- Specialty & Fine Chemicals

- Chromic Acid Market

Chromic Acid Market Size, Share, and Growth Forecast, 2026- 2033

Chromic Acid Market by Grade (Excellent Grade, First Grade, and Qualified), By Application (Metal plating / Electroplating (metal finishing), Coating / Surface treatment, Detergent (specialty uses), Glass processing/polishing, Wood preservation, and Others), and Regional Analysis for 2026 – 2033

Chromic Acid Market Size and Trends Analysis

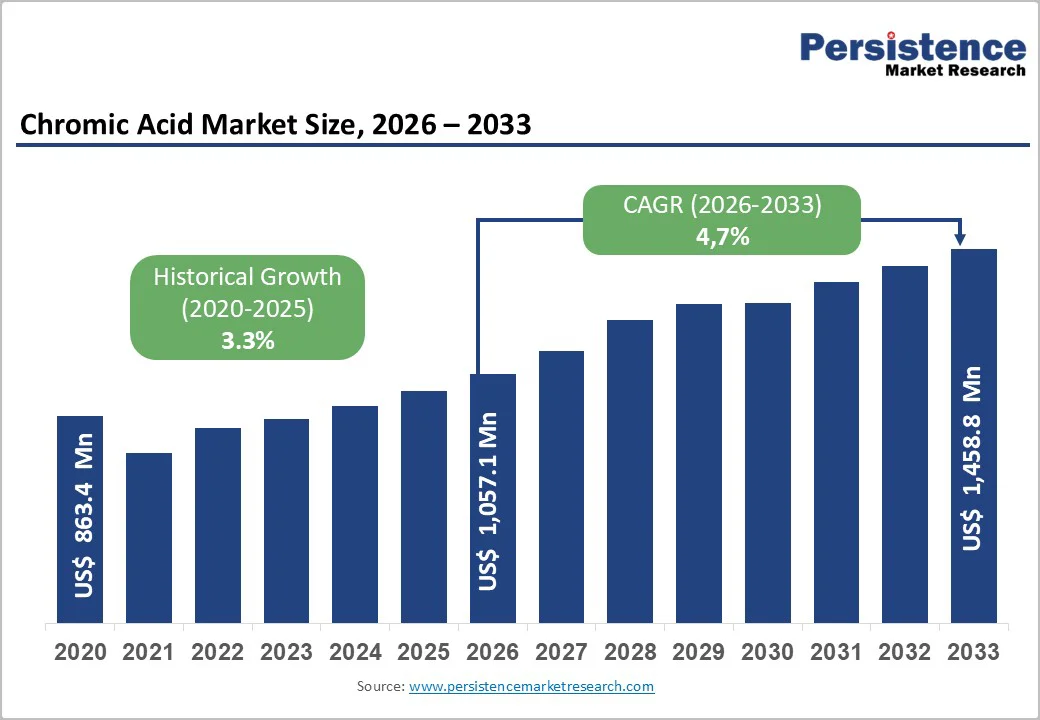

The global chromic acid market size was valued at US$ 863.4 Million in 2020 and is projected to reach US$ 1,057.1 Million by 2026, expanding further to US$ 1,458.8 Million by 2033, growing at a CAGR of 4.7% during the 2026-2033 forecast period.

The market's sustained growth trajectory is driven by escalating demand from industrial metal finishing operations, particularly in automotive and aerospace sectors, coupled with expanding applications in specialty chemical manufacturing. Rising adoption of advanced surface treatment technologies and stringent environmental compliance standards are reshaping production methodologies, while emerging markets in Asia Pacific present significant expansion opportunities for established and new market participants.

Key Industry Highlights:

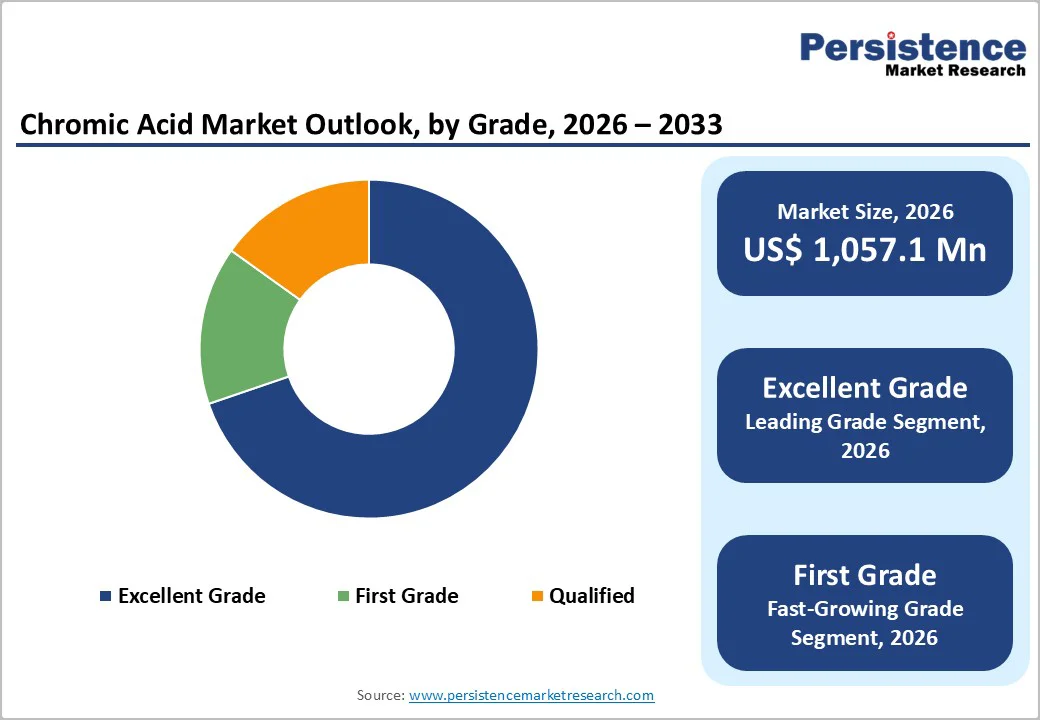

- Grade Analysis: Excellent-grade chromic acid dominates with 65%+ market share, while first-grade products demonstrate faster growth at 4.4% CAGR, reflecting emerging market industrialization and cost-sensitive manufacturing base expansion in the Asia Pacific.

- Application-Analysis: Metal plating/electroplating commands 60%+ revenue share as the dominant application, while coating and surface treatment applications are growing fastest at 4.6% CAGR, indicating market diversification into advanced material finishing and electronics manufacturing.

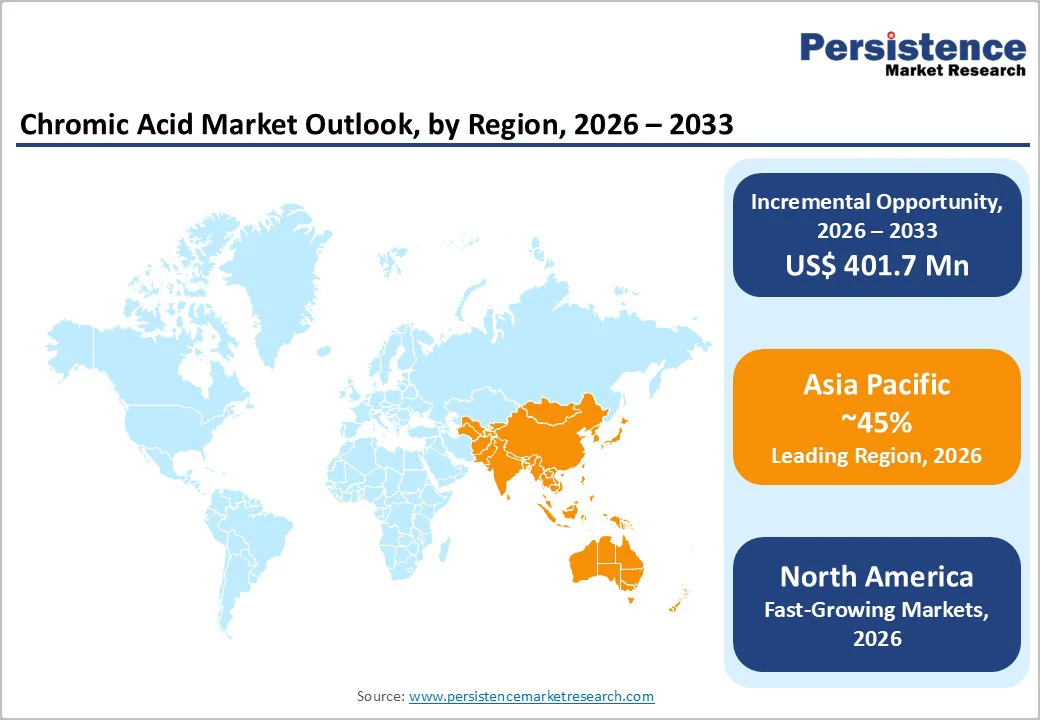

- Regional Analysis: Asia Pacific leads with 45%+ market share, with North America experiencing accelerated growth at 4.7% CAGR driven by premium product demand and aerospace/advanced manufacturing applications, while Europe maintains a regulatory leadership position in sustainability-aligned product development.

- Opportunity: Advanced electronics and semiconductor manufacturing represent a high-value growth opportunity, with chromic acid used in precision plating for semiconductor packaging, connectors, and PCBs.

- Moderate market concentration with top 5-6 multinational suppliers controlling 55-60% share; strategic focus on chromium recycling integration, emerging market geographic expansion, and specialized electronics formulations is reshaping competitive positioning and supporting differentiated growth strategies.

| Report Attribute | Details |

|---|---|

|

Chromic Acid Market Size (2026E) |

US$ 1,057.1 Mn |

|

Market Value Forecast (2033F) |

US$ 1,458.8 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

4.7% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.3% |

Market Dynamics

Robust Demand from Automotive and Aerospace Manufacturing

The automotive and aerospace industries remain the primary drivers of chromic acid consumption, with metal plating and electroplating applications accounting for over 60% of market revenue. Global automotive production reached approximately 80 million vehicles in 2023, and electroplating operations are critical for corrosion resistance and the aesthetic finishing of components. The aerospace sector's stringent quality standards necessitate high-grade chromic acid for precision metal finishing, where surface integrity directly impacts structural performance and regulatory compliance. According to International Organization of Standardization (ISO) standards and aerospace manufacturing protocols, chromium-based plating provides superior adhesion and protective coating characteristics. As vehicle electrification accelerates, new battery component manufacturing requires specialized metal finishing, creating incremental demand. The historical CAGR of 3.3% reflects this established demand base, while projected growth to 4.7% indicates accelerating adoption in high-performance applications and emerging vehicle technologies.

Market Restraining Factors

Health and Safety Concerns Associated with Hexavalent Chromium Exposure

Hexavalent chromium compounds, including chromic acid, present well-documented occupational health risks when workers face inhalation or dermal exposure. Regulatory bodies including OSHA (Occupational Safety and Health Administration) classify hexavalent chromium as a carcinogen, imposing stringent workplace exposure limits (currently 5 micrograms per cubic meter in the U.S.). These safety requirements necessitate significant capital investment in ventilation systems, personal protective equipment, and worker training programs, effectively raising operational costs for manufacturers utilizing chromic acid. Increasingly stringent regulations in developed economies are constraining growth in traditional markets, while some manufacturers are investing in alternative plating technologies to minimize hexavalent chromium dependency. This regulatory pressure reduces addressable market size in consumer-facing applications and creates barriers for smaller industrial operators unable to meet compliance costs, thereby limiting market democratization and growth potential in price-sensitive segments.

Chromic Acid Market Trends and Opportunities

Integration of Chromic Acid in Advanced Electronics and Semiconductor Manufacturing

The semiconductor and advanced electronics industries require ultra-high-purity metal finishing for component reliability and performance optimization. As global semiconductor capital expenditure exceeded US$ 150 billion in 2023, associated chemical supply demand is expanding correspondingly. Chromic acid's role in precision plating for semiconductor packaging, connector manufacturing, and printed circuit board applications represents an underexploited market segment with premium pricing power. Technology convergence between specialty chemicals and microelectronics manufacturing is creating opportunities for chromic acid suppliers to develop specialized formulations meeting semiconductor industry specifications. Market analysis suggests this segment could contribute 8-12% incremental revenue growth over the forecast period if existing technological barriers are overcome and supply chain integration is achieved with major semiconductor equipment and materials providers.

Chromic Acid Market Insights and Trends

Excellent-Grade Dominance and First-Grade Growth Reshape Global Chromic Acid Market Dynamics

Excellent-grade chromic acid remains the clear market leader, driven by its superior purity levels exceeding 99.5% and tightly controlled metal impurity specifications. Accounting for over 65% of global revenue, this segment is indispensable in aerospace, pharmaceutical, and precision electronics applications, where even minor contamination can compromise performance, safety, and regulatory compliance. Suppliers of excellent-grade material benefit from 20–30% price premiums over lower grades, translating into stronger margins supported by advanced manufacturing capabilities and rigorous quality assurance systems. Demand is highly stable, anchored by long-term procurement from established industrial customers in North America and Europe, regions characterized by strict manufacturing standards and well-defined regulatory frameworks that favor premium-grade adoption.

In contrast, the first-grade chromic acid segment is the fastest-growing, expanding at a CAGR of 4.4%. Its growth is fueled by a balanced value proposition that combines adequate quality with cost efficiency, making it suitable for general electroplating, surface treatment, and non-critical industrial processes. Rapid industrialization across Asia Pacific is a key catalyst, as manufacturers prioritize scalable and economical inputs during early-stage capacity expansion. As a result, first-grade products are steadily gaining market share. Intensifying competition from regional producers, leveraging cost advantages and localized supply chains, is further reshaping this segment’s competitive landscape.

Application Insights

Chromic Acid Applications Driven by Plating Dominance and Advanced Surface Engineering Growth

Metal plating and electroplating remain the dominant applications within the chromic acid market, accounting for over 60% of total revenue and firmly establishing this segment as the industry’s backbone. Chromic acid-based electroplating is widely used across automotive body panels, fasteners, aerospace structural parts, and heavy industrial machinery components due to its proven effectiveness in enhancing corrosion resistance, surface hardness, wear protection, and visual finish. The segment’s leadership reflects decades of technological maturity, well-standardized production practices, and deep integration into global manufacturing supply chains. Stable demand from continuous automotive and aerospace production cycles further reinforces its position. However, growth within this segment largely mirrors the overall market average of around 4.7%, indicating a mature demand environment with limited scope for rapid acceleration unless disruptive technologies or new application areas emerge.

In contrast, coating and surface treatment applications represent the fastest-growing segment, expanding at approximately 4.6% CAGR. This growth is driven by rising adoption of advanced oxide films, high-performance corrosion-resistant coatings, and precision surface treatments for electronics and engineered components. Technological advances in thin-film deposition, nanotechnology-enabled surface modification, and high-performance material requirements are expanding chromic acid use beyond traditional electroplating. Strong electronics manufacturing growth in Athe sia Pacific is further accelerating adoption, positioning this segment for gradual market share gains over the forecast period.

Regional Insights and Trends

Asia Pacific Leads Chromic Acid Market Through Manufacturing Scale, Policy Support, and Cost Efficiency

Asia Pacific firmly dominates the global chromic acid market, accounting for over 45% of total revenue, underpinned by the region’s vast manufacturing ecosystem. China alone represents nearly 35–40% of regional consumption, supported by its automotive production base of around 28 million vehicles annually, where chromic acid is integral to electroplating across component value chains. India, Japan, and Southeast Asia—particularly Vietnam and Thailand—are emerging as incremental growth engines due to expanding automotive and electronics manufacturing. The regional market surpassed US$ 450 million in 2026 and is projected to exceed US$ 650 million by 2033, reflecting sustained industrial momentum.

Growth is driven by competitive manufacturing costs, strong foreign direct investment inflows, and government-led industrialization initiatives such as “Made in China 2025,” “Make in India,” and ASEAN manufacturing hub programs. Rising domestic consumption has further encouraged localized investments in electroplating infrastructure. Post-COVID supply chain realignment has accelerated regional capacity expansion as global manufacturers seek geographic diversification, boosting demand for cost-effective, first-grade chromic acid aligned with application-specific requirements.

Regulatory conditions remain uneven across the region. China has implemented stricter environmental enforcement, while India and Southeast Asia are gradually tightening standards. This regulatory diversity creates segmentation opportunities, with local producers leveraging cost and logistics advantages, while multinational suppliers compete in premium-grade segments through superior quality assurance and technical expertise.

North America’s Premium Chromic Acid Market Driven by Regulation, Innovation, and Manufacturing Leadership

North America accounts for approximately 20–22% of the global chromic acid market and continues to demonstrate stable yet accelerated growth, expanding at a CAGR of around 4.7%, in line with global averages. The regional market, valued at nearly US$ 200 million in 2026, is projected to surpass US$ 270 million by 2033, reflecting steady value growth despite its mature structure. The United States remains the core demand center, supported by established automotive manufacturing hubs in Michigan and Ohio and strong aerospace supply chains concentrated in California and Connecticut. High regulatory and quality requirements have resulted in excellent-grade chromic acid dominating more than 75% of regional demand, underscoring North America’s preference for premium specifications.

The region’s advanced manufacturing ecosystem and aerospace-led innovation are fostering demand for ultra-high-purity chromic acid and integrated chromium recycling solutions. Investments in sustainable manufacturing, circular economy compliance, and waste minimization are enabling suppliers to differentiate through technology and command pricing power. Stringent OSHA and EPA regulations are further accelerating innovation in worker safety and environmental performance, raising entry barriers for smaller players.

Competitive dynamics remain concentrated, with leading multinational specialty chemical manufacturers controlling roughly 60–65% of supply. Market competition emphasizes service quality, regulatory compliance support, and long-term supply reliability rather than price-based differentiation.

Chromic Acid Market Competitive Landscape

The global chromic acid market demonstrates a moderate-to-high level of concentration, with leading multinational specialty chemical manufacturers collectively accounting for approximately 55–60% of total market revenue. These dominant players are typically large chemical conglomerates with diversified product portfolios, strong financial positions, and well-established global distribution networks. Their leadership is reinforced by vertically integrated supply chains, advanced technical service capabilities, and long-standing relationships with end-use industries, enabling consistent participation across multiple grades and application segments.

Mid-tier regional producers and specialized suppliers represent an estimated 25–30% of the global market. These companies compete effectively through regional focus, tailored product specifications, and cost competitiveness, particularly in first-grade and industrial-grade chromic acid segments. Their agility and localized customer engagement allow them to address specific market requirements that larger multinationals may not prioritize.

The remaining 10–15% of the market is occupied by fragmented regional manufacturers and emerging players, which primarily compete on pricing and geographic proximity. Overall market structure is shaped by significant barriers to entry, including capital-intensive, regulatory-compliant manufacturing, stringent environmental controls, specialized technical expertise, and rigorous customer qualification processes. Regionally, Asia Pacific shows relatively higher fragmentation due to numerous local suppliers, whereas North America and Europe remain more consolidated under multinational dominance.

Key Industry Developments

- In 2021, AOTCO Metal Finishing launched a new Type I Chromic Acid Anodizing service aimed at aerospace and other high-performance industrial clients. The Boston-based company expanded its surface treatment portfolio to meet stringent aerospace specifications, reinforcing its position as a leading provider of advanced metal plating and finishing solutions across North America.

- In January 2020, LANXESS completed the divestment of its chrome chemicals business to Brother Enterprises, a Chinese leather chemicals manufacturer. This strategic move allowed LANXESS to streamline its specialty chemicals portfolio while enabling Brother Enterprises to strengthen its presence and capabilities in the global chrome chemicals value chain.

Companies Covered in Chromic Acid Market

- LANXESS South Africa

- Soda Sanayii

- Elementis

- MidUral Group

- Novotroitsk Plant of Chromium Compounds

- Hunter Chemical

- Atotech Deutschland

- Vishnu Chemicals

- Chongqing Minfeng Chemical

- Sichuan Yinhe Chemical

- Huangshi Zhenhua Chemical

- Other Market Players

Frequently Asked Questions

The Chromic Acid market is estimated to be valued at US$ 1,057.1 Mn in 2026.

The key demand driver for the Chromic Acid market is the sustained demand from metal finishing and surface treatment applications, particularly chromium plating and anodizing.

In 2026, the Asia Pacific region will dominate the market with an exceeding 45% revenue share in the global Chromic Acid market.

Among applications, metal plating / electroplating (metal finishing) has the highest preference, capturing beyond 21% of the market revenue share in 2026, surpassing other applications.

LANXESS South Africa, Soda Sanayii, Elementis, MidUral Group, Novotroitsk Plant of Chromium Compounds, Hunter Chemical, and Atotech Deutschland. There are a few leading players in the Chromic Acid market.