- Medical Devices

- Biodegradable Dressings Market

Biodegradable Dressings Market Size, Share, and Growth Forecast 2026 - 2033

Biodegradable Dressings Market by Product Type (Hydrocolloid, Alginate, Hydrogel, Foam, Film, Collagen / Chitosan–based, Others), by Application (Chronic wounds, Acute wounds, Surgical wounds, Burns, Others), by End User (Hospitals, Clinics, Ambulatory surgical centers, Home care, Others), by Regional Analysis, 2026-2033

Biodegradable Dressings Market Share and Trends Analysis

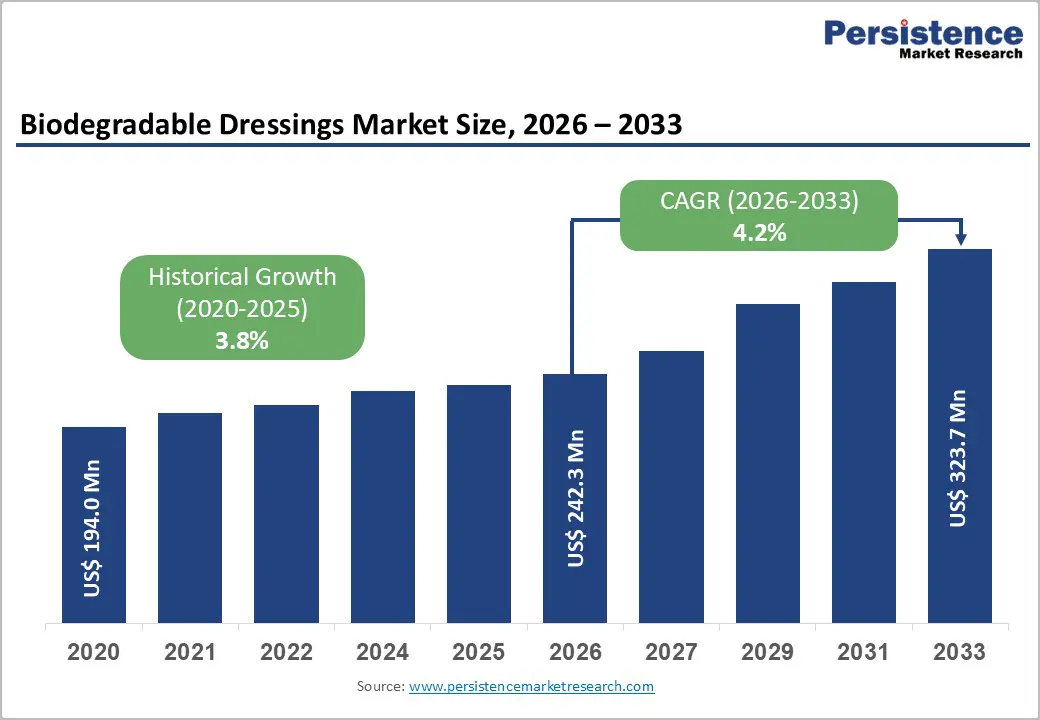

The global biodegradable dressings market size is expected to be valued at US$ 242.3 million in 2026 and projected to reach US$ 323.7 million by 2033, growing at a CAGR of 4.2% between 2026 and 2033.

The market expansion is primarily driven by the increasing global prevalence of chronic wounds coupled with rising healthcare sustainability mandates across developed and emerging economies. According to the National Institutes of Health (NIH), chronic wounds affect approximately 6.5 million patients in the United States alone, with treatment costs exceeding US$ 25 billion annually. The growing elderly population, expected to surpass 94.7 million in the United States by 2060 as per government estimates, combined with the escalating diabetes epidemic affecting over 537 million people globally as reported by the International Diabetes Foundation, is driving substantial demand for environmentally sustainable wound care solutions that offer superior healing outcomes while minimizing medical waste generation.

Key Market Highlights

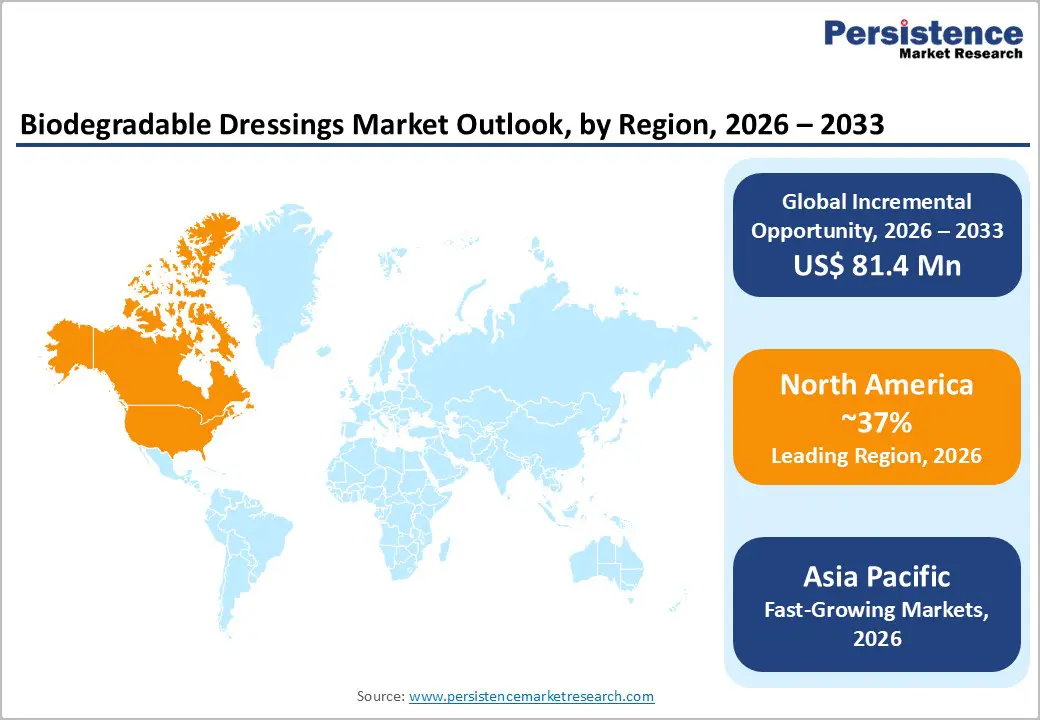

- North America maintains dominant regional leadership with 37% market share in 2025, driven by advanced healthcare infrastructure, comprehensive Medicare reimbursement coverage, stringent FDA regulatory frameworks supporting innovation, and substantial chronic wound burden affecting over 6.7 million Americans annually according to CDC data.

- Asia Pacific demonstrates the fastest regional growth trajectory through 2033, propelled by massive population demographics exceeding 1 billion elderly by 2050, escalating diabetes prevalence affecting 74 million patients in India alone, healthcare infrastructure modernization across China, Japan, and South Korea, and supportive regulatory reforms accelerating biodegradable medical device approvals.

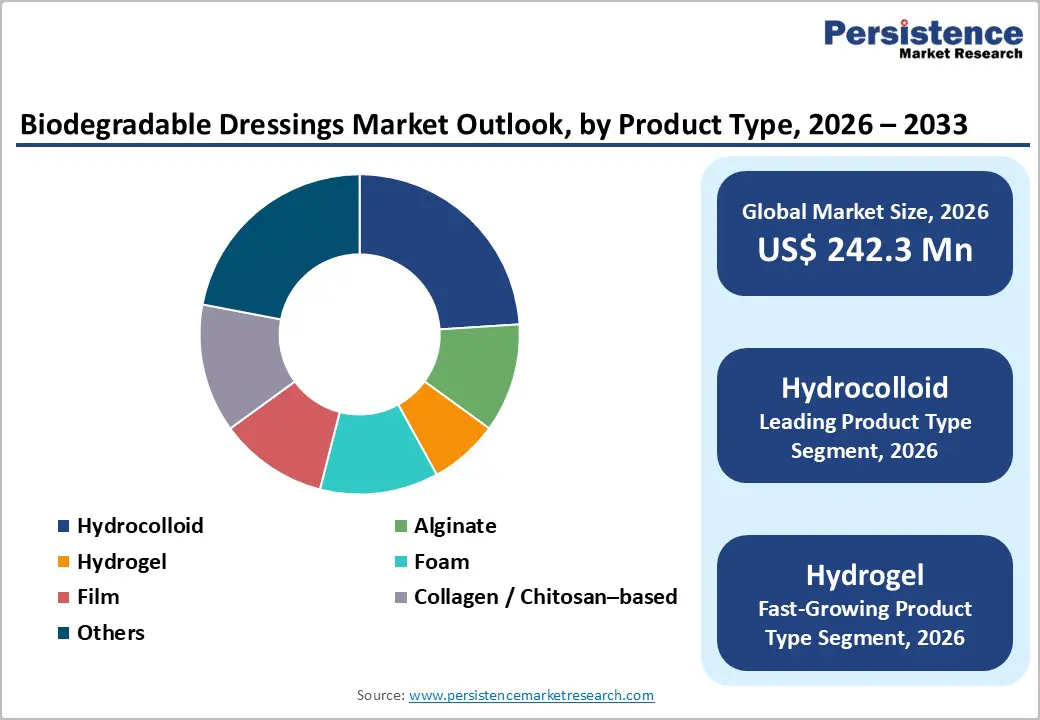

- Hydrocolloid dressings dominate the product-type segmentation, with a 24% market share in 2025, attributable to established clinical efficacy demonstrated in NIH studies (84.8% positive physician-assessed outcomes), superior moisture-management properties, and widespread familiarity among healthcare providers across hospital and home care settings globally.

- Rapid home healthcare expansion presents transformative growth opportunities, with portable biodegradable dressing platforms supported by Medicare reimbursement policies, integrated telehealth monitoring systems developed by innovators including Niramai and Tricog, and aging population preferences for cost-effective home-based chronic wound management solutions avoiding institutional care settings.

| Global Market Attributes | Key Insights |

|---|---|

| Biodegradable Dressings Market Size (2026E) | US$ 242.3 million |

| Market Value Forecast (2033F) | US$ 323.7 million |

| Projected Growth CAGR (2026-2033) | 4.2% |

| Historical Market Growth (2020-2025) | 3.8% |

Market Dynamics

Market Growth Drivers

Escalating Chronic Wound Burden Driven by Aging Demographics and Diabetes Epidemic

The rapidly expanding global burden of chronic wounds represents the most significant driver for biodegradable dressings adoption across healthcare systems worldwide. According to the United Nations Department of Economic and Social Affairs, the population aged 65 years and older in the Asia Pacific region alone is projected to exceed 1 billion by 2050, doubling from 2020 levels. This demographic transition directly correlates with elevated chronic wound incidence, as 3% of the population older than 65 years in the United States currently experience open wounds according to NIH studies. The Indian Council of Medical Research reports that over 74 million people in India live with diabetes, with a significant proportion developing diabetic foot ulcers requiring advanced wound care. The International Diabetes Foundation estimates that 40 to 60 million people globally are affected by diabetic foot ulcers, with 19% to 34% of diabetic patients developing foot ulcers during their lifetime. Biodegradable dressings manufactured from natural polymers including alginate, chitosan, collagen, and cellulose provide superior moisture management, reduced infection rates, and enhanced healing outcomes compared to conventional synthetic alternatives, positioning them as essential solutions for managing this growing patient population.

Stringent Environmental Regulations Accelerating Sustainable Healthcare Practices

Healthcare facilities worldwide are intensifying adoption of biodegradable wound care solutions in response to increasingly stringent environmental regulations and institutional sustainability commitments. The European Union's Medical Device Regulation (MDR) emphasizes environmental considerations throughout the medical device lifecycle, mandating manufacturers to assess packaging and material biodegradability. The European Union Packaging and Packaging Waste Regulation (EU) 2025/40, published in January 2025 and applicable from August 2026, establishes comprehensive recyclability requirements with mandatory Design for Recycling criteria, compelling medical device manufacturers to transition toward biodegradable alternatives. Germany's Dual System and green dot certification program requires manufacturers to demonstrate packaging recovery and recycling compliance, creating strong market pull for biodegradable dressing materials. According to industry analysis, hospitals and healthcare facilities rank among the largest medical waste producers globally, with disposable wound dressings representing a substantial waste stream component. The ANIPH Project (Avoiding the Negative Impacts produced by Plastic materials in Humanitarian contexts), a four-year European initiative, is specifically developing PHA-based biopolymer wound dressings that fully degrade in soil, freshwater, and marine environments without generating microplastic pollution, demonstrating regulatory and research alignment toward sustainable wound care paradigms.

Market Restraints

Premium Pricing and Cost Constraints in Price-Sensitive Healthcare Systems

The substantially higher manufacturing costs associated with biodegradable dressing materials compared to conventional synthetic alternatives represent a significant market restraint, particularly in emerging economies and price-sensitive healthcare environments. Bio-based natural polymers including alginate derived from seaweed, chitosan extracted from crustacean shells, and collagen sourced from animal tissues require sophisticated extraction and processing methodologies that elevate production expenses. Healthcare facilities operating under stringent budget constraints and reimbursement limitations frequently prioritize cost-effectiveness over environmental sustainability, resulting in continued preference for conventional gauze and synthetic dressings. Long-term care facilities, which maintain price-conscious procurement strategies, predominantly rely on prophylactic foam dressings rather than transitioning to higher-cost biodegradable alternatives. This cost sensitivity is particularly pronounced in developing regions including parts of Asia, Latin America, and Africa, where healthcare infrastructure limitations and resource constraints restrict access to premium wound care technologies despite growing clinical needs.

Complex Regulatory Approval Pathways and Material Standardization Challenges

The biodegradable dressings market confronts significant regulatory and standardization challenges that impede accelerated market penetration across global healthcare systems. Innovative biodegradable materials require extensive clinical validation and regulatory approval processes to demonstrate biocompatibility, safety, efficacy, and predictable degradation profiles. The U.S. Food and Drug Administration (FDA) mandates rigorous premarket notification and approval procedures for novel wound care devices, requiring comprehensive biocompatibility testing, sterility validation, and clinical performance documentation. The European Union's Medical Device Directive 93/42/EEC and subsequent regulations establish strict quality system requirements including ISO 13485 certification for design, manufacture, and final product testing. Storage stability limitations, variable degradation rates under different environmental conditions, and shelf-life considerations introduce additional complexity for manufacturers seeking to standardize biodegradable dressing products across diverse geographic markets with varying regulatory frameworks and clinical practice protocols.

Market Opportunities

Rapid Expansion of Home Healthcare and Ambulatory Care Settings

The accelerating shift toward home healthcare delivery models and ambulatory surgical centers presents substantial growth opportunities for biodegradable dressing manufacturers to expand market reach beyond traditional hospital settings. According to market analysis, the home healthcare end-user segment is projected to demonstrate the fastest growth trajectory during the forecast period, driven by aging populations preferring home-based care solutions and Medicare reimbursement policies supporting portable therapy platforms for chronic wound management. The Australian Institute of Health and Welfare reports continued growth in home healthcare service utilization, reflecting global trends toward decentralized care delivery. Biodegradable dressings offer particular advantages for home care applications through reduced dressing change frequency, simplified application protocols, and elimination of specialized disposal requirements associated with conventional synthetic alternatives. Ambulatory surgical centers, which performed substantial portions of outpatient procedures across developed markets, increasingly adopt advanced wound care solutions to minimize post-operative complications and hospital readmissions. The portability and user-friendly characteristics of modern biodegradable dressing formulations, combined with integrated telehealth monitoring platforms enabling remote wound assessment, position these products optimally for the expanding home healthcare ecosystem that prioritizes patient convenience, clinical effectiveness, and environmental responsibility.

Category-wise Insights

Product Type Analysis

Hydrocolloid dressings hold the leading position in the biodegradable dressings market, capturing approximately 24% market share in 2025, attributable to their established clinical efficacy, versatility across multiple wound types, and favorable reimbursement landscapes in developed healthcare markets. These dressings, manufactured from gel-forming agents such as carboxymethylcellulose (CMC) and gelatin, create occlusive, moisture-retentive environments that accelerate wound healing while providing bacterial impermeability. Clinical research published in the International Wound Journal demonstrates that chitosan-based hydrocolloid dressings achieve statistically significant improvements in chronic refractory wound healing compared to conventional gauze, with substantial reductions in pain scores, itching frequency, and dressing change requirements. According to PubMed studies involving 33 vascular outpatients, hydrocolloid dressing application resulted in significant quality of life improvements across all measured parameters including pain reduction, increased independence in daily activities, and improved sleep quality, with physician assessments indicating positive outcomes in 84.8% of cases. The proven clinical performance, combined with patient comfort advantages and healthcare provider familiarity, sustains the dominant market position of hydrocolloid biodegradable dressings across hospital, clinic, and home care settings globally.

End User Analysis

Hospitals maintain a leading position among end-user segments, commanding the largest market share by serving as primary treatment venues for complex acute and chronic wounds that require advanced medical interventions and specialized nursing care. Healthcare facility analysis indicates that hospitals account for approximately 36% to 48% of advanced wound care product consumption globally, driven by elevated patient admission rates for pressure ulcers, diabetic foot ulcers, surgical site infections, and burn treatments. The dominance of hospital settings reflects several structural advantages, including availability of multidisciplinary wound care teams, access to comprehensive diagnostic and treatment technologies, established procurement relationships with medical device suppliers through long-term institutional contracts, and implementation of evidence-based clinical protocols. Hospital institutions demonstrate particular preference for biodegradable dressings in managing surgical wounds and complex trauma cases where infection prevention and accelerated healing directly impact patient outcomes, length of stay, and readmission rates. The Korean Society of Plastic and Reconstructive Surgeons reports that adoption of allogeneic skin substitutes in South Korean hospitals increased by 35% between 2019 and 2023, particularly for post-surgical and burn care applications. Furthermore, hospitals serve as innovation adoption centers where emerging biodegradable technologies undergo clinical validation before diffusing to ambulatory and home care settings, reinforcing their central role in market development and product acceptance across the wound care continuum.

Regional Insights

North America Biodegradable Dressings Market Trends and Insights

North America maintains market leadership with approximately 37% market share in 2025, underpinned by advanced healthcare infrastructure, comprehensive insurance coverage, established reimbursement frameworks, and strong regulatory support for innovative medical technologies. The United States dominates regional growth through substantial federal healthcare investments, with the U.S. Food and Drug Administration (FDA) actively streamlining approval pathways for antimicrobial and bioactive dressing formulations. According to the Centers for Disease Control and Prevention (CDC), more than 6.7 million Americans suffer from chronic wounds annually, generating sustained demand for advanced wound care solutions.

The Agency for Healthcare Research and Quality highlights that pressure ulcer treatment costs range from US$ 9.1 billion to US$ 11.6 billion annually in the United States, creating compelling economic incentives for adopting biodegradable dressings that demonstrate superior healing outcomes and reduced complication rates. Medicare coverage expansion for wound care products, combined with bundled payment models rewarding interventions that minimize hospital readmissions, accelerates institutional adoption of premium biodegradable technologies. Major market participants including Smith & Nephew, 3M Company, and Medline Industries maintain substantial North American operations with extensive distribution networks serving hospitals, ambulatory surgical centers, and home healthcare providers. Recent industry developments include Medline Industries' December 2024 acquisition of a digital wound care platform enhancing analytical capabilities for outpatient settings, demonstrating ongoing

Asia Pacific Biodegradable Dressings Market Trends and Insights

Asia-Pacific emerges as the fastest-growing regional market for biodegradable dressings, driven by large populations, rising diabetes prevalence, modernization of healthcare infrastructure, and increasing disposable incomes that support the adoption of premium medical products. India demonstrates particularly robust growth potential with the Indian Council of Medical Research reporting over 74 million diabetic patients, many developing foot ulcers requiring advanced wound management. The Central Drugs Standard Control Organization has shortened approval timelines for wound biologics, encouraging domestic manufacturers, including Aegis Lifesciences Pvt Ltd and international players, to scale operations. Indigenous companies such as BioMeTushya and Stempeutics launched locally-produced stem cell-based wound healing products aligned with national health priorities.

Competitive Landscape

The global biodegradable dressings market exhibits a moderately consolidated competitive structure characterized by the presence of established multinational medical device corporations commanding significant market shares alongside emerging regional players and specialized biotechnology firms pursuing innovative material technologies. Strategic initiatives focus on product line expansion through acquisitions, partnerships with biotechnology innovators, vertical integration of manufacturing capabilities, and geographic market penetration particularly targeting high-growth emerging economies. Differentiation strategies emphasize advanced biomaterial integration, antimicrobial functionality enhancements, smart monitoring technology incorporation, and clinical evidence generation demonstrating superior healing outcomes and cost-effectiveness.

Key Market Developments

- In November 2025, the Department of Atomic Energy and Cologenesis launched ColoNoX, India’s first nitric-oxide-releasing wound dressing for diabetic foot ulcers, after Phase II/III trials and regulatory approval, marking a new advanced treatment option.

Companies Covered in Biodegradable Dressings Market

- Smith & Nephew plc

- 3M Company

- Mölnlycke Health Care AB

- Coloplast A/S

- ConvaTec Group plc

- Medline Industries, Inc.

- Baxter International Inc.

- Medtronic plc

- Stryker Corporation

- BenQ Materials Corp.

- Aegis Lifesciences Pvt Ltd.

- Hangzhou Singclean Medical Product Co., Ltd.

- Cardinal Health Inc.

- B. Braun SE

- Johnson & Johnson (Ethicon)

- Paul Hartmann AG

- Integra LifeSciences Holdings Corporation

- Derma Sciences Inc.

- MiMedx Group Inc.

- PolyNovo Limited

- Zoragen Biotechnologies

- Kerecis

- mediWound Ltd

- BioMeTushya

- Stempeutics

Frequently Asked Questions

The global biodegradable dressings market is expected to be valued at US$ 242.3 million in 2026.

The market is primarily driven by the escalating global burden of chronic wounds affecting over 6.5 million patients in the United States alone according to NIH data, coupled with the aging population projected to exceed 94.7 million by 2060 domestically and 1 billion in Asia Pacific by 2050.

North America maintains regional market leadership with approximately 37% market share in 2025, attributed to advanced healthcare infrastructure, comprehensive Medicare reimbursement frameworks, strong FDA regulatory support for innovative medical technologies, substantial chronic wound burden exceeding 10.5 million Medicare beneficiaries, and institutional sustainability commitments driving biodegradable product procurement across hospital systems.

The rapid expansion of home healthcare delivery models presents the most significant growth opportunity, with the segment projected to demonstrate the fastest growth trajectory. This is driven by aging populations preferring home-based care, Medicare reimbursement policies supporting portable therapy platforms, integrated telehealth wound monitoring systems, and biodegradable dressings offering reduced change frequency and simplified disposal compared to conventional alternatives, positioning them optimally for the expanding decentralized care ecosystem.

Leading market participants include Smith & Nephew plc, 3M Company, Mölnlycke Health Care AB, Coloplast A/S, ConvaTec Group plc, Medline Industries, Inc., Baxter International Inc., Medtronic plc, and Stryker Corporation, complemented by emerging innovators including PolyNovo Limited, Zoragen Biotechnologies, Kerecis, mediWound Ltd, and regional players such as Aegis Lifesciences Pvt Ltd, BioMeTushya, and Stempeutics advancing biodegradable material technologies and expanding geographic market penetration through strategic partnerships and product innovation initiatives.