- Automation & Robotics

- Checkweigher Market

Checkweigher Market Size, Share, and Growth Forecast, 2026 - 2033

Checkweigher Market by Product Type (Standalone Systems, Combination Systems), Technology Type (Strain Gauge, Electromagnetic Force Restoration), Capacity (Up to 12 kg, 12 to 60 kg, above 60 kg), Industry (Food and Beverages, Pharmaceutical, Personal Care, Logistics and Packaging, Others) and Regional Analysis for 2026 - 2033

Checkweigher Market Size and Trends Analysis

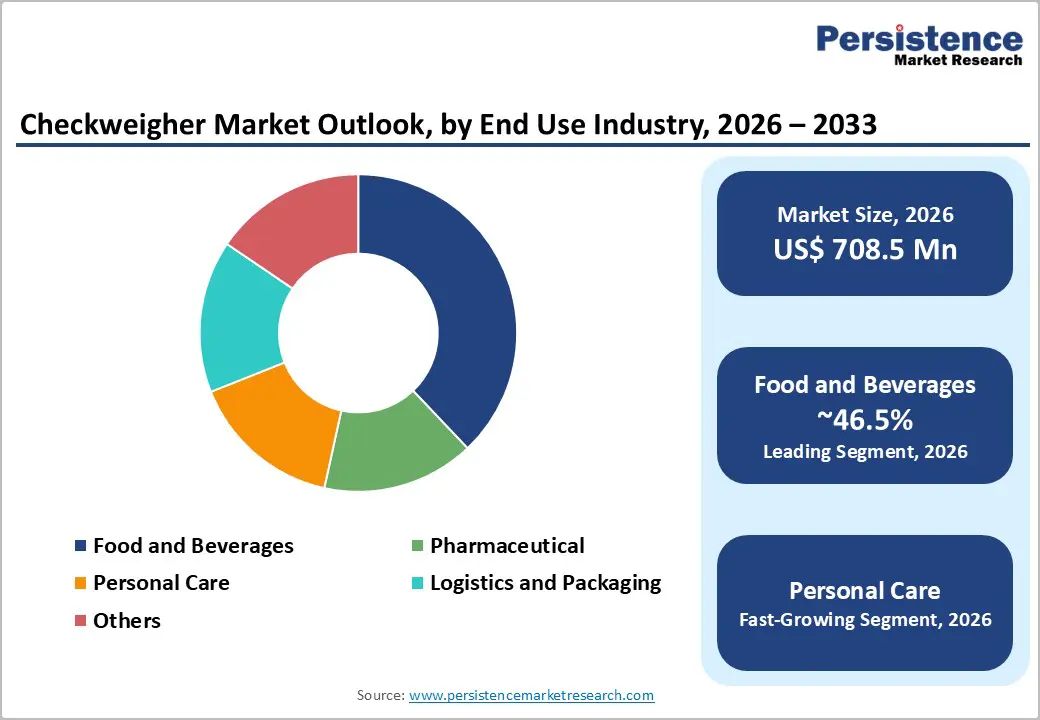

The global checkweigher market size is likely to be valued at US$ 708.5 million in 2026 and is projected to reach US$ 1,037.5 million by 2033, growing at a CAGR of 5.6% between 2026 and 2033. This expansion reflects fundamental structural shifts in manufacturing quality control, regulatory compliance mandates, and automation adoption across the food & beverage, pharmaceutical, and logistics industries.

The market's acceleration from a historical CAGR of 5.2% to 5.6% signals intensifying demand for precision weight verification systems that address product consistency, waste reduction, and regulatory compliance. Standalone checkweighing systems maintain foundational market dominance, while combination systems and AI-enabled solutions capture disproportionate growth, reflecting the industry's transition toward integrated quality control ecosystems and real-time process optimisation.

Key Industry Highlights:

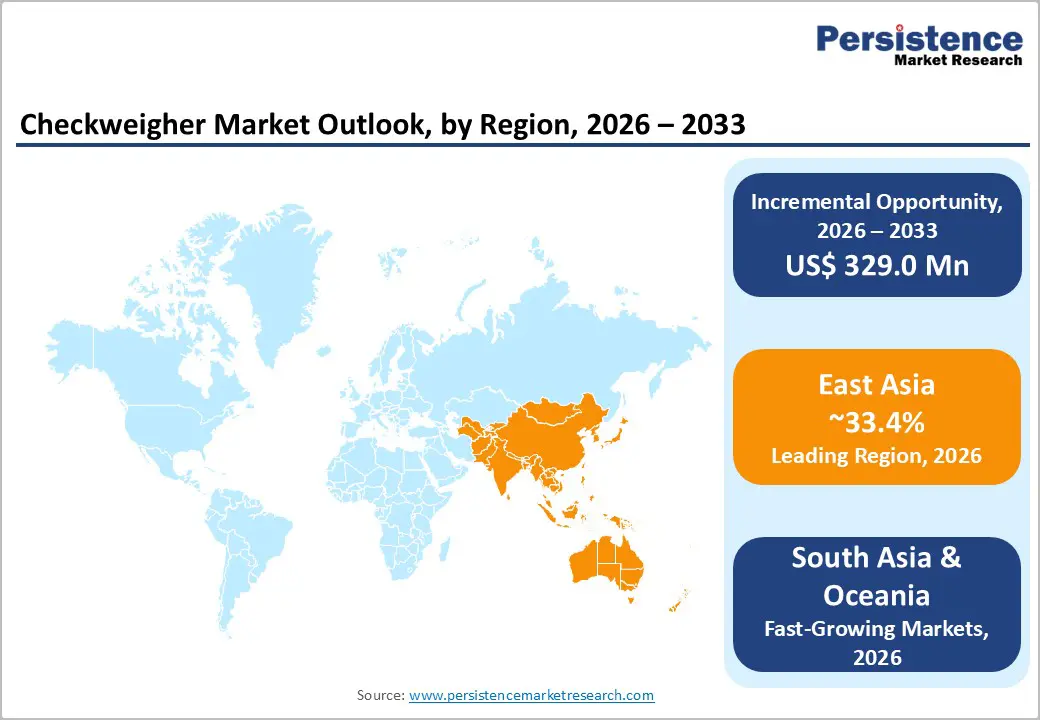

- Leading Regional Market: East Asia accounts for 33.4% of the Checkweigher market, supported by strong food-processing clusters, pharmaceutical manufacturing growth, and rapid factory automation in China, Japan, and South Korea.

- High-Value Regional Contributor: Europe accounts for 25.0% of global market value, driven by strict packaging accuracy regulations, GMP compliance in the pharma sector, and advanced inspection automation maturity.

- Dominant Product Segment: Standalone checkweighers account for 68.5% of the market, reflecting broad adoption on medium- to high-speed packaging lines across food, beverage, and pharmaceutical applications.

- Regulatory Growth Indicator: Weight-accuracy mandates, GMP/GLP pharmaceutical standards, and food-safety regulations (FDA, EU, CFDA) across major economies are accelerating the adoption of continuous inline weight inspection.

- Industrial End-user Opportunity: Food & Beverages dominate with 46.5% share, while pharmaceuticals exhibit the fastest growth due to stricter dosing accuracy, serialization, and hygiene compliance systems.

| Key Insights | Details |

|---|---|

|

Checkweigher Market Size (2026E) |

US$ 708.5 Mn |

|

Market Value Forecast (2033F) |

US$ 1,037.5 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

5.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.2% |

Market Dynamics

Drivers - Regulatory Compliance and Pharmaceutical Good Manufacturing Practice (GMP) Mandates

Pharmaceutical industry regulatory requirements are a transformative force reshaping the global checkweigher market, requiring sophisticated weight verification systems that deliver audit-ready documentation, traceability, and assurance of dosage accuracy. FDA (21 CFR 210, 211) and EU GMP regulations establish explicit expectations for equipment used in pharmaceutical manufacturing, mandating comprehensive documentation, calibration protocols, validation procedures, and data integrity frameworks that meet the ALCOA+ principles (Attributable, Legible, Contemporaneous, Original, Accurate, plus associated metadata). These regulatory frameworks eliminate substandard checkweighing designs from procurement considerations, thereby consolidating the market in favor of established manufacturers with engineering, validation, and compliance capabilities.

Pharmaceutical manufacturers face substantial operational and financial risks from non-compliant checkweighing systems, with regulatory failures resulting in batch release delays, product recalls, costly manufacturing investigations, and reputational damage. The Checkweigher Market is responding by developing GMP-compliant systems featuring Part 11-compliant software, automated rejection mechanisms with audit trails, serialization integration, and real-time data monitoring.

Pharmaceutical checkweigher adoption is accelerating across weight-critical applications, including tablet and capsule weight verification, vial inspection, ampoule verification, and the integration of serialization and anti-counterfeiting. Industry data indicate that pharmaceutical manufacturers now require 100 percent in-line inspection, backed by audit trails that support batch release and root cause investigations. The regulatory compliance imperative establishes a quality-first procurement dynamic in which GMP certification, validation support, and compliance documentation are non-negotiable purchasing criteria.

Food and Beverage Industry Weight Compliance and Product Safety Requirements

Food and beverage manufacturing is a critical growth driver for the Checkweigher Market, driven by stringent regulatory frameworks, consumer product safety expectations, and waste-reduction imperatives across global markets. The EU accommodation and food services sector employed approximately 10.9 million people and accounted for 6.8 percent of total business economy employment in 2022, generating €280.7 billion in value added. The food and beverage sector comprises nearly 2.0 million enterprises, reflecting a highly fragmented, small-business-intensive structure requiring cost-effective quality control solutions. India's food processing sector contributed 8.8% to manufacturing GVA and 8.4% to agricultural GVA in 2024, with a value of Rs. 30.5 lakh crore (US$ 354.5 billion) and projected to reach Rs. 45.8 lakh crore (US$ 535 billion) by FY26.

The U.S. food and beverage manufacturing sector accounted for 16.8 percent of total manufacturing sales, 15.4 percent of manufacturing employment, and employed approximately 1.7 million workers in 2021. Regulatory requirements, including FDA weight verification standards, EU food safety directives, and international Weights and Measures compliance mandate accurate, traceable weight verification systems.

High-speed checkweighing systems directly address food and beverage manufacturing priorities of package weight accuracy verification, product giveaway mitigation, compliance with weight regulations, and integration with metal detection and X-ray inspection systems for comprehensive contamination control. The Checkweigher Market benefits from sustained demand in the food and beverage industry for quality-control automation, production-efficiency optimization, waste reduction, and regulatory compliance across global production networks.

Market Restraining Factors - High Capital Investment Requirements and Integration Complexity

Deploying advanced checkweighing systems requires substantial capital investment in manufacturing infrastructure, engineering expertise, calibration protocols, and validation capabilities, creating barriers to adoption for small- to medium-sized manufacturers. Pharmaceutical-grade checkweighers with GMP compliance, serialization integration, and real-time data monitoring systems command premium pricing, with comprehensive systems ranging from US$50,000 to US$200,000 per unit, creating significant capital constraints for undercapitalised manufacturers. Integration complexity is compounded by the need for MES (Manufacturing Execution System) connectivity, cloud-based data storage, cybersecurity compliance, and operator training.

Food and beverage manufacturers face additional complexity when integrating checkweighers into existing production line infrastructure, which requires conveyor system modifications, control engineering, and cross-functional team coordination. Smaller manufacturers often defer investing in advanced checkweighers despite regulatory and operational advantages, preferring manual inspection processes or older-generation systems that cannot deliver GMP compliance or data integration capabilities.

Opportunities - AI-Powered Intelligent Checkweighing and Predictive Process Optimization

The checkweigher market faces a transformative opportunity through the integration of artificial intelligence and machine learning, enabling adaptive, self-optimising weight-verification systems with predictive maintenance capabilities. AI-enabled checkweighers are next-generation technology, automatically adjusting calibration settings based on environmental conditions (temperature fluctuations, humidity changes, production line vibration), detecting anomalies in real time, and optimizing weighing parameters without operator intervention. Advanced systems employ machine learning algorithms to analyse historical weight-distribution patterns, identify process drift before human operators detect deviations, and trigger preventive adjustments to maintain consistent product quality.

For pharmaceutical applications, AI integration enables real-time dosage control systems with serialization tracking and anti-counterfeiting capabilities. In food and beverage manufacturing, next-generation checkweighers use non-contact laser weighing and hyperspectral imaging to detect ingredient variance, identify foreign contaminants, and verify packaging compliance.

Logistics and e-commerce applications benefit from AI-driven dynamic weight thresholding that automatically adjusts tolerance bands based on product category, shipment type, and destination-specific compliance requirements. Manufacturers developing AI-integrated checkweighing platforms will achieve competitive differentiation through superior accuracy, reduced false rejections, lower total cost of ownership, and compliance assurance. The Checkweigher Market opportunity extends to predictive analytics integration, wherein AI systems alert maintenance teams to impending sensor drift or equipment failures, reducing unplanned downtime and production losses.

Real-Time Data Integration and IoT-Enabled Supply Chain Visibility

The checkweigher market presents substantial opportunity through connectivity architectures and data integration ecosystems, enabling real-time weight verification and information sharing across production lines, quality management systems, and enterprise supply chain platforms. Modern checkweighers increasingly support OPC-UA, Ethernet/IP, and cloud connectivity protocols enabling seamless integration with Manufacturing Execution Systems (MES), Enterprise Resource Planning (ERP) platforms, and Warehouse Management Systems (WMS). IoT-enabled checkweigher connectivity transforms weight-verification data from isolated production metrics into strategic supply-chain visibility tools, enabling real-time performance monitoring, batch-level traceability, predictive analytics integration, and automated compliance reporting.

For pharmaceutical applications, IoT integration links each product's weight to unique digital serialization records, supporting anti-counterfeiting verification and supply chain authentication. For food and beverage manufacturers, real-time data connectivity enables per-batch quality monitoring, automated documentation for regulatory audits, and rapid root cause analysis when quality deviations occur. Logistics and e-commerce companies leverage IoT-connected checkweighers for automated bill-of-lading verification, dimensional weight calculation, carrier compliance assurance, and real-time customer communication regarding accurate shipment weights.

Manufacturers develop comprehensive IoT platforms that combine hardware reliability, software sophistication, cybersecurity compliance, and cloud ecosystem integration, enabling premium positioning and customer lock-in through ecosystem switching costs. This connectivity opportunity extends to the digital transformation of manufacturing facilities, with checkweighers serving as anchor devices that connect quality control systems to broader Industry 4.0 ecosystems.

Category-wise Analysis

Product Type Insights

Standalone checkweigher systems maintain the dominant market position, representing 68.5% of global market share in 2026, reflecting foundational cost advantage, operational simplicity, and widespread applicability across food and beverage, pharmaceutical, and light industrial applications. Standalone systems offer manufacturers cost-effective quality control solutions for production lines where integrated material handling or specialized process requirements are not necessary. These systems deliver high-speed weight verification of up to 200 products per minute, precise accuracy within ±1–5 g, and reliable reject mechanisms for products that fall outside specified tolerances.

Standalone system architecture enables rapid installation, minimal production-line modifications, and straightforward operator training, making it particularly valuable for small- to medium-sized manufacturers and regional operations. The segment's market dominance reflects sustained demand, replacement cycles, facility expansion projects, and adoption by price-sensitive manufacturing segments that prioritise cost minimisation over advanced feature integration.

Combination checkweighing systems represent the fastest-growing product category, driven by pharmaceutical GMP requirements, food safety integration mandates, and manufacturing facility modernization toward comprehensive quality control ecosystems. Combination systems integrate checkweighing with complementary inspection technologies, including metal detection, X-ray systems, vision-based defect identification, serialization modules, and reject automation. Combination architecture enables manufacturers to deploy 100 per cent in-line inspection, addressing multiple quality parameters simultaneously, substantially reducing inspection time and improving product quality assurance.

Industry Insights

Food and beverage manufacturing represents the Checkweigher Market's dominant end-use segment, commanding 46.5% market share in 2026, reflecting universal product packaging requirements, regulatory compliance mandates, and consumer safety expectations across global food production networks. Food and beverage manufacturers require checkweighing systems that verify package weight accuracy, mitigate product giveaway, comply with international Weights and Measures regulations, and integrate with contamination detection systems.

The segment's market dominance reflects sustained demand replacement cycles across global production facilities, facility expansion projects in emerging markets, and continuous technology upgrading as manufacturers implement advanced inspection capabilities. EU food services sector employment of 10.9 million people generating €280.7 billion in value added, combined with India's US$ 354.5 billion food processing market and the U.S. 16.8% food manufacturing share of total manufacturing sales, underscores the segment's substantial scale and growth trajectory. Food and beverage customer preference for established checkweigher manufacturers with proven reliability, responsive technical support, and compliance certifications supports continued market leadership.

Logistics and packaging represent the fastest-growing end-use segment, driven by e-commerce order fulfilment expansion, global parcel volume growth, and automation infrastructure modernisation. The global logistics automation market is underscored by accelerating automation adoption supporting e-commerce fulfilment requirements. Checkweigher systems play a critical role in modern fulfilment centres, supporting real-time parcel tracking, accurate bill-of-lading generation, dimensional weight calculation, carrier compliance verification, and order-to-dispatch cycle time optimization from hours to minutes.

Regional Insights and Trends

North America Checkweigher Market Trends

North America represents a mature, technologically advanced market, commanding approximately 20% of the global checkweigher market share in 2026, characterized by established OEM supply chain networks, stringent regulatory requirements from the FDA and USDA, and substantial investment in manufacturing automation and quality-control infrastructure. The U.S. food and beverage manufacturing sector's 16.8 percent share of total manufacturing sales, 15.4 % of manufacturing employment, and 1.7 million workers underscore substantial demand for checkweighers across food processing operations. FDA and USDA regulatory compliance standards, particularly those addressing product quality, weight accuracy, and consistency, drive manufacturers to adopt high-accuracy checkweighing solutions with robust documentation, calibration protocols, and audit-trail capabilities.

North America's pharmaceutical manufacturing sector is a particularly strong market for checkweighers, with GMP compliance, FDA Part 11 data-integrity requirements, and serialization mandates sustaining demand for advanced pharmaceutical-grade systems. The region's logistics and e-commerce automation infrastructure expansions, supported by projected growth in the logistics automation market at a 12.80 percent CAGR through 2034, drive checkweigher adoption across fulfilment centres, distribution facilities, and parcel-handling operations. Regional market growth projections range from 4.5 to 5.2 percent annually, reflecting market maturity offset by continued automation adoption and regulatory compliance intensity. Leading North American manufacturers, including Mettler-Toledo, Minebea Intec, Anritsu, Thermo Fisher Scientific, and regional specialists, maintain strong market positions through established customer relationships, local service infrastructure, and proven compliance certification capabilities.

East Asia Checkweigher Market Trends

East Asia represents the global checkweigher market's largest and fastest-growing region, commanding approximately 33.4% regional market share in 2026 and demonstrating exceptional growth momentum driven by manufacturing-intensive expansion, pharmaceutical industry modernisation, and emerging market food and beverage production growth. China represents the region's manufacturing powerhouse, supporting large-scale food and beverage production, pharmaceutical manufacturing, and e-commerce logistics infrastructure.

Japan's manufacturing sector demonstrates maturity and advanced adoption of automation, with Japanese manufacturers prioritising AI-driven weight monitoring, real-time data analytics, and smart factory integration. The region benefits from a rising B2B e-commerce GMV growth trajectory, with Asia-Pacific accounting for 80 percent of projected global B2B e-commerce by 2026, thereby driving demand for logistics and parcel checkweighers across fulfilment operations. East Asia's estimated annual growth rates range from 7 to 11 percent, substantially exceeding global averages, reflecting structural manufacturing expansion, emerging market regulatory convergence, and sustained food/pharmaceutical industry investment.

Europe Checkweigher Market Trends

Europe is a mature, technologically sophisticated market, accounting for approximately 25% of the global market in 2026, characterized by stringent environmental regulations, advanced manufacturing standards, and substantial investment in pharmaceutical innovation and food safety infrastructure. The EU accommodation and food services sector employs 10.9 million people, generating €280.7 billion in value added, underscoring substantial food and beverage checkweigher demand across European production networks. EU regulatory frameworks, including strict food safety directives, pharmaceutical GMP mandates aligned with ICH guidelines, and weight verification standards, establish particularly stringent checkweigher specifications and compliance requirements. European pharmaceutical manufacturing represents a particularly strong market segment, with companies deploying advanced validation protocols, comprehensive documentation frameworks, and serialisation capabilities supporting CDSCO (Indian regulatory alignment), EMEA (European Medicines Agency), and ICH guidelines.

The region's food and beverage sector demonstrates sustained demand for checkweighing systems that integrate metal detection, X-ray inspection, and vision-based quality control, thereby ensuring comprehensive contamination prevention and product safety. The European Union's emphasis on the circular economy, waste-reduction mandates, and sustainability commitments create additional market preference for checkweigher systems that optimise material efficiency, reduce product giveaway, and minimise packaging waste. Regional market growth projections range from 4.8 to 5.8 percent annually, reflecting market maturity balanced against strong pharmaceutical innovation momentum and food safety regulation intensity.

Competitive Landscape

The global checkweigher market is moderately consolidated with oligopolistic characteristics, dominated by a few multinational players, while smaller regional suppliers serve niche markets. Leading companies such as Mettler-Toledo International Inc., Ishida Co., Ltd., Minebea Intec, Thermo Fisher Scientific Inc., Bizerba SE & Co. KG, and Anritsu Corporation hold significant market share, competing on precision, automation, integration with inspection systems, and real-time data analytics.

While these top players control the majority of high-value segments like food & beverages and pharmaceuticals, smaller regional firms provide cost-effective or specialized solutions, maintaining competition at the periphery. Technological innovation, including IoT-enabled and AI-based checkweighers, drives differentiation, and ongoing expansion in automated production lines sustains market growth.

Key Developments:

- In December 2025, Superior Industries International, Inc. completed an acquisition by a group of its term loan investors, including Oaktree Capital Management, converting a portion of debt into equity and strengthening its balance sheet. The transaction positions Superior for long-term growth in the global wheel industry, allowing increased investment in operations, customer relationships, and regional supply capabilities, while also appointing Michael Dorah as the new CEO to lead the company’s strategic expansion.

- In August 2025, Mettler-Toledo Product Inspection showcased its latest checkweighing and combination inspection solutions at Anuga FoodTec 2025, highlighting the C33 PlusLine Checkweigher, CM and CX combination systems, and X52 X-ray inspection system. These advanced systems integrate precision weighing with contamination detection, offering enhanced operational efficiency, reduced waste, and improved regulatory compliance, while providing flexible, Industry 4.0-ready solutions for diverse food packaging applications.

Companies Covered in Checkweigher Market

- Mettler Toledo

- Anritsu Infivis

- Multivac

- Bizerba

- Yamato Scale

- WIPOTEC-OCS

- LOMA Systems

- Ishida Co., Ltd

- Cassel Messtechnik GmbH

- Thermo Fishcer Scientific Inc

Frequently Asked Questions

The global checkweigher market is projected to be valued at US$ 708.5 Mn in 2026.

The Standalone Systems segment is expected to account for approximately 68.5% of the global checkweigher market by Product Type in 2026.

The market is expected to witness a CAGR of 5.6% from 2026 to 2033.

Regulatory compliance mandates (GMP, FDA, EU), pharmaceutical weight accuracy and traceability requirements, and food & beverage safety and weight verification standards collectively drive Checkweigher Market growth by enforcing automated, audit-ready, in-line quality control systems.

AI-powered intelligent inspection, predictive analytics, and IoT-enabled real-time data integration represent the key opportunities in the Checkweigher Market, enabling adaptive accuracy, compliance automation, supply chain visibility, and reduced total cost of ownership across pharma, food, logistics, and e-commerce applications.