- Technology

- Atomic Clock Market

Atomic Clock Market Size, Share, and Growth Forecast 2026 - 2033

Atomic Clock Market by Platform type (Satellite Systems, Ground Control & Reference Stations, Aircraft & UAVs, Missile & Weapon Guidance Systems, Naval Systems and Defense Data Centers & Command Networks), by Technology (Rubidium Atomic Clocks (Rb), Hydrogen Masers, Cesium Beam Standards, Pulsed Optically Pumped (POP) Atomic Clocks, Chip-Scale Atomic Clocks and Optical Atomic Clocks), Frequency Stability, and Regional Analysis, 2026 - 2033

Atomic Clock Market Share and Trends Analysis

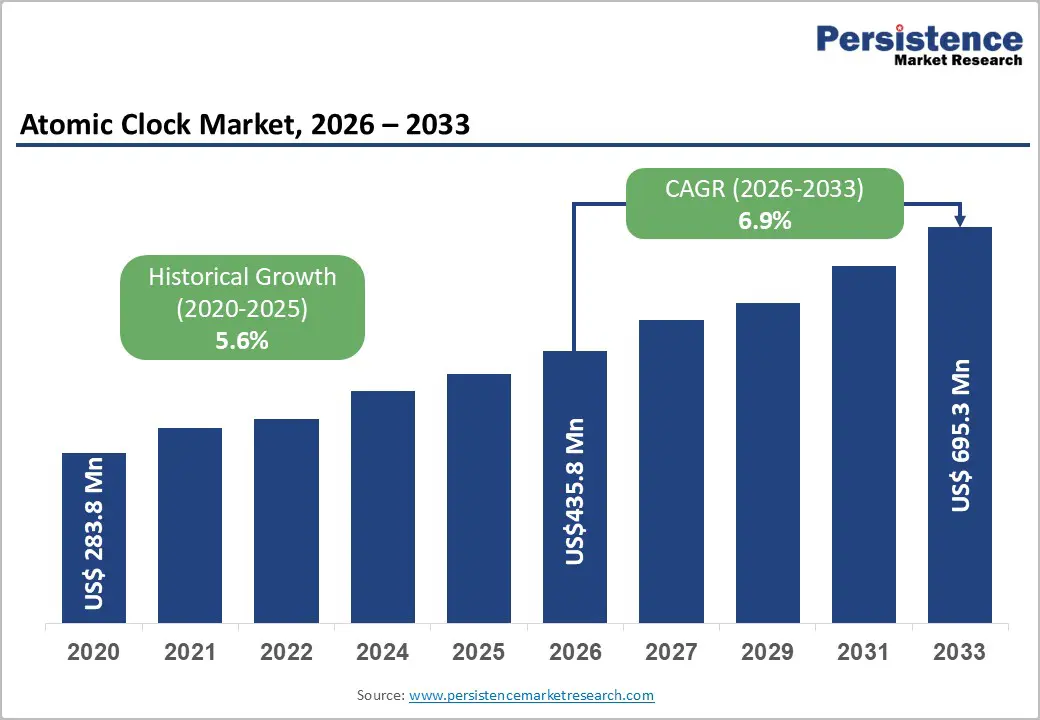

The global atomic clock market size is likely to be valued at US$ 435.8 million in 2026 and is projected to reach US$ 695.3 million by 2033, growing at a CAGR of 6.9% between 2026 and 2033.

This sustained growth trajectory reflects accelerating demand for precision timing solutions across critical defense, aerospace, and telecommunications infrastructure. The market expansion is driven by increasing adoption of atomic clocks in satellite communication systems, growing investment in GPS modernization and next-generation navigation systems, and escalating requirements for synchronized timing in 5G network deployment.

Key Industry Highlights:

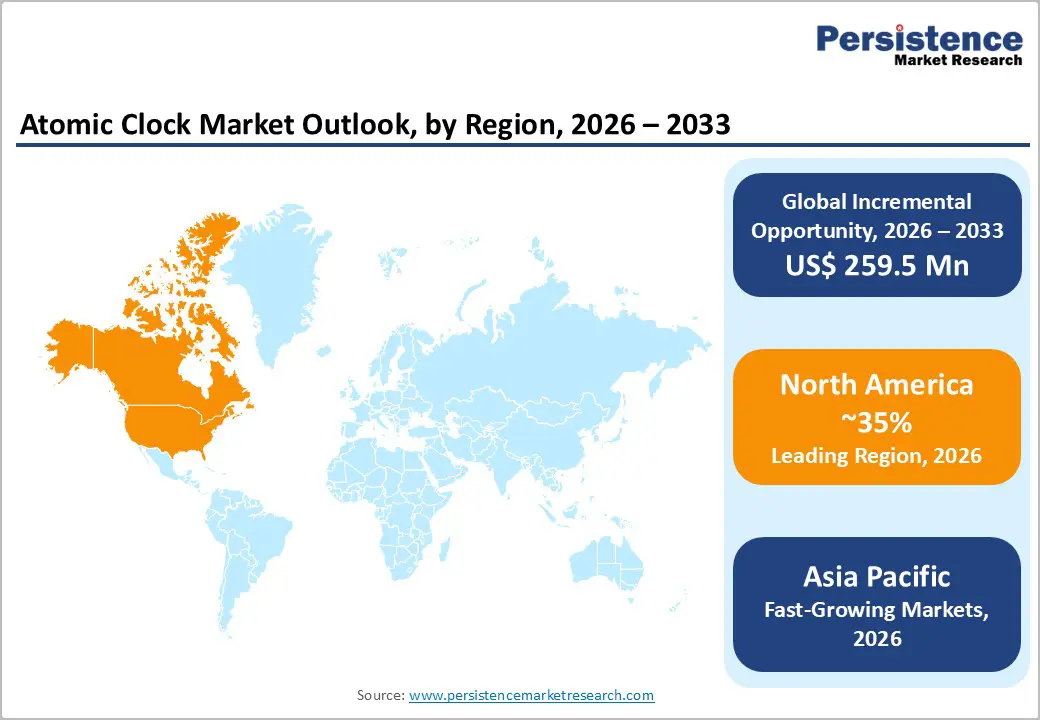

- Leading Region: North America commands significant market dominance through U.S. military infrastructure investment, GPS constellation operations, and advanced telecommunications deployment, with U.S. Department of Defense representing the largest single customer for atomic clock systems, driving sustained regional market expansion and technology advancement.

- Fastest-Growing Region: Asia-Pacific emerges as the fastest-expanding regional market driven by China's BeiDou satellite constellation expansion, India's space ambitions through ISRO, and rapid 5G telecommunications infrastructure deployment across emerging Asian economies, creating substantial incremental atomic clock demand.

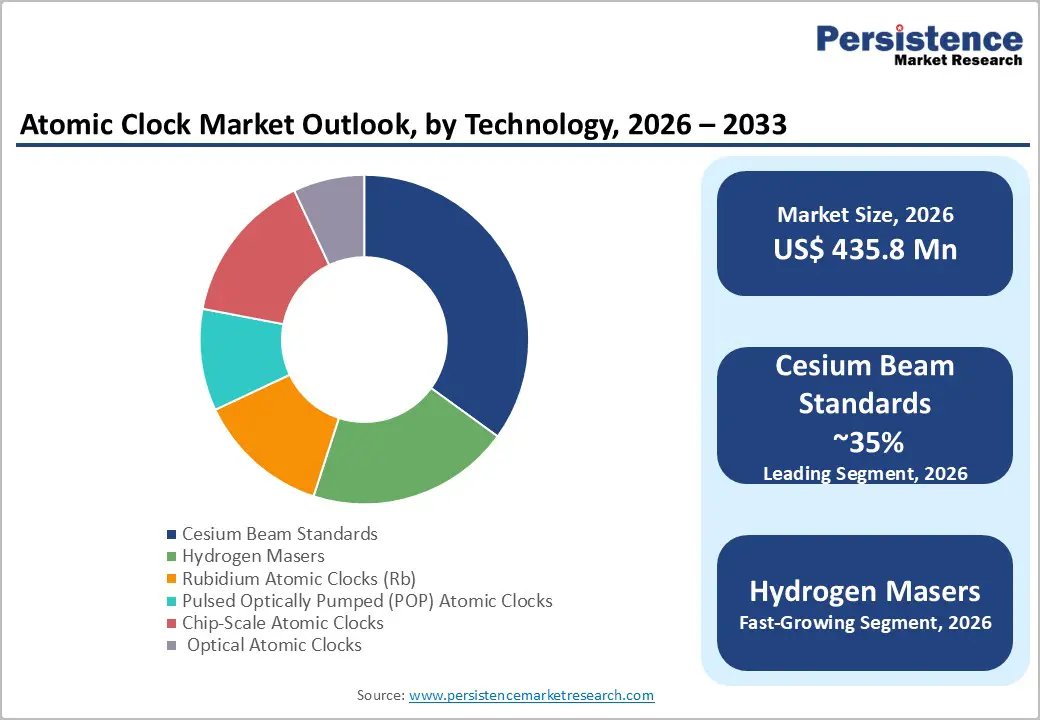

- Dominant Segment: Cesium Beam Standards maintain market leadership with approximately 35% market share, driven by exceptional long-term stability, proven reliability across decades of deployment, and validation as primary timing standards by NIST, making cesium the preferred choice for government and critical infrastructure applications.

- Optical Atomic Clocks Fastest-Growing Technology: Optical Atomic Clocks represent the fastest-growing segment advancing from laboratory development toward commercialization, offering potential frequency accuracy improvements enabling revolutionary performance enhancement beyond current cesium and hydrogen maser limitations.

- Satellite-Based Infrastructure Expansion Creating Sustained Opportunity: Emerging satellite Mega constellations for broadband connectivity and Earth observation including Starlink, Project Kuiper, and OneWeb deployment, coupled with government space modernization investments, create substantial atomic clock demand for constellation operations and technology replacement cycles.

| Key Insights | Details |

|---|---|

| Industrial Greases Market Size (2026A) | US$ 435.8 Mn |

| Projected Year Value (2033F) | US$ 695.3 Mn |

| Value CAGR (2026 - 2033) | 6.9% |

| Historical Market Growth Rate (CAGR 2019 to 2023) | 5.6% |

Market Dynamics

Drivers - Rise in Demand for Precision Timing in Next-Generation Communication Networks

Global deployment of 5G and emerging 6G communication infrastructure demands unprecedented synchronization accuracy, positioning atomic clocks as indispensable components for network infrastructure. The International Telecommunications Union (ITU) mandates timing precision standards requiring atomic clock integration across telecommunications backbone systems, driving procurement acceleration among network operators. Fiber-optic communication networks require atomic clock synchronization for wavelength multiplexing operations, creating sustained replacement demand as equipment reaches end-of-life cycles. Major telecommunications operators including Verizon, AT&T, and Vodafone are undertaking substantial infrastructure modernization initiatives incorporating atomic timing solutions. The proliferation of time-sensitive financial transactions through algorithmic trading platforms necessitates nanosecond-level accuracy, compelling investment banks and trading venues to upgrade timing infrastructure with advanced atomic clock systems delivering sub-microsecond synchronization capabilities.

Expanding Military and Defense Applications Driving Strategic Investment

Defense ministries globally are accelerating atomic clock integration in weapon guidance systems, missile targeting platforms, and advanced surveillance systems. The U.S. Department of Defense has increased allocation for precision timing modernization, recognizing atomic clocks as critical enablers for advanced missile guidance systems requiring exceptional accuracy. Satellite-based positioning systems including GPS and emerging alternatives like Europe's Galileo and China's BeiDou require atomic clock constellation support, with each satellite requiring multiple redundant atomic clocks for system reliability and accuracy. Military aircraft require atomic clock integration in avionics systems and autonomous navigation platforms, driving sustained procurement from defense contractors. Naval forces globally are modernizing fleet-wide timing infrastructure, with submarine command and control systems requiring atomic clocks for secure communications and coordinated operations. These defense applications represent strategic imperatives that transcend economic cycles, ensuring consistent funding and market expansion.

Restraints - Exceptionally High Capital Requirements and Technical Expertise Barriers

Atomic clock manufacturing requires substantial capital investment in precision engineering facilities, specialized component sourcing, and rigorous quality assurance infrastructure, creating significant barriers for new market entrants. Development timelines extending 3-5 years for new atomic clock variants necessitate sustained research funding and technical expertise difficult for emerging companies to sustain. Hydrogen maser atomic clocks require cryogenic cooling systems, specialized maintenance protocols, and technical personnel training, increasing total cost of ownership and limiting market addressability. Small and medium-sized enterprises face insurmountable financial barriers preventing competitive participation in defense and space segments where atomic clock applications command premium pricing but require extensive certification and qualification processes consuming years and millions in development expenditure.

Supply Chain Vulnerabilities and Component Sourcing Constraints

Specialized electronic components critical for atomic clock fabrication face availability constraints, with limited suppliers concentrated in developed economies creating geographic dependencies. Raw material sourcing for frequency standards including cesium and rubidium requires access to specialized suppliers, with supply disruptions cascading through production chains. Manufacturing capacity limitations prevent rapid scaling to address surging demand, particularly for specialized variants serving defense and aerospace applications requiring extended lead times. Export control regulations administered through the U.S. Commerce Department and similar agencies in allied nations restrict technology transfer and component sourcing, creating complications for manufacturers operating across multiple jurisdictions and complicating supply chain optimization.

Opportunities - Emerging Chip-Scale Atomic Clock Technology Democratizing Market Access

Chip-scale atomic clocks (CSACs) represent transformative technology enabling atomic clock integration in previously constrained applications through dramatic size reduction and power consumption improvements. These miniaturized systems consume less than one watt power compared to tens of watts for traditional hydrogen masers, enabling integration in portable military systems and unmanned platforms operating under severe power constraints. Microsemi and Orbitcomm have commercialized CSAC variants for military and commercial applications, demonstrating market viability for this technology platform. The cost reduction potential through high-volume manufacturing enables expansion into telecommunications, financial services, and industrial automation segments previously unserved due to economic constraints. Growing adoption in UAV timing systems, portable military communications, and distributed sensor networks creates substantial addressable market expansion opportunities for manufacturers delivering cost-effective atomic clock solutions.

Expanding Space-Based Infrastructure Development Creating Sustained Demand

Emerging space-based infrastructure initiatives including satellite Mega constellations for broadband connectivity, Earth observation networks, and scientific missions require atomic clock integration for position-keeping, inter-satellite communication, and scientific instrument synchronization. SpaceX's Starlink constellation expansion, Amazon's Project Kuiper, and OneWeb's satellite network deployment collectively represent thousands of satellites requiring atomic clock components for operational performance. National space agencies including NASA, the European Space Agency, and ISRO are developing advanced space platforms requiring next-generation atomic timing solutions. Government-directed space modernization investments in the United States, Europe, and Asia-Pacific regions ensure sustained funding for satellite atomic clock development. The growing commercialization of space activities through private launch providers and emerging space industries creates expanding markets for satellite-based services dependent on reliable atomic timing infrastructure, generating consistent replacement demand and technology upgrade cycles.

Category-wise Analysis

Platform Type Insights

Satellite Systems command dominant market positioning with approximately 38% market share, driven by indispensable requirements for satellite constellation operations across communication, navigation, and Earth observation missions. GPS satellites operated by the U.S. Space Force carry multiple atomic clocks ensuring accurate positioning data for billions of global users, representing the largest single application category. Galileo satellites operated by the European Space Agency similarly require precision timing for European positioning infrastructure, while BeiDou satellites administered by China's CNSA maintain separate timing infrastructure.

The proliferation of commercial satellite broadband constellations including Starlink and OneWeb introduces substantial new atomic clock demand as each satellite requires redundant timing systems. Commercial Earth observation operators including Planet Labs and Maxar Technologies require atomic clocks for precise image geo-referencing and timing synchronization across distributed satellite networks. Satellite replacement cycles every 5-8 years create recurring replacement demand sustaining market growth.

Technology Insights

Cesium Beam Standards maintain market leadership with approximately 35% market share, representing the most widely deployed atomic clock technology across government, military, and commercial applications. Cesium standards offer exceptional long-term stability and proven reliability over decades of operational deployment, making them the preferred choice for ground-based reference stations and timing infrastructure. The National Institute of Standards and Technology (NIST) maintains cesium-based atomic clocks as primary timing standards for the United States, validating technology maturity and reliability.

Hydrogen Masers represent the second-largest segment at approximately 32% market share, delivering superior short-term stability and frequency accuracy essential for specialized applications including scientific research and advanced military systems. Rubidium Atomic Clocks capture approximately 20% market share, serving portable military communications, aerospace applications, and emerging autonomous systems with favorable size-to-performance characteristics. Optical Atomic Clocks represent the fastest-growing segment, advancing from laboratory prototypes toward commercialization with potential to revolutionize timing accuracy beyond current cesium and hydrogen maser limitations.

Frequency Stability Insights

Ultra-High Stability atomic clock systems command approximately 42% market share, serving mission-critical defense, space, and telecommunications applications where frequency accuracy represents operational necessity. Military weapon guidance systems, satellite constellation operations, and financial transaction infrastructure require ultra-high stability atomic clocks delivering frequency accuracy exceeding one part in 10^13 to 10^15. GPS modernization initiatives emphasize ultra-high stability atomic clocks ensuring accurate positioning data for navigation applications.

High Stability systems occupy approximately 36% market share, supporting telecommunications infrastructure, scientific research, and commercial timing applications requiring exceptional but less stringent performance than ultra-high stability systems. Medium Stability/Ruggedized systems serve portable military communications, autonomous systems, and environmental monitoring applications where robustness and power efficiency take precedence over ultimate frequency accuracy, capturing approximately 22% market share.

Regional Insights

North America Atomic Clock Market Share and Trends

North America maintains commanding market dominance through extensive military infrastructure, advanced space capabilities, and sophisticated telecommunications networks requiring precision atomic timing. The U.S. Department of Defense represents the largest single customer for atomic clocks, with strategic investments in missile guidance modernization, satellite command systems, and advanced communications creating sustained procurement demand. GPS constellation operations administered by the U.S. Space Force require continuous atomic clock replacement and technology upgrades, supporting robust domestic supplier ecosystem.

North American telecommunications infrastructure modernization pursuing 5G deployment and emerging 6G development drives significant atomic clock adoption across network backbone systems. Private satellite operators including SpaceX and Amazon establishing North American manufacturing and operational centers create incremental atomic clock demand for constellation expansion. Canadian and Mexican aerospace and defense sectors contribute additional market volume through supplier networks and defense partnerships.

Europe Atomic Clock Market Trends

Europe demonstrates sophisticated atomic clock applications spanning space infrastructure, telecommunications, and scientific research, with particularly strong emphasis on next-generation timing technologies. Galileo satellite system operations administered by the European Space Agency drive substantial atomic clock procurement across European and international supply chains. Germany maintains technology leadership through precision manufacturing capabilities and research excellence in atomic physics, supporting advanced hydrogen maser and optical atomic clock development.

European telecommunications infrastructure emphasizes frequency synchronization for 5G networks and emerging time-sensitive applications, driving atomic clock integration across network infrastructure. The European Union's regulatory framework including directives on precision timing and synchronization standards drives technology adoption and standardization. United Kingdom maintains independent atomic clock development capabilities through NPL (National Physical Laboratory), supporting both domestic applications and international collaboration.

Asia Pacific Atomic Clock Market Share and Trends

Asia Pacific emerges as the fastest-growing regional market, driven by rapidly expanding defense capabilities, space ambitions, and telecommunications infrastructure development across the region. China has undertaken substantial atomic clock development initiatives supporting BeiDou satellite constellation expansion, domestic telecommunications infrastructure, and advanced military capabilities. CETC (China Electronics Technology Group) represents the dominant domestic atomic clock manufacturer, pursuing vertical integration and technology advancement to support national space and defense objectives.

Japan maintains world-class atomic clock research and development capabilities through institutions and manufacturers focusing on advanced frequency standards and optical atomic clock technology. South Korea supports growing telecommunications infrastructure through atomic clock integration in 5G network deployment and emerging autonomous systems applications. ASEAN nations including Singapore, Thailand, and Vietnam are establishing manufacturing and assembly capabilities for atomic clock components, capitalizing on regional cost advantages and strategic supply chain positioning.

Competitive Landscape

The atomic clock market exhibits consolidated competitive structure dominated by established manufacturers with deep technology expertise, significant capital resources, and extensive customer relationships across defense, aerospace, and telecommunications segments. Microchip Technology, Safran, and Leonardo command dominant market positions through comprehensive product portfolios, proven reliability across critical applications, and established relationships with government and military customers.

Emerging technology innovators including AccuBeat and ORA Graphene are pursuing specialized niches focusing on chip-scale atomic clocks and advanced materials representing potential market disruption. Manufacturers are undertaking substantial research and development investments in optical atomic clock technology, next-generation cesium standards, and miniaturized atomic clock variants enabling broader market access.

Key Developments:

- June 2024: Microchip Technology Expands Atomic Clock Product Portfolio - Microchip Technology announced advanced timing solutions targeting defense and aerospace applications, demonstrating continued investment in atomic clock technology development and market expansion supporting growing demand across military and space segments.

- February 2026: Safran Enhances Cesium Atomic Clock Performance Specifications - Safran unveiled next-generation cesium atomic clock variants delivering enhanced frequency stability and extended operational lifespan, targeting telecommunications infrastructure modernization and space constellation applications requiring superior performance characteristics.

Companies Covered in Atomic Clock Market

- Microchip Technology Inc.

- Safran

- Leonardo S.p.A.

- AccuBeat Ltd.

- Oscilloquartz

- Stanford Research Systems

- Meinberg GmbH & Co. KG

- IQD Frequency Products

- CETC - China Electronics Technology Group

- India Space Research Organization

Frequently Asked Questions

The global Atomic Clock Market is valued at US$ 435.8 Million in 2026 and is expected to reach US$ 695.3 Million by 2033, expanding at a CAGR of 6.9% during the forecast period.

Market growth is propelled by 5G and emerging 6G telecommunications network deployment, U.S. Department of Defense modernization initiatives, satellite constellation expansion through SpaceX Starlink and Amazon Project Kuiper, GPS constellation technology upgrades, and military weapon guidance system advancement, creating sustained demand across defense, aerospace, and critical infrastructure segments.

Cesium Beam Standards command approximately 35% global market share due to exceptional long-term frequency stability exceeding one part in 10^13, proven reliability across decades of operational deployment, validation as primary timing standards by NIST, and cost-effective manufacturing enabling competitive pricing across government and commercial applications.

North America maintains significant market dominance through U.S. military infrastructure investment, GPS constellation operations requiring continuous atomic clock support, advanced space capabilities including satellite development, and telecommunications infrastructure modernization, with the U.S.

Key market participants include Microchip Technology Inc., Safran, Leonardo S.p.A., AccuBeat Ltd., Oscilloquartz, Stanford Research Systems, Meinberg GmbH & Co. KG, IQD Frequency Products, CETC, China Electronics Technology Group, and India Space Research Organization.