- Industrial Machinery

- Assembly Line Solutions Market

Assembly Line Solutions Market Size, Share, and Growth Forecast, 2025 - 2032

Assembly Line Solutions Market By Technology (Robotics Integration, Artificial Intelligence (AI), Others), Line Type (Manual, Others), End-user Industry (Automotive, Electronics & Semiconductors, Consumer Goods, Pharmaceuticals, Others), and Regional Analysis for 2025 - 2032

Assembly Line Solutions Market Share and Trends Analysis

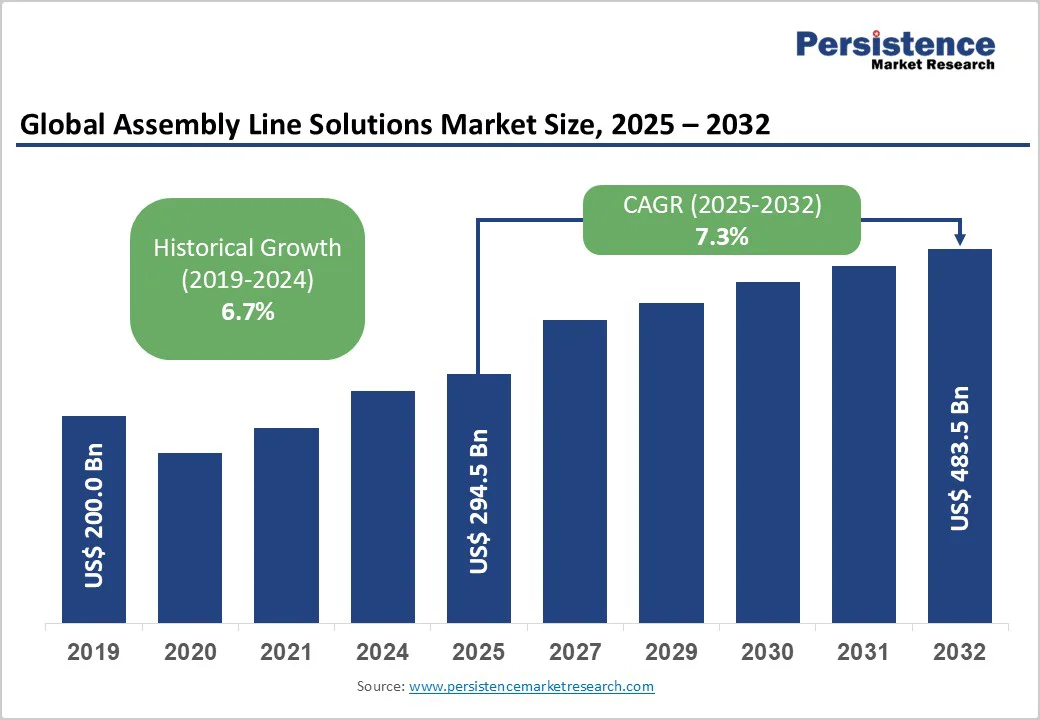

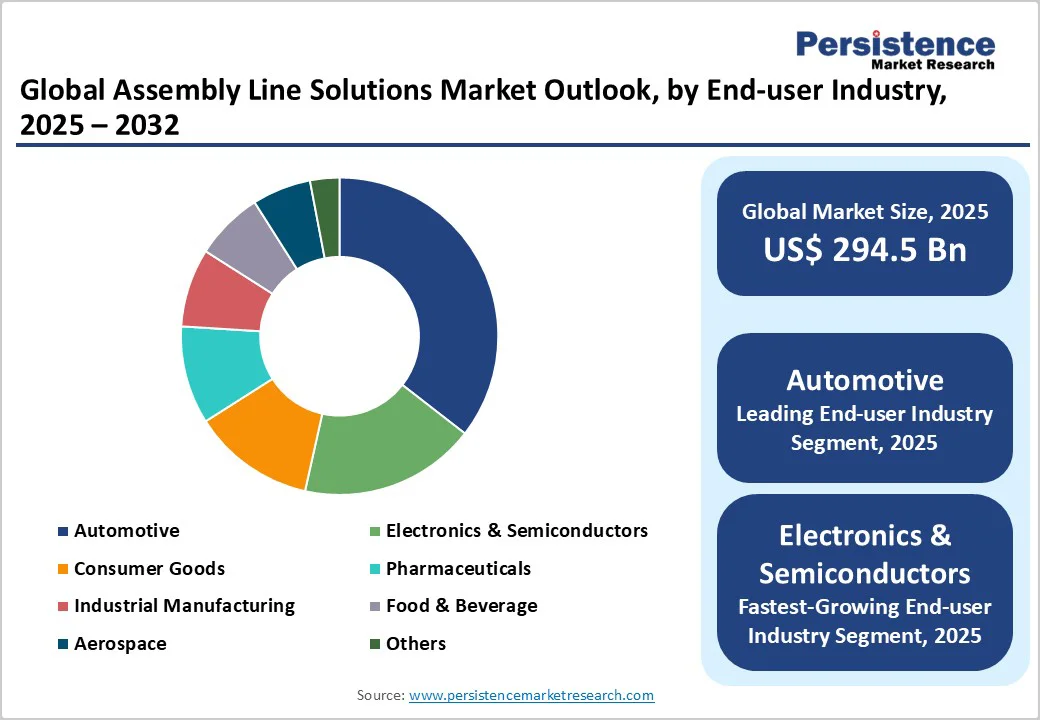

The global assembly line solutions market size is likely to be valued at US$294.5 billion in 2025, and is estimated to reach US$483.5 billion by 2032, growing at a CAGR of 7.3% during the forecast period 2025 - 2032, driven by the adoption of automation technologies across industries and increasing demand for production efficiency in factories and plants.

Key growth drivers include Industry 4.0 mandates, skilled labor shortages, and the shift to EV production, boosting operational agility, reducing labor reliance, and supporting sustainable manufacturing.

Key Industry Highlights

- Dominant End-user Industry: Automotive holds the largest share at 36% in 2025, driven by complexities in EV production.

- Fastest-growing Line Type: Fully automated assembly lines are the fastest-growing segment, projected to expand at a CAGR of around 10.5% through 2032, boosted by advancements in AI and robotics.

- Leading Technology: Robotics integration is anticipated to secure 32.5% of the market share in 2025 and grow at the highest CAGR from 2025 to 2032.

- Dominant Region & Fastest-growing Regional Market: Asia Pacific is poised to dominate with approximately 45% market share in 2025 and emerge as the fastest-growing regional market, led by China’s robust robot ecosystem.

- Regional Dynamics: North America is set to capture about 24% of the market, catalyzed by federal tax incentives and a strong innovation ecosystem. At the same time, Europe is aided by regulatory mandates and energy cost pressures.

- Competitive Environment: Strategic developments revolve around the integration of robotics and AI, merger & acquisition activities, and the increased use of digital twin technologies to enhance automation efficiency.

- April 2025: Valeo expanded its manufacturing capabilities in Pune, India, which includes the installation of new production lines focused on advanced EV components such as electric motors and power electronics.

| Key Insights | Details |

|---|---|

| Assembly Line Solutions Market Size (2025E) | US$294.5 Bn |

| Market Value Forecast (2032F) | US$483.5 Bn |

| Projected Growth (CAGR 2025 to 2032) | 7.3% |

| Historical Market Growth (CAGR 2019 to 2024) | 6.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Industry 4.0 Adoption & Smart Factory Mandates

Industry 4.0 adoption is fundamentally transforming the market growth trajectory by integrating advanced digital technologies such as artificial intelligence (AI), robotics, the Industrial Internet of Things (IIoT), and digital twin simulations. Manufacturers worldwide are transitioning from traditional, rigid conveyor systems to highly adaptive and AI-orchestrated workcells that enable real-time decision-making and operational flexibility.

This shift supports production agility required for increasingly customized and smaller batch manufacturing while maintaining or increasing throughput. For example, at ABB’s Shanghai factory, a US$150 million investment in autonomous robots and digital twins has led to more efficient changeover processes and increased line utilization.

This transformation is driven by the increasing capability of smart factories to predictively maintain equipment, reduce operational hazards, and optimize overall equipment effectiveness (OEE). According to a recent industry survey, 41% of manufacturers plan to increase investments in factory automation hardware within the next 24 months, alongside a notable push into sensor deployment and vision systems, further fueling the intelligent assembly ecosystem.

High Capital Intensity and Long ROI Cycles

The market for assembly line solutions faces significant capital intensity challenges that constrain rapid adoption, particularly among small & medium enterprises (SMEs). Deploying robotic workcells requires upfront investments typically ranging from US$175,000 to US$400,000 per system based on complexity and customization.

Achieving a standard two-year return on investment (ROI) compels companies to sustain high utilization rates —generally above 85% OEE —which is difficult in volatile market environments characterized by demand fluctuations and product changeovers.

Several manufacturing facilities also operate legacy brownfield plants, where integrating modern automation requires costly middleware, interface engineering, and access to scarce specialized talent, thereby increasing the total cost of ownership.

Although Robotics-as-a-Service (RaaS) models offer subscription-based alternatives to ease upfront capital burdens, they require operators to exhibit operational maturity and stable production to realize benefits. Without sufficient government financing or attractive tax incentives, adoption rates among SMEs are hampered, as firms prefer incremental upgrades over full-scale automation, limiting productivity gains and slowing overall market growth.

Flexible Assembly Lines for Electric Vehicle (EV) Production

The automotive industry’s ongoing shift to electric vehicles (EVs) presents a highly lucrative growth opportunity for flexible, software-defined assembly line solutions. Global electric car sales worldwide already surpassed 17 million units in 2024, according to the International Energy Agency (IEA).

EV manufacturing demands versatile production lines capable of swiftly transitioning between various powertrain architectures with minimal downtime, necessitating advanced AI monitoring, autonomous mobile robotics, and digital twin simulations to ensure operational excellence.

Ford’s Cologne plant, for example, invested US$2 billion and now operates over 600 robots, efficiently optimizing drivetrain variability. Similarly, startups such as Turkey's Togg employ unified digital twin environments and 250 robots to maintain a high throughput of 20 vehicles per hour while ensuring operational resilience and scalability.

This electrification trend not only drives extended multi-year automation contracts but also fuels aftermarket services, including predictive maintenance and upgrade installations, thereby increasing vendors’ recurring revenue streams.

Category-wise Analysis

Technology Insights

In 2025, robotics integration is poised to dominate the technology segment, accounting for an estimated 32.5% of revenue. This leadership stems from substantial advances in AI-driven algorithms, multifunctional grippers, and enhanced sensing technologies that enable intricate tasks such as handling semiconductor wafers and assembling complex battery modules.

Complementary technologies, including vision systems and control software, are increasingly integrated to provide real-time quality assurance, process optimization, and predictive insights, thereby reducing defect rates and improving cycle times. These developments are a testament to the strategic importance of robotics in advancing assembly lines and to the robust growth trajectory of the market.

Line Type Insights

Semi-automated assembly lines are poised to lead with approximately a 34% market share in 2025, offering a synergistic balance between human dexterity and robotic accuracy. This segment appeals particularly to industries that require customization and flexibility without sacrificing automation benefits.

In contrast, fully automated assembly lines are experiencing the fastest growth, with a projected CAGR of around 10.5% through 2032. The growth drivers include an industry-wide push toward lights-out manufacturing to maximize speed and repeatability while minimizing human error.

Fully automated systems benefit from modular architectures and AI-enabled control systems, enabling rapid reconfiguration and continuous optimization, thus justifying higher capital expenditures through superior total cost of ownership reductions and throughput gains.

End-user Industry Insights

The automotive sector is anticipated to maintain dominance as the largest end-use market segment, holding roughly a 36% of market share in 2025. This is chiefly due to the extensive use of robotics across welding, painting, and complex final assembly processes.

The electronics and semiconductors segment follows, with the fastest growth at a CAGR of approximately 10.4%, driven by escalating demand for precision handling and assembly of miniaturized components and for surface-mount technology.

At the same time, the pharmaceutical and food & beverage industries are ramping up automation investments to comply with stringent regulatory and hygiene standards, diversifying the portfolio of assembly-line solution applications while bolstering steady market expansion.

Regional Insights

North America Assembly Line Solutions Market Trends

North America is expected to capture an estimated 24% share of the assembly line solutions market in 2025, propelled primarily by the U.S.'s leadership in manufacturing innovation and proactive federal incentives, including Section 179 tax relief for capital equipment investments. The regional market is forecasted to register a notable CAGR over the 2025 - 2032 period.

Key growth drivers include rising electric vehicle production, labor shortages in skilled manufacturing roles, and a fertile innovation ecosystem that encourages the development and adoption of AI and robotics technologies.

Localized state funding programs, such as Illinois's extension of incentives worth US$827 million to Rivian and Automate ND in North Dakota, are expanding the deployment of automation technologies in targeted sectors. Regulatory frameworks emphasize cybersecurity and operational safety standards, shaping vendor technology offerings and deployment strategies.

Europe Assembly Line Solutions Market Trends

Europe is likely to account for nearly 20% of the assembly line solutions market share in 2025, with Germany, the U.K., France, and Spain as leading contributors. The regional market anticipates a modest CAGR from 2025 to 2032, constrained by energy cost inflation and prevailing economic uncertainties. Regulatory alignment across the European Union (EU) has fostered the adoption of advanced digital twin technologies and the integration of AI systems in manufacturing.

The InvestAI program, a EUR 200 billion funding initiative, targets automotive supply chain resilience and competitiveness by accelerating the deployment of automation and predictive analytics. European decarbonization policies and sustainability mandates further influence investment direction, urging manufacturers to upgrade assembly technologies to reduce carbon footprints and comply with tightening regulations, ultimately enhancing regional market sustainability and innovation capacity.

Asia Pacific Assembly Line Solutions Market Trends

Dominating the global landscape, the Asia Pacific is slated to hold approximately 45% of the assembly line solutions market share in 2025, backed by China’s robust industrial robotics ecosystem and aggressive government incentives.

The regional market is projected to sustain a vigorous CAGR of 8.2% through 2032. Contributing factors include comparatively affordable robotic systems, expansive electronics, and battery manufacturing sectors, alongside growing talent development initiatives across India and ASEAN countries.

China leads globally with 52% of robot installations, reflected in sprawling smart factory programs and digital transformation investments. India and ASEAN nations are scaling semiconductor fabs and EV production lines to meet global demand, supported by focused skill development and infrastructure policies that propel the region’s manufacturing competitiveness.

Competitive Landscape

The global assembly line solutions market structure is moderately concentrated, with leaders such as ABB, Siemens, and KUKA collectively ruling the market. These companies differentiate themselves through advanced AI capabilities, broad digital twin applications, and innovative subscription-based Robotics-as-a-Service (RaaS) models, enhancing accessibility and scalability.

Alongside these industry giants, a diverse array of niche and regional players, especially in Asia, have stimulated competitive pressure and expedited innovation cycles. This market configuration achieves a balanced dynamic of global technological leadership synergized with localized market responsiveness, allowing firms to tailor solutions for specific regional or sectoral requirements effectively.

Key Industry Developments

- In October 2025, Airbus opened its second Tianjin assembly line to increase A320neo production, targeting 75 jets per month by 2027. The facility will be fully operational by early 2026, strengthening China-Europe trade ties.

- In August 2025, Ford and Toyota began overhauling U.S. assembly lines to compete with Chinese automakers. Ford is investing US$2 Billion in Louisville to produce a US$30,000 midsize EV pickup by 2027 using a triple-line universal EV platform. Toyota is upgrading its Kentucky plant with the flexible “K-flex” line to build multiple models, including EVs, with high automation.

- In February 2025, 3M and GM launched the first robotic paint repair system on a moving assembly line, automating paint defect fixes without removing vehicles. The innovation boosts efficiency, quality, and supports smart automotive manufacturing.

Companies Covered in Assembly Line Solutions Market

- ABB Ltd.

- Siemens AG

- KUKA AG

- ACRO Automation Systems, Inc.

- Hochrainer GmbH

- JR Automation

- Central Machines, Inc.

- Totally Automated Systems

- ALIGN PRODUCTION SYSTEMS, LLC

- Adescor Inc.

- Eriez Manufacturing Co.

- Fusion Systems Group

- Gemtec GmbH

- SITEC Industrietechnologie GmbH

- UMD Automated Systems

- Rockwell Automation

- Dixon Automatic Tool, Inc.

- Invio Automation

- Advent Design Corporation

- Isotech, Inc.

Frequently Asked Questions

The assembly line solutions market is projected to reach US$294.5 Billion in 2025.

Accelerating adoption of automation technologies across industries and increasing demand for production efficiency in factories and plants are driving the assembly line solutions market.

The market is poised to witness a CAGR of 7.3% from 2025 to 2032.

Industry 4.0 mandates, labor shortages in skilled manufacturing roles, and the shift to electric vehicle production requiring flexible, smart assembly lines are the key market opportunities.

ABB Ltd., Siemens AG, and KUKA AG are some of the key players in the assembly line solutions market.