- Specialty & Fine Chemicals

- Barite Market

Barite Market Size, Share, and Growth Forecast 2026 - 2033

Barite Market by Grade (Up to Sp. Gr. 3.9, Sp. Gr. 4.0, Sp. Gr. 4.1, Sp. Gr. 4.2, Sp. Gr. 4.3 & Above), Application (Drilling Mud, Chemical Intermediate, Medical Imaging, Paints & Coatings, Rubber & Plastics, Others), and Regional Analysis (North America, Europe, East Asia, South Asia and Oceania, Latin America, Middle East & Africa), 2026 - 2033

Barite Market Size and Trend Analysis

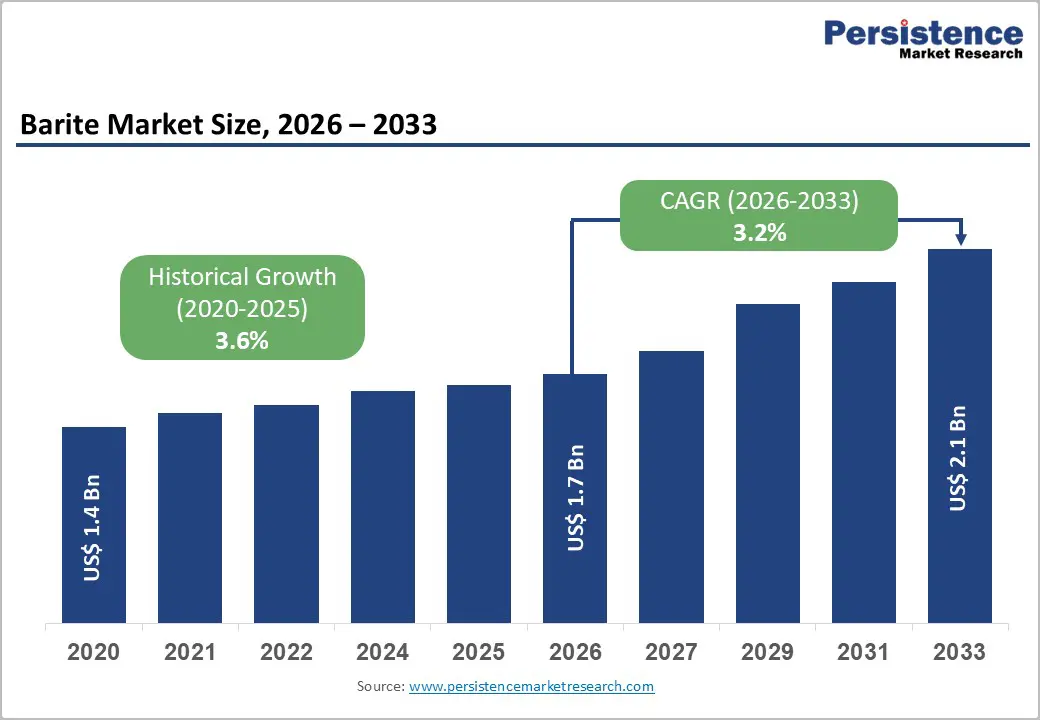

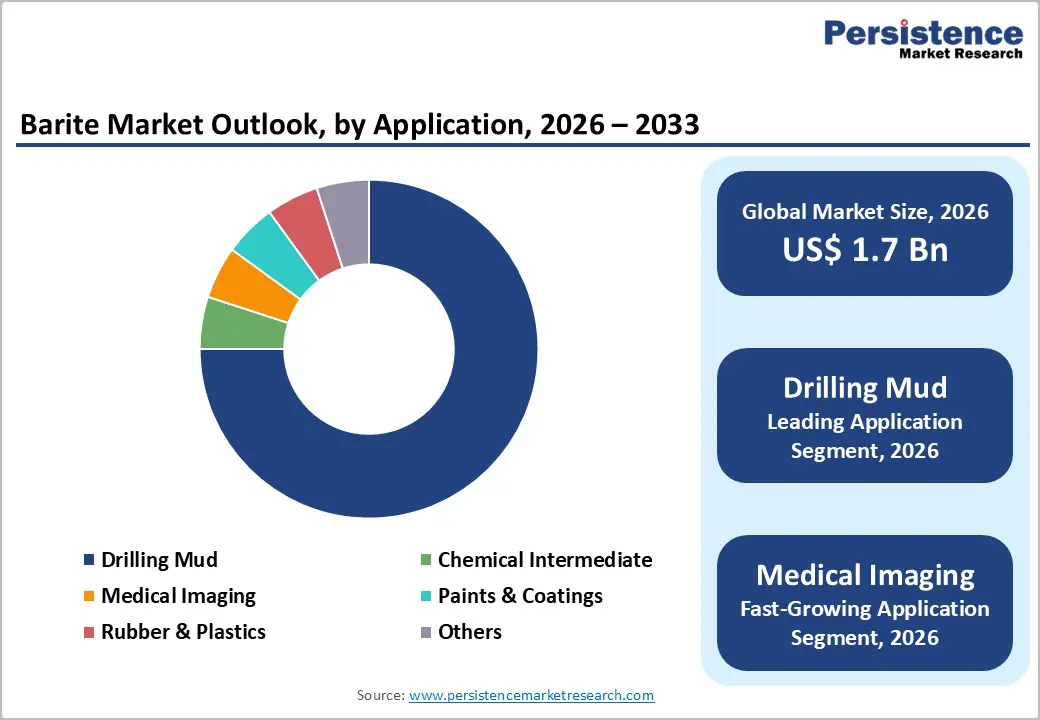

The global Barite market size is expected to be valued at US$ 1.7 billion in 2026 and projected to reach US$ 2.1 billion by 2033, growing at a CAGR of 3.2% between 2026 and 2033. Sustained global oil and gas drilling activity, particularly across unconventional shale basins, deepwater projects, and high-pressure high-temperature (HPHT) environments, remains the cornerstone of barite demand, where the mineral serves as an indispensable weighting agent in drilling fluids, accounting for over 75% of total consumption.

Underpinned by the International Energy Agency (IEA) forecast of global oil demand growth of approximately 2.5 mb/d through 2030, reinforcing drilling investment cycles, barite consumption is further bolstered by expanding industrial applications in paints and coatings, rubber and plastics, and rapidly growing pharmaceutical-grade demand from the medical imaging segment across emerging healthcare markets in Asia and the Middle East.

Key Industry Highlights:

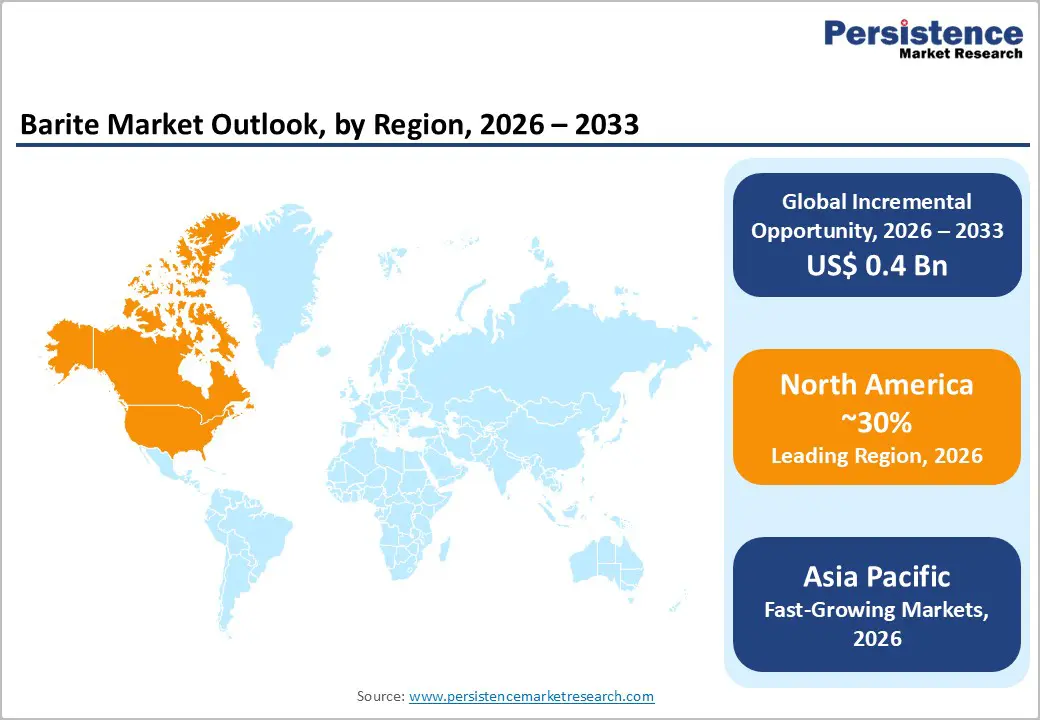

- Leading Region: North America leads the global Barite market, with the U.S. consuming over 2.2 million tons annually and representing the world's single largest import market, driven by structurally high unconventional shale drilling activity in the Permian Basin, Eagle Ford, and Bakken formations.

- Fastest Growing Region: Asia Pacific is the fastest growing regional market through 2033, led by India's accelerating oil exploration, healthcare expansion under Ayushman Bharat, and industrial manufacturing growth, alongside incremental demand from ASEAN construction and infrastructure development programs.

- Dominant Application Segment: Drilling mud dominates the global market with over 75% share in 2026, underpinned by the mineral's irreplaceable role as a wellbore pressure-control weighting agent in both water-based and oil-based drilling fluid systems across onshore, offshore, and HPHT drilling environments globally.

- Fastest Growing Segment: Medical imaging is the fastest growing application segment, driven by expanding diagnostic procedure volumes globally, aging demographics in developed markets, and rapid healthcare infrastructure scaling across India, Southeast Asia, and Africa, with pharmaceutical-grade barium sulfate commanding 5–8x price premiums over commodity drilling-grade barite.

- Key Opportunity: The key market opportunity lies in downstream value-added product development, pharmaceutical-grade barium sulfate for medical imaging, and barium chemical intermediates for specialty glass, ceramics, and advanced materials, offering producers significantly higher margins versus commodity drilling-grade sales while hedging against oil and gas drilling cycle volatility by 2033.

| Key Insights | Details |

|---|---|

|

Global Barite Market Size (2026E) |

US$ 1.7 Billion |

|

Projected Market Value (2033F) |

US$ 2.1 Billion |

|

Global Market Growth Rate (CAGR 2026–2033) |

3.2% |

|

Historical Market Growth Rate (CAGR 2020–2025) |

3.6% |

Market Dynamics and Trend Analysis

Drivers – Sustained Oil and Gas Drilling Activities Driving Core Demand

Barite demand is fundamentally tied to global drilling activity, with oil and gas applications accounting for over 75% of total consumption in 2026. According to Baker Hughes, the global rig count has remained broadly resilient, with the international rig count (excluding the U.S.) averaging 1,169 active rigs in late 2024 per U.S. Geological Survey (USGS) data, signaling sustained drilling momentum across Middle Eastern, Latin American, and Asian markets.

The IEA's World Energy Outlook 2024 projects global oil demand to rise to approximately 103.8 mb/d by 2030, necessitating continuous upstream investment and well completions. In the United States, the Permian Basin alone accounts for approximately 47% of total U.S. crude oil output, with horizontal drilling and multi-stage fracturing intensifying per-well barite consumption. Deepwater and ultra-deepwater projects in the Gulf of Mexico, Brazil, Guyana, and West Africa require high-density drilling fluids capable of maintaining wellbore integrity at water depths exceeding 2,500 meters and bottom-hole temperatures above 200°C, directly driving demand for API 13A-specification Sp. Gr. 4.2 barite.

Expansion of Unconventional Oil and Gas Resources

The accelerating development of unconventional hydrocarbon resources, including shale gas, tight oil, and deepwater reserves, is intensifying per-well barite consumption requirements globally. According to the U.S. Energy Information Administration (EIA), U.S. crude oil production is projected to peak near 13.5 million barrels per day around 2027, sustaining structural demand for API-specification drilling-grade barite across Permian Basin, Eagle Ford, and Bakken shale formations. Ultra-deepwater projects offshore Brazil, Mexico, and Guyana, where Exxon Mobil, Hess Corporation, and Petroleo Brasileiro S.A. (Petrobras) are active operators, require drilling fluids engineered with barite to achieve mud densities up to 2,400 kg/m³ while maintaining chemical stability under extreme HPHT conditions. Horizontal drilling and multi-stage hydraulic fracturing technologies have progressively increased the barite loading per well, particularly in North American shale basins and Middle Eastern carbonate reservoirs, structurally amplifying demand per unit of hydrocarbon output compared to conventional vertical well drilling.

Growing Industrial Applications Beyond the Energy Sector

Barite consumption in industrial applications continues to expand, with the paints and coatings segment registering robust growth driven by accelerating construction activity, infrastructure development, and automotive production across Asia Pacific and Middle Eastern economies. The mineral's chemical inertness, high specific gravity, and low oil absorption properties make it a highly effective functional filler and extender, enabling manufacturers to partially replace expensive titanium dioxide (TiO2) while maintaining coating performance metrics, including opacity, brightness, and film durability. The Asia-Pacific Coatings Journal and European Coatings Journal document consistent demand expansion in industrial protective and marine coatings, segments growing alongside offshore energy infrastructure buildout. The rubber and plastics segment also benefits from barite's role as a cost-effective high-density filler in automotive soundproofing, vibration-damping compounds, and high-performance polymer composites, with the global automotive industry's recovery post-2023 semiconductor shortage providing incremental uplift to industrial-grade barite consumption through the forecast period.

Restraints - Supply Chain Vulnerabilities and Geopolitical Dependencies

The global barite market faces significant supply chain challenges stemming from concentrated production sources and geopolitical dependencies. The U.S., despite being the world's largest barite consumer with annual demand exceeding 2.2 million tons, satisfies only approximately 15% of requirements through domestic production, primarily from Nevada and Georgia, rendering it heavily dependent on imports, principally from China, India, and Morocco. According to the U.S. Geological Survey (USGS) Mineral Commodity Summaries 2024, China remains the world's dominant barite producer, accounting for approximately 30–35% of global supply. The 2024 U.S.-China trade tensions, freight cost escalation following Red Sea shipping disruptions, and port congestion created measurable supply chain disruption for domestic drilling operations. Transportation costs represent 25–40% of delivered barite pricing, making logistics efficiency a critical competitive parameter and structural barrier to geographic supply diversification.

Environmental Regulations and Mining Constraints

Increasing environmental regulations surrounding barite mining operations present persistent operational challenges and cost pressures across producing regions. Concerns about sulfate contamination in groundwater, waste rock disposal, and land disturbance are driving stricter permitting requirements, particularly in China, the European Union, and India. In China, which accounts for approximately 42% of global production but only 9.25% of known global reserves per USGS data, accelerating depletion of high-grade, easily accessible deposits is forcing a structural shift toward lower-grade, more complex ores requiring intensive beneficiation that increases production costs by 15–25%. China's Ministry of Natural Resources tightened mining permits for barite between 2023 and 2025, reducing the number of operating mines and compressing domestic supply availability. Stringent environmental regulations can increase overall production costs by 10–20%, disproportionately impacting smaller regional producers and contributing to gradual market consolidation.

Opportunity - Medical Imaging and Healthcare Applications Growth

The medical imaging segment represents a compelling high-growth, high-margin opportunity for barite producers, with pharmaceutical-grade barium sulfate experiencing rising demand as a radiocontrast agent in gastrointestinal diagnostics globally. Barite's exceptional radiopacity, underpinned by barium's high atomic number of 56, makes it irreplaceable in X-ray, fluoroscopy, and CT examinations, diagnosing gastroesophageal reflux, peptic ulcers, and colorectal disorders.

According to the World Health Organization (WHO), global diagnostic imaging procedure volumes are growing at approximately 4.5% annually, driven by aging populations in Europe, Japan, and North America, combined with rapid expansion of secondary and tertiary healthcare infrastructure across India, Southeast Asia, and Africa. The Government of India's Ayushman Bharat Pradhan Mantri Jan Arogya Yojana (PM-JAY) scheme, covering over 500 million citizens under public health insurance, is accelerating diagnostic imaging center proliferation across Tier-2 and Tier-3 cities, creating a structural expansion in pharmaceutical-grade barite demand. Medical-grade barium sulfate commands premium pricing 5–8x commodity drilling-grade barite, offering producers a significant margin enhancement opportunity through downstream product upgrading.

Chemical Intermediate Applications and Value-Added Products

Barite serves as the primary feedstock for producing a range of high-value barium compounds, including barium carbonate (BaCO3), barium chloride (BaCl2), barium hydroxide [Ba(OH)2], and barium sulfide (BaS), which find extensive application in specialty glass manufacturing, ceramic glazes, pyrotechnics, and electronic materials. The global specialty glass market, encompassing CRT substrates, optical glass, and radiation-shielding glass for nuclear and medical facilities, is driving demand for high-purity barium carbonate as a flux and stabilizer.

The emerging battery materials sector presents a nascent opportunity: barium compounds are under active investigation as electrolyte additives for solid-state and next-generation lithium-ion batteries, as documented in research published in the Journal of Power Sources and ACS Applied Materials & Interfaces. Through carbothermal reduction processes, barite is converted to barium sulfide, serving as the starting material for high-value barium chemicals used in lubricating greases, flame retardants, and PVC heat stabilizers, all registering steady demand growth within the global specialty chemicals industry. These downstream chemical applications offer barite producers meaningful diversification from drilling cycle volatility and structurally higher margins than commodity drilling-grade sales.

Category-wise Analysis

By Grade Insights

The specific gravity 4.2 grade commands the dominant market position, holding over 35% market share in 2026, driven by its status as the American Petroleum Institute (API) 13A specification standard for drilling-grade barite. This classification, mandating a minimum specific gravity of 4.20, maximum soluble alkaline earth metals of 250 mg/kg, and maximum residue on a 75-micron sieve of 3.0%, is the globally accepted benchmark for oilfield applications. Major oilfield services companies, including Halliburton, SLB (formerly Schlumberger), and Baker Hughes, specify Sp. Gr. 4.2 barite for virtually all onshore and offshore drilling operations globally. Pure barium sulfate possesses a theoretical specific gravity of 4.5, and the 4.2 grade reflects the commercially achievable purity level in beneficiated barite concentrates from major producing countries. The API's longstanding acceptance of this grade as the industry benchmark, combined with abundant global supply from China, India, Morocco, and Nevada (U.S.), ensures its continued market leadership through the 2033 forecast horizon.

The Sp. Gr. 4.1 grade has emerged as the fastest-growing segment in the barite market, gaining sustained commercial traction following the American Petroleum Institute's 2010 approval of alternate specifications permitting this lower density grade in non-critical drilling operations. The acceptance of 4.1-grade barite has enabled producers to utilize lower-grade ore deposits, previously lacking commercial viability under stricter specifications, thereby meaningfully expanding global supply capacity and creating additional sourcing flexibility for drilling contractors. While initially adopted for routine non-critical operations, improved drilling fluid formulation technologies incorporating polymer stabilizers and weighting agent blends have progressively broadened Sp. Gr. 4.1 Barite's application scope. The grade offers cost advantages of 10–15% compared to standard 4.2 material, making it increasingly attractive to cost-conscious operators in mature basin drilling where HPHT conditions do not mandate maximum-density fluids.

By Application

Drilling mud applications represent the dominant and structural demand driver of the global barite market, accounting for over 75% market share in 2026. This commanding dominance stems from barite's unique combination of high specific gravity, chemical inertness, non-toxic nature, and commercial availability at scale, properties for which no cost-competitive mineral substitute has been commercialized. In drilling operations, barite serves multiple critical functions: increasing hydrostatic pressure in the wellbore to control subsurface formation pressures and prevent blowouts, stabilizing wellbore walls to prevent collapse, suspending drill cuttings, and lubricating the drill string. The API's and ISO 13500 standards mandate specific barite characteristics for oilfield use, creating a quality-certified, defensible demand moat for specification-grade producers. The mineral's compatibility with both water-based (WBM) and oil-based mud (OBM) systems, the two dominant drilling fluid architectures globally, ensures ubiquitous application across diverse geological and operational environments from Arctic permafrost to Saudi Arabian carbonate reservoirs.

The medical imaging segment has emerged as the fastest-growing application for barite, driven by expanding healthcare infrastructure, aging populations in developed markets, and rapidly rising diagnostic imaging procedure volumes across Asia, Africa, and Latin America. Pharmaceutical-grade barium sulfate is the globally established radiocontrast agent in X-ray, fluoroscopy, and CT examinations of the gastrointestinal tract. Its high atomic number (56) enables strong X-ray absorption, while its chemical insolubility ensures biological inertness and patient safety, unlike heavy metal alternatives. Applications span diagnostics for gastroesophageal reflux disease (GERD), peptic ulcers, inflammatory bowel disease (IBD), and colorectal malignancies, all of which are rising in global prevalence. The WHO projects global healthcare spending to grow at over 5% annually through 2030, with diagnostic imaging among the highest-investment subsectors. The medical barium sulfate segment commands premium pricing multiples of 5–8x versus commodity drilling-grade material, making pharmaceutical-grade barite production a strategically attractive margin-enhancement avenue for producers investing in downstream beneficiation and purification capabilities.

Regional Market Insights

North America Barite Market Trends and Insights

The North American barite market remains structurally mature, with the United States accounting for more than 95% of regional consumption and remaining the world’s largest importer of barite used in oilfield drilling fluids. Demand is strongly tied to shale oil and gas activity in the Permian Basin, Eagle Ford, and Bakken formations, where horizontal drilling and hydraulic fracturing require higher volumes of drilling-grade barite per well. However, the regional market is increasingly influenced by geopolitical developments affecting crude supply and refining economics.

A major turning point occurred in January 2026 when the United States carried out a military operation that removed Venezuelan president Nicolás Maduro, reshaping control of Venezuela’s oil sector and triggering a realignment of global heavy-crude trade flows. The policy shift was followed by partial easing of U.S. sanctions and new licensing frameworks allowing international energy companies to resume investment in Venezuela’s oil industry.

As several U.S. Gulf Coast refineries are configured to process heavy Venezuelan crude, a gradual redirection of Venezuelan oil exports toward the United States and away from Asian buyers. This evolving geopolitical dynamic is likely to influence drilling activity, refinery utilization rates, and upstream investment cycles across North America, indirectly shaping regional barite consumption trends through the remainder of the decade.

Europe Barite Market: High-Value Products and Regional Trends

Europe barite market is characterized by a high-value product orientation, with significant consumption concentrated in industrial manufacturing applications, coatings, plastics, pharmaceuticals, and specialty chemicals, rather than pure drilling-fluid volumes. Germany leads regional industrial barite consumption, driven by its automotive and specialty chemicals manufacturing base, with a projected market growth rate of approximately 2.0% CAGR by 2033. France and Spain maintain steady demand in architectural and industrial coatings, while the United Kingdom supports pharmaceutical-grade consumption. Norway's oil and gas industry recorded a record capital investment of approximately 275 billion Norwegian crowns (US$ 24.7 billion) in 2025, per Statistics Norway (SSB), representing a 4%+ increase over 2024, directly supporting drilling-grade barite consumption for North Sea operations.

Russia retains a substantial share of European barite demand, driven by its position as a major energy producer with active drilling programs in Siberian, Ural, and Far Eastern regions, though trade flow realignments following 2022 geopolitical disruptions have shifted portions of supply toward Chinese and Indian sources. The European Union's stringent REACH Regulation (EC No 1907/2006) and Classification, Labelling and Packaging (CLP) Regulation continue to drive quality upgrading in industrial barite applications. The region represents a premium-priced specialty barite market where producers with pharmaceutical-grade and high-purity micronized product capabilities, such as Anglo Pacific Minerals Ltd. and Broychim Group, maintain defensible positions against lower-cost commodity import competition.

Asia Pacific Barite Market: Export and Production Trends

Asia Pacific controls over 25% of global barite consumption in 2026, with China as both the world's largest producer and a major domestic consumer, and India representing the region's fastest-growing market exhibiting a CAGR exceeding 5.5% through 2033. China accounts for approximately 30–35% of global barite supply, though concerns about reserve depletion, with Chinese reserves representing only 9.25% of the global total per USGS data despite producing 42% of output, are driving industry consolidation and investment in beneficiation efficiency. China's Ministry of Natural Resources tightened barite mining permit issuance during 2023–2025, constraining expansion of new mining operations and moderating future export growth. Japan maintains stable industrial barite consumption across coatings and specialty chemicals, with the sector benefiting from the country's advanced manufacturing base.

India's barite market demonstrates exceptional growth momentum, underpinned by accelerating oil and gas exploration across offshore blocks in the Bay of Bengal and Arabian Sea under ONGC's and Reliance Industries' exploration programs, expanding industrial manufacturing, and rapidly growing healthcare infrastructure under the Ayushman Bharat PM-JAY scheme. Andhra Pradesh and Rajasthan are India's primary producing states, with APMDC (Andhra Pradesh Mineral Development Corporation) operating as a key institutional producer and exporter. ASEAN nations, including Thailand, Vietnam, and Indonesia, contribute incremental growth through infrastructure development and expanding industrial manufacturing, benefiting from proximity to major Chinese and Indian production sources that materially reduce transportation cost premiums versus Atlantic basin supply routes.

Middle East & Africa Barite Market Trends

The Middle East & Africa barite market represents a significant share of global consumption, primarily driven by intensive oil and gas drilling activity across Gulf economies. Saudi Arabia remains the dominant regional consumer as national oil companies continue long-term upstream investment programs aimed at sustaining crude output near 10 million barrels per day. Kuwait, Oman, and the UAE also contribute to steady demand as operators expand exploration programs and develop technically challenging reservoirs that require high-density barite-weighted drilling fluids for well pressure control and drilling stability. However, the regional market is increasingly influenced by geopolitical volatility following the escalation of military conflict involving the United States, Israel, and Iran.

The February 2026 strikes on Iranian targets and subsequent retaliation have disrupted energy flows and maritime logistics across the Persian Gulf, particularly around the Strait of Hormuz, through which roughly 20% of global oil trade normally passes.

Disruptions to tanker traffic, higher shipping insurance costs, and temporary port suspensions have elevated operational risks for drilling operators and supply chains. At the same time, rising crude prices and energy infrastructure vulnerabilities may delay drilling investments in certain areas. Despite these short-term uncertainties, long-term upstream development strategies by Gulf national oil companies continue to provide a structural demand base for drilling-grade barite across the region, while Africa contributes through exports from Morocco and growing oilfield demand in Algeria, Nigeria, and Egypt.

Competitive Landscape

The global barite market exhibits a fragmented competitive structure, characterized by the presence of several large mining and mineral processing companies alongside numerous regional producers supplying local markets. While a handful of multinational players control a notable share of global supply capacity, a significant portion of production remains distributed among small and medium-scale miners, particularly across Asia, Africa, and Latin America. These regional producers often cater to domestic oilfield drilling demand and localized industrial applications.

Competitive differentiation among leading companies is largely driven by product quality compliance with API standards, integrated mining-to-processing operations, and strong logistics networks supporting bulk mineral transportation to major oil and gas basins. Strategic investments in micronization facilities and purification technologies are enabling suppliers to expand into higher-value applications such as coatings, plastics, and medical-grade materials. Simultaneously, companies are prioritizing supply chain diversification and resource security through acquisitions of mining assets in emerging regions, along with long-term supply agreements with oilfield service providers to ensure stable demand and pricing visibility.

Key Developments

- March, 2026: Voyageur Pharmaceuticals Ltd. confirmed that barite from its Frances Creek project achieved pharmaceutical-grade purity of around 98.8% barium sulfate, exceeding USP standards, and announced plans to advance its barium contrast agents into Health Canada-supported human clinical trials.

- December, 2025: Shine Minerals Corp. executed a definitive agreement to acquire Red Cloud Silver Ltd., gaining an option to obtain a high-grade silver–fluorspar–barite project in Arizona, strengthening its exploration portfolio and advancing its plan to reactivate as a Tier-2 mining issuer.

Companies Covered in Barite Market

- The Andhra Pradesh Mineral Development Corporation Ltd. (APMDC)

- Anglo Pacific Minerals Ltd.

- GUIZHOU SABOMAN IMP. & EXP. CO., LTD

- Guizhou Tianhong Mining Co., Ltd.

- Yingfengyuan Industrial Group Limited

- Excalibar Minerals

- M-I SWACO (SLB)

- P&S Barite Mining Company Limited

- CIMBAR Performance Minerals

- International Earth Products LLC

- Emprada Mines and Minerals LLC

- Broychim Group

- The Kish Company, Inc.

- Oren Hydrocarbons Private Limited

- Halliburton (Baroid Division)

- Baker Hughes (drilling fluids segment)

Frequently Asked Questions

The global barite market is estimated to be valued at US$ 1.7 billion in 2026 and is projected to reach US$ 2.1 billion by 2033, driven primarily by oil and gas drilling demand and growing industrial applications.

Key demand drivers include rising oil and gas drilling activity where barite is used in drilling fluids, along with expanding demand from paints, coatings, plastics, rubber, and pharmaceutical applications.

North America leads global barite consumption, largely due to strong oil and gas drilling activity in major U.S. shale basins.

A major growth opportunity lies in pharmaceutical-grade barium sulfate used as a radiocontrast agent in diagnostic imaging.

Key market participants include CIMBAR Performance Minerals, Excalibar Minerals, SLB, Halliburton, Baker Hughes, and Anglo Pacific Minerals Ltd.