- Automotive Components & Materials

- Gaskets and Seals Market

Gaskets and Seals Market Size, Trends, Share, and Growth Forecast 2025 - 2032

Gaskets and Seals Market Analysis By Product (Gaskets, Seals), Material Type (Nitrile (NBR), Ethylene Propylene (EPDM), Polyurethane), Industry (Automotive, Electrical & Electronics, Marine & Rail, Aerospace), Distribution Channel and Regional Analysis 2025 - 2032

Gaskets and Seals Market Share and Trends Analysis

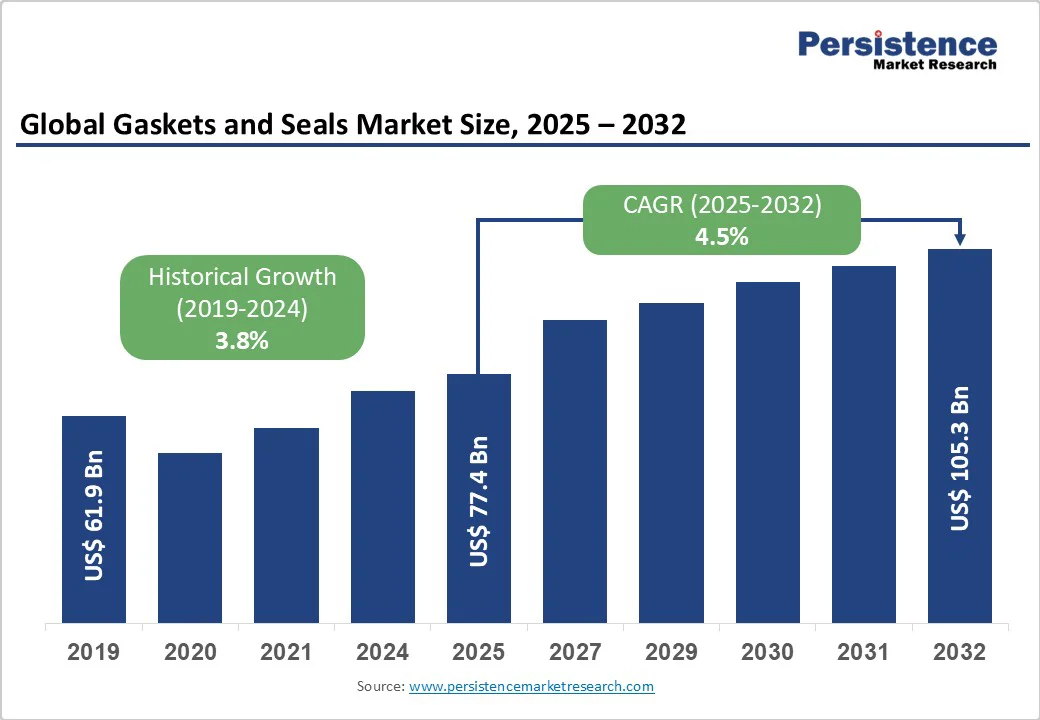

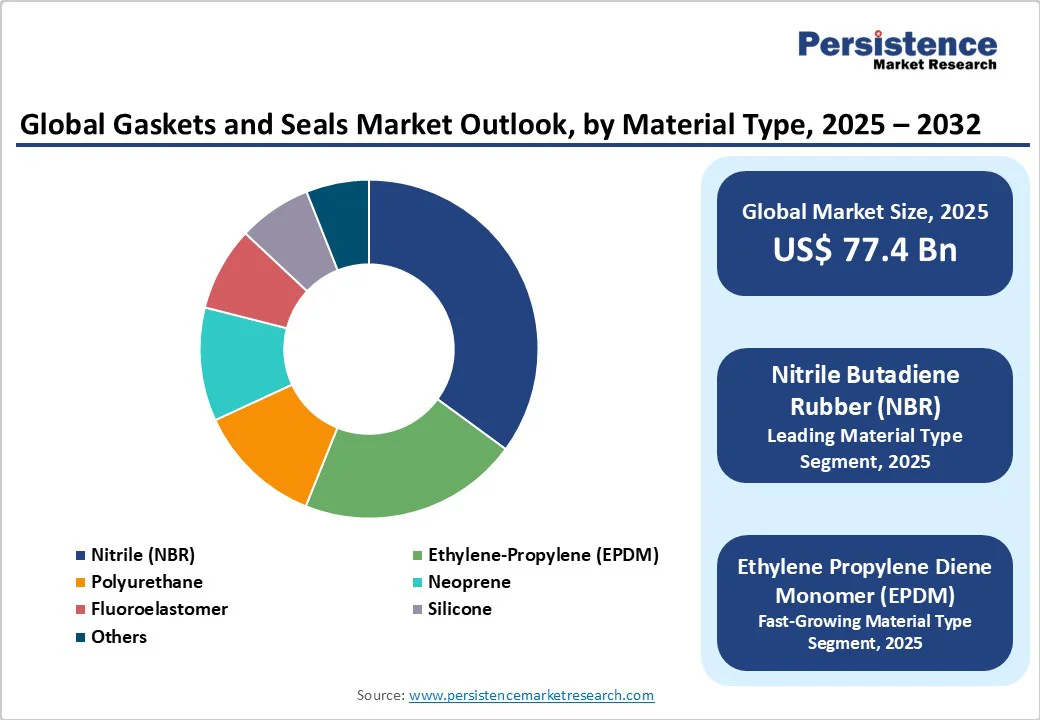

The global gaskets and seals market size is likely to value at US$ 77.4 Billion in 2025 and is projected to reach US$ 105.3 Billion by 2032, growing at a CAGR of 4.5% between 2025 and 2032. This robust growth is primarily driven by accelerating industrialization across emerging economies, stringent environmental regulations mandating advanced sealing solutions, and the rapid expansion of electric vehicle production requiring specialized thermal management and battery pack sealing technologies.

Key Market Highlights

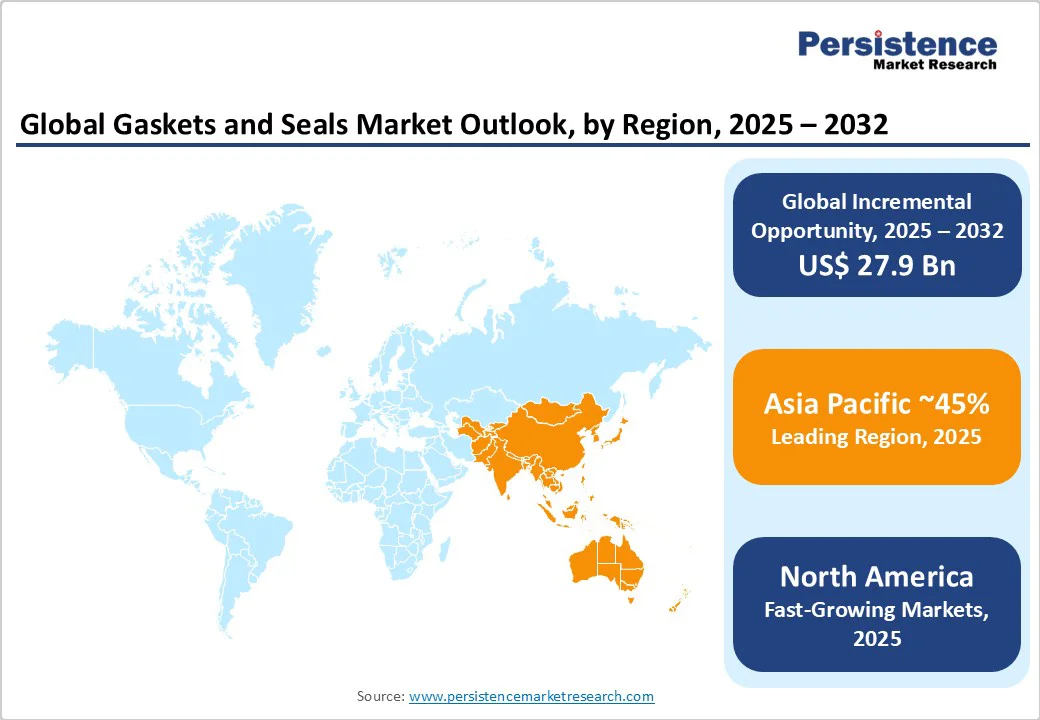

- Leading Region: Asia Pacific leads global demand with 45% market share, driven by China's manufacturing dominance, India's rapid industrialization, and expanding electric vehicle production across the region.

- Leading Product Type: Seals segment dominates with 64% market share due to widespread dynamic applications in rotating equipment, automotive systems, and superior cost-effectiveness for motion sealing requirements.

- Leading Material Type: NBR material leads with 35% share, offering an optimal balance of oil resistance, mechanical properties, temperature capability, and cost-effectiveness for automotive and industrial applications.

- Key Opportunity: Smart sealing solutions for electric vehicles and predictive maintenance applications represent the primary market opportunity, driven by Industry 4.0 and automotive electrification trends.

| Key Insights | Details |

|---|---|

|

Gaskets and Seals Market Size (2025E) |

US$ 77.4 Bn |

|

Market Value Forecast (2032F) |

US$ 105.3 Bn |

|

Projected Growth CAGR (2025-2032) |

4.5% |

|

Historical Market Growth (2019-2024) |

3.8% |

Market Dynamics

Driver - Energy Transition to Renewable Sources

The global energy transition toward renewable sources and electric mobility is revolutionizing demand patterns for advanced sealing solutions across multiple industrial sectors. Electric vehicle production reached 21.3 million units in 2025, representing a 20% increase from the previous year, driving unprecedented demand for specialized battery pack seals, thermal management gaskets, and electromagnetic interference shielding solutions. Wind turbines require weather-resistant gaskets capable of withstanding extreme environmental conditions, while hydrogen infrastructure investments surged by 30% in 2024, necessitating High Pressure Seals Market solutions resistant to extreme pressures up to 700 bar. Government mandates on emission reduction, renewable portfolio standards, and carbon neutrality targets further accelerate the adoption of high-performance sealing technologies. The International Energy Agency projects global renewable energy capacity additions to exceed 85% of new power generation through 2030, creating sustained demand for specialized gaskets and seals in wind, solar, and energy storage applications.

Industrial automation spending is likely to exceed US$ 250 billion globally in 2025. For industrial automation operations, precision sealing solutions are required for robotics, CNC machinery, and chemical processing equipment. The International Federation of Robotics reports industrial robot installations grew by 31% in 2024, with each unit requiring multiple high-performance seals for hydraulic and pneumatic systems. Oil and gas sector capital expenditures topped US$ 2 trillion worldwide, driving demand for Mechanical Seals Market products in refineries, LNG plants, and offshore platforms operating under high temperature and pressure conditions.

The American Petroleum Institute standards for fugitive emission control are becoming increasingly stringent, mandating advanced sealing technologies that reduce environmental impact while maintaining operational reliability. Aerospace applications continue adopting lightweight composite seals to achieve fuel efficiency targets, with the Federal Aviation Administration projecting 4.1% annual growth in commercial aviation through 2035.

Market Restraint - High Costs of Raw Materials

Raw material cost volatility significantly impacts gaskets and seals manufacturing economics, with synthetic rubber, specialty elastomers, and polymers comprising approximately 60% of total production costs. Natural rubber prices experienced dramatic fluctuations between US$1.20/kg and US$2.50/kg during 2020-2025 due to weather disruptions, supply chain constraints, and geopolitical tensions affecting major producing regions including Thailand, Indonesia, and Malaysia. The Association of Natural Rubber Producing Countries reported production shortfalls of 8% in 2024, exacerbating price volatility and constraining manufacturer profitability. Synthetic rubber feedstock costs are closely tied to petroleum prices, creating additional uncertainty for long-term contract pricing and capital investment planning. Smaller manufacturers lacking commodity hedging capabilities or supply chain diversification face particular challenges in managing input cost fluctuations while maintaining competitive pricing structures.

Market Opportunities - Investments in Emerging Markets to Strengthen Market Position

Emerging markets in Asia-Pacific, particularly India, Vietnam, Indonesia, and Bangladesh, offer substantial growth opportunities driven by rapid industrialization, infrastructure development, and foreign investment attraction. India's gasket and seals market is projected to grow positively through the forecast period, supported by the "Make in India" initiative, expanding automotive production capacity, and significant investments in renewable energy infrastructure.

The Ministry of New and Renewable Energy targets 500 GW of renewable capacity by 2030, creating sustained demand for specialized sealing solutions in wind turbines, solar thermal plants, and energy storage systems. Vietnam's manufacturing sector expansion, driven by supply chain diversification and US-China trade tensions, is attracting foreign direct investment exceeding US$ 15 billion annually, with multinational corporations establishing production facilities requiring high-quality sealing solutions. The ASEAN region's combined GDP growth projection of 4.8% through 2030 supports infrastructure investments in transportation, energy, and industrial facilities that drive sealing product demand.

Category-wise Insights

Product Type Analysis

The seals segment dominates the global market with approximately 64% market share, driven by widespread applications in dynamic sealing requirements across rotating equipment, automotive powertrains, and industrial machinery. Seals deliver superior cost-effectiveness and reliability in applications involving moving components, including hydraulic cylinders, pumps, compressors, and transmission systems. Their market leadership is reinforced by increasing adoption in electric vehicle drivetrains, where specialized lip seals and rotary shaft seals are essential for battery cooling systems and electric motor assemblies.

The Society of Automotive Engineers standards for electric vehicle sealing systems emphasize performance requirements that favor advanced seal designs over static gasket solutions. Industrial automation trends further support seal segment growth, as robotic systems and automated manufacturing equipment require precise dynamic sealing solutions capable of millions of operational cycles. The gasket segment maintains steady growth at 5% CAGR, benefiting from rising demand in heat exchanger applications, pipeline systems, and pressure vessel installations where static sealing performance is critical for operational safety and environmental compliance.

Material Type Analysis

Nitrile Butadiene Rubber (NBR) maintains market leadership with approximately 35% material segment share, attributed to its exceptional resistance to petroleum-based oils, fuels, and hydraulic fluids combined with broad temperature operating range from -40°C to +108°C. NBR's dominance is supported by automotive industry specifications for fuel system components, where its chemical compatibility and cost-effectiveness make it the preferred elastomer for fuel injector seals, carburetor gaskets, and transmission seals. The American Society for Testing and Materials standards recognize NBR's superior mechanical properties and abrasion resistance, making it suitable for demanding industrial applications including compressor seals and hydraulic system components.

Ethylene Propylene Diene Monomer (EPDM) represents the fastest-growing material segment, driven by exceptional weather resistance, ozone stability, and temperature capability up to 150°C that makes it ideal for outdoor applications and automotive cooling systems. EPDM's growth is accelerated by increasing adoption in HVAC systems, potable water applications, and automotive weatherstrip seals where long-term durability and regulatory compliance are essential requirements. The National Sanitation Foundation certification of EPDM compounds for potable water contact supports its expansion in plumbing and water treatment applications.

Industry Analysis

The automotive sector commands the largest end-use market share at approximately 31%, supported by global vehicle production exceeding 85 million units annually and increasing system complexity requiring specialized sealing solutions. Electric vehicle sales reached 14 million units globally in 2023, representing 18% of total automotive production and driving demand for specialized battery pack seals, thermal management gaskets, and power electronics sealing systems.

The International Organization of Motor Vehicle Manufacturers projects continued electrification growth, with EV market share expected to reach 30% by 2030, creating sustained demand for advanced sealing technologies. Automotive lightweighting initiatives and fuel efficiency regulations are accelerating the adoption of fluoroelastomer and silicone-based seals capable of withstanding higher temperatures while reducing component weight.

The oil and gas industry represents 32% of specialized sealing applications, driven by upstream exploration activities, midstream pipeline expansions, and downstream refinery modernization projects requiring high-pressure, high-temperature sealing solutions. API standards for fugitive emission control and process safety management mandate advanced sealing technologies in critical applications, supporting premium pricing for engineered solutions in this sector.

Distribution Channel Analysis

The Original Equipment Manufacturer (OEM) channel dominates with approximately 60% market share, reflecting the critical importance of sealing solution integration during equipment design and manufacturing phases. OEM partnerships enable collaborative development of customized sealing solutions tailored to specific performance requirements, operating conditions, and cost targets while ensuring optimal compatibility with host equipment systems. The OEM channel's dominance is reinforced by increasing equipment complexity and performance requirements that demand engineered sealing solutions rather than standard commercial products. Major industrial equipment manufacturers maintain preferred supplier relationships with sealing specialists, creating barriers to entry for new participants while providing stable revenue streams for established players.

The aftermarket segment exhibits robust growth driven by equipment aging, scheduled maintenance requirements, and replacement part demand across industrial facilities, with aftermarket sales providing higher margins and recurring revenue characteristics. Maintenance, Repair, and Operations (MRO) spending patterns show steady growth in developed markets, where mature industrial infrastructure generates consistent demand for high-quality replacement sealing products and technical support services.

Regional Insights

North America Gaskets and Seals Market Trends

The United States maintains technological leadership in advanced sealing solutions development, supported by stringent Environmental Protection Agency fugitive emission regulations that drive innovation in leak prevention technologies. Recent EPA initiatives targeting volatile organic compound emissions from industrial facilities have accelerated the adoption of Mechanical Seals Market products in chemical processing, petroleum refining, and pharmaceutical manufacturing applications. The regulatory framework creates competitive advantages for domestic manufacturers developing compliant solutions, with companies collaborating closely with equipment manufacturers to ensure regulatory compliance while optimizing operational performance.

Canada's energy sector expansion, including oil sands development and renewable energy projects, generates sustained demand for extreme service sealing solutions capable of operating in harsh environmental conditions. The Canada Energy Regulator has implemented enhanced pipeline integrity requirements following recent infrastructure incidents, mandating advanced sealing technologies for critical applications. The region's robust research and development ecosystem, supported by institutions such as the National Institute of Standards and Technology, fosters innovation in smart sealing systems incorporating predictive maintenance capabilities and condition monitoring sensors.

Europe Gaskets and Seals Market Trends

Germany's position as a global manufacturing leader, particularly in automotive and industrial machinery sectors, creates substantial demand for precision-engineered sealing solutions meeting exacting performance standards. The Verband Deutscher Maschinen- und Anlagenbau reports continued investment in Industry 4.0 technologies, driving the adoption of advanced sealing systems with integrated monitoring capabilities. European Union regulations on industrial emissions create harmonized standards across member states, benefiting manufacturers like Freudenberg Sealing Technologies and ElringKlinger AG with comprehensive product portfolios meeting diverse regulatory requirements.

The United Kingdom and France lead renewable energy infrastructure development, with offshore wind projects requiring specialized sealing solutions resistant to saltwater corrosion and extreme weather conditions. The European Commission's Green Deal initiative targets carbon neutrality by 2050, accelerating investments in renewable energy infrastructure and energy-efficient industrial systems that utilize advanced sealing technologies. Spain's expanding high-speed rail network and aerospace manufacturing capabilities create demand for lightweight, high-performance sealing solutions meeting stringent safety and reliability requirements.

Asia Pacific Gaskets and Seals Market Trends

China dominates regional manufacturing with a 25% share, supported by massive investments in automotive production, renewable energy infrastructure, and industrial automation systems. The National Development and Reform Commission policies promoting electric vehicle adoption and renewable energy development create sustained demand for specialized sealing solutions in emerging technology applications. Local electric vehicle manufacturers, including BYD and NIO, are driving innovation in battery thermal management sealing systems, while international automotive companies establishing Chinese production facilities require high-quality sealing suppliers.

India exhibits the highest regional growth rate at 6.8% CAGR, supported by the "Make in India" initiative and substantial infrastructure investments across transportation, energy, and industrial sectors. The Ministry of Road Transport and Highways' infrastructure development program creates demand for construction equipment and vehicle sealing solutions, while expanding manufacturing capabilities, attracting foreign direct investment requiring technical sealing products. Japan and South Korea maintain technology leadership in automotive and industrial applications, with companies focusing on high-value specialty sealing solutions for semiconductor manufacturing, precision machinery, and advanced automotive systems requiring exceptional reliability and performance characteristics.

Competitive Landscape

The global gaskets and seals market shows a balanced mix of consolidation at the top tier and fragmentation in standard product categories. Leading suppliers dominate through advanced R&D capabilities, extensive manufacturing footprints, and strong aftermarket support, allowing them to maintain strategic partnerships with major OEMs in automotive, industrial, and energy sectors. Their focus remains on delivering high-value engineered solutions tailored to critical applications.

Mid- and small-scale players continue to thrive in niche and price-sensitive segments, leveraging localized supply chains and customized offerings. The market is also witnessing a gradual shift toward service-driven business models, with contracts covering installation, condition monitoring, and lifecycle management-helping suppliers strengthen customer loyalty and create recurring revenue opportunities.

Key Market Developments:

- In September 2025, Boyd Corporation launched IP68-rated battery pack sealing solutions designed for next-generation electric vehicles. These solutions enhance thermal management, water resistance, and safety performance, addressing stringent industry requirements and positioning the company as a key enabler in supporting the accelerating global shift toward electrified mobility.

- In June 2025, John Crane, part of Smiths Group, unveiled its advanced Type 93AX Coaxial Separation Seal. This innovative design reduces nitrogen consumption by up to 80% compared to traditional systems, enabling energy industry operators to improve sustainability, cut operational costs, and enhance overall environmental performance.

- In May 2022, Datwyler strengthened its global sealing solutions portfolio through the acquisition of QSR, a U.S.-based specialist in connector sealing technologies. The deal added approximately US$ 164 million in annual revenue, enhancing its presence in electrical applications and expanding growth opportunities across automotive and industrial markets.

Companies Covered in Gaskets and Seals Market

- AB SKF

- Boyd Corporation

- Bruss Sealing System GmbH

- Dana Holding Corporation

- Datwyler

- Flowserve Corporation

- Freudenberg Sealing Technologies GmbH & Co. KG,

- Garlock Sealing Technologies LLC

- Hutchinson SA

- James Walker

- Magnum Automotive Group LLC

- Parker Hannifin Corporation

- Smiths Group Plc

- Trelleborg Sealing Solutions AB

- ElringKlinger AG

Frequently Asked Questions

The global gaskets and seals market was valued at US$ 77.4 billion in 2025 and is projected to reach US$ 105.3 billion by 2032, growing at a CAGR of 4.5% during the forecast period.

Key demand drivers include electric vehicle production growth, renewable energy infrastructure development, stringent environmental regulations, industrial automation expansion, and oil and gas sector capital investments requiring advanced sealing technologies.

The seals segment leads with approximately 64% market share due to widespread applications in dynamic sealing requirements across rotating equipment, automotive powertrains, and industrial machinery systems.

Asia Pacific dominates with 45% market share, led by China's manufacturing capabilities and India's rapid industrialization, supported by electric vehicle adoption and infrastructure development investments.

Development of smart sealing solutions incorporating IoT sensors for predictive maintenance and specialized electric vehicle applications, driven by Industry 4.0 digitalization and automotive electrification trends.

Market leaders include Freudenberg Sealing Technologies, Trelleborg Sealing Solutions, and Parker Hannifin Corporation, collectively holding significant market share through advanced technology portfolios, global manufacturing capabilities, and comprehensive customer service networks.