- Hardware & Software IT Services

- Global Content Services Platform Market

Global Content Services Platform Market Size, Share, and Growth Forecast 2026 – 2033

Global Content Services Platform Market by Component (Solution [Document & Records Management, Workflow & Process Management, Information Security & Governance, Case Management, Data Capture & Indexing, Misc.], Services [Integration & Deployment, Consulting, Support & Maintenance]), by Deployment Model (Cloud, On-Premise, Hybrid), by Enterprise Size (Large Enterprises, Small & Medium Enterprises), by End Use Industry (BFSI, Government & Public Sector, IT & Telecommunications, Healthcare, Retail & e-Commerce, Manufacturing, Transportation & Logistics, Miscellaneous), and Regional Analysis, 2026–2033

Global Content Services Platform Market Size and Trend Analysis

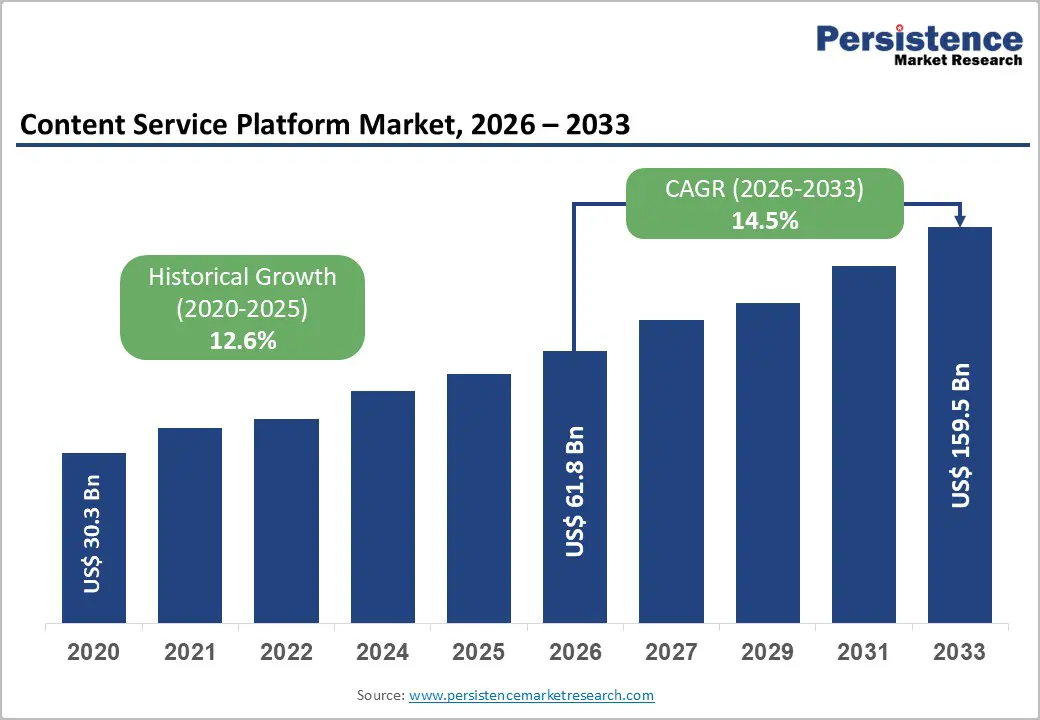

The global Content Services Platform market size is expected to be valued at US$ 61.8 billion in 2026 and projected to reach US$ 159.5 billion by 2033, growing at a CAGR of 14.5% between 2026 and 2033. The Content Services Platform market is on an exceptional growth trajectory, driven by the enterprise-wide imperative to unify fragmented document repositories, automate compliance-driven workflows, and enable intelligent information governance at scale across hybrid and multi-cloud environments.

The European Union's GDPR, the U.S. Securities and Exchange Commission (SEC)'s electronic recordkeeping mandates, and sector-specific frameworks, including HIPAA and Basel III, are compelling regulated industries, particularly BFSI, healthcare, and government, to deploy structured content management and audit-ready governance platforms as operational necessities. Simultaneously, the proliferation of digital-first enterprise architectures reinforced by ITU's estimate that approximately 74% of the global population was online in 2025 is generating document and unstructured data volumes that only purpose-built CSP platforms can govern, analyse, and operationalise at an organisational scale.

Key Market Highlights

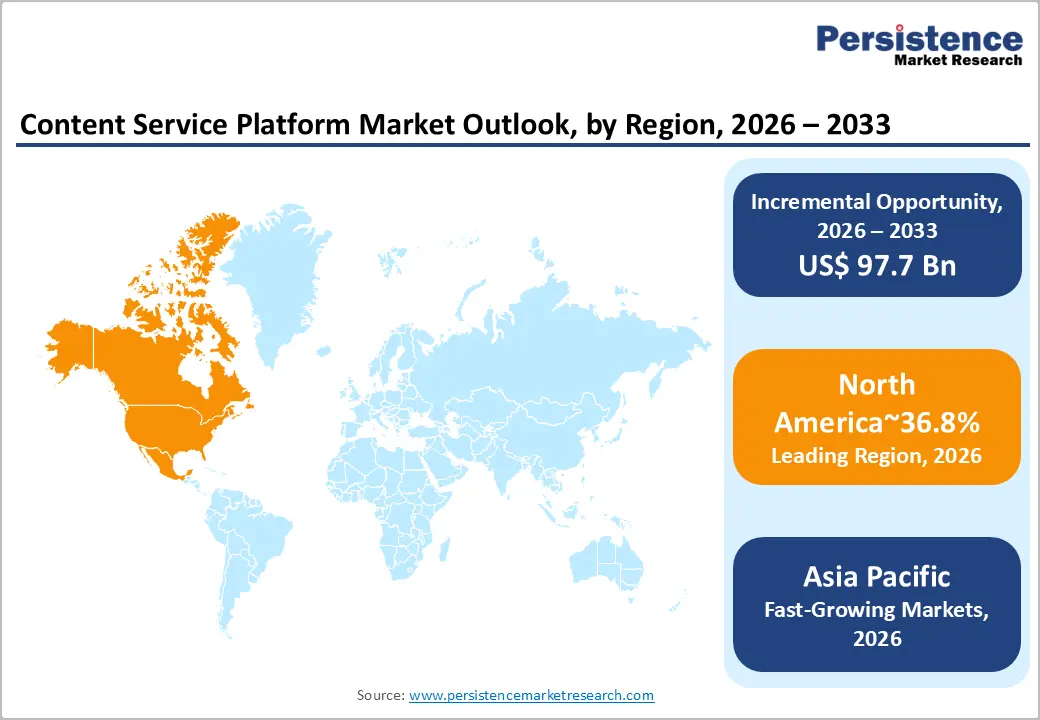

- Leading Region: North America leads the global Content Services Platform market with approximately 36.8% revenue share in 2025, anchored by the U.S. market valued at US$17.5 billion, driven by SEC recordkeeping mandates, HIPAA compliance obligations, and the world's highest concentration of enterprise CSP software vendors, including OpenText, Hyland, Laserfiche, Box, and Microsoft.

- Fat-Growing Region: Asia Pacific is the fastest-growing region through 2033, propelled by China's PIPL and Cybersecurity Law compliance mandates, India's BFSI sector reaching US$ 1 trillion market capitalisation and Digital Personal Data Protection Act obligations, and Japan's e-Document Law driving national-scale CSP deployment across financial services and government.

- Leading Component Type: The Solution component segment dominates with approximately 67% market share in 2025, reflecting enterprises' non-discretionary investment in Document & Records Management, Information Security & Governance, and Workflow & Process Management platforms driven by GDPR, SEC, HIPAA, and DORA compliance mandates across regulated industries globally.

- Fast-Growing Segment: The Services component segment is the fastest-growing category at a projected CAGR of 14% through 2033, fueled by surging demand for Integration & Deployment, Consulting, and Support services as enterprises migrate complex legacy ECM environments to cloud-native CSP architectures and embed generative AI capabilities within content governance workflows.

DRO Analysis

Market Growth Drivers

Regulatory Compliance Mandates Across BFSI and Healthcare: Compelling Information Governance Investment

The global regulatory landscape is imposing non-negotiable information governance obligations on enterprises across the most commercially significant end-use verticals, creating structurally embedded demand for Content Services Platforms that can automate records retention, audit trail generation, and compliance reporting. The European Union's financial and insurance sector, which generated €0.9 trillion in value added and employed nearly 5 million people across 867,000 enterprises in 2022, operates under layered compliance frameworks including MiFID II, DORA, GDPR, and the Digital Finance Package that each impose specific document management and evidence retention obligations.

In banking alone, the European Banking Authority (EBA) requires comprehensive document governance across credit risk models, stress test documentation, and supervisory disclosures, which demand that CSP solutions with built-in records management and audit workflows are architecturally designed to address. India's BFSI sector, which reached US$ 1 trillion in market capitalisation in 2025 while reducing gross NPAs to 2.2%, similarly requires robust case management and loan documentation governance platforms as the sector's complexity compounds.

Digital Transformation of Enterprise Operations Creating Unstructured Data Governance Challenges

The accelerating digitisation of enterprise operations spanning cloud migration, remote work infrastructure, and digital customer engagement is generating unstructured content volumes that are overwhelming legacy document management architectures and creating enterprise risk from uncontrolled information sprawl. The global B2B e-Commerce market, projected to reach US$ 36,163 billion in GMV by 2026 at a CAGR of 14.5%, is generating procurement contracts, supplier communications, compliance certificates, and transaction records at an industrial scale that demands CSP platforms capable of auto-classifying, indexing, and governing content in real time.

The EU's IT and communications sector employed nearly 7.2 million people and generated €667 billion in value added in 2022 (per Eurostat), with computer programming and IT services alone contributing 60% of sectoral employment, a workforce producing and consuming digital content at a rate that makes intelligent CSP governance a competitive necessity rather than a discretionary IT investment.

Market Restraints

Data Sovereignty Concerns and Multi-Jurisdictional Privacy Regulation Constraining Cloud CSP Adoption

The fragmented global landscape of data sovereignty legislation, including GDPR's data residency provisions, China's Personal Information Protection Law (PIPL), India's Digital Personal Data Protection Act (DPDPA) 2023, and sector-specific data localisation requirements in financial services and healthcare, creates a structural constraint on the deployment of cloud-hosted Content Services Platforms for multinational enterprises.

Organisations operating across jurisdictions with conflicting data residency requirements cannot freely migrate content to single-tenant cloud CSP environments without risking regulatory non-compliance, forcing either hybrid architectural compromises or costly multi-instance deployments. The compliance cost of multi-jurisdictional data management reduces the total cost of ownership advantage of cloud CSP relative to on-premises alternatives, moderating the pace of cloud migration in the most data-intensive enterprise verticals.

Market Opportunities

AI-Powered Document Intelligence and Generative AI Integration Within CSP Platforms

The integration of generative AI and large language model (LLM) capabilities directly within Content Services Platforms represents the most transformative near-term value expansion for both CSP vendors and enterprise buyers, unlocking intelligent document processing, automated contract analysis, AI-assisted case summarisation, and natural language-driven content discovery at enterprise scale. Microsoft's integration of Copilot AI capabilities within SharePoint and Microsoft 365, its primary CSP platform serving over 400 million commercial licenses, demonstrates the market validation of AI-augmented content services.

OpenText, Hyland, and M-Files are each embedding LLM-powered extraction, classification, and summarisation capabilities within their CSP offerings, compressing the value gap between structured and unstructured content governance. The European Commission's AI Act is simultaneously creating a regulatory framework that mandates documentation, transparency, and audit trails for AI systems a compliance requirement that CSP platforms with embedded AI governance modules are uniquely positioned to fulfil, creating a regulatory-demand feedback loop.

SME Segment Penetration Through Cloud-Native, Subscription-Based CSP Delivery Models

Small and medium enterprises represent the largest underserved addressable market in the Content Services Platform space, as the historical cost and implementation complexity of enterprise content management systems have historically positioned CSP as a large-enterprise-only proposition. The structural shift toward cloud-native, subscription-based CSP delivery with platforms including M-Files, DocuWare, Laserfiche, and Box offering SME-accessible pricing tiers is unlocking a vast new procurement stratum.

In the EU, approximately 1.4 million IT and communications enterprises operated in 2022, with the vast majority being SMEs , and the digitisation mandates of the EU's Data Act and eIDAS 2.0 are compelling even small businesses to adopt certified document management systems. India's IT sector, with its 979 million internet users, US$ 43.42 billion in telecom gross revenues in FY25, and a rapidly formalising SME economy, represents one of the highest-growth SME CSP penetration markets globally, where cloud-first platforms can leapfrog legacy system barriers entirely.

Category-wise Insights

Component Analysis

The Solution segment leads the Content Services Platform market by component, commanding approximately 67% of total market share in 2025. This dominance reflects enterprises' prioritisation of platform software over implementation services in the initial procurement cycle, with Document & Records Management, Information Security & Governance, and Workflow & Process Management sub-modules collectively constituting the highest-value solution components purchased at the platform license level.

The core compliance imperative across regulated industries, where GDPR penalties reach €20 million or 4% of global annual turnover, SEC recordkeeping failure fines, and HIPAA breach costs create existential incentives for robust records management, ensures that solution procurement remains non-discretionary for tier-1 enterprise buyers. OpenText's DOCUMENTUM, IBM FileNet, Microsoft SharePoint, and Hyland OnBase represent the dominant enterprise solution platforms, each commanding multi-year license commitments from regulated enterprise customers. The Services segment is the fastest-growing component at a projected CAGR of 14% through 2033.

Deployment Model Analysis

The Cloud deployment model leads the Content Services Platform market, accounting for approximately 54% of total market share in 2025, reflecting the enterprise sector's broad migration toward cloud-hosted content management infrastructure driven by scalability, total cost of ownership, and remote workforce enablement. Cloud CSP platforms offer elastic storage scaling for growing document volumes, seamless version management, mobile access for distributed teams, and built-in disaster recovery capabilities that on-premise alternatives cannot match at comparable cost. Microsoft 365 SharePoint Online, Google Workspace, Box, and Dropbox Business have each captured large enterprise and SME cloud CSP adoption at scale.

The Hybrid deployment model is the fastest-growing configuration, driven by multinational enterprises requiring on-premise data sovereignty compliance for specific jurisdictions while leveraging cloud scalability for global operations, a pattern particularly prevalent in BFSI and government end-users subject to multi-jurisdictional data residency obligations.

End Use Industry Analysis

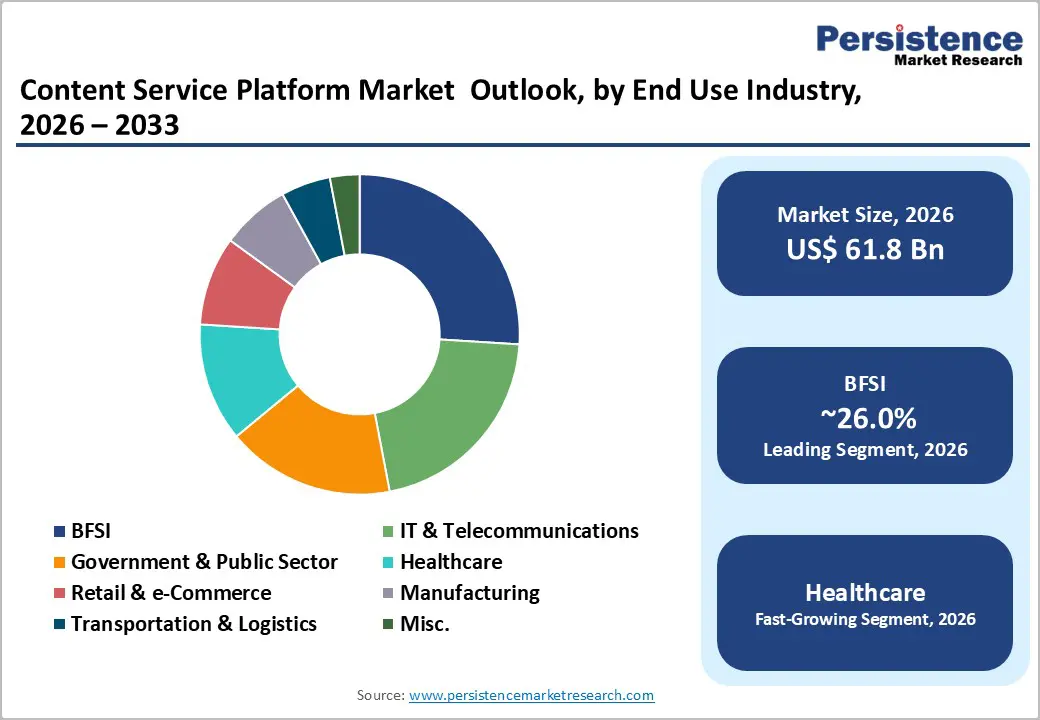

The BFSI sector is the dominant end-use industry for Content Services Platforms, commanding approximately 26% of global market share in 2025. Financial institutions deploy CSP across the broadest and most compliance-intensive use cases: loan origination document management, trade finance record governance, regulatory reporting archives, AML case management, and audit-ready correspondence storage, each demanding the highest tiers of information security, access control, and retention management.

China's banking sector alone reported total banking assets of RMB 467.3 trillion (up 7.9% YoY as of Q2 2025), while the European banking sector held assets of €43.6 trillion in 2023, scales of financial record generation that require industrial-grade CSP governance infrastructure. The Government & Public Sector end-use segment is the fastest-growing vertical, driven by e-government digital transformation mandates, freedom of information compliance requirements, and the universal public sector obligation to archive and retrieve government records across extended retention periods.

Regional Insights

North America Content Services Platform Market Trends and Insights

North America holds approximately 36.8% of the global Content Services Platform market revenue in 2025, anchored by the United States' position as the world's largest enterprise software market, the most stringent regulatory compliance environment for corporate recordkeeping, and the highest concentration of CSP platform vendors, including OpenText, Hyland, Laserfiche, Box, and Microsoft.

The region's market is being shaped by the SEC's electronic recordkeeping enforcement actions against major financial institutions, including US$ 1.8 billion in fines levied against 16 broker-dealers in 2022 for WhatsApp communication recordkeeping failures, compelling every financial services firm to upgrade their communications and document governance infrastructure urgently.

U.S. Content Services Platform Market Size

The U.S. Content Services Platform market is valued at approximately US$17.5 billion in 2025, driven by the structural convergence of SEC, FINRA, HIPAA, and FDA 21 CFR Part 11 compliance mandates that make CSP investment non-discretionary for the financial services, healthcare, and pharmaceutical sectors, collectively employing tens of millions of regulated workers.

The U.S. hosts over 6,500 medical device companies (per AdvaMed) and financial institutions managing trillions in regulated assets, each generating documentation governance requirements that sustain enterprise CSP procurement at scale. The Inflation Reduction Act's pharmaceutical pricing provisions are also compelling pharma companies to deploy robust clinical trial and regulatory submission document management platforms as competitive compliance infrastructure.

Europe Content Services Platform Market Trends and Insights

Europe accounts for approximately 24.2% of the global Content Services Platform market revenue in 2025, shaped by the world's most comprehensive data governance regulatory framework encompassing GDPR, the EU Data Act, eIDAS 2.0, DORA, and sector-specific mandates that collectively make structured content management a compliance obligation rather than a discretionary technology investment.

The EU's IT and communications sector, generating €667 billion in value added with 7.2 million employees in 2022, is both a primary demand driver and a major supplier of CSP integration and consulting services, with Germany leading in absolute terms by contributing over 22% of EU-wide IT sector value added.

Germany Content Services Platform Market Size

Germany's Content Services Platform market is valued at approximately US$3.9 billion in 2025, driven by the country's industrial-scale document governance requirements across its automotive, chemical, and financial services sectors, and its leading position in EU-wide IT value added. Germany's GoBD (Grundsätze zur ordnungsmäßigen Führung und Aufbewahrung von Büchern) electronic bookkeeping compliance requirements, combined with GDPR enforcement by the Bundesdatenschutzbeauftragter (BfDI), create mandatory CSP adoption frameworks for enterprises across every commercial sector.

U.K. Content Services Platform Market Size

The U.K. Content Services Platform market is valued at approximately US$3.4 billion in 2025, sustained by the FCA's MiFID II-derived transaction reporting and communications recordkeeping obligations, the NHS's clinical document management requirements, and the UK Government's digital transformation agenda under the Central Digital and Data Office (CDDO).

The UK's post-Brexit independent data regulation trajectory, including the Data Protection and Digital Information Act, is creating UK-specific CSP configuration requirements that differentiate the domestic market from EU-standard deployments.

Asia Pacific Content Services Platform Market Trends and Insights

Asia Pacific holds approximately 27.5% of global Content Services Platform market revenue in 2025 and is the fastest-growing region, projected to expand at the highest regional CAGR through 2033. China is the region's largest individual market, driven by its massive BFSI sector with total banking assets of RMB 467.3 trillion (up 7.9% YoY as of Q2 2025) and the government's digital economy mandates under the 14th Five-Year Plan requiring electronic records management across state-owned enterprises.

India is the fastest-growing country market within Asia Pacific, underpinned by its 979 million internet users, the BFSI sector's US$ 1 trillion market capitalisation milestone in 2025, and government digital transformation under the Digital India mission.

China Content Services Platform Market Size

China's Content Services Platform market is valued at approximately US$5.8 billion in 2025, propelled by state-mandated electronic recordkeeping compliance under the Cybersecurity Law, PIPL, and Data Security Law, which collectively impose comprehensive content governance obligations on enterprises handling personal or sensitive data.

China's banking sector, managing assets of RMB 467.3 trillion with an NPL ratio of just 1.49% as of Q2 2025, requires industrial-scale loan documentation, regulatory reporting, and audit trail governance that CSP platforms with localised data residency and Chinese-language NLP capabilities uniquely address.

India Content Services Platform Market Size

India's Content Services Platform market is valued at approximately US$3.7 billion in 2025 and is among the fastest-growing country-level CSP markets globally, anchored by the country's BFSI sector's rapid formalisation, having expanded market capitalisation 50 times to US$ 1 trillion by 2025 while reducing NPAs to 2.2%, which compels comprehensive loan documentation, case management, and regulatory reporting CSP deployments.

India's telecom sector gross revenue of US$ 43.42 billion in FY25, combined with the country's Digital Personal Data Protection Act 2023, creating new records management obligations, is accelerating enterprise CSP adoption across IT-intensive industries.

Competitive Landscape

Market Structure Analysis

The global Content Services Platform market is moderately consolidated, with enterprise software conglomerates OpenText, IBM (FileNet), Microsoft (SharePoint), Hyland, Laserfiche, M-Files, and Box commanding significant combined share across large enterprise accounts. However, the cloud-native SaaS tier is substantially more fragmented, with specialised vertical players, regional vendors, and AI-native entrants competing effectively.

Key differentiators are AI document intelligence depth, regulatory compliance certification coverage, vertical-specific workflow templates, and pre-built ERP integration connectors. The dominant emerging business model is the intelligent content services platform embedding AI classification, generative AI summarisation, and automated governance within a unified SaaS architecture, replacing legacy point-solution ECM with horizontal, AI-augmented content operating platforms that generate recurring subscription and usage-based revenue.

Key Market Developments

- In April 2026, Box announced the general availability of the Box Agent, an AI-powered capability designed to transform enterprise interaction with unstructured content. The Box Agent leverages advanced AI reasoning models to enable enterprises to search, analyze, synthesise, and generate content autonomously across enterprise files while maintaining built-in security, governance, and access control frameworks.

In April 2026, Oracle, in partnership with Google Cloud, announced the expansion of its Oracle AI Database@Google Cloud platform, introducing the Oracle AI Database Agent for Gemini Enterprise, enabling enterprises to interact with governed enterprise data using natural language instead of SQL-based querying. This development enhances the broader Content Services Platform (CSP) ecosystem by improving intelligent access, retrieval, and utilisation of enterprise content and structured/unstructured data.

Companies Covered in Global Content Services Platform Market

- OpenText Corporation

- IBM Corporation (FileNet)

- Microsoft Corporation (SharePoint)

- Hyland Software

- Laserfiche

- M-Files Corporation

- Box Inc.

- Newgen Software Technologies

- Kofax (Tungsten Automation)

- DocuWare GmbH

- Fabasoft

- Kyocera Document Solutions

- Oracle Corporation

- SAP SE

- Google LLC

Frequently Asked Questions

The global Content Services Platform market is valued at US$ 61.8 Billion in 2026, driven by AI integration, regulatory compliance mandates, and enterprise cloud content migration acceleration across BFSI, government, and healthcare sectors.

The two primary drivers are regulatory compliance mandates across BFSI and healthcare with GDPR penalties up to €20 million, SEC recordkeeping fines exceeding US$ 1.8 billion across 16 broker-dealers in 2022, and HIPAA breach costs compelling non-discretionary CSP investment, and the enterprise digital transformation imperative that is generating unstructured content volumes across cloud, remote work, and B2B e-commerce environments that only structured CSP governance can manage.

North America leads with approximately 36.8% revenue share in 2025, anchored by the U.S. market valued at US$ 17.5 Billion. This leadership reflects the world's most stringent corporate recordkeeping regulation SEC, FINRA, HIPAA, and FDA 21 CFR combined with the highest concentration of enterprise CSP software vendors and the largest installed base of regulated enterprises requiring sophisticated document governance infrastructure globally.

AI-powered intelligent content services represent the most transformative opportunity, with Microsoft Copilot's 400 million+ commercial license base, OpenText Aviator's generative AI platform, and AI-native entrants enabling automated document governance, contract intelligence, and regulatory compliance automation. The EU AI Act's documentation mandates are simultaneously creating a regulatory-demand feedback loop that positions AI-integrated CSP platforms as compliance infrastructure for every enterprise deploying AI systems.

The market is led by OpenText Corporation (Content Cloud and Aviator AI platform), Microsoft Corporation (SharePoint Premium with Copilot AI), IBM Corporation (FileNet / Content Manager for regulated enterprise), Hyland Software (OnBase, Nuxeo, Alfresco consolidated platform), and Laserfiche (government and financial services specialist). M-Files, Box, Newgen Software, Kofax (Tungsten Automation), and DocuWare represent significant mid-market and SME-focused participants.