- Medical Devices

- Coronary Stents Market

Coronary Stents Market Size, Share, and Growth Forecast, 2025 - 2032

Coronary Stents Market By Product Type (Bare Metal, Drug Eluting, Bioresorbable Vascular Scaffolds), Mode of Delivery (Balloon-expandable, Self-expanding), Material (Metallic Stents, Cobalt Chromium), by End-user, and Regional Analysis for 2025 - 2032

Coronary Stents Market Size and Trends Analysis

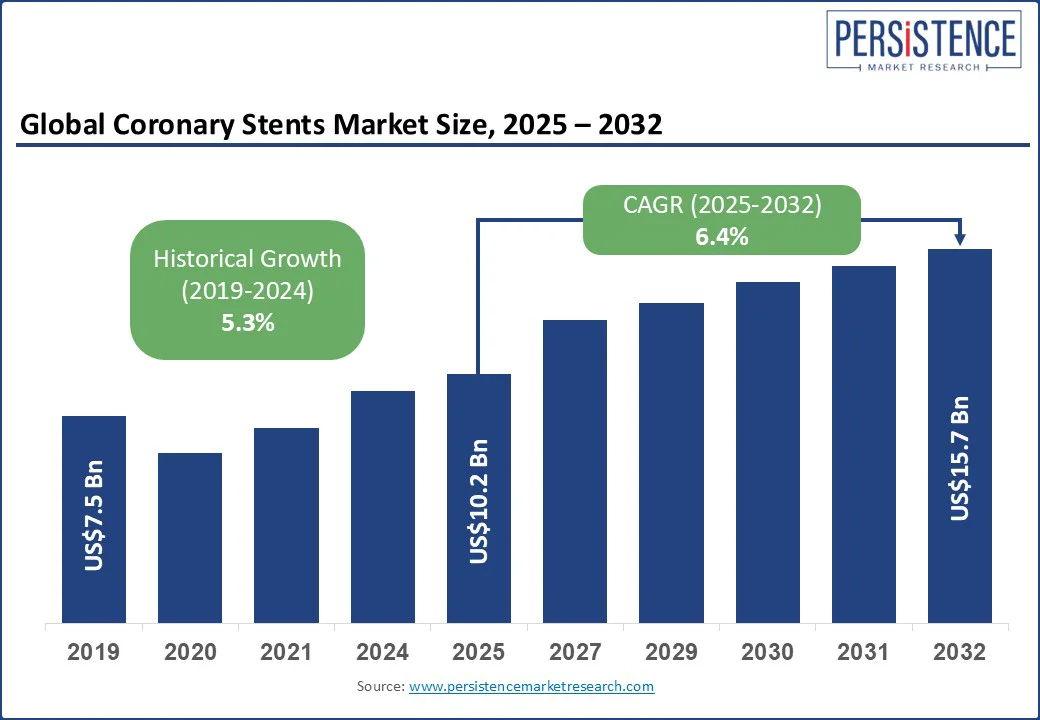

The global coronary stents market size is projected to rise from US$ 10.2 Bn in 2025 to US$ 15.7 Bn by 2032. It is anticipated to witness a CAGR of 6.4% during the forecast period from 2025 to 2032.

The coronary stents market growth is driven by increasing adoption of drug-eluting and bioresorbable variants with developments in materials science and precision manufacturing. Surging cardiovascular disease prevalence is pushing procedural volumes. Manufacturing companies are focusing on supply chain expansion and differentiated product portfolios to capture share in both mature and emerging economies.

Key Industry Highlights:

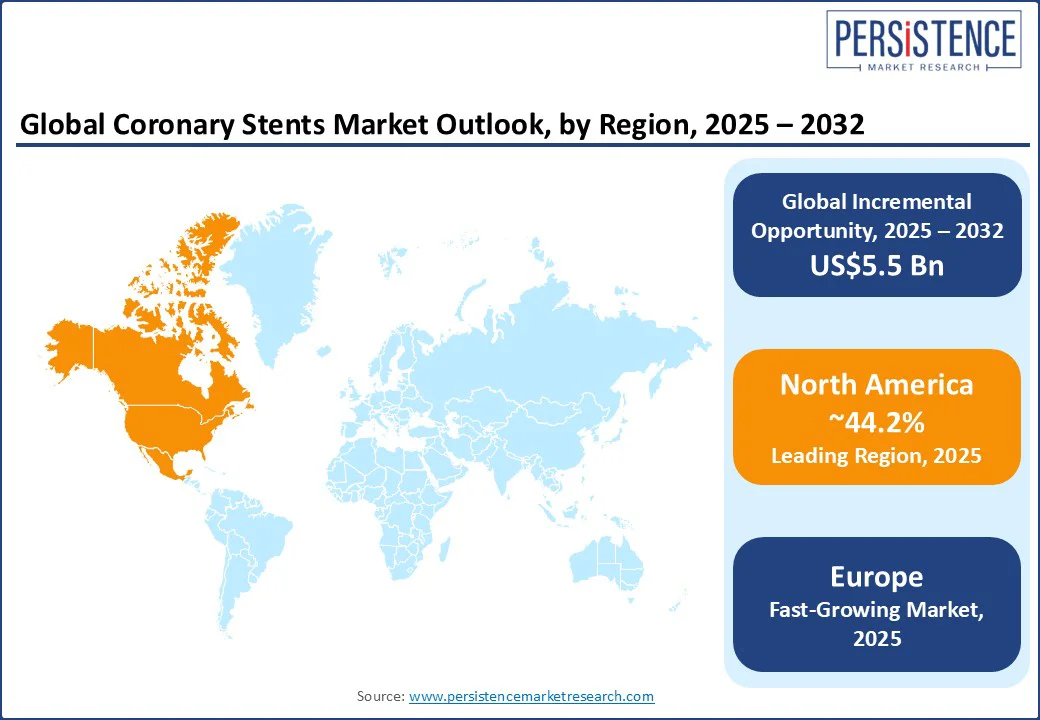

- Leading Region: North America, with around 44.2% share in 2025, spurred by early adoption of novel stent technologies and favorable reimbursement frameworks.

- Fastest-growing Region: Europe, due to increased adoption of next-generation stents under supportive regulatory pathways.

- Research Activity: Results from a randomized study published in the Journal of the American College of Cardiology demonstrated that treatment with a paclitaxel-coated balloon drastically reduced one-year Target Lesion Failure (TLF) in patients suffering from multilayer In-Stent Restenosis (ISR).

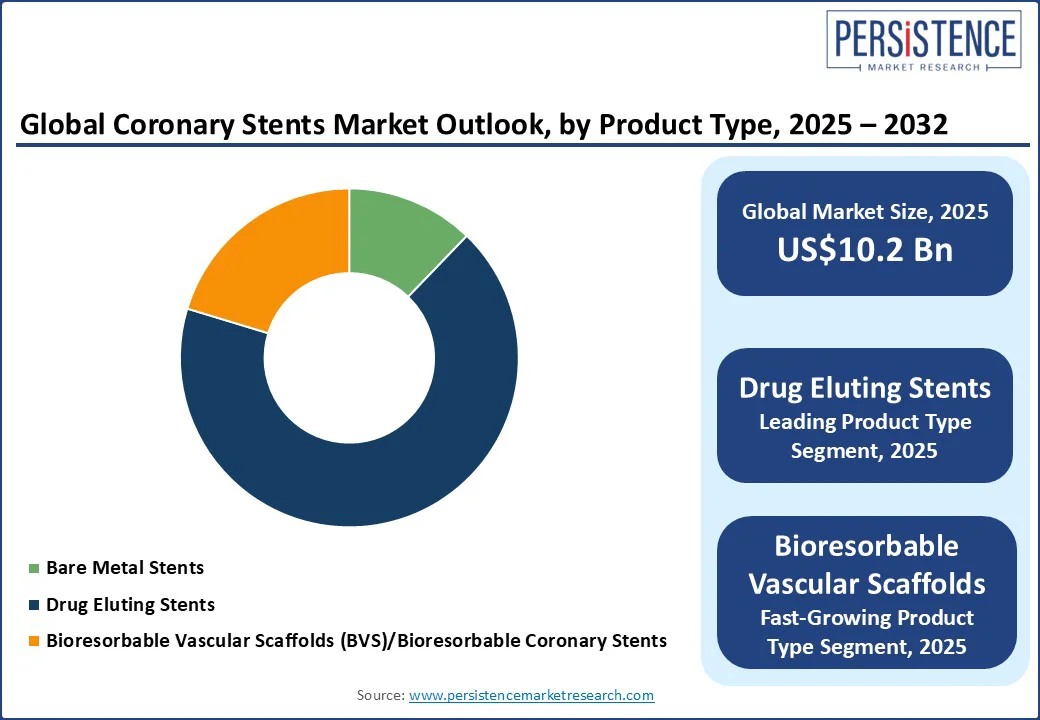

- Dominant Product Type: Drug eluting stents, approximately 67.5% share in 2025, fueled by their ability to lower restenosis rates and reduce the requirement for repeat interventions.

- Leading End-user: Outpatient facilities record nearly 58.3% share in 2025, augmented by developments in PCI techniques enabling same-day discharge.

|

Global Market Attribute |

Key Insights |

|

Coronary Stents Market Size (2025E) |

US$ 10.2 Bn |

|

Market Value Forecast (2032F) |

US$ 15.7 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.4% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.3% |

Market Dynamics

Driver - Rising CAD Cases Worldwide Spur Demand

The increasing prevalence of Coronary Artery Disease (CAD) is pushing demand for coronary stents by increasing the number of patients eligible for Percutaneous Coronary Intervention (PCI). Aging populations, high rates of obesity, diabetes, and hypertension, and lifestyle factors are spurring CAD cases worldwide. In China and India, the disease burden is increasing due to changing dietary patterns, resulting in a surging requirement for interventional treatments rather than solely medical management.

According to the American Heart Association’s 2024 update, CAD remains the leading cause of death in the U.S., affecting more than 20 Mn adults. A major portion of this population requires stent implantation to restore blood flow. In the Asia Pacific region, China performs over 1.2 million PCI procedures annually, with most of the cases involving DES. The trend is notable in countries adopting screening programs and early diagnostic interventions.

Restraint - Safety Concerns from Stent Recalls Hinder Physician Confidence

Product failures and recalls are hampering demand for coronary stents by eroding physician confidence and prompting hospitals to reassess procurement decisions. When safety concerns emerge, the reputational damage can extend across a manufacturer’s entire product line. This tends to delay purchasing cycles as clinicians wait for updated safety data or switch to alternative brands with strong post-market performance records.

In March 2023, Medtronic issued a voluntary recall of certain lots of its Onyx Frontier drug-eluting stent in the U.S. due to delivery system defects that could lead to balloon separation during use. Although no fatalities were reported, the recall prompted some hospitals to temporarily halt all new orders of the model until replacement inventory was verified. Similarly, Abbott’s 2017 global withdrawal of the first-generation Absorb bioresorbable vascular scaffold, following high thrombosis rates in long-term data, continues to influence perceptions of the latest BVS devices.

Opportunity - 3D Printing Enables Personalized Stents for Complex Vessel Anatomies

The emergence of 3D-printed coronary stents is creating new avenues by enabling personalized device design, improved material performance, and faster prototyping compared to conventional manufacturing. 3D printing allows for patient-specific geometries based on detailed imaging data, which can improve fit and reduce complications such as restenosis or stent migration. This customization is ideal for complex lesions or patients with atypical vessel anatomies, where off-the-shelf solutions do not provide optimal outcomes.

Recent developments are bolstering real-world applicability. In 2021, researchers at ETH Zurich, in collaboration with the University Hospital Zurich and University of Zurich, developed a 3D-printed bioresorbable airway stent using digital light processing (DLP). It was made from a custom, biocompatible resin and tested successfully in rabbits. The stents remained in place for around seven weeks before being fully absorbed and becoming radiographically invisible. As regulatory frameworks evolve to accommodate these technologies, 3D-printed coronary stents are predicted to transition from research to commercial use.

Category-wise Analysis

Product Type Insights

Based on product type, the market is trifurcated into bare metal stents, drug-eluting stents, and Bioresorbable Vascular Scaffolds (BVS)/bioresorbable coronary stents. Among these, Drug Eluting Stents (DES) are poised to hold approximately 67.5% of market share in 2025 as they release antiproliferative drugs that help reduce the risk of in-stent restenosis. This drug release prevents excessive tissue growth over the stent, which is a common drawback with bare-metal stents. Clinical trials consistently show lower rates of repeat revascularization with DES, making these a durable solution for several patients.

BVS/bioresorbable coronary stents are gaining momentum owing to their ability to provide temporary vessel support and then gradually dissolve, eliminating the long-term presence of a metallic implant. This restores natural vessel flexibility and function, which is not possible with permanent stents. They also help lower risks associated with chronic metal implants, including late stent thrombosis or impaired imaging for future interventions. Hence, these stents appeal to young patients who often require repeat procedures over their lifetime.

End-user Insights

By end-user, the market is segregated into inpatient and outpatient facilities. Out of these, outpatient facilities are expected to account for nearly 58.3% of the coronary stents market share, backed by developments in stent technology and procedural techniques. These have reduced the requirement for prolonged hospital stays. The shift toward minimally invasive Percutaneous Coronary Interventions (PCI), as well as improved DES designs, enables patients to be safely discharged the same day. This change not only improves patient comfort but also reduces healthcare costs.

Inpatient facilities are witnessing considerable growth due to the rising number of complex and high-risk cases that require intensive monitoring and multi-specialty care. Patients with multi-vessel disease, chronic total occlusions, or severe comorbidities often require extended hospitalization. The increasing prevalence of elderly patients with multiple health conditions in Europe and Japan is also spurring demand. This is because these cases frequently involve long recovery times and a high likelihood of complications.

Regional Insights

North America Coronary Stents Market Trends - The U.S. Leads with FDA Approval of Paclitaxel-coated Balloons

In 2025, North America is predicted to account for nearly 44.2% of market share owing to the presence of a well-established healthcare infrastructure, surging prevalence of cardiovascular disease, and developments in medical technology. The U.S. coronary stents market is anticipated to dominate with the rising preference for DES for various coronary interventions. Recent developments in stent technology have led to the emergence of bioresorbable scaffolds and Drug-Coated Balloons (DCBs). These provide alternatives for patients with specific requirements.

In March 2024, for example, the U.S. Food and Drug Administration (FDA) approved the Agent Coronary DCB, a paclitaxel-coated device, for the treatment of In-Stent Restenosis (ISR). It marked a key innovation in coronary intervention. Johnson & Johnson's acquisition of Shockwave Medical for US$ 13.1 Bn in 2024 highlighted the market’s focus on extending capabilities in treating complex coronary conditions. Shockwave's technology, which uses acoustic energy to treat calcified lesions, complements J & J's existing cardiovascular portfolio.

Europe Coronary Stents Market Trends - Regulatory Approvals Expand Clinical Use in Complex Cardiovascular Cases

Europe is spurred by recent regulatory approvals that broaden clinical use in complex cases. For instance, Biotronik’s Orsiro Mission DES gained approval in early 2025 for one-month dual antiplatelet therapy in high-bleeding-risk patients and for treating calcified lesions. It addresses the requirement for safe and effective interventions in vulnerable populations. In addition, Getinge’s Advanta V12 covered stent system secured EU MDR certification in 2024, mainly targeting renal artery stenosis and aortoiliac occlusive disease.

Developments such as Elixir Medical’s DynamX bioadaptor, presented at EuroPCR 2024, deliver a unique sirolimus-eluting device that restores coronary artery hemodynamic function. It shows promise in improving outcomes beyond traditional stent designs. These developments reflect a shift toward precision devices addressing highly specific anatomical and clinical challenges in cardiovascular care. Unlike other regions focusing mainly on broad market growth, Europe’s recent activity centers on intricate device approvals and specialized solutions that push clinical boundaries.

Asia Pacific Coronary Stents Market Trends - China Dominates through Government Procurement Initiatives

Asia Pacific is likely to be the fastest-growing region in 2025, due to large patient volumes, local manufacturing strength, and evolving healthcare infrastructure. In addition, accelerated regulatory approvals for new technologies and wide procedural access are supporting the market. China currently leads the regional market as local manufacturers supply more than 70% of stents used in the country. It is due to several government procurement programs and expanded insurance coverage. In 2024, Shanghai MicroPort Medical achieved a milestone with National Medical Products Administration (NMPA) approval for Firesorb, the world’s first fully bioresorbable coronary stent.

India’s market is boosted by affordability measures such as government-imposed price caps, which have widened access to novel DES while keeping procedure costs within reach of a surging middle class. Private healthcare expansion and increasing public investment in cardiac care are further augmenting adoption. Japan sustains high usage of drug-eluting metallic stents, bolstered by its aging population and universal health coverage that facilitates high intervention volumes.

Competitive Landscape

The global coronary stents market is characterized by a few key global players who dominate through research and development, extensive product portfolios, and powerful distribution networks. Key companies lead the market with their novel DES that focus on reducing restenosis and refining long-term patient outcomes. They invest heavily in research and development to create stents with thin struts, biodegradable polymers, and improved drug formulations. Regional players compete by delivering cost-effective Bare-Metal Stents (BMS) and early-generation DES, targeting price-sensitive segments.

Key Industry Developments

- In August 2025, a subgroup analysis from the AGENT IDE trial demonstrated that paclitaxel-coated drug-coated balloons (DCBs) effectively reduce restenosis in patients with multilayer coronary stent restenosis. This development provides a promising alternative to adding extra stent layers, improving treatment outcomes for patients with complex coronary artery disease.

- In May 2024, Abbott introduced the XIENCE Sierra Everolimus (drug) Eluting Coronary Stent System in India. It is one of the latest generations of stents in the XIENCE range, available to individuals suffering from blocked coronary arteries.

Companies Covered in Coronary Stents Market

- Abbott Laboratories

- Boston Scientific Corporation

- MicroPort Scientific Corporation

- Terumo Corporation

- Stentys SA

- B Braun SE

- C. R. Bard, Inc.

- Biotronik

- Cook Medical

- Meril Life Sciences Pvt. Ltd.

- Biosensors International Group Limited

Frequently Asked Questions

The coronary stents market is projected to reach US$ 10.2 Bn in 2025.

The rising global burden of coronary artery disease and the shift toward minimally invasive outpatient PCI procedures are the key market drivers.

The coronary stents market is poised to witness a CAGR of 6.4% from 2025 to 2032.

Increasing interest in biodegradable polymers for stents and integration of 3D printing in stent design are the key market opportunities.

Abbott Laboratories, Boston Scientific Corporation, and MicroPort Scientific Corporation are a few key market players.