- Food Packaging

- Biodegradable Food Packaging Market

Biodegradable Food Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Biodegradable Food Packaging Market by Material (Paper & Paperboard, Bioplastics, Others), Packaging Type (Pouches & Bags, Trays & Clamshells, Others), Application, and Regional Analysis for 2026 - 2033

Biodegradable Food Packaging Market Size and Trends Analysis

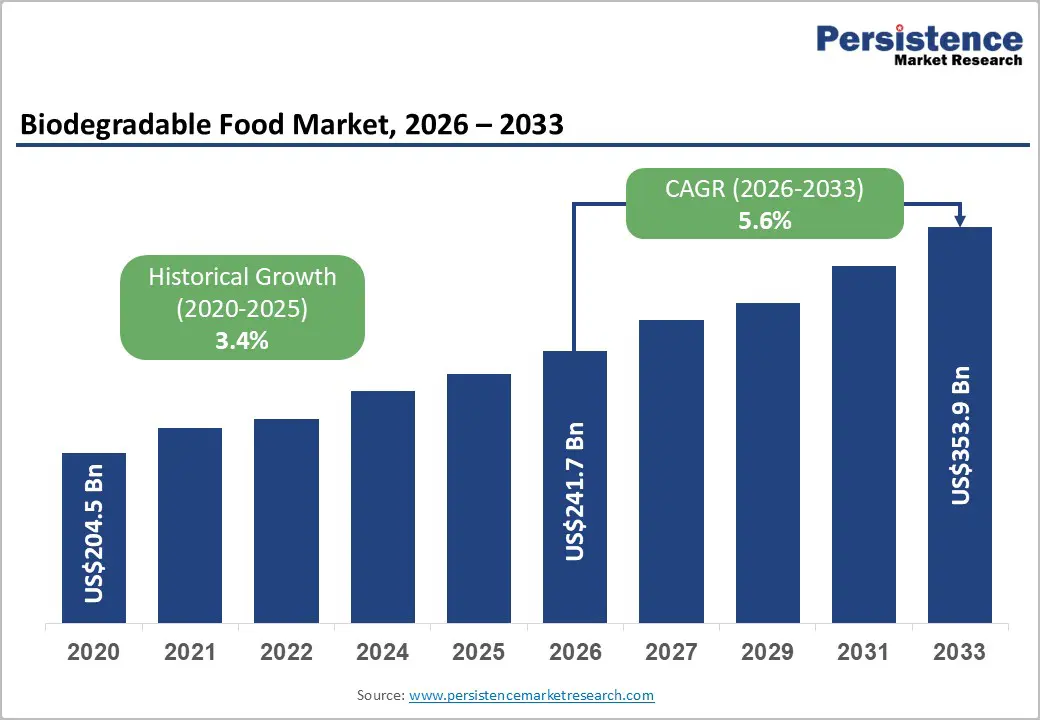

The global biodegradable food packaging market size is likely to be valued at US$241.7 billion in 2026 and is expected to reach US$353.9 billion by 2033, growing at a CAGR of 5.6% between 2026 and 2033, drivenby regulatory mandates restricting single-use plastics, advancements in bioplastic materials such as PLA and PHA, and expanding demand from foodservice and retail sectors. Industrial composting capacity is gradually increasing in developed markets, improving end-of-life viability.

Consumer preference for sustainable packaging and the continued rise of online food delivery are accelerating adoption, particularly in flexible and takeaway packaging formats. Historical growth remained moderate at 3.4%, reflecting early-stage infrastructure and cost constraints, while the forecast period reflects stronger regulatory and commercial alignment.

Key Industry Highlights:

- Leading Region: Asia Pacific is projected to hold the largest share of the market at approximately 37.6%, supported by strong manufacturing scale, China's bioplastic production capacity, rising food delivery demand across ASEAN, and regulatory enforcement in India and Japan.

- Fastest-Growing Region: North America, driven by state-level legislation such as California’s SB 54, corporate sustainability commitments from major QSR and beverage brands, and expanding composting infrastructure in the U.S. and Canada.

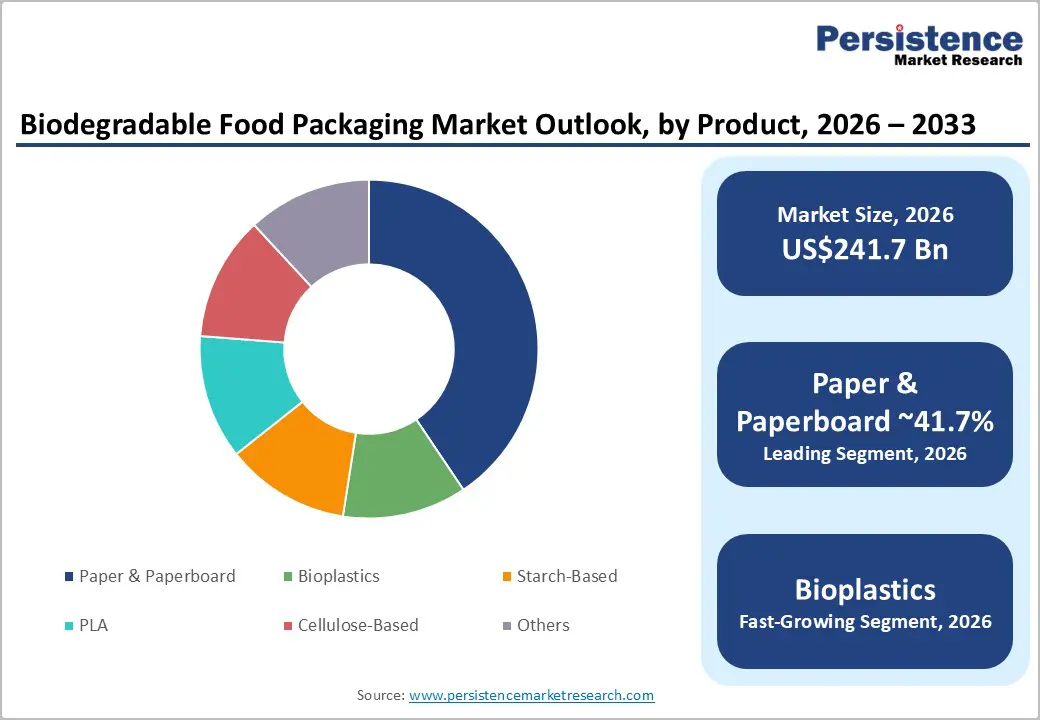

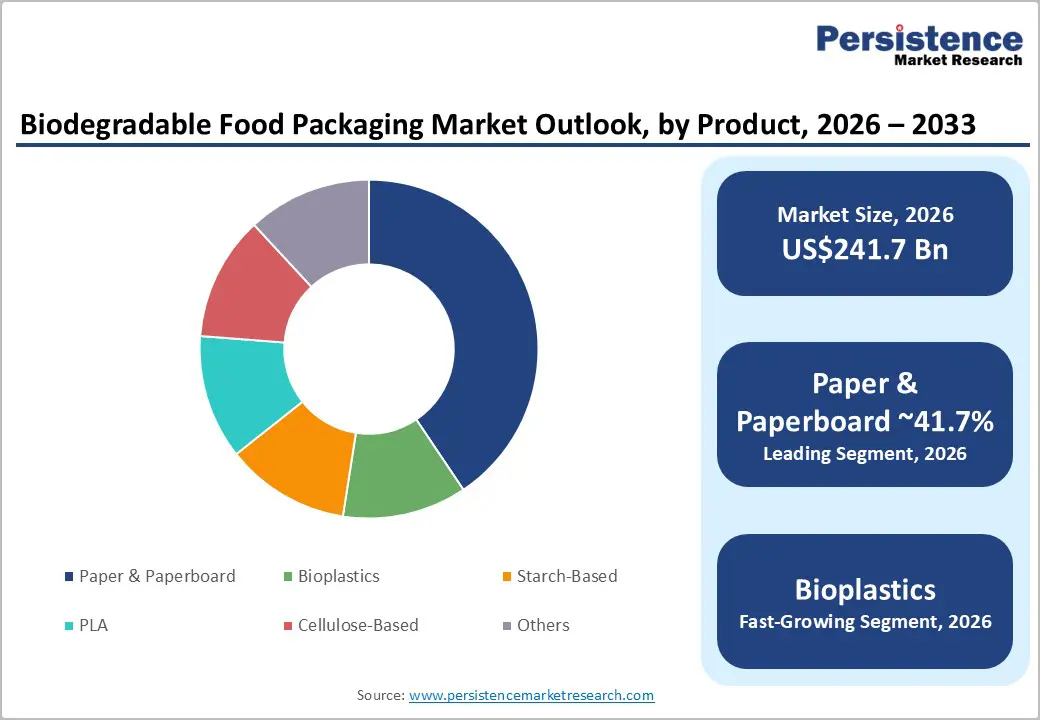

- Dominant Material: The paper & paperboard is anticipated to lead the material segment with an anticipated 41.7% market share, supported by established recycling systems, molded fiber adoption in foodservice, and regulatory familiarity across North America and Europe.

- Leading Packaging Type: Pouches & bags are estimated to account for approximately 28.2% share, driven by lightweight structure, lower transportation costs, strong adoption in snacks and fresh produce packaging, and compatibility with biodegradable flexible laminate technologies.

| Key Insights | Details |

|---|---|

|

Biodegradable Food Packaging Market Size (2026E) |

US$241.7 Bn |

|

Market Value Forecast (2033F) |

US$353.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Regulatory Tightening and Public Policy

Governments across North America, Europe, and parts of Asia Pacific are strengthening packaging waste legislation and restricting certain single-use plastics. Regulations increasingly require recyclable or compostable packaging designs and impose producer responsibility obligations. In Europe, packaging reforms establish mandatory recyclability targets by 2030 and restrict selected single-use items used in food contact applications. Similar state-level regulations in the U.S. and national policies in Asia are accelerating the shift toward biodegradable materials. Food manufacturers and quick-service restaurants are transitioning to certified compostable materials such as PLA, molded fiber, and cellulose-based packaging. Companies operating across multiple jurisdictions must comply with varying standards, increasing the urgency for standardized biodegradable solutions and supporting sustained market expansion.

Advances and Scale-up in Bioplastic Technologies

Significant innovation in PLA, PHA, and starch-blend chemistries has improved barrier performance, heat resistance, and mechanical strength. Investments in fermentation and polymerization capacity are lowering per-unit production costs. Increased upstream integration in bio-feedstocks has stabilized supply chains and improved production efficiency. Cost improvements are narrowing the price gap between conventional plastics and biodegradable alternatives. Enhanced material performance allows biodegradable plastics to enter applications such as hot-fill containers, rigid trays, and high-barrier films that were previously limited to petrochemical-based plastics. Larger production capacity reduces lead times and supports mainstream brand adoption.

Changing Consumer and Retail Procurement Behavior

Retailers and foodservice operators increasingly integrate sustainability key performance indicators into procurement strategies. Packaging sustainability ranks among the most influential factors affecting purchasing decisions for fresh and prepared food products. Major retail chains require suppliers to demonstrate compostability or recyclability certifications. Demand is concentrated in private label retail and quick-service restaurant channels, which favor scalable, certified packaging formats compliant with ASTM and EN compostability standards. Converters are expanding certified product lines in pouches, trays, and takeaway containers. High-visibility categories such as fresh produce, bakery, and ready-to-eat meals are experiencing accelerated adoption.

Barrier Analysis - Higher Raw Material and Conversion Costs

Biodegradable polymers and specialty fiber materials often carry a cost premium compared to conventional plastics. Expenses include raw resin pricing, tooling modifications, and certification testing for compostability and food contact safety. In price-sensitive product categories, even a 5–12% cost differential may discourage conversion unless mandated by regulation. Feedstock price volatility, particularly corn and sugarcane, combined with energy cost fluctuations, further pressures margins for packaging converters and brand owners.

Infrastructure and End-of-Life Limitations

Industrial compostability depends on access to commercial composting facilities. Infrastructure remains uneven across regions, particularly in developing economies. Without appropriate collection systems and labeling clarity, compostable packaging risks diversion to landfill or conventional recycling streams. In markets lacking robust composting networks, effective circular processing rates may fall below 30–40% of volumes placed on the market. This infrastructure gap can undermine environmental benefits and slow long-term adoption unless waste management systems expand.

Opportunity Analysis - Flexible Formats for Food Delivery and Retail

Rapid growth in online food delivery and ready-to-eat meal kits is driving demand for lightweight, high-performance biodegradable films and pouches. Flexible packaging offers material efficiency and transportation advantages. Converting 15–20% of global food-delivery packaging volumes to biodegradable formats by 2030 represents a multi-billion-dollar incremental opportunity. Strategic co-development partnerships with meal-kit providers and quick-service restaurants can secure long-term supply contracts and justify capital investments in specialized converting equipment.

Emerging Markets and Manufacturing Localization

Asia Pacific’s feedstock availability and lower conversion costs create competitive manufacturing advantages. With the region holding approximately 37.6% of global market share, incremental capacity expansion could significantly expand export and domestic supply. Capturing an additional five percentage points of global market share through localized production and certification infrastructure may generate substantial incremental revenue by 2030. Multinational packaging companies are increasingly pursuing joint ventures with regional bioplastic producers to accelerate market penetration.

Category-wise Analysis

Material Insights

The paper and paperboard segment is anticipated to maintain its leadership position, accounting for 41.7% of market share in 2026, driven by widespread raw material availability, mature recycling infrastructure, and compatibility with the existing converting equipment. The segment dominates applications such as trays, cartons, cups, folding cartons, and secondary packaging. Molded fiber and bagasse-based formats are extensively used in quick-service restaurants (QSRs), supermarket deli counters, and takeaway packaging.

Major food chains increasingly deploy molded fiber clamshells and paperboard bowls as substitutes for expanded polystyrene. Retail-ready paperboard cartons for dairy, bakery, and fresh produce remain a preferred solution due to cost efficiency and regulatory acceptance. Manufacturers are advancing grease-resistant and moisture-barrier performance using water-based dispersions and PFAS-free coatings to meet tightening chemical compliance requirements. The regulatory familiarity of fiber-based packaging, combined with established curbside recycling streams in North America and Europe, reinforces continued adoption. Over the forecast period, fiber innovations such as barrier-coated recyclable paper laminates are expected to sustain this segment’s dominant position.

Bioplastic materials, including PLA (polylactic acid), PHA (polyhydroxyalkanoates), and bio-based polyethylene blends, represent the fastest-growing material segment due to sustained performance improvements and scaling production capacity. Advances in crystallized PLA and high-heat PHA formulations have enhanced thermal resistance and oxygen barrier properties, enabling broader application in rigid trays, lidded yogurt cups, coffee cup lids, and flexible films. Several packaging manufacturers have introduced thermoformed PLA trays for fresh-cut produce and ready-to-eat meals, replacing PET in select markets.

Compostable coffee capsules and takeaway containers made from bio-resins are gaining traction in Europe and parts of North America. Vertical integration across feedstock sourcing and resin manufacturing is improving cost competitiveness, narrowing the price gap with conventional plastics. As industrial composting infrastructure expands in urban centers, bioplastics are expected to capture an incremental share of flexible polyethylene and polypropylene packaging.

Packaging Type Insights

Pouches and bags are anticipated to hold approximately 28.2% of the market share in 2026, making them the leading packaging type. Their dominance stems from low material intensity, lightweight construction, and logistical efficiency, which reduce transportation costs and emissions. These formats are widely adopted for snack foods, dried grains, frozen vegetables, fresh produce, and bakery items. Biodegradable stand-up pouches and compostable snack wrappers are increasingly used in private-label retail brands seeking to enhance sustainability positioning.

Meal-kit providers and specialty organic food brands have also adopted compostable flexible packaging to align with environmentally conscious consumers. Retailers favor flexible biodegradable laminates due to shelf appeal and compatibility with automated filling lines. Incremental growth is supported by promotional packaging campaigns and sustainability-driven product relaunches, particularly in natural and health-focused food categories.

Trays and clamshells represent the fastest-growing packaging type, driven primarily by expansion in foodservice and takeaway applications. Molded fiber clamshell containers and thermoformed bioplastic trays provide compostable alternatives to polystyrene foam and PET formats traditionally used for hot meals and fresh produce. Quick-service restaurants are increasingly transitioning to molded fiber burger boxes and compostable salad bowls in response to municipal plastic restrictions.

Supermarket deli sections are adopting fiber-based or PLA-lined trays for ready meals and prepared foods. Improvements in structural rigidity, heat tolerance, and grease resistance have enhanced product performance in hot-food environments. Capital investment in thermoforming and molded fiber production lines is increasing globally, positioning converters to capture rapid growth in ready-meal and delivery-driven packaging demand.

Regional Market Insights

North America Biodegradable Food Packaging Market Trends - State-Level Plastic Mandates and QSR-Led Fiber & Compostable Packaging Adoption

North America is projected to record the fastest growth rate between 2026 and 2033, supported by tightening regulatory enforcement and measurable corporate sustainability commitments. While the region holds a smaller overall share than Asia Pacific, its growth trajectory is strengthened by rapid substitution of conventional plastics in foodservice and retail packaging. The U.S. leads regional demand due to its large quick-service restaurant (QSR) footprint, organized retail penetration, and evolving state-level regulations.

California’s SB 54 (Plastic Pollution Prevention and Packaging Producer Responsibility Act) mandates 100% recyclable or compostable packaging by 2032 and requires a 25% reduction in plastic packaging, directly accelerating procurement shifts toward fiber-based and certified compostable formats. Oregon’s Plastic Pollution and Recycling Modernization Act similarly strengthens producer responsibility and recyclability standards. These policies are influencing national brand strategies because manufacturers often standardize packaging formats across states to maintain supply chain efficiency.

Corporate initiatives reinforce regulatory momentum. For example, Starbucks has expanded its transition to fiber-based molded lids and compostable cold cups in select U.S. markets, reducing reliance on petroleum-based plastics. McDonald’s USA continues phasing out foam packaging and expanding fiber-based clamshell deployment, aligning with its global packaging sustainability goals. These procurement shifts create scale demand for molded fiber and compostable resin suppliers. Canada complements U.S. policy drivers with federal measures such as the Single-Use Plastics Prohibition Regulations, which restrict specific plastic foodservice items.

Major Canadian municipalities, including Toronto and Vancouver, have expanded organics diversion programs, supporting certified compostable packaging uptake. Investment activity is also reshaping the regional supply base. Danimer Scientific expanded PHA biopolymer production capacity in Kentucky, aiming to supply compostable food packaging applications. NatureWorks announced progress toward establishing North American Ingeo™ PLA capacity, strengthening local resin availability. Private equity firms have increased participation in sustainable packaging converters, targeting businesses with molded fiber and compostable film capabilities.

Europe Biodegradable Food Packaging Market Trends - EU Policy Harmonization, Plastic Taxation, and Fiber-Based Food Packaging Scale-Up

Europe’s biodegradable food packaging market is characterized by policy harmonization, strong enforcement mechanisms, and high consumer awareness. The EU Single-Use Plastics Directive (SUPD) and Packaging and Packaging Waste Regulation (PPWR) reforms are central to procurement transformation, requiring recyclability, reduced plastic intensity, and extended producer responsibility compliance. The U.K. has accelerated change through the Plastic Packaging Tax, which applies to plastic packaging with less than 30% recycled content. This fiscal mechanism incentivizes material substitution and bio-based alternatives. UK-based foodservice chains increasingly deploy compostable takeaway containers and fiber clamshells in response to both taxation and municipal plastic bans.

In France, anti-waste legislation (AGEC Law) mandates progressive elimination of single-use plastic packaging for fruits and vegetables, directly increasing paper-based and compostable film adoption. French food brands have introduced cellulose-based and paper flow-wrap solutions for fresh produce. Spain has strengthened enforcement of EU waste directives, encouraging foodservice operators to transition toward certified compostable takeaway packaging. Industry developments illustrate supply-side scaling. Huhtamaki has expanded molded fiber capacity across Europe, including investments in sustainable fiber packaging lines to replace polystyrene trays. Stora Enso has commercialized fiber-based barrier materials designed to replace plastic laminates in food applications, addressing recyclability and PFAS concerns.

Investment trends emphasize PFAS-free coatings, water-based barrier technologies, and closed-loop material innovation. Strategic collaborations between material science companies and converters are accelerating recyclable paper-based alternatives for dairy cups and ready-meal trays. Europe’s growth remains policy-led, with compliance requirements acting as a structural demand catalyst rather than discretionary adoption. Regulatory clarity continues to provide long-term visibility for investment and capacity expansion.

Asia Pacific Biodegradable Food Packaging Market Trends - Manufacturing Scale, Biopolymer Capacity Expansion, and Food Delivery–Driven Demand

Asia Pacific is anticipated to hold approximately 37.6% of market share in 2026, making it the largest regional market. Manufacturing scale, feedstock availability, rapid urbanization, and rising food delivery consumption underpin demand growth. The region combines cost-competitive production with expanding domestic consumption, strengthening its leadership position.

China maintains a significant bioplastic production base and has implemented phased restrictions on non-degradable plastic bags and single-use items in major cities. Government policy has encouraged substitution with biodegradable alternatives, stimulating domestic PLA and PBAT production. Chinese manufacturers have expanded export-oriented capacity to supply global food packaging converters. Companies such as Kingfa Sci. & Tech. and other biopolymer producers have scaled biodegradable resin output, supporting both domestic and international markets.

India has implemented nationwide restrictions on specific single-use plastic products, encouraging fiber-based and compostable packaging adoption in organized retail and QSR chains. Major food delivery platforms such as Swiggy and Zomato have piloted sustainable packaging initiatives, including compostable cutlery and containers for partner restaurants. Domestic molded fiber producers are scaling capacity to serve urban foodservice demand.

Across ASEAN countries, growth is linked to expanding e-commerce and food delivery platforms. Indonesia and Thailand are strengthening plastic waste regulations, encouraging gradual substitution toward biodegradable formats. Regional converters are investing in thermoforming lines capable of processing PLA and starch-based materials to serve both domestic and export markets. Investment activity includes greenfield PLA production projects, expansion of PBAT blending facilities, and export-focused molded fiber manufacturing plants. The combination of production scale, regulatory enforcement, and consumer adoption positions Asia Pacific as both the largest and one of the structurally most dynamic biodegradable food packaging markets globally.

Competitive Landscape

The global biodegradable food packaging market is moderately fragmented, comprising diversified global packaging companies and specialized biodegradable material producers. Fiber-based packaging segments show higher consolidation among established paper manufacturers, while compostable film and bioplastic segments remain more fragmented. Strategic partnerships, acquisitions, and vertical integration across feedstock, resin production, and converting operations are reshaping competitive positioning.

Key strategies include product innovation in high-barrier compostable films, vertical integration across bio-feedstock supply chains, and geographic expansion through joint ventures in Asia Pacific. Companies differentiate through certification compliance, performance reliability, and circular economy partnerships.

Key Industry Developments:

- In July 2025, INEOS Styrolution launched its 100% bio-based polystyrene product, Styrolution PS 158K BC100, with food trays made from this material entering the Japanese market through a retail partnership, demonstrating expanded biopolymer innovation in food packaging applications.

- In April 2025, Bubbies Ice Cream introduced new certified home-compostable paper pulp trays for its mochi ice cream products, replacing conventional clamshell liners and significantly reducing plastic waste from its packaging lines.

Companies Covered in Biodegradable Food Packaging Market

- Amcor plc

- Huhtamaki Oyj

- Stora Enso Oyj

- Mondi Group

- Tetra Pak International S.A.

- Sealed Air Corporation

- Smurfit Westrock plc

- DS Smith plc

- NatureWorks LLC

- Novamont S.p.A.

- BASF SE

- Danimer Scientific

- TIPA Corp Ltd.

- Vegware Ltd.

- BioPak Pty Ltd.

- TotalEnergies Corbion

- Futamura Group

- Walki Group Oy

Frequently Asked Questions

The global biodegradable food packaging market is projected to be valued at US$241.7 billion in 2026.

The biodegradable food packaging market is expected to reach approximately US$353.9 billion by 2033.

Key trends include the rapid scale-up of PLA and PHA bioplastics, increasing adoption of molded fiber and bagasse-based trays, integration of PFAS-free barrier coatings, expansion of compostable flexible pouches, and strategic partnerships between packaging producers and waste management companies to improve end-of-life outcomes.

Paper & paperboard is the leading material segment, anticipated to account for 41.7% of total market share in 2026, driven by strong recycling infrastructure and regulatory acceptance.

The biodegradable food packaging market is projected to grow at a CAGR of 5.6% between 2026 and 2033.

Major players include Amcor plc, Huhtamaki Oyj, Stora Enso Oyj, Mondi Group, and NatureWorks LLC.