- Non-food Packaging

- Compostable Food Trays Market

Compostable Food Trays Market Size, Share, and Growth Forecast, 2026 - 2033

Compostable Food Trays Market By Material (Bagasse, Bamboo, Others), Compartment (Single, 2 to 5, More than 5), End-user, and Regional Analysis for 2026 - 2033

Compostable Food Trays Market Size and Trends Analysis

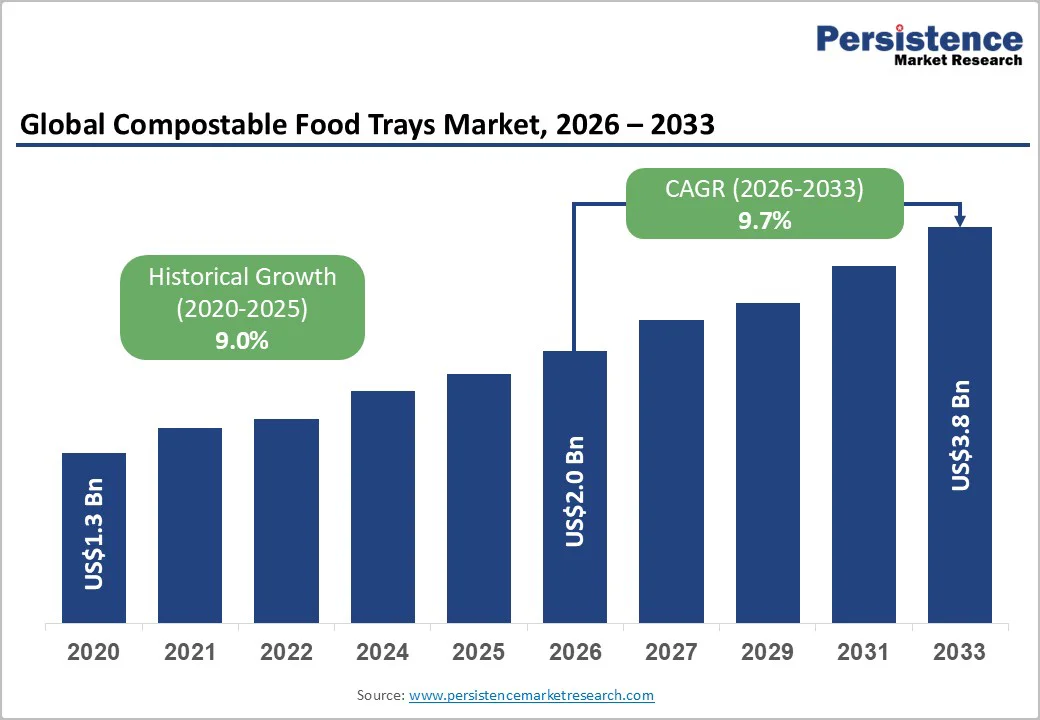

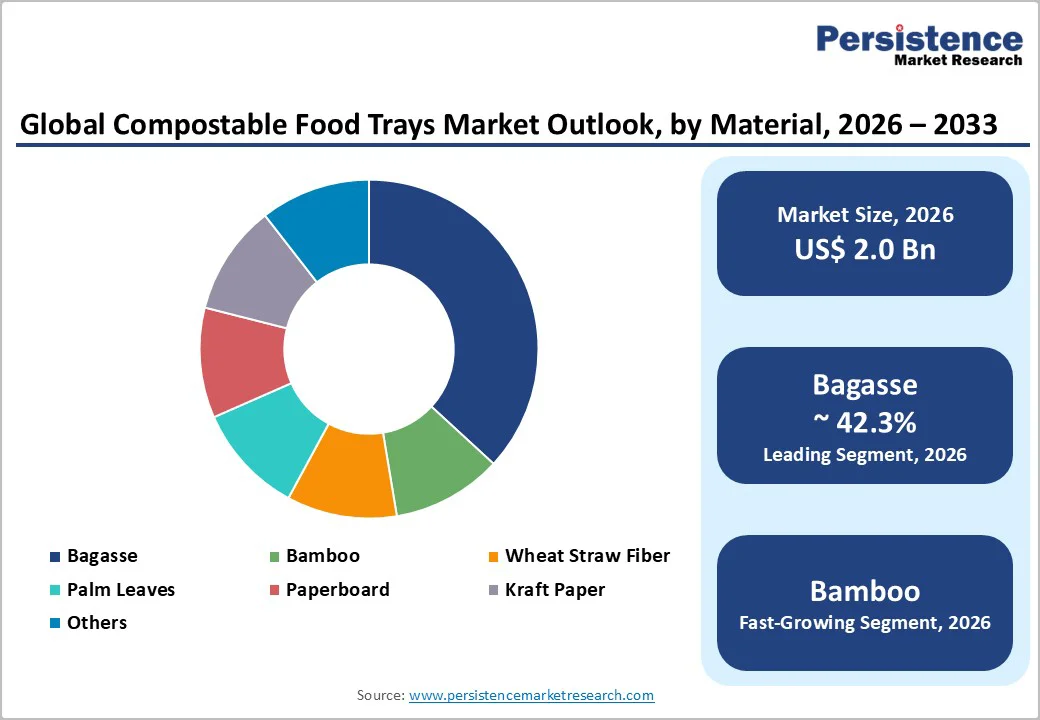

The global compostable food trays market size is likely to be valued at US$2.0 billion in 2026 and is expected to reach US$3.8 billion by 2033, growing at a CAGR of 9.7% during the forecast period from 2026 to 2033, driven by demand from foodservice operators, regulatory initiatives aimed at reducing single-use plastics, and the expansion of industrial composting infrastructure.

Additional drivers include policy mandates, increased availability of agricultural fiber feedstock, and rising off-premise food consumption.

Key Industry Highlights

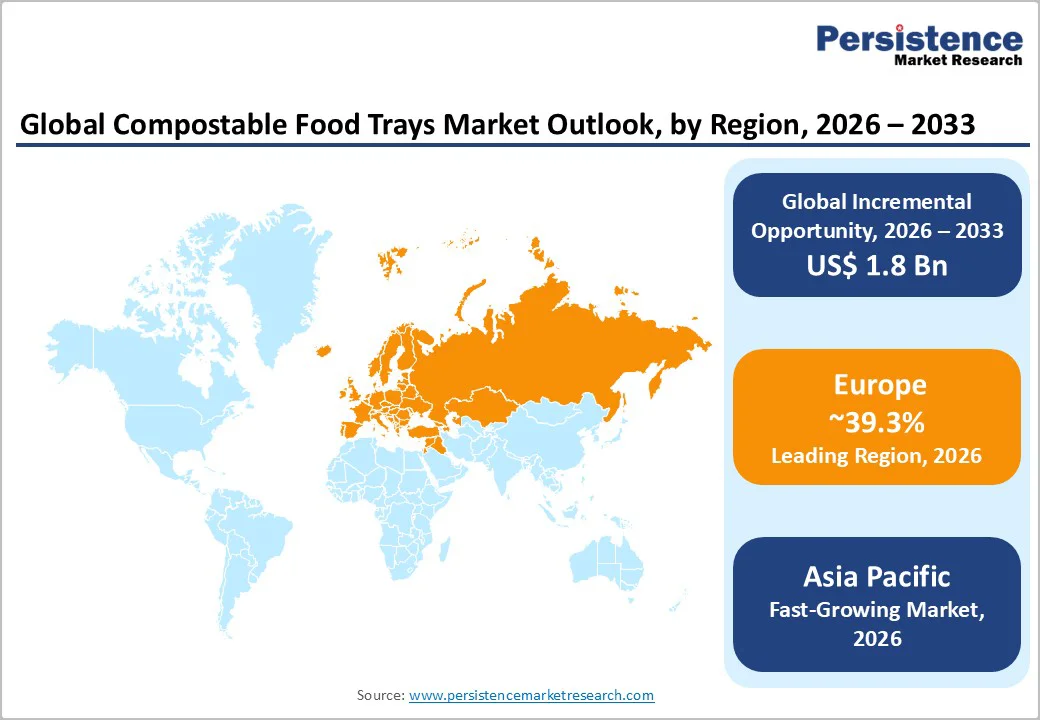

- Leading Region: Europe, to contribute an estimated 39.3% of the global market revenue in 2026, supported by strict packaging waste regulations, EU-wide sustainability mandates, and rapid commercial adoption across foodservice operators.

- Fastest-growing Region: Asia Pacific is projected to expand, driven by accelerated foodservice growth in China and India, rising plastic-reduction policies, and large-scale OEM production capacity.

- Investment Plans: Capital spending is increasing in fiber-molding lines and in R&D for biodegradable materials, with manufacturing expansions concentrated in China, India, and Western Europe. Industry estimates indicate that more than 30% of new capacity additions planned between 2025 and 2028 will focus on bagasse-based and bamboo-based tray production.

- Dominant Material: Bagasse, representing 42.3% of total material-based revenue in 2026, due to strong availability, favorable compostability characteristics, and growing adoption across quick-service restaurants and institutional food programs.

- Leading Compartment Type: Single-compartment trays, projected to account for 48.5% of revenue in 2026, remain the preferred format for restaurants, cafés, and fresh-produce distributors due to their cost efficiency and suitability for high-volume distribution.

| Key Insights | Details |

|---|---|

| Compostable Food Trays Market Size (2026E) | US$2.0 Bn |

| Market Value Forecast (2033F) | US$3.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 9.0% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Regulatory Pressure on Single-use Plastics Reshaping Packaging Demand

Regulations such as the Single-use Plastics Directive in Europe and updated packaging waste targets are creating clear timelines and procurement incentives for non-plastic solutions. These measures directly increase demand for compostable fiber trays and biodegradable coated alternatives as buyers adjust to procurement requirements that favor certified compostable materials.

Extended producer responsibility programs and municipal rules further reinforce the shift, especially in takeaway and institutional foodservice. Large foodservice operators increasingly issue tenders that specify compostable or bio-based materials.

The impact on the market is significant, as regulatory clarity accelerates conversion across chain restaurants, institutional catering, and retail prepared foods, meaningfully expanding the addressable market in regulated regions.

Feedstock Economics and Vertical Integration around Bagasse and Agricultural Fibers

Bagasse and agricultural residues have become reliable, economical feedstocks in sugarcane and cereal-producing regions. Studies of molded fiber packaging consistently show bagasse representing approximately 40 to 44% of the material mix, reflecting strong availability and lower cost relative to engineered biopolymers.

Producers increasingly pursue vertical integration by co-locating pulping and molding operations near sugar mills. This reduces logistics costs and stabilizes margins by creating a direct raw material pipeline. The market impact is considerable since a secure feedstock supply supports pricing stability, enables large-scale manufacturing, and attracts capital investment.

Asia Pacific and Latin America, in particular, continue to benefit from proximity to feedstock and expanding molded fiber capacity.

Growth of PLA and Engineered Biopolymers as Complementary Compostable Materials

Polylactic acid and engineered biopolymers are expanding rapidly as capacity additions bring costs closer to parity with conventional materials. Forecasts indicate sustained double-digit growth for PLA, driven by new plants, improved polymer performance, and rising adoption by brands seeking both barrier performance and compostability.

Manufacturers increasingly blend fiber with PLA coatings or liners to achieve moisture resistance, heat performance, and, in some cases, clarity. This broadens the range of compostable tray applications, including chilled prepared meals, fresh produce, and premium retail packaging. As PLA supply expands, more cost-competitive laminated or hybrid tray formats become viable, enabling manufacturers to target higher-value segments.

Limited Composting Infrastructure and Inconsistent Acceptance Rules

Industrial composting capacity is uneven across global markets, and municipal acceptance of compostable packaging remains inconsistent. Many municipalities accept food waste but do not yet process compostable packaging at scale. Data indicate that only a small portion of total food waste is handled by industrial composters, constraining real-world end-of-life pathways.

In numerous regions, fewer than 10-15% of communities offer curbside or industrial programs that consistently accept compostable fiber or coated packaging, creating contamination risk and complicating disposal messaging for both brands and consumers.

Price Premiums and Performance Tradeoffs versus Conventional Plastics

Compostable trays often carry a higher price tag than petroleum-based plastics or EPS, especially for buyers with limited purchasing scale. Performance factors such as heat resistance, wet strength, and barrier durability may create operational concerns in foodservice settings.

These realities raise switching costs for smaller restaurants and budget-sensitive quick service chains. Volatility in feedstock and energy prices can compress margins and delay procurement decisions. Buyers often require certification, verified performance data, and compatibility testing with high-volume filling lines, which slows adoption and lengthens the qualification cycle.

Meal-Kit and Multi-Compartment Trays Aligned With Food-Delivery Growth

Rapid expansion of meal-kit services and third-party delivery platforms is driving demand for durable, compartmentalized trays that maintain meal integrity. Multi-compartment compostable trays align with trends in portion control and premium convenience foods. As meal-kit penetration rises globally, higher-value packaging formats emerge as an attractive opportunity for compostable tray manufacturers.

If meal-kit and delivery markets continue to grow at mid- to high-single-digit rates through 2030, multi-compartment compostable trays could unlock several hundred million dollars in additional addressable market value. This opportunity is supported by rising consumer expectations for sustainable packaging in direct-to-consumer channels.

Regional Capacity Expansion for Bagasse and PLA in Asia

Asia Pacific offers significant upside due to abundant sugarcane residues and ongoing investments in both molded fiber and PLA production. New industrial projects converting sugarcane into molded pulp, along with integrated sugar-to-PLA initiatives, are reshaping the regional cost structure.

These developments reduce reliance on imported biopolymers and can lower unit costs by mid-single-digit levels. The combination of feedstock proximity, large domestic foodservice demand, and expanding compostable supply chains positions the Asia Pacific as a growth engine. Public-private initiatives, green financing, and government support for green manufacturing further enhance the regional opportunity.

Category-wise Analysis

Material Insights

Bagasse is expected to account for approximately 42.3% of the market share in 2026. This leadership position reflects its status as a co-product of sugar milling, its consistent supply availability, and the well-established processes for converting bagasse into molded fiber. Bagasse-based trays are widely used in quick service restaurants, cafes, institutional catering, and takeaway meal applications.

Cost advantages arise from the co-location of bagasse pulping operations near sugar mills, which lowers the cost of raw material handling.

Bamboo is the fastest-growing material segment in the compostable food trays market. Its rapid expansion is supported by strong supply availability across the Asia Pacific, rising adoption in premium foodservice packaging, and its favorable strength-to-weight ratio compared with other natural fibers.

Bamboo trays offer higher durability, improved heat resistance, and a smoother surface finish, making them suitable for hot meals, ready-to-eat foods, and retail-grade produce packaging. Regulatory encouragement for rapidly renewable materials and increasing investments in bamboo pulp processing plants further support its accelerated growth trajectory.

Compartment Insights

Single-compartment trays are expected to account for 48.5% of total revenue in 2026, making them the dominant category. They fit the majority of use cases for takeout meals, sandwiches, fast-casual dining, and ready-to-eat offerings. Their relatively simple design results in lower unit costs and broad compatibility with existing filling and sealing lines.

High-volume consumption across quick service restaurants and takeaway operators reinforces this segment’s leadership. The simplicity of single-compartment formats enables rapid conversion from plastic to fiber-based alternatives and supports the high-turnover nature of foodservice operations. These factors ensure sustained demand and strong volume density in this segment.

Multi-compartment trays are expanding at the fastest rate due to the rising adoption in meal-kit delivery services, healthcare catering, school feeding programs, and corporate cafeterias. These sectors require portion control and separation of wet and dry components. Growth trends in meal-kit subscriptions and the increasing importance of convenience foods provide strong momentum for compartmentalized trays.

Multi-compartment products command higher price points and allow for value-added features such as enhanced barrier coatings, moisture resistance, and structural reinforcement. As off-premise consumption continues to grow, demand for premium compostable partitioned trays strengthens, making this the fastest-expanding compartment category.

Regional Insights

North America Compostable Food Trays Market Trends - Fragmented Composting Access and Foodservice-Led Adoption

North America is supported by a mature foodservice ecosystem and widespread consumption of takeout and prepared meals. The U.S. dominates regional demand, with major national chains integrating compostable trays into their packaging portfolios to meet sustainability goals and regulatory pressures.

Single-compartment bagasse trays account for the majority of market value, serving as direct, cost-effective substitutes for traditional plastic trays in quick-service and casual-dining segments.

Despite growing adoption, composting infrastructure in the U.S. remains fragmented. Only a minority of municipalities accept compostable packaging, while many can process food waste but not fiber-based packaging due to technological limitations or contamination concerns. Canada’s leading metropolitan regions exhibit stronger acceptance, supported by advanced organic waste programs and clearer guidelines for compostable materials.

Sustainability-driven packaging rollouts by large foodservice brands, expansion of industrial composting pilots, and rising consumer preference for environmentally responsible dining continue to fuel market momentum. State-level bans on single-use plastics and emerging extended producer responsibility (EPR) schemes further accelerate the shift toward compostable solutions, even though the patchwork of regulations complicates national implementation.

Suppliers with robust certification credentials, transparent end-of-life communication, and local infrastructure partnerships are best positioned to capture growth. Industry investments are expanding molded fiber production capacity near raw material sources and strengthening the supply chain.

A major milestone was Novolex’s acquisition of Pactiv Evergreen, enhancing production scale, distribution reach, and leadership in sustainable packaging solutions across the North American market.

Europe Compostable Food Trays Market Trends - Regulation-Driven Uptake and Advanced Composting Infrastructure

Europe is expected to lead, accounting for an estimated 39.3% of the market in 2026, driven by early regulation, strong consumer preference for sustainable packaging, and well-developed foodservice and retail channels.

The Single-Use Plastics Directive and subsequent packaging waste legislation generate clear demand for compostable alternatives across takeaway, catering, and ready-meal applications. Germany, the U.K., France, and Spain exhibit different adoption patterns. Germany and France benefit from more extensive industrial composting infrastructure that supports organic waste processing.

The U.K. shows strong private sector uptake, particularly in catering and events as food-service businesses, cafés, restaurants and event organizers increasingly switching to compostable/eco-friendly packaging. At the same time, Spain demonstrates rapid conversion within hospitality and tourism-driven markets. National procurement standards and extended producer responsibility schemes influence purchasing behavior across all major European markets.

Key growth drivers include policy stability, strong demand in tourism and hospitality, and retail commitments to reduce single-use plastics. High meal-on-the-go consumption in urban centers reinforces the adoption of compostable trays.

Retailers and food brands increasingly promote compostable solutions in prepared meals and grab-and-go categories, which accelerates volume growth in both fiber and hybrid materials. These developments strengthen buyer confidence and encourage long-term commitments to compostable packaging.

Product campaigns and end-of-life collaboration programs remain central to buyer engagement strategies. Investment activity focuses on high-performance coatings and composite solutions that improve tray durability and moisture resistance, as well as logistics models that support organics collection.

Asia Pacific Compostable Food Trays Market Trends - Feedstock-Driven Expansion and Integrated Biopolymer Growth

Asia Pacific is the fastest-growing market for compostable food trays, driven by abundant agricultural residues, rapid population growth, and expanding foodservice industries. The region benefits from readily available feedstocks such as bagasse and wheat straw, enabling cost-efficient molded fiber production.

China leads in both scale and technology, with major investments in molded fiber packaging and biopolymer capacity expansion. Companies such as YFY Jupiter operate high-output lines supplying global markets, while groups such as COFCO and manufacturers such as Hubei Greenland invest heavily in PLA and PBAT production to build a self-reliant biopolymer ecosystem.

India is emerging as a key growth hub with accelerating bagasse-based tableware manufacturing and evolving industrial models linking sugar mills to PLA production. These initiatives promise cost-friendly compostable polymers and improved domestic availability. Rising urbanization, strong food delivery growth, and increasing environmental awareness are key market drivers.

Across India, China, and Southeast Asia, capacity investments enhance efficiency, quality, and export readiness. Government incentives for green manufacturing bolster competitiveness, allowing regional suppliers to scale exports and meet growing demand in both domestic and international foodservice markets, particularly North America and Europe.

Competitive Landscape

The global compostable food trays market is moderately fragmented, with specialized brands and regional molded-fiber producers holding key positions alongside expanding multinational packaging groups. Distribution scale remains vital for large foodservice contracts, while local producers in Asia and Latin America benefit from feedstock proximity.

Consolidation opportunities are increasing as firms pursue cost efficiency, broader reach, and integrated operations. Key strategies include vertical integration into feedstocks, enhanced certifications, product innovation, distributor acquisitions, and partnerships with composting operators to strengthen sustainability credibility and waste management effectiveness.

Key Industry Developments

- In May 2025, Metpack announced a collaboration with BASF to launch a home-compostable coated paperboard (branded “Ezycompost” with BASF’s “ecovio 70 PS14H6” coating) designed for food packaging, including trays, and offering performance (liquid/fat/grease barrier, heat resistance up to 100 °C) comparable to conventional materials while maintaining certified compostability under home-compost standards.

- In June 2025, researchers from the University of Queensland developed an innovative biodegradable biocomposite for food packaging, including trays and punnets, capable of decomposing naturally in soil, freshwater, and marine environments. This advancement has the potential to drive next-generation compostable tray solutions beyond conventional bagasse and molded fiber materials.

Companies Covered in Compostable Food Trays Market

- Huhtamaki

- Genpak LLC

- Novolex

- Sabert Corporation

- Vegware

- Biopak

- Pactiv Evergreen

- Dart Container Corporation

- GreenGood

- Eco-Products Inc.

- Bio Futura

- Lollicup (Karatzis Group)

- Good Start Packaging

- Packnwood

- Geotegrity Eco Packaging

- Be Green Packaging

- Biodegradable Food Service LLC

- Natural Tableware

- Earthens

- Shandong Tianming Paper Company

Frequently Asked Questions

The compostable food trays market size is estimated to reach US$2.0 billion in 2026.

By 2033, the compostable food trays market value is projected to reach US$3.8 billion.

Key trends include the rising shift toward bagasse-based trays, expanding adoption across restaurants and institutional foodservice, rapid regulatory enforcement on single-use plastics, and the growth of home-compostable and fiber-coated technologies.

The leading material segment is bagasse, accounting for 42.3% of total revenue.

The compostable food trays market is projected to grow at a CAGR of 9.7% between 2026 and 2033.

Major players include Huhtamaki, Genpak LLC, Novolex, Sabert Corporation, and Vegware.