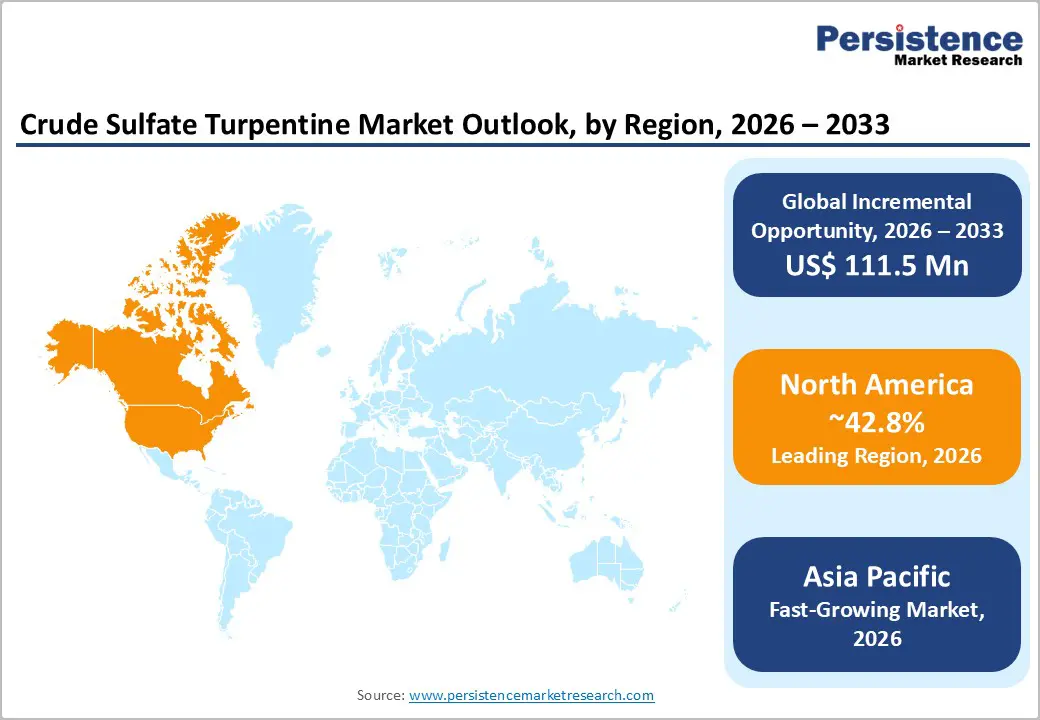

- Leading Region: North America is anticipated to remain the leading regional market, accounting for 42.8% share, supported by a well-established pulp & paper industry, advanced recovery systems for CST, and strong downstream demand for terpene-based chemicals.

- Fastest-growing Region: Asia Pacific is projected to be the fastest-growing region, driven by expanding industrial production in countries such as China, India, and Japan, along with rising demand for consumer goods and fragrance chemicals.

- Investment Plans: Market participants are focusing on capacity expansion, advanced distillation technologies, and downstream integration, particularly in Asia Pacific and North America, to improve yield efficiency and capture higher-margin derivatives such as alpha-pinene and terpineol.

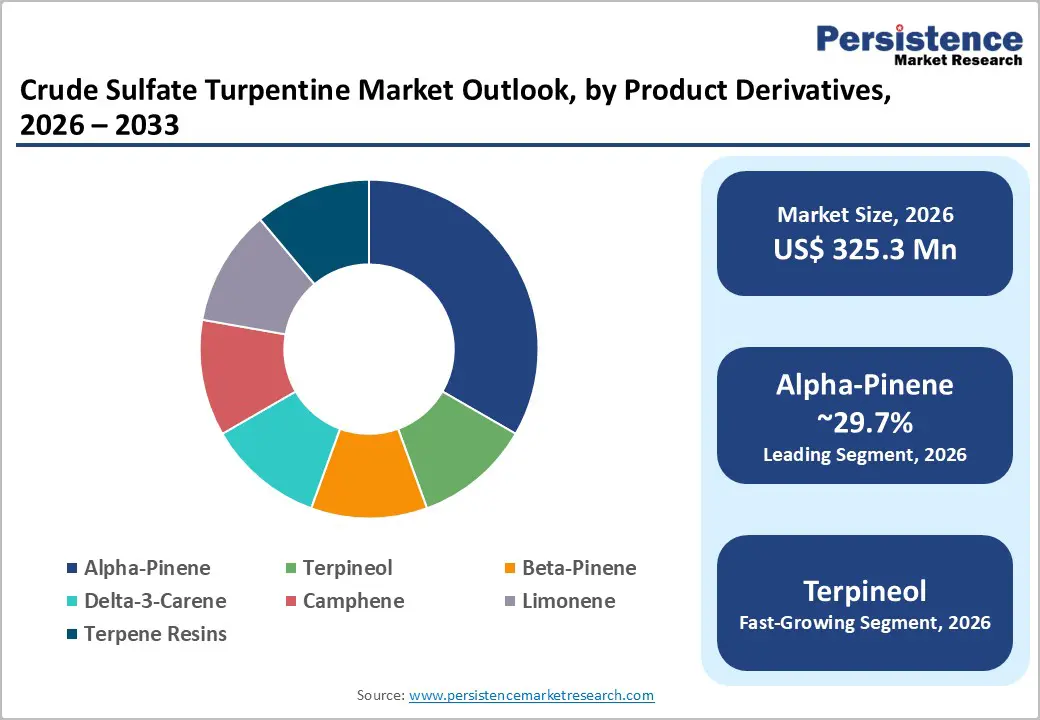

- Dominant Product Derivatives: Alpha-pinene is expected to dominate with an anticipated share of 29.7%, supported by its high recovery rate and extensive use in aroma chemicals, resins, and specialty intermediates.

- Leading Applications: Aroma chemicals are projected to lead with an anticipated share of 32.7%, driven by strong demand from fragrance, flavor, and personal care industries, along with increasing adoption of bio-based ingredients.

| Key Insights | Details |

|---|---|

| Crude Sulfate Turpentine Market Size (2026E) | US$325.3 Mn |

| Market Value Forecast (2033F) | US$436.8 Mn |

| Projected Growth (CAGR 2026 to 2033) | 4.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.5% |

DRO Analysis

Driver Analysis - Structural Linkage to Kraft Pulp Production Ensures Consistent Feedstock Availability

Crude sulfate turpentine is inherently tied to the kraft pulping process, where it is recovered during the digestion of wood chips. This structural linkage ensures a relatively stable supply base, as CST production increases with pulp manufacturing activity. Global pulp production remains a foundational industrial activity, particularly in packaging, hygiene, and specialty paper segments. As pulp mills operate at scale, CST recovery benefits from economies of integration, reducing the need for standalone feedstock cultivation. This embedded production model supports long-term supply stability and reduces raw material volatility compared to independent bio-based chemical markets.

Rising Demand for Fragrance and Aroma Chemicals Enhances Downstream Value

The growing global demand for fragrances, flavors, and aroma chemicals is significantly increasing the value of CST derivatives. Compounds such as alpha-pinene, terpineol, and limonene serve as key intermediates in the synthesis of fragrance ingredients and specialty chemicals. Consumer preferences are shifting toward natural and renewable ingredients, encouraging manufacturers to incorporate terpene-based inputs. As a result, CST is transitioning from a low-value by-product to a strategic feedstock for high-margin applications. This shift is driving investment in purification and fractionation technologies to maximize yield and quality of derivative outputs.

Environmental Regulations and Sustainability Trends Favor Bio-Based Inputs

Regulatory frameworks targeting VOC emissions and chemical safety are driving industries toward cleaner, more sustainable raw materials. CST-derived chemicals, being renewable and plant-based, align well with these regulatory expectations. Manufacturers in coatings, adhesives, and personal care are increasingly adopting terpene-based alternatives to petroleum-derived chemicals. This transition is further supported by corporate sustainability goals and consumer demand for environmentally responsible products. The ability of CST derivatives to meet both performance and compliance requirements strengthens their adoption across multiple industrial sectors.

Restraint Analysis - Supply Volatility Due To Dependence on Pulp Industry Cycles

Despite its integration with pulp production, CST supply remains vulnerable to fluctuations in the paper and packaging industry. Changes in demand for paper products, mill shutdowns, or shifts toward recycled fiber can impact CST recovery volumes. This creates periodic supply constraints that are beyond the direct control of CST producers. Additionally, regional disparities in pulp production can lead to uneven supply distribution, affecting pricing and availability in global markets.

High Processing Costs and Technical Complexity in Refining

Raw CST contains sulfur compounds and impurities that limit its direct usability. Significant investment in distillation, purification, and desulfurization is required to convert CST into commercially viable derivatives. These processes demand advanced technology, skilled operation, and strict quality control. Variability in crude composition further complicates processing, increasing operational costs and reducing yield efficiency. Smaller producers may face challenges in scaling these capabilities, limiting their competitiveness in high-value applications.

Opportunity Analysis - Value Creation through Advanced Fractionation and Derivative Production

The ability to convert CST into high-value derivatives such as alpha-pinene and terpineol presents a major opportunity for market participants. These compounds are widely used in fragrances, solvents, and specialty chemicals, offering significantly higher margins than crude CST. Investment in advanced distillation, catalytic conversion, and purification technologies can enhance product quality, improve yield efficiency, and expand the range of downstream applications. Companies that integrate upstream recovery with downstream processing are better positioned to capture this value, reduce dependency on volatile crude pricing, and strengthen long-term profitability. This shift toward value-added processing is also enabling suppliers to align more closely with high-growth end-use industries.

Expansion in Asia Pacific Driven By Industrial Growth and Demand

Asia Pacific represents the fastest-growing region for CST, supported by rapid industrialization, expanding pulp production, and rising demand for consumer goods. Countries such as India, China, and Japan are strengthening their capabilities in fragrance chemicals, coatings, and specialty materials, supported by increasing investments in manufacturing infrastructure. Growth in the packaging, personal care, and home care sectors is further driving demand for CST derivatives, particularly in urbanizing economies. The region offers strong opportunities for capacity expansion, cost-efficient manufacturing, and export-oriented production strategies, making it an attractive destination for both global and regional players seeking to scale operations and improve supply chain efficiency.

Increasing Adoption of Renewable Chemicals in Consumer and Industrial Applications

The global shift toward sustainable and circular economy models is creating new opportunities for CST-based products. Industries are actively seeking renewable alternatives to petrochemical inputs, particularly in adhesives, coatings, and cleaning products, where regulatory pressure and consumer awareness are increasing. CST derivatives offer a viable solution due to their biodegradability, lower environmental impact, and competitive performance characteristics. As sustainability becomes a key purchasing criterion, manufacturers are incorporating bio-based terpene chemicals into product formulations to meet environmental targets and brand positioning.

This trend is expected to accelerate as companies prioritize carbon reduction and adopt greener supply chains.

Category-wise Analysis

Product Derivatives Insights

Alpha-pinene dominates, anticipated to hold 29.7% of market share in 2026, due to its versatility and wide range of industrial applications. It serves as a key intermediate in the production of fragrance chemicals, solvents, synthetic resins, and adhesives, making it highly valuable across multiple downstream industries. Its relatively high yield during CST fractionation and stable recovery rates from kraft pulping processes contribute to its leading market position. The compound is also extensively used in the synthesis of camphor, terpene resins, and lubricant additives, reinforcing its importance in the value chain.

From an application standpoint, alpha-pinene is widely utilized by major fragrance and flavor manufacturers such as Givaudan and International Flavors & Fragrances, where it acts as a precursor for aroma molecules like linalool and geraniol. Its role in the production of bio-based solvents for coatings and cleaning products also supports demand growth, particularly as industries transition toward sustainable raw materials. This combination of high-volume demand, diverse applications, and strong industrial integration continues to anchor alpha-pinene as the leading derivative segment.

Terpineol is emerging as the fastest-growing derivative due to its increasing use in fragrances, personal care products, and cleaning formulations. It offers desirable scent characteristics, antimicrobial properties, and excellent solubility, making it suitable for high-value applications such as perfumes, soaps, detergents, and disinfectants. The shift toward premium and natural ingredients in consumer products is significantly driving demand for terpineol, especially in regions with strong personal care consumption growth.

For example, terpineol is widely incorporated in formulations by global consumer goods companies like Unilever and Procter & Gamble, where it enhances fragrance stability and product performance. Its growth is also supported by advancements in catalytic hydration and purification technologies, which improve production efficiency and scalability. As manufacturers increasingly focus on bio-based fragrance ingredients, terpineol is expected to witness sustained high growth across both industrial and consumer-facing applications.

Application Insights

Aroma chemicals are anticipated to hold 32.7% market share in 2026, as CST derivatives are widely used in the formulation of fragrances and flavors across multiple industries. These compounds provide essential building blocks for scent and taste profiles in products such as perfumes, cosmetics, food flavorings, and household cleaners. The established demand from fragrance manufacturers, coupled with the increasing preference for bio-based and naturally derived ingredients, supports the dominance of this segment. CST-derived components such as alpha-pinene, limonene, and terpineol are extensively utilized by companies like Symrise and Firmenich to develop sustainable aroma solutions.

Growth in premium fragrances and clean-label food products is further strengthening demand. The segment also benefits from rising disposable incomes and changing consumer preferences, particularly in emerging economies, where demand for high-quality personal care and packaged food products continues to expand.

Fragrance chemicals are experiencing rapid growth due to rising demand in personal care, home care, and fine fragrance applications. Consumer trends favoring natural, sustainable, and high- performance ingredients are accelerating this growth, especially as brands emphasize transparency and eco-friendly formulations. CST-derived fragrance chemicals offer a renewable alternative to petroleum-based inputs, aligning with evolving regulatory and environmental standards.

For instance, CST-based ingredients are increasingly used in premium perfume lines developed by companies such as L'Oréal and niche fragrance brands focusing on sustainable sourcing. Continuous innovation in fragrance delivery systems, including encapsulation technologies and long-lasting scent formulations, is further expanding the application scope of CST-derived chemicals. This trend is particularly strong in Asia Pacific and Europe, where consumer awareness of sustainability and product differentiation is driving demand for advanced fragrance solutions.

Regional Insights

North America Crude Sulfate Turpentine Market Trends - Integrated Pulp Infrastructure and Bio-Based Innovation Leadership

North America leads the market with a 42.8% share in 2026, supported by a strong pulp and paper industry and advanced chemical processing infrastructure. The U.S. plays a central role, with well-established Kraft pulp mills and integrated chemical production facilities that enable efficient recovery and conversion of CST into high-value derivatives. The region benefits from high levels of technological innovation, particularly in distillation and terpene conversion processes, along with strong collaboration between chemical manufacturers and end-use industries such as coatings, adhesives, and personal care.

Regulatory frameworks in North America emphasize environmental compliance, particularly in VOC emissions and chemical safety standards enforced by agencies such as the U.S. Environmental Protection Agency. This regulatory pressure encourages the use of cleaner and more sustainable raw materials, including CST derivatives. For instance, companies such as Kraton Corporation have expanded their pine chemical portfolios and invested in bio-based product innovation following their acquisition of Arizona Chemical, strengthening their position in CST derivatives.

Similarly, International Flavors & Fragrances continues to integrate renewable terpene-based ingredients into fragrance formulations, reflecting rising demand for sustainable inputs. Investment across the region is focused on improving purification processes, enhancing derivative conversion yields, and strengthening supply chain resilience, particularly in response to raw material volatility and sustainability goals.

Europe Crude Sulfate Turpentine Market Trends - Regulation-Driven Sustainability and Premium Derivatives Focus

Europe remains a key market, driven by its strong focus on sustainability and the circular economy. Countries such as Germany, France, the U.K., and Spain play significant roles in both production and consumption. The region is characterized by advanced chemical manufacturing capabilities, a highly skilled workforce, and a high level of regulatory harmonization under frameworks such as the REACH Regulation.

Strict environmental and safety regulations influence product development and sourcing strategies. While these regulations increase compliance costs, they also create opportunities for high-quality, sustainable products. For example, Symrise has strengthened its portfolio of renewable aroma chemicals by integrating terpene-based ingredients into its product lines, aligning with European sustainability goals. Similarly, Givaudan has expanded its natural ingredient sourcing and green chemistry initiatives, including the use of bio-based terpenes derived from CST.

Investment trends in Europe focus on renewable chemical production, advanced processing technologies, and innovation in fragrance and specialty applications. The region continues to serve as a hub for high-value derivative production, particularly for premium fragrance and flavor markets.

Asia Pacific Crude Sulfate Turpentine Market Trends - Rapid Industrial Expansion and Cost-Driven Production Growth

Asia Pacific is the fastest-growing region, driven by expanding industrial activity, increasing consumer demand, and rapidly evolving manufacturing capabilities. Key contributors include China, India, and Japan, where growth in pulp production, fragrance chemicals, and consumer goods industries is accelerating demand for CST derivatives. The region is witnessing significant capacity expansion in pulp and paper mills, which directly increases CST availability as a by- product.

The region benefits from cost-effective manufacturing, the availability of raw materials, and rising domestic consumption. Rapid urbanization and income growth are driving demand for personal care and household products, which in turn increases the need for CST-derived ingredients. For instance, companies such as Foreverest Resources Ltd. are expanding their terpene product portfolios and export capabilities, supplying global markets with CST derivatives. In India, firms such as Mentha & Allied Products Pvt. Ltd. are strengthening domestic production and tapping into the growing demand for fragrance and flavor ingredients.

Meanwhile, Takasago International Corporation continues to innovate in high-value aroma chemicals, leveraging advanced R&D capabilities. Governments across the region are also strengthening regulatory frameworks and promoting sustainable chemical adoption, creating favorable conditions for long-term market growth. Investment opportunities remain strong in capacity expansion, technology upgrades, and export-oriented production strategies, positioning Asia Pacific as a critical growth engine for the CST market.

Competitive Landscape

The global crude sulfate turpentine market is moderately fragmented at the crude level but more concentrated in downstream processing and high-value derivatives. Crude supply is distributed among pulp mills, while advanced processing is dominated by specialized chemical companies. Market leaders differentiate themselves through integration, technological capabilities, and access to end-use industries. Competitive positioning is largely determined by the ability to convert CST into high-quality, specification-grade products.

Key players are focusing on vertical integration, innovation in bio-based chemistry, and expansion into high-growth markets. Emphasis is placed on improving processing efficiency, ensuring regulatory compliance, and developing high-value derivatives. Strategic partnerships and investments in biotechnology are emerging as critical drivers of competitive advantage.

Key Industry Developments:

- In November 2025, Kraton Corporation introduced new 2032 climate and resource-efficiency targets, focusing on reducing carbon emissions and improving sustainable sourcing of pine-based feedstocks, reinforcing the strategic shift toward bio-based CST derivatives and circular economy integration.

Companies Covered in Crude Sulfate Turpentine Market

- Kraton Corporation

- Symrise

- DRT

- Arizona Chemical Company

- International Flavors & Fragrances

- Givaudan

- Firmenich

- Takasago International Corporation

- Lawter Inc.

- Pine Chemical Group

- Harima Chemicals Group

- Foreverest Resources Ltd.

- PT. Naval Overseas

- Mentha & Allied Products Pvt. Ltd.

- Respol Resinas S.A.

- Eastman Chemical Company

Frequently Asked Questions

The global crude sulfate turpentine market size is estimated to be US$325.3 million in 2026.

The crude sulfate turpentine market is projected to reach US$436.8 million by 2033.

Key trends include growing adoption of renewable and bio-based chemicals, increased conversion of CST into high-value derivatives such as alpha-pinene and terpineol, and expansion of production capacity in Asia Pacific.

By product derivatives, alpha-pinene is the leading segment, holding an anticipated share of 29.7%, due to its widespread use in fragrance chemicals, resins, and specialty intermediates.

The crude sulfate turpentine market is expected to grow at a CAGR of 4.3% between 2026 and 2033.

Some of the major players include Kraton Corporation, Symrise, DRT (Derives Resiniques et Terpeniques), Arizona Chemical Company, and International Flavors & Fragrances.