- Medical Devices

- Coronary Intravascular Lithotripsy Market

Coronary Intravascular Lithotripsy Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Coronary Intravascular Lithotripsy Market by Product (Coronary Intravascular Lithotripsy (IVL) Balloon Catheters, and Intravascular Lithotripsy (IVL) Control Consoles), by Application (Coronary Artery Disease, and Peripheral Artery Disease), End-user (Hospitals, Specialty Cardiac Centers, and Ambulatory Surgical Centers (ASCs)), and Regional Analysis from 2026 - 2033

Coronary Intravascular Lithotripsy Market Share and Trend Analysis

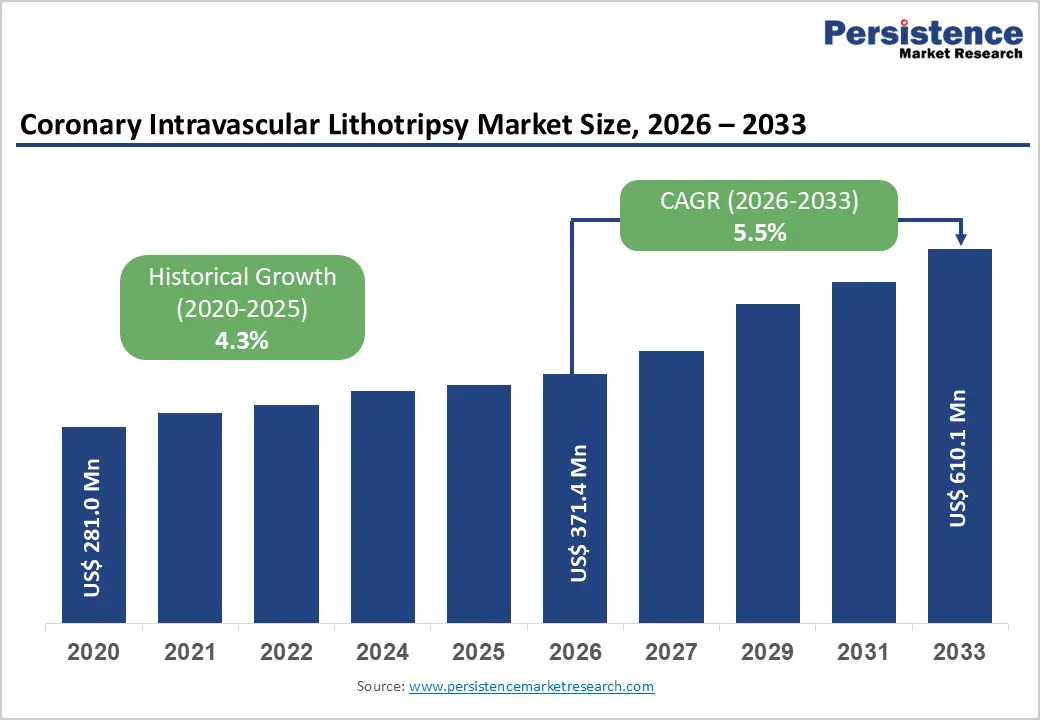

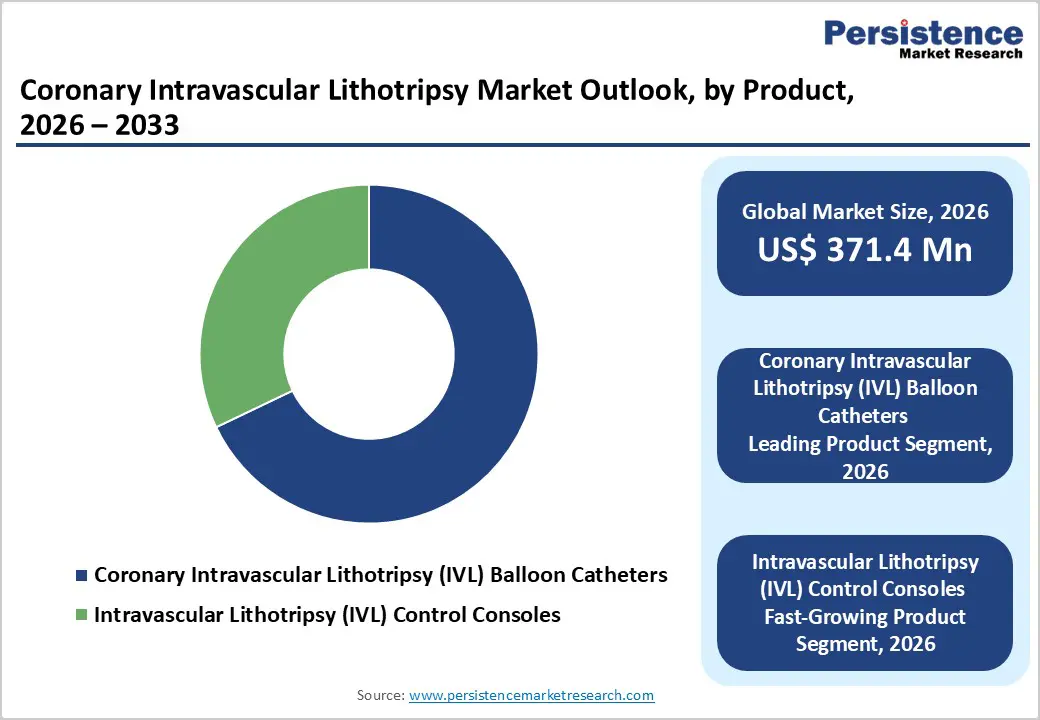

The global coronary intravascular lithotripsy market size is estimated to be valued at US$371.4 million in 2026 and is expected to reach US$610.1 million by 2033, and is expected to reach a CAGR of 5.5% during the forecast period from 2026 to 2033. Global demand for coronary intravascular lithotripsy is rising steadily, supported by the increasing prevalence of complex and heavily calcified coronary artery disease worldwide. Aging populations, higher incidence of diabetes, chronic kidney disease, obesity, and long-standing atherosclerosis are contributing to a growing volume of calcified lesions that are difficult to treat with conventional balloon angioplasty alone. As interventional cardiologists increasingly encounter under-expanded stents and procedural complications associated with rigid calcium, adoption of IVL as a safer and more controlled plaque-modification technology continues to accelerate.

A clear shift toward vessel-friendly, non-atherectomy-based lesion preparation approaches is strengthening procedural confidence and clinical uptake. Expanding PCI volumes, growing treatment of elderly and high-risk patients, and increasing preference for predictable stent expansion outcomes are sustaining long-term demand. Rising healthcare expenditure, improving access to advanced cath lab infrastructure, and wider availability of IVL systems are further supporting growth. Ongoing advancements in catheter deliverability, acoustic pressure wave efficiency, and integration with intravascular imaging technologies are enhancing procedural success rates. Additionally, the increasing focus on improving long-term PCI outcomes, reducing complications, and optimizing complex coronary interventions is further propelling the global coronary intravascular lithotripsy market.

Key Industry Highlights:

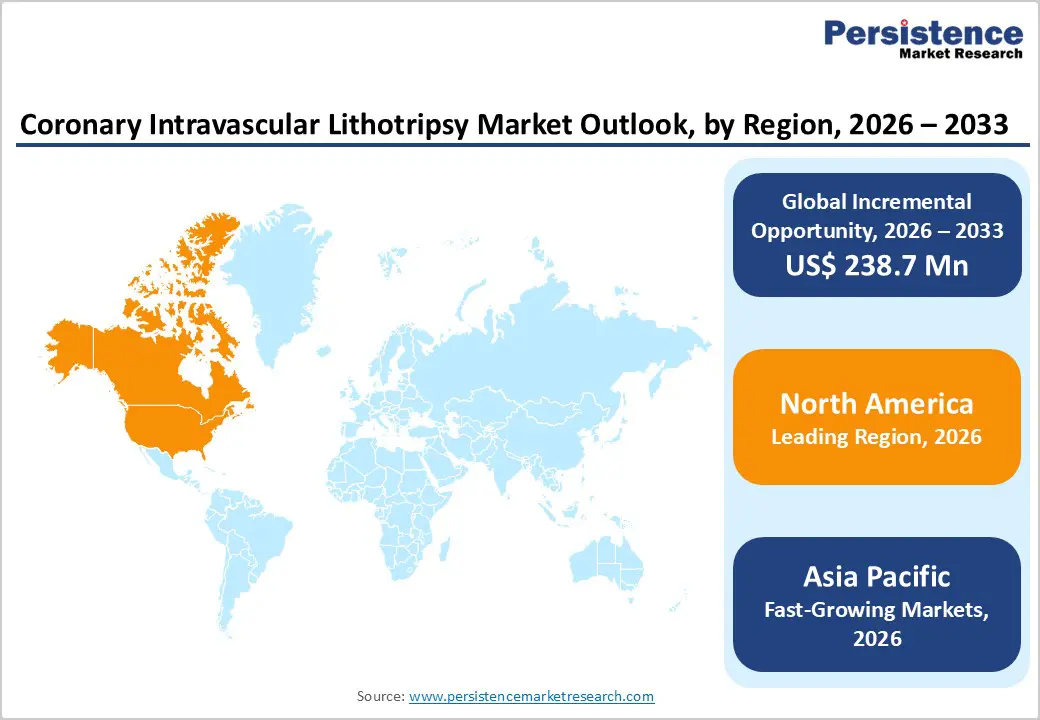

- Leading Region: North America holds the largest share at 47.3%, supported by advanced cardiovascular care infrastructure, high PCI procedure volumes, early adoption of innovative interventional technologies, and the strong presence of leading IVL manufacturers.

- Fastest-Growing Region: Asia Pacific is expanding fastest, driven by a large patient base, rising prevalence of coronary artery disease, improved access to advanced cardiac care, rising healthcare investments, and the rapid expansion of private hospitals and specialty cardiac centers.

- Leading Product Segment: Coronary intravascular lithotripsy (IVL) balloon catheters dominate the market due to their essential role in calcium modification, single-use disposability, and high utilization in complex PCI procedures.

- Fastest-Growing Product Segment: Intravascular lithotripsy (IVL) control consoles are expanding rapidly as hospitals and cardiac centers increase system installations to support rising procedural volumes and broader clinical adoption.

- Leading Application Segment: Coronary artery disease remains the top segment, driven by the high prevalence of calcified coronary lesions and growing use of IVL in complex and high-risk PCI.

- Fastest-Growing Application Segment: Peripheral artery disease is growing rapidly as IVL adoption expands beyond coronary interventions into peripheral vascular applications that require effective calcium modification.

| Key Insights | Details |

|---|---|

|

Coronary Intravascular Lithotripsy Market Size (2026E) |

US$ 371.4 Mn |

|

Market Value Forecast (2033F) |

US$ 610.1 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

4.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.5% |

Market Dynamics

Driver - Rising Prevalence of Calcified Coronary Disease and Demand for Safer Lesion Preparation

The increasing incidence of advanced coronary artery disease, characterized by moderate-to-severe calcification, is a key factor accelerating the adoption of intravascular lithotripsy in interventional cardiology. Aging populations, combined with higher prevalence of diabetes, chronic kidney disease, hypertension, and long-standing atherosclerosis, are contributing to a growing pool of patients with heavily calcified coronary lesions. These lesions are challenging to treat with conventional balloon angioplasty and are associated with poor stent expansion, higher restenosis rates, and adverse clinical outcomes.

Clinical limitations and complication risks associated with traditional atherectomy techniques have intensified interest in alternative plaque-modification approaches. Intravascular lithotripsy offers controlled calcium fracture with minimal vessel trauma, reducing the risk of perforation, distal embolization, and no-reflow. Increasing procedural confidence among interventional cardiologists, supported by positive real-world outcomes and clinical evidence, is further driving uptake. Additionally, rising global PCI volumes and the shift toward treating higher-risk and elderly patients are reinforcing the role of IVL as a preferred technology for complex coronary interventions.

Restraints - High Device Costs, Procedural Economics, and Limited Access in Emerging Settings

The economic and structural challenges continue to restrain broader adoption. IVL systems entail substantial upfront capital investment in consoles and recurring costs for disposable balloon catheters, which can strain hospital budgets, particularly in cost-sensitive healthcare systems. In regions with limited reimbursement coverage for advanced interventional devices, hospitals may hesitate to adopt IVL routinely, thereby restricting its use to select high-risk cases.

In addition, access to IVL remains uneven across emerging and lower-tier healthcare facilities due to infrastructure limitations, including a lack of advanced cath labs and trained interventional specialists. Procedural learning curves and the need for physician training may further slow the penetration of these procedures in secondary and rural hospitals. Regulatory approval timelines and varying compliance requirements across regions also increase the complexity of commercialization for manufacturers. Competition from established plaque-modification techniques, including rotational and orbital atherectomy, continues to influence treatment selection in cost-driven environments. These combined factors limit the rapid, uniform adoption of these interventions despite clear clinical benefits.

Opportunity - Expansion into Complex PCI, Emerging Markets, and Adjacent Vascular Applications

Significant growth opportunities exist as treatment paradigms evolve toward managing increasingly complex coronary anatomy. Rising treatment of elderly, high-risk patients and greater willingness to intervene in severe calcified lesions create a favorable environment for wider IVL utilization. Expansion into emerging healthcare markets presents additional upside, supported by increasing cardiovascular disease prevalence, improving cath lab infrastructure, and growing investment in advanced cardiac care.

Healthcare modernization initiatives, the expansion of private hospital networks, and rising insurance penetration in the Asia-Pacific, Latin America, and parts of the Middle East are improving access to complex PCI technologies. Manufacturers can leverage these trends through localized pricing strategies, physician education programs, and strategic partnerships with distributors. Beyond coronary use, opportunities also exist in peripheral and structural heart–related vascular interventions, where calcium modification is critical. Continued innovation in catheter design, energy delivery efficiency, and integration with intravascular imaging can further enhance clinical value. Strengthening clinical evidence, expanding indications, and aligning with value-based care models are expected to unlock sustained long-term growth.

Category-wise Analysis

By Product Insights

Coronary intravascular lithotripsy (IVL) balloon catheters are projected to lead the global coronary intravascular lithotripsy market in 2026, accounting for 67.9% of the market, driven by their indispensable role in calcium modification during percutaneous coronary interventions. These single-use catheters deliver localized acoustic pressure waves that fracture deep and superficial vascular calcium while minimizing vessel trauma, enabling optimal stent expansion in heavily calcified lesions. High procedural volumes, combined with the disposable nature of IVL balloons, generate consistent recurring revenue for manufacturers. Growing adoption of IVL as a safer alternative to atherectomy in complex coronary anatomy further strengthens demand. Continuous improvements in catheter deliverability, balloon compliance, and energy transmission efficiency enhance procedural success and operator confidence. In addition, expanding indications for complex PCI and increasing treatment of elderly patients with severe calcification support sustained dominance of IVL balloon catheters within the overall market.

By Application Insights

The coronary artery disease segment is expected to dominate the global coronary intravascular lithotripsy market in 2026, accounting for 64.6% of revenue, primarily due to the high prevalence of moderate-to-severe coronary calcification among patients undergoing PCI. Aging populations, diabetes, chronic kidney disease, and long-standing atherosclerosis significantly increase the incidence of calcified coronary lesions, which are difficult to treat using conventional balloon angioplasty alone. IVL provides controlled plaque modification with a favorable safety profile, making it increasingly preferred in complex coronary interventions. Rising global PCI procedure volumes and growing awareness of the long-term risks associated with underexpanded stents further drive adoption. Interventional cardiologists increasingly incorporate IVL into treatment algorithms for complex coronary anatomy, reinforcing coronary artery disease as the leading application segment within the global IVL market.

By End-user Insights

Hospitals are projected to dominate the global coronary intravascular lithotripsy market in 2026, accounting for 58.9% of revenue, owing to their role as primary centers for complex coronary interventions. Most IVL procedures are performed in hospital-based cardiac catheterization laboratories equipped with advanced imaging systems, trained interventional cardiologists, and comprehensive emergency support. Hospitals manage a high volume of elderly and high-risk patients with severe coronary calcification, making them the principal adopters of IVL technology. Favorable reimbursement pathways for inpatient and complex PCI procedures further strengthen hospital adoption. Additionally, hospitals often serve as early adopters of innovative cardiovascular technologies, thereby accelerating the uptake of IVL systems relative to outpatient settings. Integration of IVL into standardized PCI protocols and growing physician familiarity continue to reinforce hospital dominance within the end-user landscape.

Region-wise Insights

North America Coronary Intravascular Lithotripsy Market Trends

North America is expected to dominate the global coronary intravascular lithotripsy market, accounting for 48.3% of the market value in 2026, led primarily by the United States. The region benefits from a highly developed cardiovascular care ecosystem, high PCI procedure volumes, and early adoption of advanced interventional technologies. A significant proportion of coronary artery disease patients in North America present with severe calcification due to aging demographics, obesity, diabetes, and chronic kidney disease, creating strong clinical demand for IVL. Interventional cardiologists in the region demonstrate high awareness and acceptance of IVL as a safer and more predictable alternative to atherectomy in complex lesions.

Favorable reimbursement frameworks for advanced PCI procedures further support the adoption of technology. The strong presence of leading IVL manufacturers, continuous clinical trial activity, and rapid regulatory approvals accelerate innovation and market penetration. Increasing focus on improving long-term stent outcomes and reducing procedural complications continues to reinforce North America’s dominant position in the coronary intravascular lithotripsy market.

Europe Coronary Intravascular Lithotripsy Market Trends

The European coronary intravascular lithotripsy market is expected to grow steadily, supported by a rising burden of cardiovascular disease and an aging population across countries such as Germany, the U.K., France, Italy, and Spain. The increasing prevalence of coronary calcification among elderly patients has driven demand for advanced plaque modification technologies during PCI. European healthcare systems emphasize evidence-based adoption of innovative devices, and growing clinical data supporting IVL safety and efficacy have strengthened physician confidence. Hospitals across the region are increasingly incorporating IVL into complex PCI workflows, particularly for high-risk and calcified lesions.

Regulatory frameworks focused on medical device safety, quality, and clinical validation further enhance adoption. Expansion of specialized cardiac centers and improvements in interventional cardiology training also support market growth. Additionally, public healthcare funding and structured reimbursement mechanisms in several European countries facilitate access to IVL technology, contributing to sustained long-term expansion of the coronary intravascular lithotripsy market across the region.

Asia Pacific Coronary Intravascular Lithotripsy Market TrendsThe

Asia Pacific coronary intravascular lithotripsy market is expected to register a relatively higher CAGR of around 7.5% between 2026 and 2033, driven by rapid healthcare infrastructure development and rising cardiovascular disease prevalence. Countries such as China, India, Japan, South Korea, and Australia are witnessing increasing PCI volumes due to urbanization, lifestyle changes, and improved access to cardiac care. Growing awareness of advanced interventional techniques and expanding training programs for interventional cardiologists are accelerating the adoption of IVL.

The expansion of private hospitals and specialty cardiac centers is improving access to complex PCI procedures, particularly in urban areas. Government initiatives supporting healthcare modernization, rising healthcare expenditure, and improving insurance coverage further enhance market growth. Additionally, strategic expansion by global manufacturers, local distribution partnerships, and competitive pricing strategies are improving affordability and accessibility, positioning the Asia Pacific as the fastest-growing regional market for coronary intravascular lithotripsy.

Competitive Landscape

The global coronary intravascular lithotripsy (IVL) market is highly competitive, with strong participation from companies such as FastWave Medical Inc., Shockwave® Medical Inc., Boston Scientific Corporation, MicroPort Scientific Corporation, and Johnson & Johnson. These players leverage robust brand positioning, established global distribution networks, and deep expertise in interventional cardiology devices to address the rising burden of complex, heavily calcified coronary artery disease. Their solutions focus on improving calcium modification efficiency, procedural safety, balloon deliverability, and stent expansion outcomes, supported by advancements in acoustic pressure wave technology and catheter design. Continuous product innovation, clinical evidence generation, regulatory approvals, and strict adherence to international quality and safety standards remain critical for sustaining competitive advantage in the global coronary intravascular lithotripsy market.

Key Industry Developments:

- In October 2025, FastWave Medical unveiled its first-in-human (FIH) and preclinical results for the Sola™ coronary laser intravascular lithotripsy (L-IVL) system at TCT 2025 (Transcatheter Cardiovascular Therapeutics), the premier global symposium on interventional cardiovascular medicine hosted by the Cardiovascular Research Foundation (CRF).

- In April 2025, Shockwave Medical, Inc. (part of Johnson & Johnson MedTech) launched its pivotal FORWARD CAD IDE study to evaluate the safety and efficacy of the Javelin Coronary IVL Catheter for treating calcified, hard-to-cross de novo coronary lesions before stenting.

- In March 2025, Abbott announced that the FDA granted an investigational device exemption (IDE) for its Coronary Intravascular Lithotripsy (IVL) System to assess its safety and effectiveness in treating severe coronary artery calcification before stent implantation.

Companies Covered in Coronary Intravascular Lithotripsy Market

- FastWave Medical Inc.

- Shockwave® Medical Inc.

- Boston Scientific Corporation

- MicroPort Scientific Corporation

- Johnson & Johnson

- Abbott

- Elixir Medical

- Lepu Medical Technology (Beijing) Co., Ltd.

- Sino Medical Sciences Technology Inc.

- AVS Pulse, Inc.

- Spectrumedics International

- Others

Frequently Asked Questions

The global coronary intravascular lithotripsy market is projected to be valued at US$ 371.4 Mn in 2026.

Rising prevalence of calcified coronary artery disease and vascular calcification globally, coupled with increasing preference for minimally invasive cardiovascular procedures and strong clinical evidence supporting IVL efficacy.

The global coronary intravascular lithotripsy market is poised to witness a CAGR of 5.5% between 2026 and 2033.

Expansion into emerging regions with growing cardiovascular disease burdens and healthcare infrastructure development, and technological integration with advanced imaging and AI-enabled procedural support.

FastWave Medical Inc., Shockwave® Medical Inc., Boston Scientific Corporation, MicroPort Scientific Corporation, and Johnson & Johnson are some of the key players in the coronary intravascular lithotripsy market.