- Food Packaging

- Biodegradable Meal Trays Market

Biodegradable Meal Trays Market Size, Share, and Growth Forecast, 2026 - 2033

Biodegradable Meal Trays Market By Material (Bagasse, Bamboo, Others), Compartment (Single-compartment, Multi-compartment, Others), Application, and Regional Analysis for 2026 - 2033

Biodegradable Meal Trays Market Size and Trends Analysis

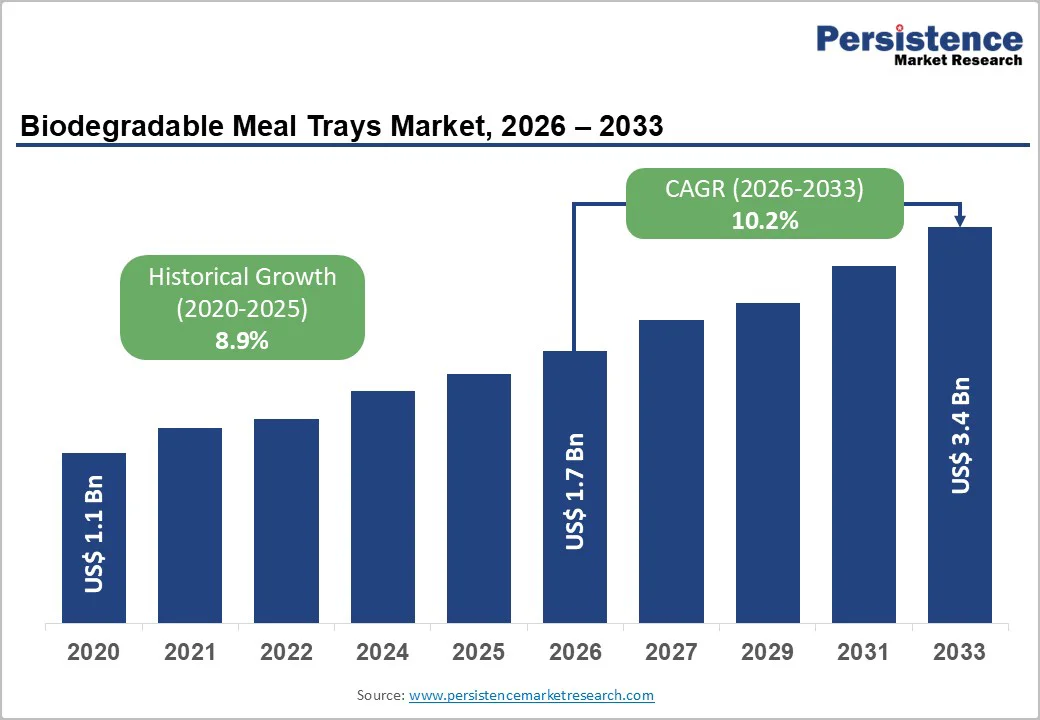

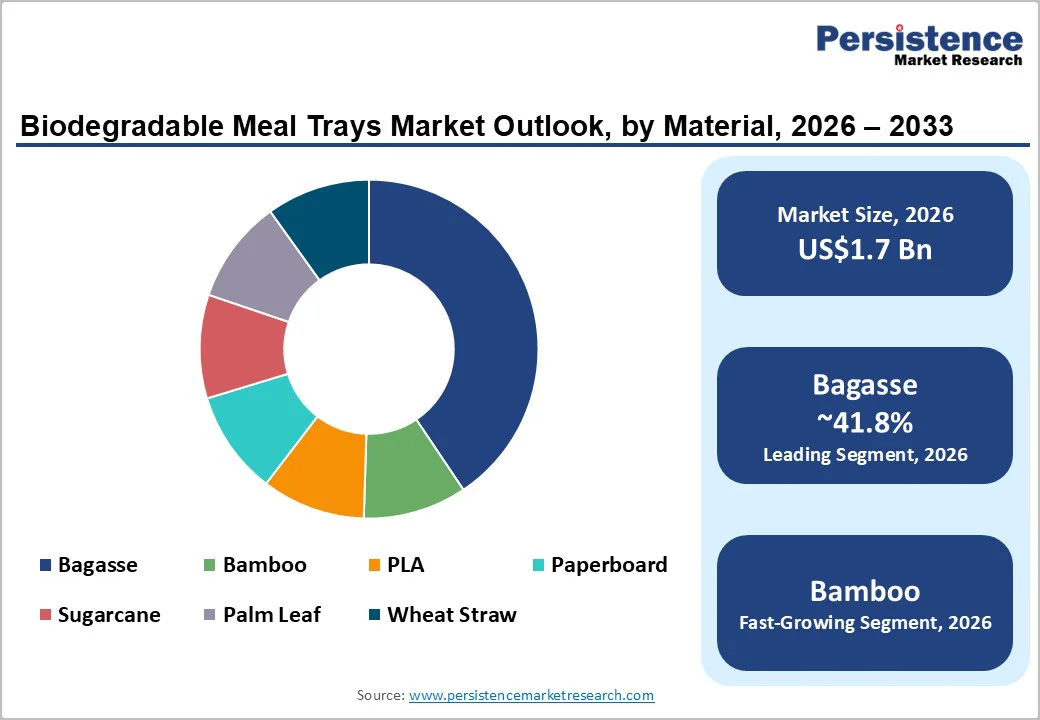

The global biodegradable meal trays market size is likely to be valued at US$1.7 billion in 2026 and is expected to reach US$3.4 billion by 2033, growing at a CAGR of 10.2% between 2026 and 2033, driven by the stringent regulations on single-use plastics, rapid adoption of fiber-based and compostable materials such as bagasse and PLA, and rising foodservice and takeaway consumption.

Improvements in molded-fiber manufacturing and expanding industrial composting infrastructure are reducing the total cost of ownership for institutional buyers. The market outlook remains influenced by feedstock pricing, certification compliance, and variation in regional waste-collection systems.

Key Industry Highlights

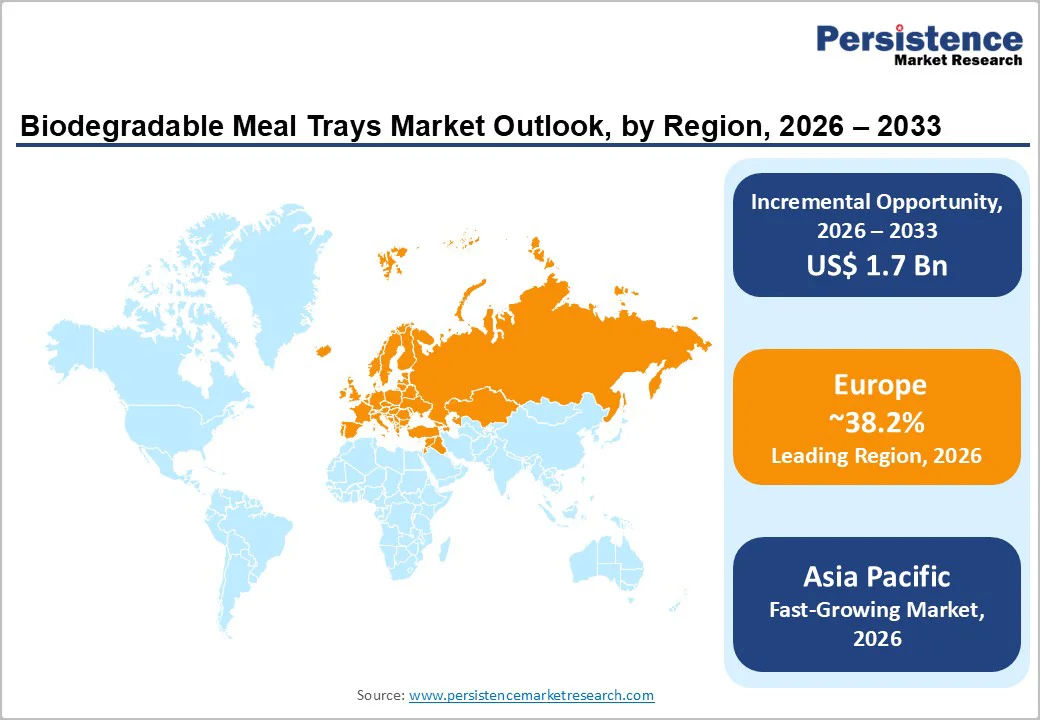

- Leading Region: Europe is anticipated to lead the market with an estimated 38.2% market share, supported by strong regulatory frameworks, mature composting infrastructure, and high institutional procurement of certified compostable trays.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, driven by abundant bagasse feedstock, expanding foodservice ecosystems, and rising sustainability mandates.

- Investment Plans: Global investments are boosting molded-fiber capacity, advancing bio-barrier technologies, and scaling dry-molded systems. Notable examples include Huhtamaki’s U.S. and EU expansions, Stora Enso’s upgrades in Sweden, and major capacity additions in India by Yash Pakka and CHUK.

- Dominant Material: Bagasse, to hold 41.8% market share in 2026, due to wide feedstock availability, cost efficiencies, and suitability for high-volume tray manufacturing.

- Leading Compartment: Single-compartment trays, to account for 47.4% of total revenue in 2026, owing to their widespread use in quick-service restaurants, institutional kitchens, and mass meal distribution.

| Key Insights | Details |

|---|---|

| Biodegradable Meal Trays Market Size (2026E) | US$1.7 Bn |

| Market Value Forecast (2033F) | US$3.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 10.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis - Regulatory Tightening and Single-Use Plastics Bans

Government regulations restricting single-use plastics have become one of the most influential catalysts driving the biodegradable meal trays market. Policies implemented across the European Union, U.S. states, and several Asia-Pacific countries are accelerating the shift toward certified compostable products.

Standards such as EN 13432 in Europe and ASTM D6400/D6868 in the U.S. provide clear guidelines for compostability claims, influencing procurement among institutions such as schools, hospitals, public agencies, and nationwide foodservice chains.

These mandates redirect purchasing away from petroleum-based packaging and toward biodegradable trays, resulting in sustained double-digit growth across regulated regions. The regulatory emphasis on recyclability, organic-waste diversion, and reduced plastic pollution has strengthened market certainty and long-term investment flows.

Cost and Performance Improvements in Molded-Fiber and PLA Technologies

Advancements in molded-fiber forming equipment, dry-molding systems, and PLA or bio-based barrier-film technologies have reduced energy and water consumption during production. These improvements lower per-unit manufacturing costs and elevate performance characteristics such as heat resistance, strength, and microwave compatibility.

Dry-molded fiber, in particular, minimizes water usage and shortens cycle times compared with traditional wet molding. These developments have enabled manufacturers to produce larger, multi-compartment trays at competitive costs, broadening adoption across catering, meal-kit services, and institutional food distribution.

The improved economics bring biodegradable trays closer to price parity with coated paperboard and plastic alternatives, supporting wider commercial use.

Foodservice and E-Commerce Delivery Growth

The expansion of takeaway, delivery, and online food ordering continues to raise demand for durable, grease-resistant, and microwave-safe disposable containers. Meal trays made from bagasse and PLA-lined materials meet performance requirements without compromising sustainability guidelines.

High-growth markets such as the U.S., the U.K., China, and India show accelerated adoption of compostable trays due to rising delivery volumes, dense urban populations, and strong restaurant and cloud-kitchen ecosystems. Operators seeking to align with sustainability targets increasingly prioritize biodegradable trays for menu items that require compartmentalization or reheating.

Barrier Analysis - Feedstock Price Volatility and Supply Constraints

Key raw materials, including bagasse, paperboard, PLA, and agricultural fiber residues, experience price fluctuations influenced by crop yields, competitive demand from pulp and biopolymer markets, and transportation costs. A shortfall in sugarcane harvests or disruptions in trade routes can raise feedstock costs substantially, compressing margins for manufacturers operating on tight cost structures.

When feedstock inflation exceeds typical procurement budgets, end users, especially price-sensitive foodservice operators, may delay transitions from plastic to biodegradable alternatives. Margin pressure can range from two to six percentage points during volatile cycles unless producers secure long-term supply agreements or vertically integrate upstream.

End-Of-Life Infrastructure Gaps and Certification Confusion

The environmental benefits of biodegradable trays rely on access to industrial composting and organic-waste collection systems. Regions with limited infrastructure or unclear municipal guidelines often face challenges in processing these products.

Confusion over terms like “biodegradable,” “compostable,” and “home-compostable,” along with inconsistent labeling or lack of third-party certification, can hinder adoption. In areas with inadequate composting capacity, uptake of biodegradable trays may lag by over a year compared to regions with established waste-diversion programs.

Opportunity Analysis - Expansion into Industrial Composting and Extended Producer-Responsibility (EPR) Solutions

Manufacturers can strengthen their market position by integrating waste-collection and composting services into their product offerings. Firms that partner with municipalities or private composters can provide end-to-end solutions that simplify compliance for large customers.

Even if 10–15% of tray volume enters service-linked composting programs, providers can unlock premium pricing and capture recurring service revenue. Hospitals, universities, and hospitality chains increasingly seek verifiable end-of-life pathways, creating room for new business models centered on take-back logistics, composting verification, and closed-loop sustainability reporting.

Premiumization of Microwaveable and Multi-Compartment Trays

High-performance biodegradable trays featuring multi-compartment structures, grease-resistant linings, and microwave-safe designs offer strong revenue potential. These products serve the fast-growing segments of meal-kit services, institutional catering, airline and rail catering, and premium delivery platforms.

Multi-compartment trays command price premiums typically ranging from 15% to 40%, depending on barrier properties and certifications. As consumer expectations shift toward convenience and meal presentation, demand for specialized biodegradable trays is rising globally. Manufacturers who invest in high-barrier compostable linings and advanced forming technologies are well-positioned to capture early share.

Category-wise Analysis

Material Insights

Bagasse is anticipated to dominate the market, holding a market share of 41.8% due to its wide availability, cost-effectiveness, and suitability for high-volume manufacturing.

As a by-product of sugar processing, bagasse benefits from consistent feedstock availability in major agricultural economies such as India, Brazil, and Thailand. Its thermal stability, rigidity, and natural grease resistance make it ideal for ovenable and microwave-safe trays used in quick-service restaurants, airline catering, and institutional settings.

Producers such as Huhtamaki, Genpak, and Pactiv Evergreen rely heavily on bagasse to meet procurement standards that emphasize durability, compostability, and food-contact safety for large catering contracts.

Government-backed procurement programs, such as India’s ban on certain single-use plastics and Brazil’s municipal composting initiatives, have strengthened demand further. The combination of scalability, predictable pricing, and broad regulatory acceptance enables bagasse to maintain long-term leadership in the material segment.

Bamboo represents the most rapidly expanding material category, driven by its premium aesthetic and growing consumer preference for minimally processed natural fibers. Bamboo fiber trays are seeing strong adoption in high-end hospitality, eco-conscious retail food chains, and luxury airlines that are repositioning their in-flight meals toward sustainable packaging.

Brands such as Pret A Manger, Marriott International, and certain wellness-focused cloud kitchens have begun piloting bamboo trays for salads, ready meals, and chef-curated menus. Bamboo’s fast regrowth rate and low environmental footprint align well with stringent compostability and renewable-material benchmarks in Europe, North America, and advanced Asian markets such as Japan and South Korea.

Compartment Insights

Single-compartment trays are expected to account for 47.4%market share, due to their widespread use in quick-service restaurants, institutional catering, and public meal-distribution programs. Their simple geometry supports lower production costs, efficient stackability, and high-speed thermoforming, traits valued by large buyers such as school meal programs, government nutrition schemes, and major workplace cafeterias.

QSR chains such as Subway, Domino’s, and regional tiffin delivery networks in India rely heavily on single-compartment trays because they accommodate fixed-portion menus and integrate easily with standard lids, sealing films, and automated filling lines. Their straightforward design also reduces material wastage and simplifies storage, reinforcing their position as the leading segment for high-volume service environments.

Multi-compartment trays are expanding at the fastest pace as foodservice operators focus on meal customization, improved presentation, and separated portioning. Meal-kit brands such as HelloFresh, Blue Apron, and FreshMenu increasingly use compartmentalized designs to keep sauces, proteins, and sides distinct during delivery.

Airlines and premium institutional kitchens are also shifting toward multi-compartment formats to elevate plating quality and portion consistency. These trays often require stronger forming characteristics, enhanced rigidity, and compatible high-barrier lids, allowing manufacturers to command higher margins.

Growth momentum is strongest in Europe and North America, where convenience-driven purchasing and premium delivery services are expanding rapidly. Urban markets in Asia Pacific, such as Singapore, Tokyo, and Seoul, are also adopting multi-compartment options as consumers embrace healthier meals and diversified food combinations.

Regional Insights

North America Biodegradable Meal Trays Market Trends - Institutional Adoption, Compostability Standards & Innovation-Led Fiber Expansion

North America remains one of the most commercially attractive regions for molded-fiber trays, supported by strong institutional adoption, rising sustainability commitments, and advanced product-innovation capabilities. Major foodservice distributors and national restaurant chains are accelerating the transition to certified compostable trays.

Sysco’s 2024 expansion of its Earth Plus molded-fiber line increased uptake across hospitals and universities, while procurement standards in healthcare, hospitality, education, and corporate foodservice continue to drive demand. Regulatory frameworks such as ASTM D6400, ASTM D6868, and FDA food-contact guidelines further strengthen market credibility and compliance.

Manufacturers in the U.S. are expanding capacity to meet growing requirements for sustainable, high-performance trays. Huhtamaki’s 2023 investment in its Kansas molded-fiber facility reinforced domestic supply for major restaurant chains, while Footprint introduced new fiber-based ready-meal trays adopted by retailers such as Conagra Brands.

These developments reflect the region’s focus on scalability, reliability, and product performance as key competitive advantages in sustainable packaging.

North America’s market growth is also supported by corporate sustainability goals and advancements in recycling and organic-waste recovery. Restaurant chains such as Chipotle continue prioritizing compostable, plant-based serviceware, further boosting demand. Innovation momentum remains strong, with PulPac partnering with regional converters to expand dry-molded fiber technology, enabling water-efficient, next-generation tray production.

Recent initiatives, including Cruise LLC and Rubicon’s 2024 organic-waste pilot programs and the launch of Renewable Packaging Solutions’ fiber-forming facility in South Carolina, underscore the region’s shift toward an innovation-driven, infrastructure-supported growth model.

Europe Biodegradable Meal Trays Market Trends - Regulation-Driven Compostable Procurement & Advanced Fiber-Barriers Growth

Europe is anticipated to hold the largest market share at 38.2%, driven by early adoption of sustainability regulations and well-developed organic-waste infrastructure. The EU Single-Use Plastics Directive and national packaging laws have made biodegradable trays a preferred option for institutional procurement.

Mature composting systems across key countries support consistent use of certified compostable trays in hospitality, retail foodservice, and public-sector tenders. Many governments have also established procurement pathways that explicitly favor molded-fiber serviceware, accelerating regional adoption.

Germany leads the region with extensive industrial composting capacity and stringent compliance rules that support compostable trays in hospitals, universities, and corporate catering. Producers such as Bio Futura and GreenBox have expanded certified compostable product lines to meet public-sector demand.

In the U.K., companies such as Vegware and Sabert UK operate closed-loop composting partnerships with processors such as Envar and Paper Round, enabling large hospitality operators and event venues to adopt trays with verifiable end-of-life management.

Regulatory clarity, strong consumer preference for sustainable packaging, and strict enforcement of compostability standards remain key growth drivers. Investment momentum is rising, with Stora Enso expanding molded-fiber capacity in Sweden and Huhtamaki introducing advanced bio-barrier coatings for microwaveable and ovenable trays.

Emerging opportunities include home-compostable formats, waste-processor partnerships, and fiber solutions for airline catering and premium ready-meal categories.

Asia Pacific Biodegradable Meal Trays Market Trends - High-Volume Fiber Manufacturing, Policy Acceleration & Export-Led Expansion

Asia Pacific is projected to be the fastest-growing region, supported by abundant feedstock availability, expanding foodservice operations, and rapid policy transitions toward sustainable materials. The region’s competitive manufacturing base allows producers to scale quickly and serve global markets.

For example, Yash Pakka (India) expanded its Chhattisgarh molded-fiber facility in 2024, significantly boosting exports to Europe and the Middle East. China maintains one of the world’s largest biodegradable tableware manufacturing ecosystems.

Companies such as Xiamen Wei Mon Environmental Materials and Zhiben are developing high-strength molded-fiber trays for ready meals sold through retail platforms such as Alibaba’s Freshippo. Policy incentives under China’s 2025 green-packaging standards continue to push producers toward compostable and plastic-free alternatives.

India’s domestic ecosystem has grown rapidly; brands such as Chuk supply biodegradable trays to quick-service restaurants, corporate canteens, and airlines, while government initiatives such as the national single-use plastics phaseout stimulate further adoption.

Thailand’s TPLAS expanded its production of molded-fiber trays dedicated to airline and retail meal applications, while Indonesia has seen new joint ventures between sugar mills and packaging companies to supply high-volume bagasse. Producers across Asia-Pacific are increasingly supplying certified compostable trays to Europe, North America, and the Middle East, strengthening the region’s role as a global manufacturing hub.

Competitive Landscape

The global biodegradable meal trays market is moderately consolidated, characterized by a mix of large multinational manufacturers and numerous regional producers. Global leaders maintain advantages in molded-fiber capacity, automated forming technology, and international distribution networks.

Regional players often compete through material specialization, localized feedstock access, and flexible production tailored to small and mid-size customers. Market structure varies by region: North America favors larger manufacturers due to large institutional buyers, while Europe supports a more diverse ecosystem connected to composting services and localized sustainability initiatives.

Market leaders prioritize innovation in fiber-forming, PLA/PHA barrier technologies, and supply-chain integration to stabilize feedstock availability. Companies increasingly bundle composting partnerships, certification compliance, and waste-management solutions to differentiate offerings. Strategic themes include cost optimization, product premiumization, and market expansion into high-growth regions.

Key Industry Developments

- In June 2025, Pulpcraft showcased its latest bagasse-based compostable trays and 5-compartment meal trays at Biodegradable Expo 2025 in India, demonstrating innovation in high-function, fully biodegradable tableware for foodservice and delivery markets.

Companies Covered in Biodegradable Meal Trays Market

- Huhtamaki

- Stora Enso

- Vegware

- Sabert Corporation

- Yash Pakka (CHUK)

- Bio Futura

- GreenGood

- Genpak

- Pactiv Evergreen

- Biotrem

- Eco-Products

- Fabri-Kal

- Good Start Packaging

- Packnwood

- Bionatic

- Detpak

- Zhiben

- Xiamen Wei Mon Environmental Materials

- Lollicup Eco Products

- Papstar

Frequently Asked Questions

The global biodegradable meal trays market is estimated to reach US$1.7 billion in 2026.

By 2033, the biodegradable meal trays market is projected to reach US$3.4 billion.

Key trends include the rapid transition toward compostable and fiber-based food packaging, expansion of molded-fiber production capacity, adoption of dry-molded fiber technologies, and growth of certified compostable products.

The bagasse material segment leads with 41.8% market share, supported by abundant feedstock and cost-efficient production.

The biodegradable meal trays market is expected to grow at a CAGR of 10.2% between 2026 and 2033.

Major companies with strong portfolios in molded-fiber and compostable meal trays include Huhtamaki, Stora Enso, Vegware, Yash Pakka/CHUK, and Sabert Corporation.