- Hardware & Software IT Services

- Structured Content and Product Label Management Market

Structured Content and Product Label Management Market Size, Share, and Growth Forecast, 2025 - 2032

Structured Content and Product Label Management Market by Solution Type (Software, Services), Deployment Model (Cloud-based, Others), Application (Pharmaceuticals, Others), Functionality (Label Design, Version Control, Others), and Regional Analysis for 2025 - 2032

Structured Content and Product Label Management Market Size and Trends Analysis

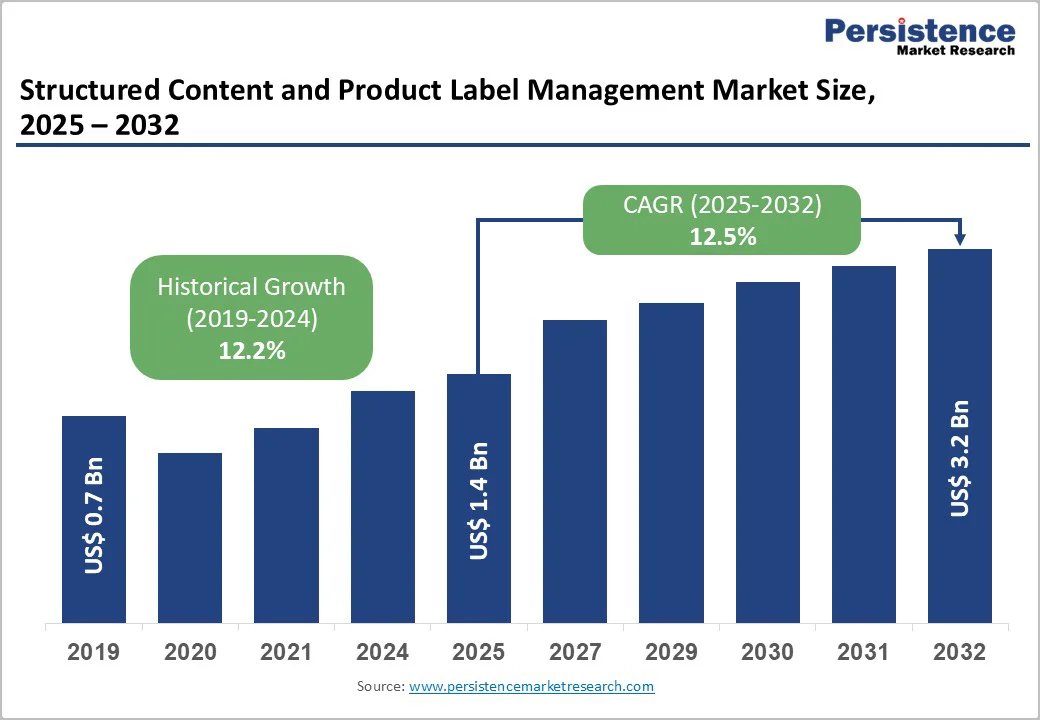

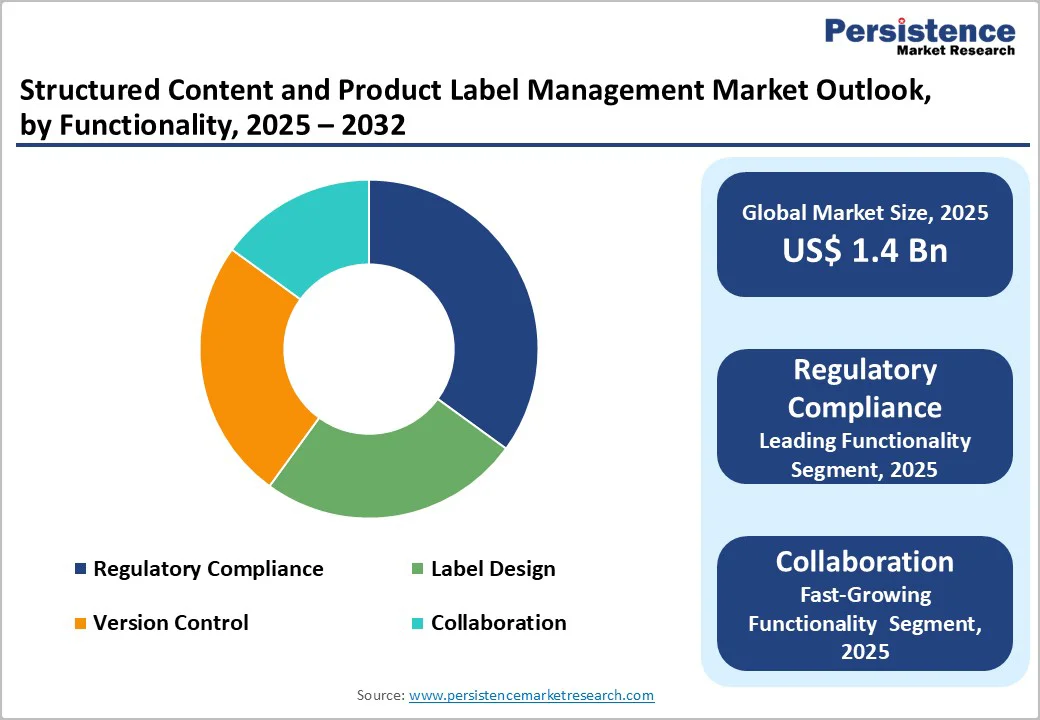

The global structured content and product label management market size is likely to be valued at US$1.4 billion in 2025. It is expected to reach US$3.2 billion by 2032, growing at a CAGR of 12.5% during the forecast period from 2025 to 2032, driven by the increasing prevalence of regulatory compliance requirements, rising demand for efficient label lifecycle management in pharmaceuticals, and advancements in digital workflow technologies.

The growing demand for accurate, multilingual labeling and strict version control, especially in the food & beverage industry, is driving the rapid adoption of structured content and product label management. Cloud-based, collaborative platforms are accelerating growth by offering scalable, integrated solutions, while rising emphasis on supply chain transparency in consumer goods is reinforcing these tools as business-critical.

Key Industry Highlights:

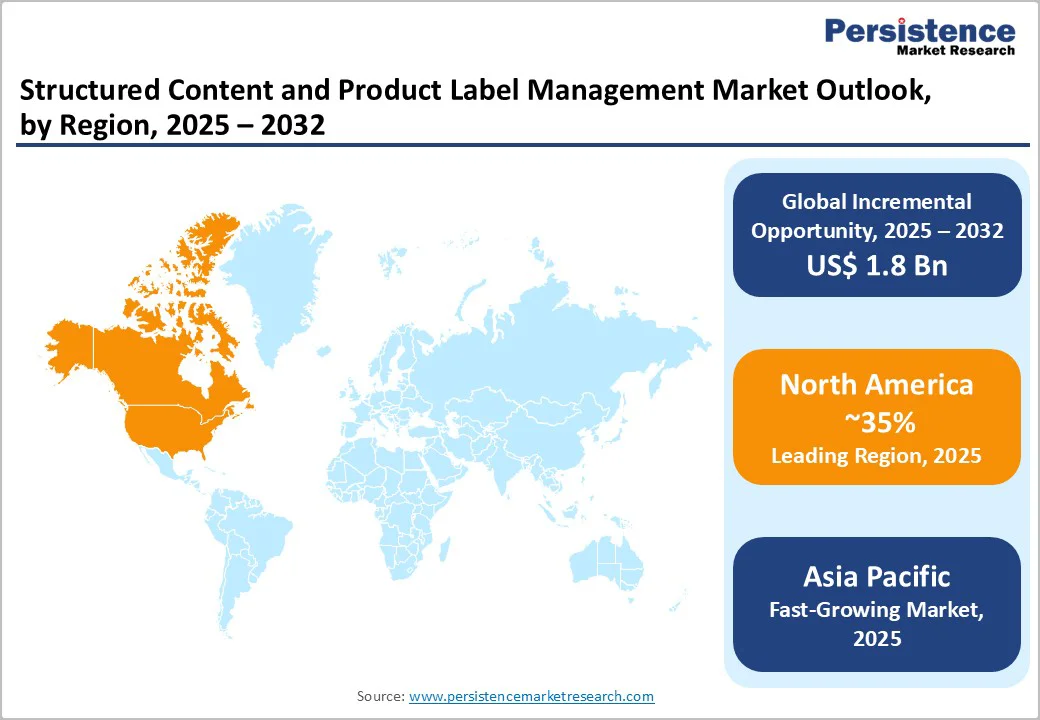

- Leading Region: North America, with a 35% market share in 2025, driven by stringent FDA regulations, high prevalence of pharma labeling, and strong R&D activities in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by increasing manufacturing hubs, rising awareness of compliance software, and growing investments in digital transformation in China and India.

- Dominant Solution Type: Software, holding 60% of the market share, due to core automation capabilities.

- Leading Deployment Model: Cloud-based, accounting for 55% of market revenue, driven by scalability needs.

- Leading Application: Pharmaceuticals, contributing nearly 45% of market revenue, due to regulatory demands.

- Leading Functionality: Regulatory Compliance, with 35% share, driven by audit trails.

| Key Insights | Details |

|---|---|

|

Structured Content and Product Label Management Market Size (2025E) |

US$1.4 Bn |

|

Market Value Forecast (2032F) |

US$3.2 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

12.5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

12.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Regulatory Compliance Pressure Driving Label Lifecycle Automation

The rising prevalence of regulatory compliance requirements and the growing demand for efficient label lifecycle management are significantly shaping the structured content and product label management market. Industries such as pharmaceuticals, medical devices, chemicals, and food & beverages face increasingly complex regulations that mandate accuracy, transparency, and real-time traceability of product information. Frequent updates from regulatory bodies such as the FDA, EMA, and regional authorities require companies to maintain consistent, validated, and up-to-date labels across all markets. This makes manual processes prone to errors, delays, and costly non-compliance risks.

Organizations are shifting toward structured content management systems that centralize information, automate validation, and streamline approval workflows. Efficient label lifecycle management is becoming essential to reduce time-to-market, avoid product recalls, maintain audit readiness, and ensure alignment across packaging, digital channels, and global submissions. Automation, version control, and standardized templates help accelerate updates while preserving accuracy. Globalization and the expansion of multi-product portfolios demand systems capable of managing large volumes of content simultaneously.

High Development and Integration Costs

The substantial costs of developing and integrating structured content and product label management systems are a major constraint on market growth. Creating advanced solutions with AI-driven features, automated workflows, and regulatory intelligence demands heavy investment in development, testing, and ongoing maintenance. For many organizations, particularly small and mid-sized enterprises, these high upfront expenses can be a significant barrier to adoption.

Integration adds another layer of complexity. Structured content and labeling platforms must synchronize with existing systems, including ERP, PLM, QMS, CRM, and regulatory databases. Ensuring seamless data flow, maintaining compatibility, and customizing solutions for industry-specific workflows require skilled implementation teams, long deployment timelines, and substantial financial commitment. Hidden expenditures, including employee training, migration of large content libraries, ongoing maintenance, cybersecurity enhancements, and periodic compliance updates, further increase the total cost of ownership. For global enterprises operating across multiple regulatory environments, costs rise further due to localization requirements, multilingual support, and validation testing.

Advancements in AI-Enhanced Content Validation and Blockchain Traceability

Advancements in AI-enhanced content validation and blockchain-based traceability are transforming the structured content and product label management market by improving accuracy, security, and regulatory compliance. AI-powered validation tools now automate the review of complex labeling content, detecting inconsistencies, missing data, outdated references, and non-compliant elements in seconds. This significantly reduces manual workload, shortens approval cycles, and minimizes the risk of regulatory errors, especially in pharmaceuticals, medical devices, and chemicals, where precision is critical. Natural language processing (NLP) and machine learning further enable automated comparison of global regulatory guidelines, ensuring labels remain up to date across regions.

Blockchain traceability brings unmatched transparency and integrity to product labeling workflows. Each update, approval, or modification in a label is recorded as a tamper-proof transaction, strengthening audit trails and enhancing trust among manufacturers, regulators, and supply chain partners. Blockchain also supports end-to-end product authentication, crucial for high-risk categories such as drugs and medical devices.

Category-wise Analysis

Solution Type Insights

Software dominates the market, accounting for 60% of the share in 2025, due to its ability to streamline complex operations through automation, scalability, and frequent updates. Enterprise software solutions, for example, those offered by Veeva Systems Inc., enable efficient template and document management, ensuring consistency, regulatory compliance, and audit readiness across multiple sites. Cloud-based deployment enhances flexibility, real-time collaboration, and remote access, making these solutions highly preferred by manufacturers seeking to optimize workflows, maintain data integrity, and accelerate operational efficiency.

Services are the fastest-growing segment, as companies increasingly rely on consulting and implementation partners to navigate complex digital transformations, cloud adoption, and emerging technologies such as AI. These services offer customized solutions, managed innovation, and deep expertise, making them especially valuable for large enterprises seeking business agility and competitive advantage. Demand is strongest in North America and Europe. For example, Accenture is expanding AI consulting and implementation offerings to help enterprises adopt advanced technologies, a trend reflecting strong demand for services-led solutions in complex digital projects.

Deployment Model Insights

Cloud-based leads the market, holding 55% of the market share in 2025, due to its scalability, ease of remote access, and seamless cross-team collaboration. Organizations prefer cloud platforms for faster deployments, lower infrastructure costs, and real-time updates. As global teams and digital workflows expand, demand for cloud-based structured content and label management continues to rise, strengthening their market dominance. For example, the U.S. Federal Cloud Computing Strategy “Cloud Smart” promotes cloud adoption to modernize federal IT, improve service delivery, and enable secure, scalable, and flexible operations across agencies, highlighting the cloud’s role in supporting collaboration and real-time access to data and services.

Hybrid is the fastest-growing segment, as it offers the perfect balance of on-premise control and cloud-based scalability. Regulated industries prefer this model for its strong security, ease of compliance, and the ability to keep sensitive data in-house while still benefiting from cloud efficiency. This flexibility accelerates adoption, especially among companies modernizing legacy systems without full cloud migration. For example, the Government of Telangana’s Cloud Adoption Policy explicitly mandates cloud deployment for e-governance applications except “Top Secret and Secret” data, to ensure agility and scalability while keeping highly sensitive data under local control. This reflects hybrid models in practice, where governments balance on-premise security with cloud benefits to meet regulatory and operational requirements.

Application Insights

Pharmaceuticals dominate the market, contributing nearly 45% of revenue in 2025, as the industry relies heavily on precise, compliant, and frequently updated product information. Strict regulatory frameworks, such as the FDA and EMA guidelines, require accurate labeling, structured content, and real-time documentation control. Growing drug approvals, complex portfolios, and global market expansions further increase the need for advanced content and label management solutions. For example, the U.S. FDA’s Structured Product Labeling (SPL) standard mandates the electronic submission of drug labeling content, including text, tables, and figures, for human drugs and biologics in a machine-readable XML format. This ensures consistent, accurate, and accessible product information across applications and updates, reflecting strict regulatory control in the pharma sector.

Medical devices are the fastest-growing segment, driven by stricter FDA mandates and the expanding need for precise traceability. The rise of Unique Device Identification (UDI) requirements pushes companies to adopt structured content and labeling systems. These solutions offer versatility, ensure accuracy across product variations, and streamline global submissions, making them essential for fast-evolving medical device portfolios. For example, the FDA’s UDI System requires device labelers to include a unique device identifier on packaging and submit standardized device information to the GUDID, improving identification, traceability, and postmarket surveillance.

Functionality Insights

Regulatory compliance commands about 35% of market revenue in 2025, driven by stringent government requirements that force companies to maintain accurate, audit-ready documentation for product approvals, submissions, and ongoing compliance. For example, the U.S. FDA requires regulated industries such as pharmaceuticals, biologics, and medical devices to submit regulatory applications (e.g., INDs, NDAs, ANDAs, BLAs) in the Electronic Common Technical Document (eCTD) format, ensuring standardized, structured, and complete content for review and archiving. Failure to meet these content standards can delay approvals, making compliance tools essential for preparing, validating, and managing submission documents efficiently.

Collaboration is the fastest-growing, as remote and globally distributed teams increasingly rely on real-time content creation and review. Companies value shared workspaces, instant updates, and synchronized version control to speed approvals and reduce errors. Seamless integration with regulatory, quality, and enterprise systems further boosts adoption, enabling efficient teamwork and consistent labeling across multiple regions. For example, the FDA’s Structured Product Labeling (SPL) requirement. SPL mandates that pharmaceutical and medical device companies create, review, and submit labeling content in a standardized digital format, requiring multiple teams, regulatory affairs, quality, medical, and IT to work simultaneously on the same content to avoid inconsistencies.

Regional Insights

North America Structured Content and Product Label Management Market Trends

North America dominates the market, accounting for a 35% share in 2025, and is advancing rapidly as industries prioritize regulatory compliance, operational efficiency, and accelerated product launches. The region’s pharmaceutical, biotechnology, medical device, and consumer goods sectors operate under strict frameworks such as the FDA, Health Canada, and GMP guidelines, pushing companies to adopt structured, centrally managed labeling systems. This shift supports accuracy, auditability, and faster approval cycles, especially for products with frequent updates or multiple regional versions.

Integration of structured content platforms with enterprise systems such as ERP, QMS, and RIM is accelerating as organizations adopt cloud-based architectures that enable flexibility, real-time collaboration, and robust data governance. AI-powered authoring, automated content validation, and predictive compliance tools are gaining traction, helping companies minimize labeling errors and shorten review cycles. Across North America, digital transformation initiatives are driving a shift from static documents to modular content models that ensure consistency across multiple channels and product lines.

Europe Structured Content and Product Label Management Market Trends

The European market is evolving quickly as regulatory expectations, digitalization, and quality-driven operations reshape how companies manage product information. With stringent frameworks such as the EMA guidelines, REACH, MDR, and food safety regulations, European manufacturers are prioritizing structured authoring and centralized content systems to ensure accuracy, traceability, and fast regulatory submissions. This is driving strong adoption across pharmaceuticals, medical devices, chemicals, and packaged goods.

The shift toward integrated platforms that connect labeling with regulatory information management, quality systems, and product lifecycle management. Companies are investing in structured content models that allow reusable components and consistent messaging across countries and languages. Cloud-based deployments are gaining momentum, especially among mid-sized firms that need scalable and secure solutions without heavy infrastructure costs.

AI-enabled content automation, automatic compliance checks, and smart translation tools are increasingly embedded into European workflows, helping reduce review cycles and minimize labeling errors. Sustainability initiatives are also influencing labeling strategies, with companies using digital tools to support eco-friendly designs and to communicate product transparency.

Asia Pacific Structured Content and Product Label Management Market Trends

Asia Pacific is the fastest-growing market for structured content and product label management, driven by accelerating digital transformation across pharmaceuticals, medical devices, food and beverage, and consumer goods industries. Companies in the region are increasingly moving from manual, document-heavy labeling practices to structured, automated systems that ensure accuracy, regulatory compliance, and faster product rollout. Growing alignment with international regulatory standards, particularly in China, India, South Korea, and Japan, is pushing organizations to adopt centralized content platforms that can manage multilingual labels and frequent regulatory updates.

Cloud adoption is a major trend, as regional manufacturers and contract development and manufacturing organizations (CDMOs) prefer scalable, subscription-based solutions that reduce IT burden. Local vendors and global players are investing in AI-enabled authoring tools, automated validation, and rule-based compliance engines to serve markets with diverse regulatory environments. The rise of regional pharma manufacturing hubs and strong growth in export-oriented industries further enhance the demand for consistent, high-quality labeling.

Competitive Landscape

The global structured content and product label management market is highly competitive, with a mix of large software vendors and niche technology specialists. In North America and Europe, companies such as Veeva Systems Inc. and Oracle lead due to strong R&D, integrated regulatory platforms, and long-standing relationships with pharmaceutical, medical device, and consumer goods firms.

In Asia Pacific, players like i4i Inc. are gaining traction through localized expertise and cost-effective implementations. Competition increasingly centers on AI-driven automation, smart validation, and structured authoring. Strategic partnerships, acquisitions, and cloud expansion are key strategies, with vendors offering scalable, compliant solutions gaining an advantage.

Key Industry Developments

- In October 2025, Veeva Systems announced the integration of agentic AI into the Veeva Vault Platform through Veeva AI Agents, expanding intelligent automation across clinical, regulatory, quality, safety, medical, and commercial functions to enhance productivity, decision-making, and end-to-end lifecycle management.

- In September 2025, Specright expanded its platform with AI-driven PLM capabilities tailored for the food & beverage industry, strengthening its spec-first strategy to help brands accelerate innovation while improving compliance, sustainability, and quality management across formulas, ingredients, packaging, and bills of materials.

Companies Covered in Structured Content and Product Label Management Market

- Veeva Systems Inc.

- Zebra Technologies Corp.

- Loftware Inc.

- Oracle

- Salesforce, Inc.

- i4i.inc.

- DITA Exchange ApS

- Data Conversion Laboratory

- Freyr

- Others

Frequently Asked Questions

The global structured content and product label management market is projected to reach US$1.4 billion in 2025.

Stringent global regulations on product labeling and content management are accelerating the adoption of structured solutions in regulated industries.

The structured content and product label management market is expected to grow at a CAGR of 12.5% from 2025 to 2032.

Expansion in food & beverage and consumer goods creates strong opportunities for AI-enhanced, multilingual label management platforms.

Key players include Veeva Systems Inc., Loftware Inc., Oracle, Salesforce, Inc., and Zebra Technologies Corp.