- Retail

- Cocktail Mixers Market

Cocktail Mixers Market Size, Share, and Growth Forecast 2026 - 2033

Cocktail Mixers Market by Product Type (Tonic Water, Clun Soda, Syrups & Cordials, Ginger Ale, Mixers, Other), Nature (Conventional, Organic), End Use (HoReCa, Household Retail), and Regional Analysis for 2026 - 2033

Cocktail Mixers Market Size and Trend Analysis

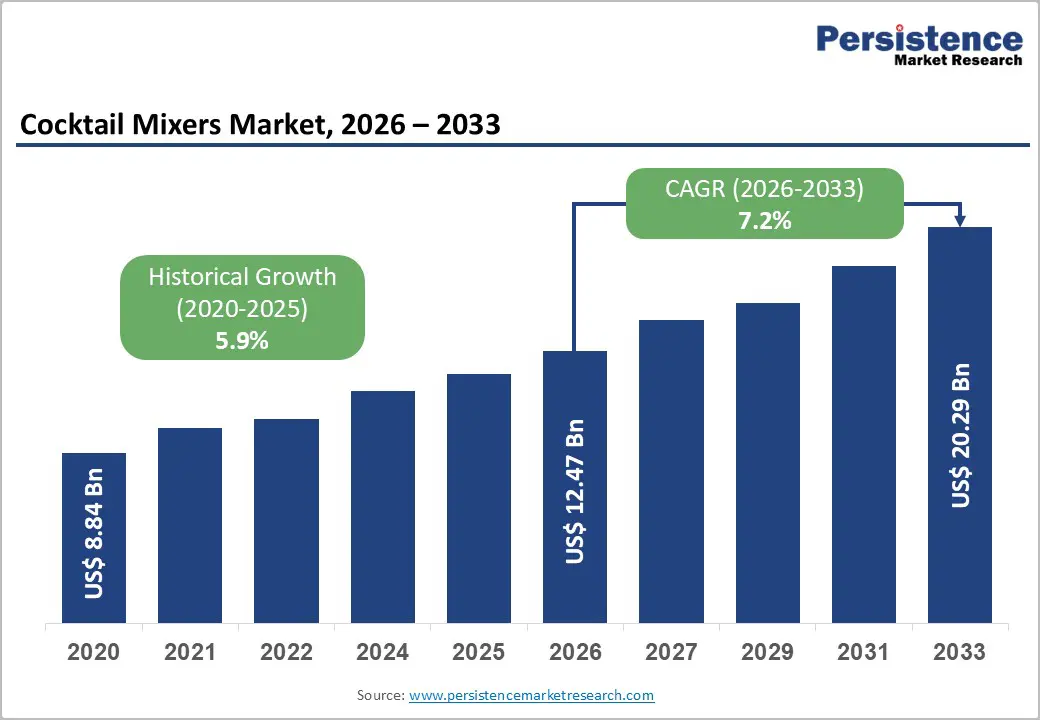

The global cocktail mixers market size is likely to be valued at US$ 12.5 Bn in 2026 and is projected to reach US$ 20.3 Bn by 2033, growing at a CAGR of 7.2% between 2026 and 2033.

The market is experiencing robust expansion driven by the premiumization trend and the rise of home mixology culture, with consumers increasingly seeking artisanal and craft mixers that complement high-end spirits. The craft cocktail movement has gained significant momentum, with 58% of consumers prioritizing premium mixers to elevate their at-home drinking experience, reflecting a shift toward experiential consumption and sophisticated flavor profiles.

Key Market Highlights

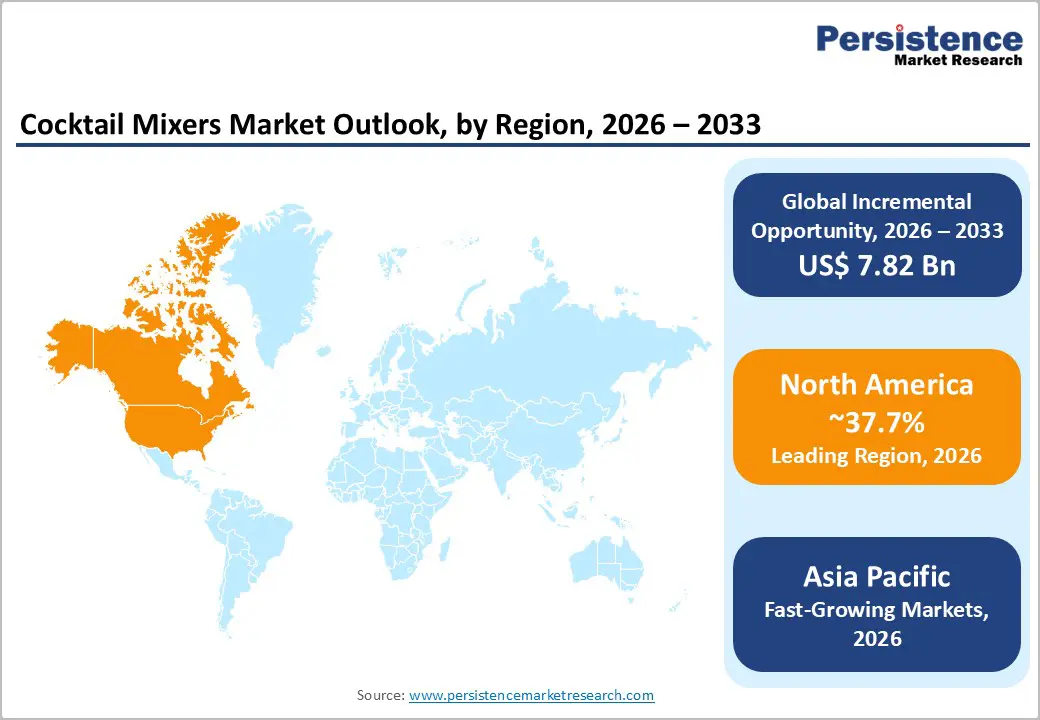

- Regional Leader: North America dominates the global cocktail mixers market with 37.7% market share, characterized by entrenched cocktail culture, premium consumer segments, and sophisticated retail infrastructure.

- FastestGrowing Region: Asia Pacific exhibits the highest growth trajectory, driven by urbanization, rising disposable incomes, and accelerating adoption of Western-style cocktail culture among younger demographics.

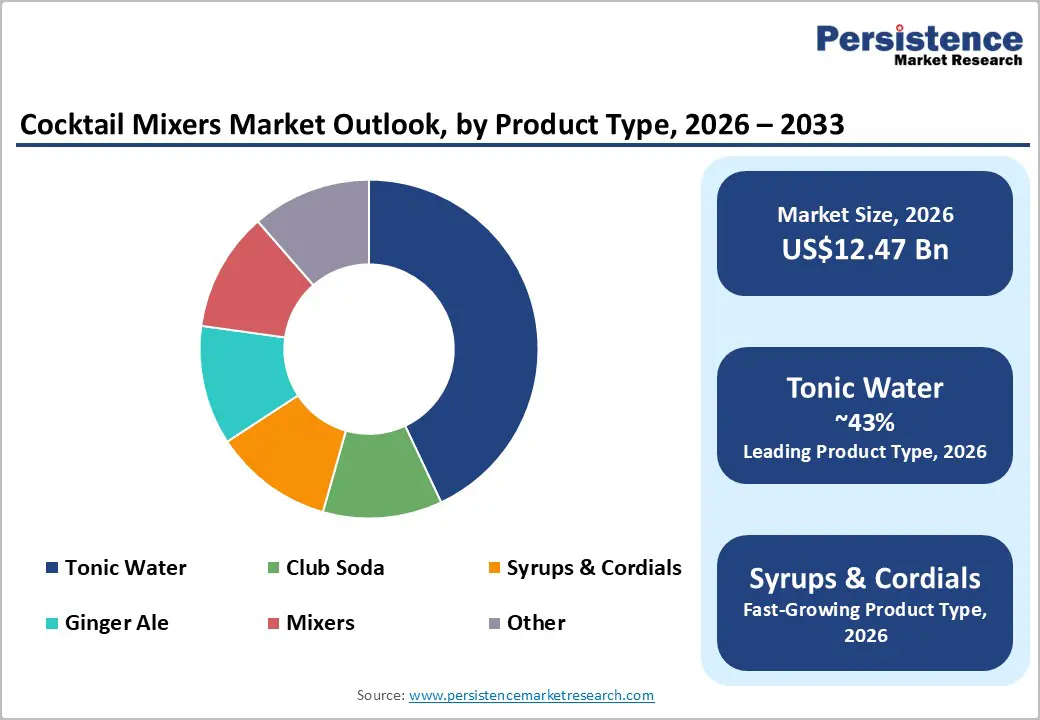

- Leading Segment: Tonic Water maintains market dominance with 43% market share, benefiting from traditional consumer familiarity, established distribution networks, compatibility with premium spirits, and the resurgence of the Gin and Tonic cocktail globally.

- Fastest-Growing Segment: Organic mixers emerge as the fastest-growing segment, driven by health-conscious consumer demand for natural ingredients, clean-label formulations, and sustainability-focused production methodologies aligned with broader wellness trends.

- Key Market Opportunity: A major opportunity lies in aligning mixers with low/no-alcohol cocktails and RTD ecosystems, combining natural flavors, sugar reduction, and functional benefits to address wellness, convenience, and premium experience trends.

| Key Insights | Details |

|---|---|

|

Cocktail Mixers Market Size (2026E) |

US$ 12.5 Bn |

|

Market Value Forecast (2033F) |

US$ 20.3 Bn |

|

Projected Growth CAGR (2026-2033) |

7.2% |

|

Historical Market Growth (2020-2025) |

5.9% |

Market Dynamics

Drivers - Rising Home Mixology Trend

The COVID-19 pandemic significantly altered consumer behavior, accelerating the shift toward home entertainment and do-it-yourself cocktail preparation. This trend has persisted beyond lockdowns and is expected to reshape market dynamics, with home mixology projected to account for nearly 50% of industry revenue by 2031. In 2020, the U.S. recorded a 36% increase in cocktail mixer sales, underscoring the growing preference for recreating bar-quality experiences at home.

Digital platforms have amplified this movement, as bartending tutorials and cocktail recipes attract substantial engagement, with 58% of global consumers experimenting with cocktail-making in 2022. Customized mixer kits and personalized cocktail solutions have emerged as distinct categories, supported by brands such as Shaker & Spoon. The democratization of mixology knowledge through social media and the availability of ready-to-use kits have lowered entry barriers, driving sustained demand across retail channels.

Premiumization and Flavor Innovation

Premium spirits and the craft cocktail movement are driving a significant shift toward high-value mixers that deliver complex flavor profiles and replicate bar-quality experiences at home. The broader non-alcoholic beverages market, projected to surpass US$ 1,900 billion by 2032 at a CAGR of approximately 7%, underscores consumers’ growing willingness to invest in quality, flavor innovation, and health-oriented options. This trend extends to mixers, driven by rising demand for botanical tonics, low-sugar sodas, and artisanal syrups that enhance both alcoholic and zero-proof cocktails.

Furthermore, bartenders and mixologists increasingly prioritize fresh, natural ingredients and inventive recipes, creating a ripple effect across the supply chain. Leading manufacturers such as Fever-Tree and Q Mixers are expanding portfolios with botanical-infused premium offerings. This evolution has reshaped consumer expectations, prompting establishments to focus on distinctive flavors and superior ingredients to foster brand loyalty.

Restraint - Stringent Regulatory Frameworks

The rising consumer focus on health and wellness has fundamentally challenged conventional mixer formulations containing artificial sweeteners and high sugar content. The World Health Organization released updated guidelines in 2023, recommending reduced sugar consumption and cautioning against long-term use of artificial sweeteners, intensifying regulatory and consumer pressure on traditional mixer manufacturers.

This health-conscious trend has compelled brands to reformulate products and invest in low-sugar, zero-calorie alternatives, which require substantial research and development while potentially compromising the taste profiles consumers expect from premium mixers. Regulatory hurdles on labeling, alcohol content, and health claims impede innovation and market expansion. These restrictions limit product variety, particularly for imported goods, slowing market penetration in regions with rigorous food safety standards.

High Cost Premium and Market Accessibility Challenges

Premium spirits and the craft cocktail movement are driving a structural shift toward high-value mixers that replicate complex flavor profiles and deliver bar-quality experiences at home. The non-alcoholic beverages market, projected to exceed US$ 1,900 billion by 2032 at a CAGR of approximately 8.2%, reflects consumers’ growing willingness to invest in quality, flavor innovation, and health-oriented options. This trend extends to mixers, driven by rising demand for botanical tonics, low-sugar sodas, and artisanal syrups that enhance both alcoholic and zero-proof cocktails.

Bartenders and mixologists increasingly emphasize fresh, natural ingredients and inventive recipes, creating a ripple effect across the supply chain. Leading brands such as Fever-Tree and Q Mixers are expanding portfolios with botanical-infused premium offerings, reshaping consumer expectations and prompting establishments to prioritize distinctive flavors and superior ingredients to foster brand loyalty.

Opportunity - Health-Conscious and Organic Variants

The rising demand for functional beverages offering health benefits beyond hydration presents significant growth opportunities for innovative mixer manufacturers. Consumers increasingly favor mixers enriched with vitamins, botanical extracts, and probiotic components. The global functional beverage market is expanding rapidly, driven by health-conscious buyers seeking ingredients that deliver tangible wellness advantages. Brands focusing on low-calorie formulations, such as Skinny Mixes, which reported a 30% year-over-year sales increase, illustrate the commercial viability of health-oriented positioning.

According to the International Food Information Council, 43% of consumers actively seek “low sugar” or “no sugar” labels, highlighting a substantial market for reduced-sugar mixers without compromising taste. The convergence of mixology and wellness trends enables brands to introduce products featuring adaptogenic botanicals, enhanced electrolytes, and natural energy boosters, positioning cocktails as lifestyle-aligned rather than purely indulgent.

Capitalizing on low/no-alcohol and RTD cocktail ecosystems

The global surge in demand for high-strength RTD malt beverages and ready-to-drink cocktails reflects consumers’ preference for convenient, bar-quality experiences without complex preparation. Mixer brands can capitalize on this trend by offering bases, co-branded components, and companion products tailored for RTD and low-alcohol formats. Simultaneously, the proliferation of non-alcoholic cocktail ranges in supermarkets and hospitality venues positions mixers as essential elements in zero-proof beverages.

Hospitality operators across North America, Europe, and the Asia Pacific are increasingly incorporating premium non-alcoholic options to attract health-conscious and younger demographics. The RTD cocktail segment is projected to grow by over 20% by 2026, with non-alcoholic variants gaining significant traction. Emerging players such as Bartisans in India and Thomas Henry in Germany are redefining mixers as sophisticated alternatives, while HoReCa investments in premium mocktail programs continue to drive demand for complex, high-quality non-alcoholic mixers.

Category-wise Analysis

Product Type Insights

Tonic water remains the leading product segment in the global cocktail mixers market, accounting for approximately 43% of the total share. Its dominance is driven by traditional appeal and versatility across multiple spirits, particularly the iconic Gin and Tonic, which has seen a strong global resurgence. The segment benefits from consumer familiarity, extensive retail distribution, and the premiumization trend within the gin category. Premium variants featuring natural quinine, botanicals, and organic sweeteners have gained traction, commanding price premiums and boosting profitability.

The rise of craft gin distilleries, especially in Europe and North America, has further fueled demand for high-quality tonics. Leading brands such as Fever-Tree, Q Mixers, and Britvic exemplify this premiumization trend. Compatibility with diverse spirits, at-home mixology growth, and increased availability through retail and e-commerce continue to reinforce tonic water’s market leadership, while other mixers, such as club soda and ginger ale, show steady growth.

Nature Insights

Conventional mixers currently dominate the market, accounting for approximately 83% of the total share due to their long-standing presence, affordability, and extensive distribution across supermarkets, convenience stores, and HoReCa channels. These products benefit from economies of scale in sourcing, manufacturing, and packaging, enabling competitive pricing in both mature and emerging markets.

In contrast, organic mixers, though a smaller niche, are expanding rapidly as health-conscious and environmentally aware consumers seek certified ingredients, reduced synthetic additives, and sustainable production practices. Brands offering verifiable organic and clean-label credentials are well-positioned to capture premium demand. Organic variants featuring natural botanicals, responsibly sourced ingredients, and minimal processing appeal to affluent and eco-conscious demographics, reflecting broader industry trends toward transparency and clean-label products.

End-user Insights

The HoReCa segment (hotels, restaurants, and cafes) is projected to account for approximately 58% of global cocktail mixer consumption, underscoring its critical role in professional cocktail programs and beverage menus. Bars and restaurants rely on consistent, high-quality mixers such as tonic water, soda, ginger ale, and syrups to ensure flavor standardization, speed of service, and premium presentation, particularly as mixology becomes a key differentiator in urban dining and nightlife.

While household retail is growing strongly thanks to home-entertaining and at-home cocktail experimentation, the HoReCa channel remains the principal volume and trend-setter, where new mixer formats and flavor concepts are often trialed before diffusing into retail shelves and e-commerce. Major retailers, including Whole Foods, Walmart, and Target, have substantially expanded cocktail mixer offerings to capture growing demand from home bartenders seeking premium formulations and diverse flavor profiles.

Regional Insights

North America Cocktail Mixers Market Trends

North America accounts for approximately 37.7% of the global cocktail mixers market, positioning the region as a leading hub for premium spirits, craft cocktails, and beverage innovation. Strong demand for high-quality mixers spans both on-trade and off-trade channels, supported by a well-developed bar and restaurant ecosystem featuring mixology-focused venues and speakeasy-style bars. Regulatory bodies such as the U.S. FDA and Health Canada emphasize labeling transparency, ingredient safety, and sugar reduction, prompting brands to adopt cleaner labels and lower-calorie formulations.

Innovation is further driven by advanced flavor houses and beverage technology firms supplying cutting-edge flavoring and carbonation solutions. Rising interest in low- and no-alcohol cocktails, functional beverages, and RTD drinks provides additional growth momentum, while e-commerce, subscription models, and direct-to-consumer strategies expand market reach for niche and craft mixer brands targeting discerning U.S. and Canadian consumers.

Europe Cocktail Mixers Market Trends

Europe represents a key market for cocktail mixers, accounting for 30% of the global share, supported by its strong heritage in spirits such as gin, vodka, and vermouth, and a dense network of cocktail bars across the U.K., Germany, France, Spain, and other countries. Stringent EU food and beverage regulations, including harmonized labeling and additive standards, drive producers toward greater transparency, quality, and safety, reinforcing consumer trust and favoring premium, natural-ingredient formulations.

Growth in low- and no-alcohol beverages is particularly strong in Western Europe, where stricter drink-driving laws and health-conscious lifestyles encourage alcohol-free cocktails built around sophisticated mixers. Germany has emerged as an innovation hub, with Thomas Henry GmbH pioneering advanced non-alcoholic and low-alcohol formulations, positioning zero-proof drinking as a lifestyle choice. Regulatory harmonization has facilitated consolidation, exemplified by Britvic’s acquisition of London Essence, while rising demand for organic and natural mixers is supported by 67% of European consumers actively avoiding artificial ingredients.

Asia Pacific Cocktail Mixers Market Trends

Asia Pacific is rapidly emerging as one of the fastest-growing regions in the cocktail mixers market, driven by rising disposable incomes, urbanization, and the expansion of modern retail and on-trade venues across China, India, Japan, and ASEAN countries. The proliferation of international hotel chains, cocktail bars, and Western-style restaurants in major cities is introducing more consumers to mixed drinks, fueling demand for tonic water, club soda, ginger ale, and flavored syrups suited to both global and local spirits.

Regional manufacturing advantages, such as cost-efficient production, access to citrus and botanical ingredients, and improved logistics, enable competitive supply at scale. Growth in flavored and RTD alcoholic beverages, including malt-based premixes in markets like China and Australia, creates collaboration opportunities for mixer brands with brewers and distillers. As health awareness and premiumization trends accelerate, demand is shifting from commoditized soft drinks to higher-value, flavor-forward mixers.

Competitive Landscape

The global cocktail mixers market is moderately fragmented, featuring competition between established multinational beverage corporations and emerging artisanal brands. While leading companies hold significant market share, they face ongoing challenges from premium and organic entrants. Differentiation strategies focus on ingredient authenticity, flavor innovation, sustainability, and brand heritage. Product innovation remains a key growth driver, with launches of low-calorie, functional mixers addressing evolving consumer preferences. Emerging business models prioritize direct-to-consumer channels, e-commerce, and subscription-based cocktail kits, reducing reliance on traditional retail and strengthening consumer engagement.

Key Market Developments

- January 2025: Molson Coors Beverage Company announced a transformational partnership with Fever-Tree, assuming exclusive commercialization rights for the brand's U.S. portfolio while acquiring an 8.5% equity stake, positioning Molson Coors as Fever-Tree's second-largest shareholder globally.

- November 2024: Thomas Henry GmbH announced aggressive North American expansion plans, establishing distribution infrastructure across California, Illinois, Colorado, and Nevada, with a strategic focus on major metropolitan markets, including Texas and New York, for 2025-2026.

- March 2024: Keurig Dr Pepper, Inc. extended its mixer and flavored soda offerings through new partnerships with leading spirit brands to strengthen visibility in on- and off-premise cocktail occasions.

Top Companies in Cocktail Mixers Market

Fever-Tree (London, U.K.) globally recognized premium mixer leader commanding substantial market share through natural ingredient positioning and sophisticated botanical formulations. The brand's commitment to quality, exemplified through natural quinine sourcing from the Democratic Republic of Congo, has established industry-leading brand equity. Fever-Tree's extensive product portfolio spanning tonic waters, ginger beers, and specialty mixers supports broad distribution across premium retail and HoReCa channels globally.

The Coca-Cola Company (Atlanta, U.S.) is a diversified beverage corporation leveraging global distribution infrastructure and substantial capital resources to compete across premium and mainstream mixer segments. Coca-Cola's portfolio encompasses multiple mixer brands and formulations, with significant HoReCa relationships supporting sustained demand across hospitality channels. The company's investment in innovation and emerging categories positions it as a formidable competitor within the evolving mixer landscape.

Keurig Dr Pepper, Inc. (Burlington, U.S.) is a major beverage conglomerate operating Canada Dry mixers and multiple portfolio brands serving diverse consumer segments. KDP's 2025 innovation pipeline featuring bold flavor launches across Dr Pepper, 7UP, Snapple, and complementary brands reflects a commitment to capturing premiumization opportunities. The company's U.S. refreshment beverages segment demonstrates strong momentum, with international expansion through Mexico and Canada representing emerging growth platforms.

Companies Covered in Cocktail Mixers Market

- Fever-Tree

- Keurig Dr Pepper, Inc.

- The Coca-Cola Company

- The London Essence Company

- Three Cents

- Fentimans

- Thomas Henry GmbH

- East Imperial

- Britvic

- Bartisans

- Master of Mixes

- White Rock Products Corporation

- Monin Inc.

Frequently Asked Questions

The global cocktail mixers market is projected to reach around US$ 20.3 Bn by 2033, growing from about US$ 12.5 Bn in 2026 at a forecast CAGR of roughly 7.2% between 2026 and 2033.

Key demand drivers include premiumization of beverages, expansion of craft cocktail culture, growth in low- and no-alcohol consumption, and rising at-home mixology supported by innovation in flavors, clean labels, and functional ingredients.

Tonic Water commands the leading position with approximately 43% market share, driven by its traditional appeal, versatility across multiple spirit categories, and the global resurgence of the Gin and Tonic cocktail.

North America commands approximately 37.7% global market share, benefiting from entrenched cocktail culture, substantial consumer disposable income, and sophisticated retail infrastructure supporting premium product penetration, particularly within the U.S. market.

A major opportunity is aligning mixers with low- and no-alcohol cocktails and RTD ecosystems, creating natural, lower-sugar, and functionally enriched mixers that cater to wellness, convenience, and premium drinking experiences across channels.