- Industrial Machinery

- Balancing Equipment Market

Balancing Equipment Market Size, Share, and Growth Forecast, 2026 – 2033

Balancing Equipment Market by Machine Type (Portable Balancing, Dynamic Balancing, Static Balancing), Method (Hard Bearing, Soft Bearing), End-User (Oil & Gas, Heavy Machinery, Power Generation, Aerospace, Automotive), and Regional Analysis for 2026-2033

Balancing Equipment Market Share and Trends Analysis

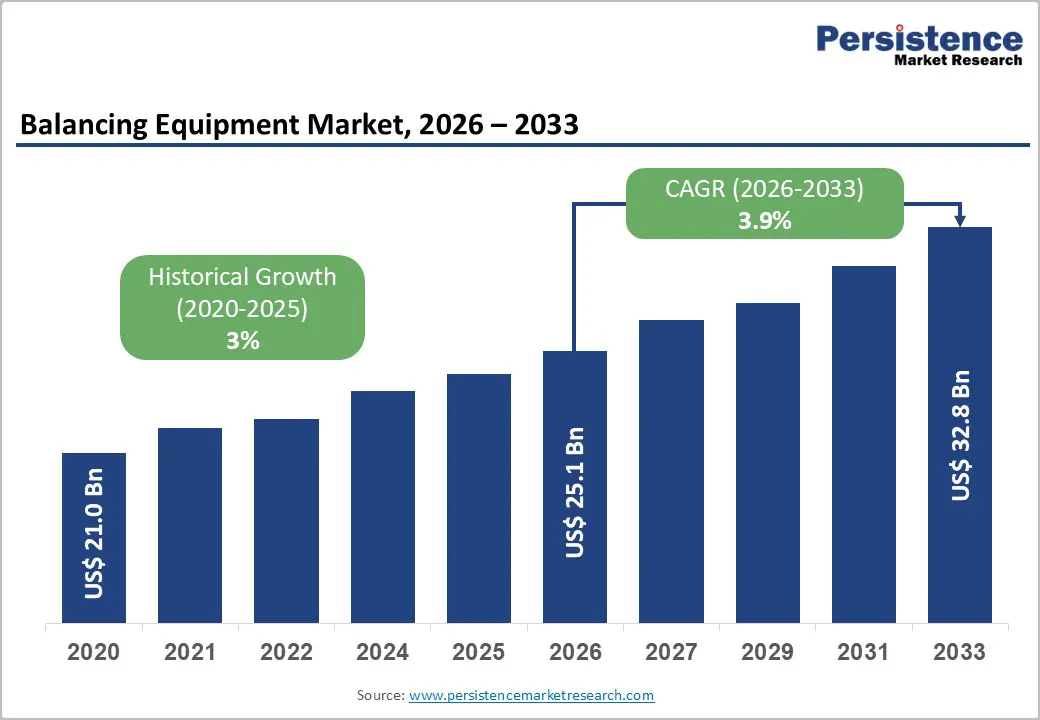

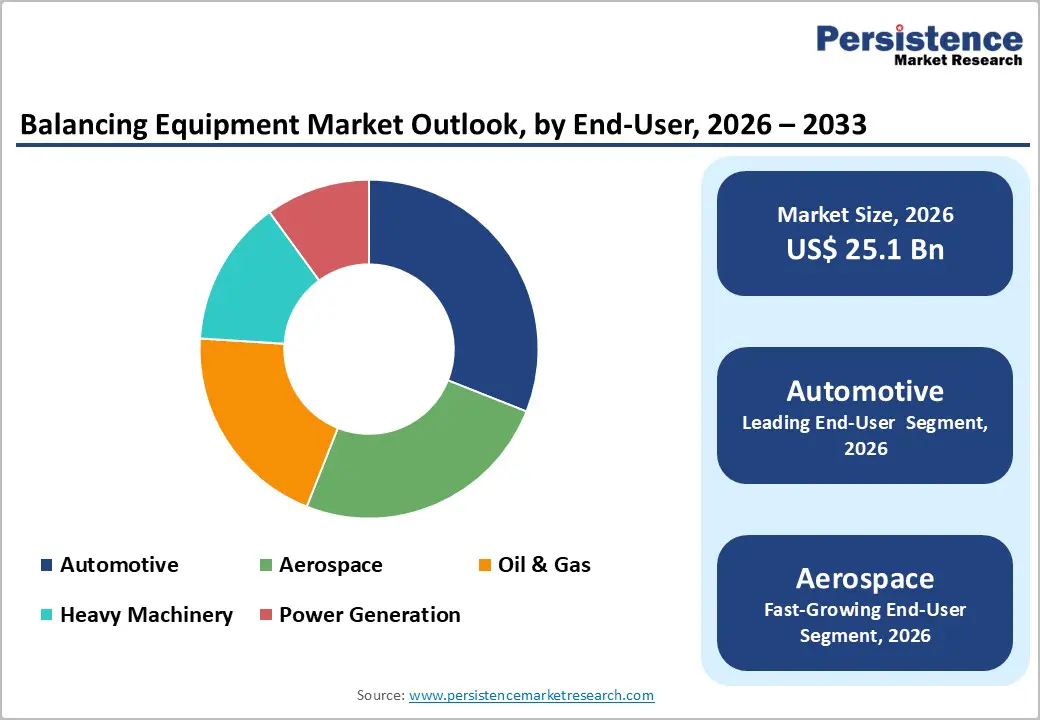

The global balancing equipment market size is likely to be valued at US$ 25.1 billion in 2026, and is projected to reach US$ 32.8 billion by 2033, growing at a CAGR of 3.9% during the forecast period 2026−2033. Market expansion reflects sustained industrial investment in asset reliability, rotational efficiency, and predictive maintenance across energy, manufacturing, and transportation sectors.

Increasing deployment of high-speed rotating machinery in power generation, aerospace, and automotive production continues to elevate precision balancing as a core operational requirement. Regulatory pressure related to vibration control, workplace safety, and equipment lifespan optimization supports consistent adoption across developed economies. Technological progress in sensor integration, digital signal processing, and condition-based monitoring strengthens balancing equipment accuracy while reducing downtime. Emerging economies contribute incremental demand through industrialization, infrastructure development, and expansion of domestic manufacturing bases. Competitive intensity remains moderate, with established suppliers benefiting from engineering credibility, calibration accuracy, and after-sales service networks.

Key Industry Highlights

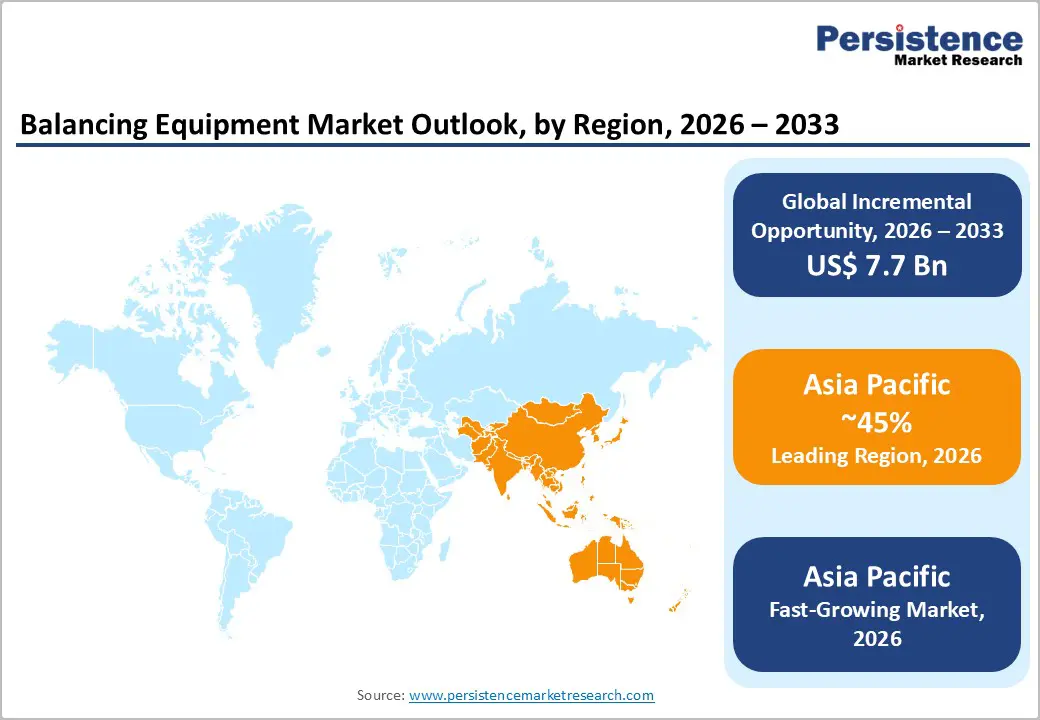

- Dominant Region: Asia Pacific is projected to hold about 45% market share in 2026, powered by a strong cross-industry demand for precision balancing technologies.

- Fastest-growing Market: Asia Pacific is forecast to be the fastest-growing market during 2026–2033, driven by the adoption and expansion of predictive maintenance across renewable energy and aerospace operations.

- Leading End-User: The automotive sector is expected to lead with a 31% market share in 2026, driven by high-volume production of engines, drivetrains, and electric motors.

- Fastest-growing End-User: The aerospace sector is slated to grow the fastest from 2026 to 2033, owing to engine efficiency requirements and rising demand for precision balancing in manufacturing and maintenance.

| Key Insights | Details |

|---|---|

|

Balancing Equipment Market Size (2026E) |

US$ 25.1 Bn |

|

Market Value Forecast (2033F) |

US$ 32.8 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

3.9% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.0% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Demand for Precision and Quality Control in Manufacturing

Manufacturing environments increasingly prioritize ultra-tight tolerances and zero-defect outcomes as production complexity and operating speeds continue to rise. High-performance rotating components form the backbone of modern industrial systems, where even marginal imbalance can lead to vibration, acoustic deviations, and premature component fatigue. Precision expectations extend beyond dimensional accuracy to include rotational stability, forcing manufacturers to embed balancing processes directly into production workflows. This shift reflects a strategic move toward process reliability, where vibration control supports consistent output quality, protects downstream assemblies, and preserves equipment efficiency under continuous operation.

Quality governance frameworks across automotive, aerospace, power equipment, and industrial machinery manufacturing reinforce this transition toward preventive precision. Regulatory benchmarks and customer qualification standards mandate documented control of vibration levels, mechanical stress, and operational smoothness during manufacturing and assembly stages. Compliance requirements increasingly extend beyond final inspection to in-process validation, placing balancing activities directly within quality assurance workflows. Original equipment manufacturer (OEM) approval programs and supplier audits evaluate traceability of balancing procedures, calibration records, and corrective actions, increasing accountability across the value chain.

Skilled Workforce Dependency and Integration Challenges

Operational reliance on advanced technical expertise constrains adoption through the precision required to operate, calibrate, and interpret outputs from sophisticated balancing systems. Effective use depends on deep knowledge of vibration behavior, rotor dynamics, sensor positioning, and tolerance compliance, while minor errors in setup or analysis translate into rework, premature component wear, or equipment failure. Industrial organizations face persistent shortages of trained personnel as skill development frameworks lag rising system complexity. Aging manufacturing workforces intensify this gap, increasing training costs and extending productivity ramp-up periods. Dependence on a limited pool of specialists elevates operational exposure, restricts deployment across multiple facilities, and reduces flexibility in high-throughput production environments.

System integration complexity further amplifies this restraint by complicating the alignment of new balancing solutions with existing manufacturing infrastructure. Diverse machine vintages, customized component designs, and inconsistent interface standards increase engineering effort during installation and commissioning. Seamless operation often requires synchronization with automation controls, production management software, and quality inspection systems, expanding implementation timelines and cost variability. Coordination across mechanical, electrical, and digital teams increases execution risk and resource strain. Prolonged integration cycles disrupt production continuity and weaken investment confidence, particularly for cost-sensitive manufacturers.

Integration with Predictive Maintenance and Digital Platforms

Advanced connectivity between balancing systems and predictive maintenance frameworks is emerging as a high-impact growth pathway as industrial operations intensify focus on asset reliability, cost discipline, and uptime optimization. Embedded sensors, Industrial Internet of Things (IIoT) architectures, and analytics layers enable continuous monitoring of vibration signatures, rotational behavior, and load distribution. This digital intelligence supports condition-based maintenance strategies that identify imbalance risks early, limiting secondary damage to bearings, shafts, and housings. Organizations gain measurable reductions in unplanned stoppages, maintenance labor intensity, and spare part consumption, while improving production continuity and asset utilization across critical operations.

Seamless linkage with digital platforms elevates balancing capabilities into enterprise-wide performance management tools. Data streams integrated into enterprise asset management systems, digital twins, and manufacturing execution platforms strengthen coordination between maintenance planning, quality assurance, and operations leadership. Standardized insights allow benchmarking across equipment fleets and production sites, supporting lifecycle optimization and long-term capital planning. Cloud-based dashboards and remote diagnostics extend value for geographically dispersed assets while reinforcing traceability and compliance requirements.

Category-wise Analysis

Machine Type Insights

Dynamic balancing equipment is anticipated to secure around 46% of the market revenue share in 2026, reflecting its critical role in high-speed, high-precision industrial applications. Core industries such as power generation, aerospace manufacturing, and automotive production rely on multi-plane correction to ensure rotational stability of turbines, compressors, and engine components. These systems support strict adherence to ISO vibration thresholds, operational safety standards, and long-term asset reliability. Large-scale manufacturing facilities favor dynamic solutions due to proven accuracy, automation compatibility, and the ability to integrate into continuous production environments without compromising throughput.

Portable balancing equipment is expected to be the fastest-growing segment from 2026 to 2033, propelled by rising demand for on-site diagnostics and maintenance across asset-intensive industries. Compact hardware design, wireless sensing, and digital interfaces enable field-level balancing with accuracy comparable to fixed installations. Energy infrastructure, oil and gas operations, and renewable installations increasingly adopt portable systems to manage dispersed assets efficiently. This flexibility supports decentralized maintenance models, lowers service dependency, and aligns with operational resilience and uptime optimization priorities.

Method Insights

The hard-bearing method is likely to lead, with a projected 58% share of the balancing equipment market revenue in 2026, due to its critical role in high-volume production environments. These systems measure unbalanced forces directly, providing consistent accuracy regardless of rotor characteristics. Automotive and appliance manufacturers favor hard-bearing solutions for standardized component balancing, ensuring quality control and high throughput. Their robustness, reliability, and compatibility with continuous production lines make them essential in industrial facilities where precision, repeatability, and operational efficiency are top priorities.

Soft-bearing balancing equipment is anticipated to be the fastest-growing segment from 2026 to 2033, fueled by rising demand in repair workshops, aerospace maintenance, and specialized rotor applications. These systems accommodate a range of rotor geometries and rotational speeds, offering flexibility that hard-bearing systems cannot. Increasing aircraft maintenance, repair, and overhaul activities drive adoption in regions with expanding commercial aviation fleets. Lightweight design, ease of use, and adaptability for diverse operational environments enable soft-bearing equipment to capture emerging opportunities in service-oriented and precision-critical applications.

End-User Insights

The automotive sector is poised to dominate, with a forecasted balancing equipment market share of 31% in 2026, driven by high-volume production of engines, drivetrains, and electric motors that require consistent balancing to meet noise, vibration, and harshness standards. Integration with automated production lines and quality assurance systems enhances efficiency and reduces rework. Manufacturers prioritize balancing solutions that maintain precision and reliability across mass production, ensuring compliance with industry standards and operational continuity.

The aerospace sector is expected to be the fastest-growing end-user segment from 2026 to 2033, driven by fleet expansion, engine-efficiency mandates, and stringent safety regulations. Precision balancing during manufacturing and maintenance ensures structural integrity, operational reliability, and regulatory compliance. Rising global air traffic and increased aircraft production drive demand for advanced balancing solutions. Suppliers offering high-accuracy, flexible equipment capture opportunities in commercial and defense aviation, supporting long-term lifecycle management and minimizing operational downtime across complex aerospace operations.

Regional Insights

North America Balancing Equipment Market Trends

North America is poised to be a significant market for balancing equipment in 2026, supported by advanced manufacturing infrastructure, high-precision industrial operations, and strong aerospace and defense sectors. Dominance is reinforced by mthe odernization of legacy production facilities, where older rotating equipment requires retrofitting with advanced dynamic and soft-bearing balancing solutions to improve efficiency and extend service life. Aerospace engine manufacturers and defense contractors demand ultra-precise balancing to comply with strict safety and vibration standards, creating a niche for high-accuracy, multi-plane balancing systems. Robust after-sales support and service networks further strengthen adoption.

North America is also experiencing accelerated growth due to the increasing adoption of digital twins, predictive analytics, and remote monitoring for industrial equipment. Companies are integrating balancing solutions with enterprise asset management and IIoT platforms to optimize maintenance schedules, reduce unplanned downtime, and track rotor performance over time. Growth in renewable energy infrastructure, including wind and natural gas power plants, drives demand for portable balancing systems suitable for on-site inspections. Investments in research and development for lightweight, adaptable equipment allow manufacturers to meet specialized industry requirements.

Europe Balancing Equipment Market Trends

Europe presents a strategic market for balancing equipment in 2026, driven by the strong presence of high-precision automotive, aerospace, and industrial machinery manufacturing hubs. Leading manufacturers in Germany, Italy, France, and the United Kingdom emphasize tight quality standards and compliance with International Organization for Standardization (ISO) vibration regulations, creating demand for dynamic, hard-bearing, and soft-bearing systems. Industrial facilities increasingly prioritize energy efficiency, rotational reliability, and equipment longevity, making balancing equipment a critical component of production workflows. Investments in automated assembly lines and standardized testing protocols further support consistent adoption across multiple industrial sectors.

Europe is also positioned for robust growth due to increasing focus on predictive maintenance and digital integration. Manufacturers leverage connected balancing systems with real-time monitoring, digital twins, and analytics to reduce unplanned downtime, optimize maintenance schedules, and track rotor performance over the entire lifecycle stages. Expansion of renewable energy projects, particularly offshore wind farms and hydroelectric power plants, increases the need for portable balancing equipment for on-site rotor inspections. Aerospace maintenance, repair, & overhaul (MRO) activity continues to grow, requiring precision balancing for engines and rotating components.

Asia Pacific Balancing Equipment Market Trends

By 2026, Asia Pacific is expected to lead with an estimated 45% of the balancing equipment market share, propelled by strong demand from automotive, heavy machinery, and power generation sectors. High-volume production of engines, turbines, compressors, and electric motors requires precise balancing to meet strict vibration and quality standards, making advanced balancing solutions essential. The expansion of automated production lines, adherence to International Organization for Standardization (ISO) standards, and a growing focus on operational efficiency drive the adoption of both dynamic and hard-bearing systems. Industrial hubs in China and India serve as key manufacturing centers, supporting a steady demand for stationary and portable equipment. The presence of domestic manufacturers alongside international suppliers ensures competitive pricing, localized service, and rapid deployment, strengthening market penetration. Increasing investments in quality control, precision engineering, and production scalability reinforce the reliance on balancing systems for high-speed and high-precision operations.

Asia Pacific is also poised to be the fastest-growing market for balancing equipment during the 2026–2033 forecast period, driven by the adoption of predictive maintenance strategies and integration with digital industrial platforms. Connected systems with real-time vibration monitoring, remote diagnostics, and lifecycle analytics enable condition-based maintenance, reducing downtime and operational costs. Expansion of renewable energy infrastructure, including wind and hydroelectric projects, and growth in aerospace production and MRO operations, increase demand for portable and soft-bearing balancing solutions. Investments in IIoT technologies, smart factories, and cloud-based maintenance platforms enhance operational visibility and efficiency. The rising emphasis on equipment longevity, operational reliability, and decentralized maintenance models is accelerating adoption across dispersed assets.

Competitive Landscape

The global balancing equipment market reflects moderate fragmentation, with the top ten players controlling approximately 50% of global revenue, indicating a mix of well-established leaders and smaller specialized manufacturers. Key players such as Schenck RoTec, Hofmann Maschinen- und Anlagenbau GmbH, IRD Balancing, CEMB S.p.A., Haimer GmbH, and SPM Instrument focus on leveraging engineering expertise, precision calibration, and product innovation to maintain competitiveness. Companies invest in research and development to enhance dynamic, hard-bearing, and soft-bearing systems, improving accuracy, throughput, and adaptability for diverse rotor types.

Entry barriers in the market remain moderate due to the technical complexity of designing and manufacturing high-precision balancing systems and the compliance requirements of certification standards such as ISO vibration regulations. While new entrants can access niche applications or portable balancing equipment, scaling operations to compete in multi-plane, high-speed dynamic balancing requires significant capital investment and engineering capabilities. International service networks and localized support systems established by leading companies create competitive advantages, making it challenging for smaller players to penetrate high-value segments. Strategic partnerships, regional manufacturing hubs, and technology licensing allow established companies to maintain leadership while addressing evolving industrial requirements.

Key Industry Developments

- In October 2025, Coats introduced the ProBalance E900 Diagnostic Wheel Balancer, a direct?drive system designed for high?volume tire and repair operations that delivers faster balancing cycles, advanced runout diagnostics, and improved ride quality to reduce comebacks and enhance service efficiency.

- In June 2025, Schenck RoTec showcased its Balancing Lab at EMO 2025 in Hannover. Key exhibits include the Pasio 100-700 universal balancing machine, the compact Pasio 15 for smaller rotors, the Schenck ONE software platform for process management and cloud integration, modernization packages for older machines, and handheld vibration measurement tools.

- In February 2025, ARI-Hetra launched a new line of heavy-duty wheel balancers designed to improve precision, efficiency, and reliability in workshop balancing operations with the support of Tri-Sensor Technology for consistent results. The lineup includes the WS-25WB50 premium model with a 19-inch LCD and built-in wheel lift, the WS-25WB30 advanced model with a digital display and lift, and the WS-25WB10 compact, portable model with a battery-powered display and hand-crank lift, all handling tires up to 50 inches in diameter and 440 pounds.

Companies Covered in Balancing Equipment Market

• Schenck RoTec

• Hofmann Maschinen- und Anlagenbau GmbH

• IRD Balancing

• CEMB S.p.A.

• Haimer GmbH

• SPM Instrument

• KOKUSAI Co. Ltd.

• Shanghai Jianping Dynamic Balancing Equipment Manufacturing Co. Ltd.

• Universal Balancing

• VibroSystM Inc.

Frequently Asked Questions

The global balancing equipment market is projected to reach US$ 25.1 billion in 2026.

Rising demand for precision, vibration control, and operational efficiency in rotating machinery drives the market.

The market is poised to witness a CAGR of 3.9% from 20232.8 to 2033.

Integration with predictive maintenance, digital platforms, and on-site portable solutions presents key growth opportunities in the market.

Key players in the market include Schenck RoTec, Hofmann Maschinen- und Anlagenbau GmbH, IRD Balancing, CEMB S.p.A., Haimer GmbH, and SPM Instrument.