- Food Ingredients & Additives

- Baking Ingredients Market

Baking Ingredients Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Baking Ingredients Market by Product Type (Emulsifiers, Leavening Agents, Enzymes, Baking Powder and Mixes, Oils and Fats, Colors & Flavors, Dough Conditioners, Starch, Other), by Form (Dry, Liquid), by Application (Bread, Biscuits & Cookies, Cakes & Pastries, Pizza Dough, Rolls & Pies), by Regional Analysis, 2026-2033

Baking Ingredients Market Size and Share Analysis

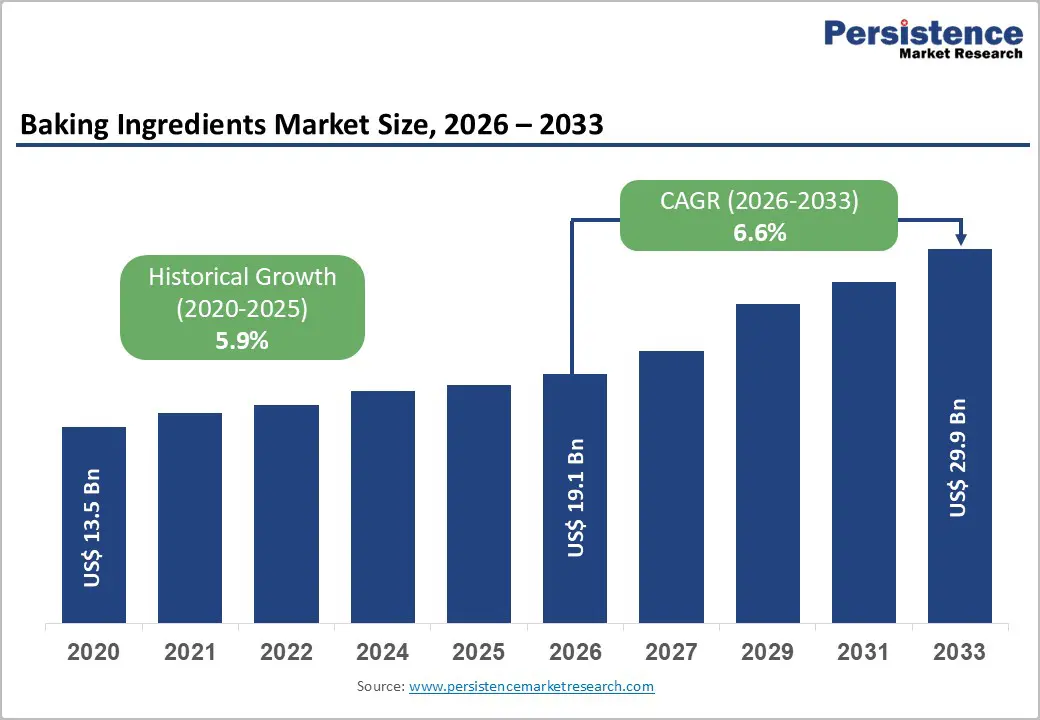

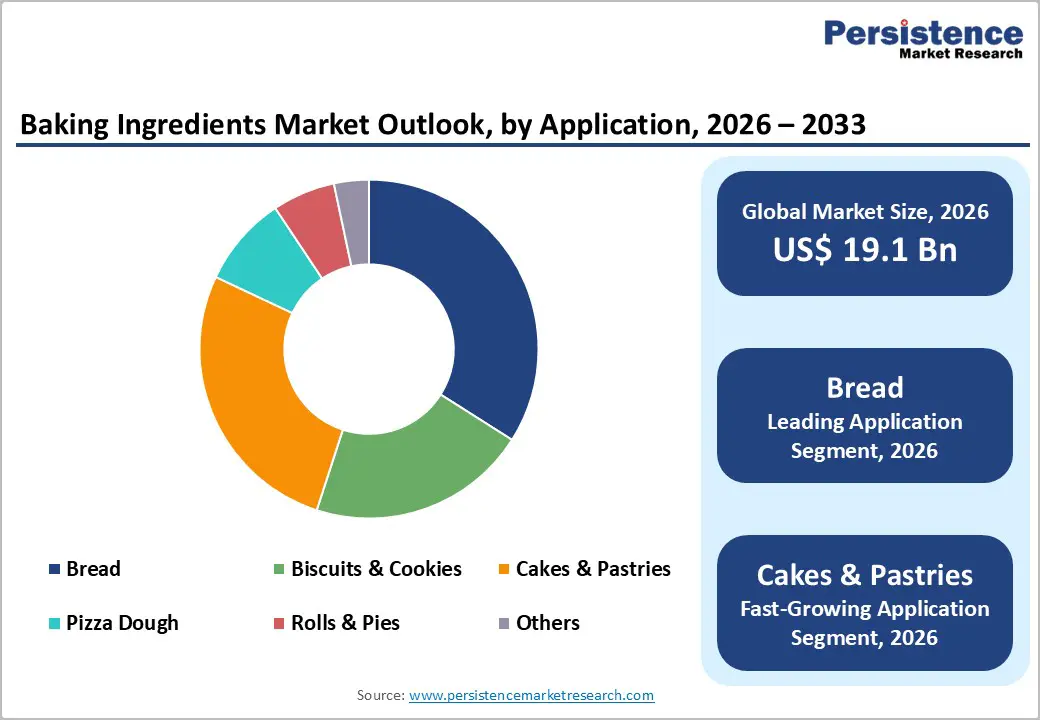

The global Baking Ingredients market size is expected to be valued at US$ 19.1 billion in 2026 and projected to reach US$ 29.9 billion by 2033, growing at a CAGR of 6.6% between 2026 and 2033

The robust expansion of the global Baking Ingredients Market is primarily necessitated by the structural shift in consumer dietary patterns toward convenience-based nutrition and the surging demand for functional, clean-label baked goods. As urbanization accelerates across emerging economies, the adoption of Western-style bakery products ranging from fortified breads to artisanal pastries has become a cornerstone of daily consumption. Furthermore, the integration of advanced food biotechnology, particularly in the development of specialized enzymes and high-stability emulsifiers, is allowing manufacturers to extend product shelf-life and enhance sensory attributes without compromising nutritional integrity.

Key Industry Highlights

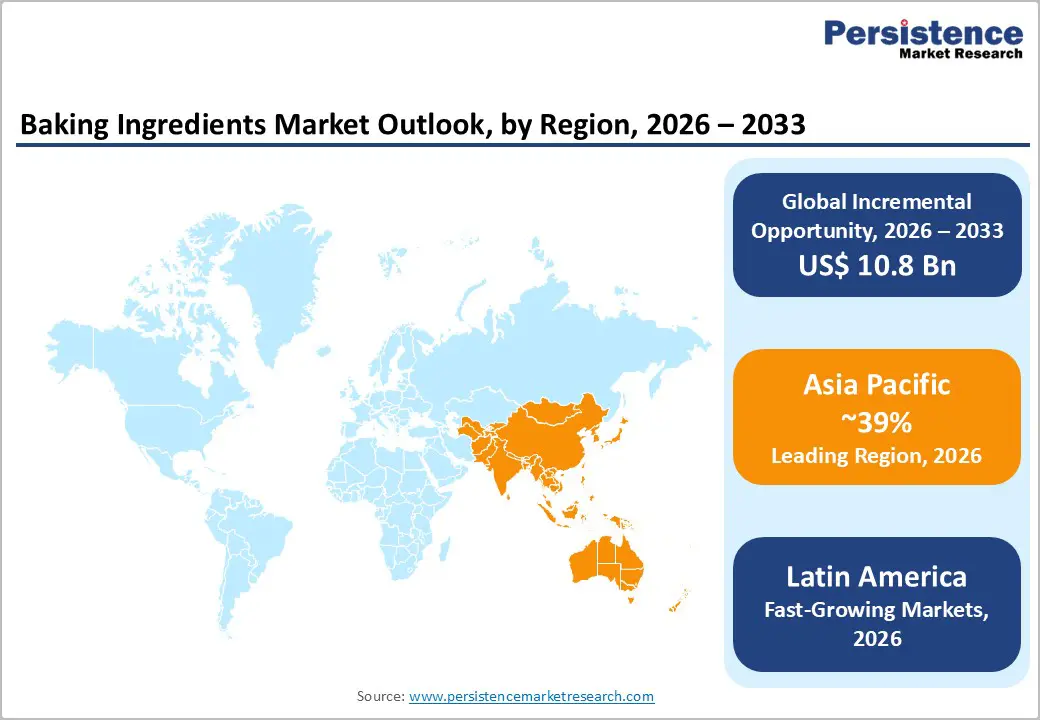

- Leading Region: Asia Pacific, accounting for around 39% market share, underpinned by rapid urbanization, large-scale industrial baking expansion, and accelerating adoption of Western-style bread, biscuits, and cakes across China, India, and Southeast Asia.

- Fastest-Growing Region: Latin America, driven by rising middle-class incomes, expansion of organized retail, strong bread consumption culture in Brazil and Mexico, and growing premiumization of packaged bakery products.

- Leading Application Segment: Bread, holding roughly 35% share, supported by its role as a daily dietary staple worldwide and sustained demand for enzymes, leavening agents, and dough conditioners to ensure consistency, shelf-life, and nutritional fortification.

- Fastest-Growing Opportunity Area: Frozen and par-baked bakery applications, fueled by the rapid uptake of frozen dough formats in QSRs, coffee chains, and in-store bakeries, creating demand for freeze-tolerant starches, emulsifiers, and dough conditioning systems.

- Market Drivers: Rising consumer inclination toward health-fortified, high-fiber, gluten-free, and protein-enriched baked goods is pushing manufacturers to reformulate using functional enzymes, plant-based fats, and clean-label ingredient systems.

- Market Opportunities: Development of specialized ingredients optimized for freeze–thaw stability and functional nutrition positioning, enabling ingredient suppliers to become long-term formulation partners rather than commodity vendors.

- Key Developments: In October 2025, Palsgaard expanded production of Emulpals® powdered cake emulsifiers in Brazil to support regional bakery growth. In April 2025, Kudos Blends launched advanced baking powder solutions in Australia and New Zealand, targeting consistency and performance in high-throughput bakery operations.

| Key Insights | Details |

|---|---|

| Baking Ingredients Market Size (2026E) | US$ 19.1 Bn |

| Market Value Forecast (2033F) | US$ 29.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.9% |

Market Dynamics

Driver – Rising Consumer Inclination Toward Health-Fortified and Functional Bakery Products

A pivotal growth driver for the Baking Ingredients Market is the intensifying focus on prevention through nutrition, which has led to a surge in demand for ingredients that offer functional benefits. Modern consumers are increasingly scrutinizing nutrition labels, seeking high-fiber, gluten-free, and protein-enriched baked goods. According to the U.S. Food and Drug Administration (FDA), over 68% of adults now actively read nutrition labels on bakery products, prompting manufacturers to reformulate products with ancient grains, prebiotics, and natural sweeteners. This shift has catalyzed the use of specialized dough conditioners and enzymes that can replicate the texture of traditional wheat-based products in gluten-free applications. The Plant Based Foods Association reported a 15% increase in vegan bakery sales in 2023, further underscoring the market's pivot toward plant-derived fats and egg replacers to meet the needs of the health-conscious and ethical consumer segments.

Restraints – High Volatility in Raw Material Pricing and Supply Chain Vulnerabilities

A significant barrier to the consistent growth of the Baking Ingredients Market is the inherent instability of core commodity prices, such as wheat, sugar, and edible oils. These raw materials often represent over 60% of the total cost structure for ingredient manufacturers. Geopolitical tensions, such as those impacting major grain-exporting regions, combined with climate-related crop failures, have led to dramatic price spikes. According to data from the Food and Agriculture Organization (FAO) of the United Nations, global cereal price indices have shown marked fluctuations in recent years, forcing manufacturers to either absorb narrowed margins or pass costs to the consumer. This volatility creates a challenging environment for long-term strategic planning and can lead to temporary market contractions as industrial bakers seek cheaper, albeit potentially inferior, substitutes to manage their bottom lines.

Opportunity – Proliferation of the Frozen Bakery Sector and Cold-Chain Innovations

The rising popularity of frozen dough and par-baked products represents a massive opportunity for the Baking Ingredients Market. Frozen bakery items allow retailers and food service operators to provide freshly-baked experiences without the need for skilled on-site bakers, significantly reducing labor costs and waste. According to industry reports, the frozen bakery segment is expanding rapidly as it appeals to consumers' desire for quality and speed. This trend creates a specific demand for freeze-tolerant ingredients, such as specialized starch variants and dough conditioners that prevent ice crystal formation and maintain structural integrity during the thawing process. Manufacturers who develop ingredients specifically optimized for the freeze-thaw cycle can tap into the burgeoning demand from coffee chains, quick-service restaurants, and grocery in-store bakeries, which are increasingly relying on frozen inventories to manage supply and demand dynamics.

Category-wise Analysis

Product Type Analysis

The Bread segment stands as the undisputed leader in the Baking Ingredients Market, commanding a dominant 35% market share in 2025. This leadership is primarily justified by the status of bread as a universal dietary staple consumed daily across almost every culture and demographic. The high volume of bread production necessitates massive quantities of leavening agents, enzymes, and dough conditioners to ensure uniformity in mass-market loaves and the desired crust characteristics in artisanal varieties. According to the USDA, the demand for whole-grain and fortified breads is particularly strong, as consumers seek fiber-rich breakfast and snack options. The versatility of bread applications from traditional sliced loaves to wraps and ethnic breads ensures a constant and high-volume demand for base ingredients. Furthermore, the industrial bread sector's focus on extending shelf-life through clean-label preservatives and natural enzymes continues to reinforce the segment's dominant revenue position.

Form Analysis

The Dry form of baking ingredients remains the preferred choice for both industrial and domestic applications, accounting for approximately 65% of the market share in 2025. The primary reason for this dominance is the superior shelf-life and ease of storage associated with dry powders and granules compared to their liquid counterparts. Dry baking mixes, leavening powders, and starches are inherently more stable, reducing the risk of microbial contamination and the need for expensive refrigerated transport. For industrial bakeries, dry ingredients allow for more precise automated dosing and easier integration into large-scale mixing systems. Additionally, the boom in home-baking, particularly through retail ready-to-bake kits, relies almost exclusively on dry-format components for consumer convenience. The Dry segment’s cost-effectiveness in logistics and its long-standing presence in the supply chain ensure it remains the cornerstone of the market's physical distribution.

Region-wise Insights

Asia Pacific Baking Ingredients Market Trends and Insights

The Asia Pacific region is the global powerhouse of the Baking Ingredients Market, holding a commanding 39% market share in 2025. This dominance is fueled by a combination of rapid urbanization, a massive population base, and the widespread adoption of Western-style dietary habits. In countries like China, India, and Indonesia, the transition from traditional grain-based meals to convenient, bread-and-biscuit-based snacks is a major driver. The Ministry of Commerce and Industry in India has highlighted the bakery sector as one of the largest segments in the country's food processing industry.

Furthermore, the region benefits from a robust manufacturing advantage and the presence of significant local and global players. China remains a major producer and consumer of baking ingredients, with a strong focus on industrial-scale production. Meanwhile, Japan and South Korea are leading in the innovation of functional and healthful indulgence products, such as low-calorie pastries and fiber-enriched breads. The explosive growth of e-commerce and modern retail across the region has made a diverse range of baking ingredients accessible to a broader consumer base, ensuring that Asia Pacific remains the primary engine of global market value.

Latin America Baking Ingredients Market Trends and Insights

Latin America is the fastest-growing region for the Baking Ingredients Market, projected to see significant expansion through 2033. This growth is underpinned by the rising purchasing power of the middle class and the expansion of organized retail in nations such as Brazil, Mexico, and Argentina. In Brazil, which accounts for a substantial portion of the region's bakery output, there is a strong tradition of fresh bread consumption, which is now being complemented by a rising demand for packaged biscuits and industrial cakes.

The region is also seeing a shift toward premiumization as urban consumers seek higher-quality alternatives to traditional mass-market products. Manufacturers in Mexico are increasingly incorporating healthier ingredients, such as whole grains and reduced-sugar sweeteners, to address public health concerns like obesity. The presence of global bakery giants like Grupo Bimbo ensures a high level of market activity and continuous investment in distribution networks. As modern retail chains expand into secondary and tertiary cities, the accessibility of a wider variety of baking ingredients is expected to drive a permanent shift in consumption patterns, positioning Latin America as a key growth frontier.

Market Competitive Landscape

The Baking Ingredients Market is moderately consolidated, with approximately 55% of the global supply controlled by a top tier of ten multinational firms. Key players like Cargill, Incorporated, ADM, and Associated British Foods plc utilize their massive vertical integration from raw material processing to finished ingredient production to maintain cost leadership and supply chain resilience. Competitive strategies are increasingly centered on R&D investments in enzymology and food science to develop clean-label and natural alternatives to synthetic additives. Differentiators such as the ability to provide customized premixes for industrial clients and robust sustainability credentials are becoming critical for securing long-term contracts. Furthermore, the market is witnessing a wave of strategic acquisitions, as leaders buy niche firms specializing in organic or allergen-free components to stay ahead of the rapid shifts in consumer health trends.

Key Developments:

- In October 2025, Palsgaard expanded production of its Emulpals® powdered cake emulsifiers to Brazil, strengthening regional supply capabilities and reducing lead times for Latin American bakeries.

- In April 2025, Kudos Blends launched advanced baking powder solutions across Australia and New Zealand, targeting professional bakeries seeking greater consistency, controlled leavening, and improved volume in high-throughput production environments.

- In March 2025, King Arthur Baking Company returned to Natural Products Expo West with its established Bread Mix Kits and introduced a new Buttermilk Biscuit Flour Blend.

Companies Covered in Baking Ingredients Market

- Cargill, Incorporated

- ADM

- Associated British Foods plc

- Kerry Group plc

- IFF

- Tate & Lyle PLC

- Puratos Group

- Corbion N.V.

- Lesaffre Group

- Bakels Group

- Dawn Food Products

- Others

Frequently Asked Questions

The global Baking Ingredients market is projected to be valued at US$ 19.1 Bn in 2026.

Rising Consumer Inclination Toward Health-Fortified and Functional Bakery Products is driving demand for Baking Ingredients market.

The Global Baking Ingredients market is poised to witness a CAGR of 6.6% between 2026 and 2033

Proliferation of the Frozen Bakery Sector and Cold-Chain Innovations is key opportunity for key players in the market.

Major players in the Global Baking Ingredients market include Cargill, Incorporated, ADM, Associated British Foods plc, Kerry Group plc, IFF, Tate & Lyle PLC, Puratos Group, and others.