- Specialty & Fine Chemicals

- Linear Alpha Olefin Market

Linear Alpha Olefin Market Size, Share, and Growth Forecast 2026 - 2033

Linear Alpha Olefin Market by Product Type (Butene, Hexene, Octene, Decene, Dodecene, Tetradecane, Hexadecene, Octadecene, Other), Application (LLDPE, HDPE, Poly Alpha Olefins, Detergents, Lubricants, Other), and Regional Analysis for 2026 - 2033

Linear Alpha Olefin Market Size and Trend Analysis

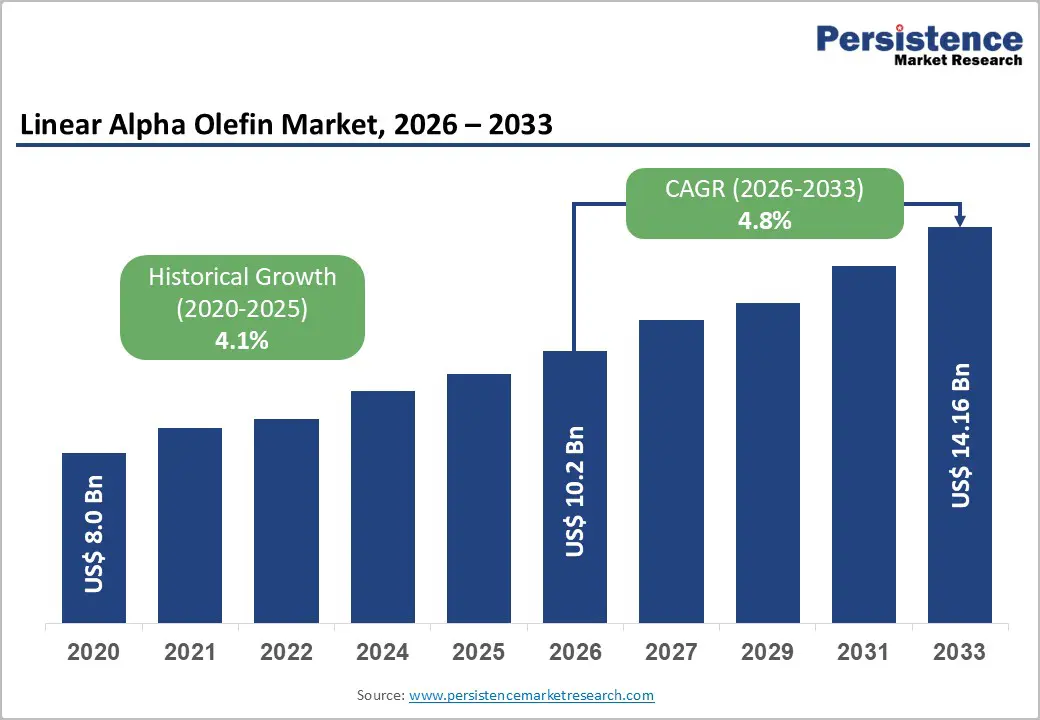

The global Linear Alpha Olefin market size is supposed to be valued at US$ 10.2 Bn in 2026 and is projected to reach US$ 14.2 Bn by 2033, growing at a CAGR of 4.8% between 2026 and 2033.

The market is experiencing significant growth driven by rising demand for linear low-density polyethylene (LLDPE) in packaging applications, coupled with expanding consumption of synthetic lubricants based on polyalphaolefin (PAO) in the automotive sector. Additionally, stringent environmental regulations are driving demand for biodegradable surfactants and detergents derived from linear alpha olefins, particularly in developed economies of North America and Europe. Furthermore, the rising consumption of Poly Alpha Olefins (PAOs) in the synthesis of high-performance synthetic lubricants is acting as a catalyst for market expansion. This upward trend is underpinned by the robust industrialization in emerging economies, where infrastructure development and manufacturing activities necessitate high-quality chemical intermediates.

Key Market highlights

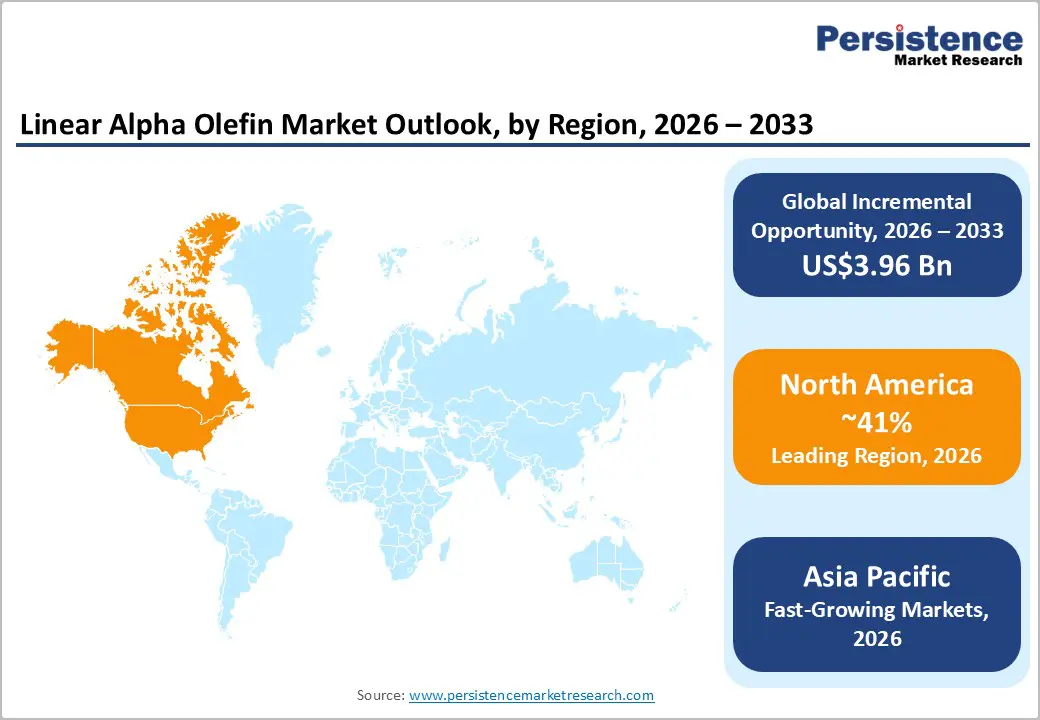

- Leading Region: North America dominates the global linear alpha olefin market, with 41% market share, due to world-class Gulf Coast infrastructure leveraging abundant shale gas-derived ethylene.

- Fastest Growing Region: Asia Pacific represents the fastest-expanding market at approximately 6.8% CAGR, driven by extensive polyethylene capacity additions in China, emerging demand growth in India, and integrated petrochemical infrastructure development.

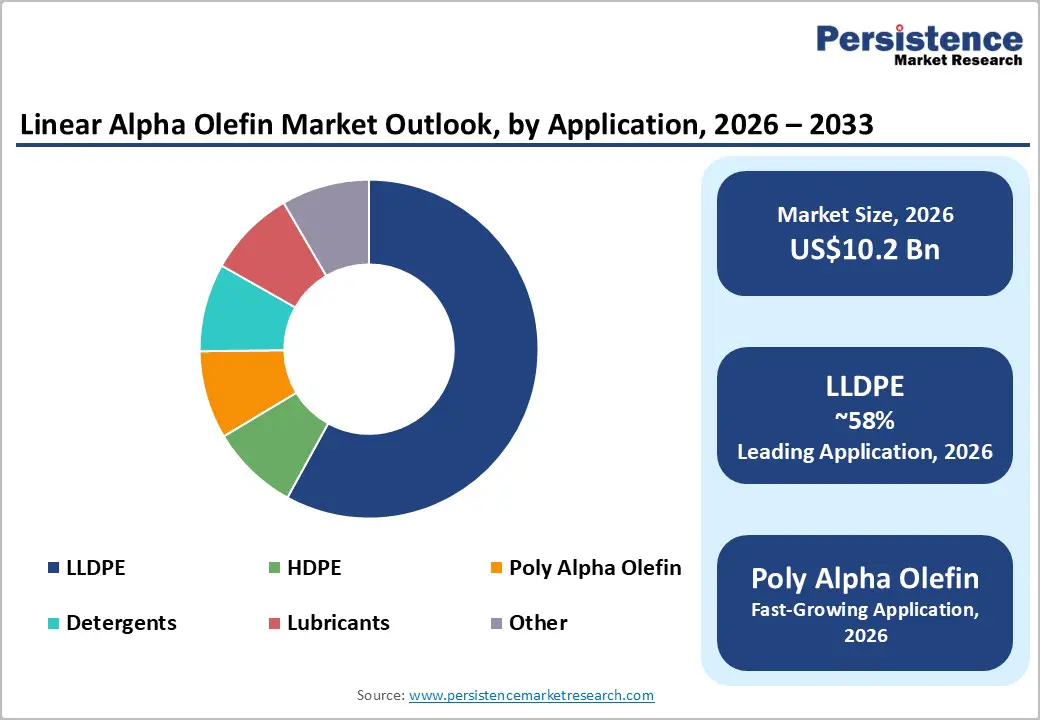

- Dominant Segment: LLDPE represents the largest application segment for linear alpha olefins, commanding approximately 58% of total market share due to widespread utilization across flexible packaging, agricultural films, and specialized coating applications.

- Fastest Growing Segment: 1-Hexene product type is expanding rapidly, driven by widespread utilization as a preferred co-monomer in LLDPE production and applications in synthetic lubricants and specialty chemicals.

- Key Market Opportunity: Development of bio-based linear alpha olefins and sustainable production technologies presents substantial growth potential, addressing environmental regulations, circular economy mandates, and consumer preferences while enabling premium positioning and differentiation in environmentally conscious market segments.

| Key Insights | Details |

|---|---|

|

Linear Alpha Olefin Size (2026E) |

US$ 10.2 Bn |

|

Market Value Forecast (2033F) |

US$ 14.2 Bn |

|

Projected Growth CAGR (2026-2033) |

4.8% |

|

Historical Market Growth (2020-2025) |

4.1% |

Market Dynamics

Market Growth Drivers

Escalating Demand for Linear Low-Density Polyethylene in Packaging Applications

The surging demand for Linear Low-Density Polyethylene (LLDPE) and High-Density Polyethylene (HDPE) in the packaging industry is a primary driver for the Linear Alpha Olefin market. Linear alpha olefins serve as critical comonomers in the production of LLDPE, which offers superior flexibility, impact resistance, and puncture strength compared to conventional low-density polyethylene. 1-Hexene and 1-Octene are critical comonomers used to enhance the mechanical properties of polyethylene, such as tear resistance, tensile strength, and flexibility.

As the global packaging sector shifts towards lightweight and durable materials for food and industrial packaging, the consumption of these high-performance polymers has accelerated. According to data from the American Chemistry Council, the production of polyethylene resins has seen consistent year-over-year growth, directly correlating to increased consumption of alpha olefins. The shift toward lightweight, cost-effective packaging solutions has further accelerated linear alpha olefin consumption across the packaging value chain.

Rising Demand for Synthetic Lubricants and Polyalphaolefin-Based Products

The automotive and industrial machinery sectors are increasingly adopting synthetic lubricants to meet stringent emission standards and improve fuel efficiency, driving demand for Poly Alpha Olefins (PAOs). The automotive industry's transition toward high-performance engines, including the growing adoption of electric vehicles requiring advanced lubricant formulations, has significantly boosted demand for PAO base stocks derived from higher-chain linear alpha olefins. Linear Alpha Olefins, specifically 1-Decene and 1-Dodecene, are the essential building blocks for manufacturing PAOs.

The Society of Automotive Engineers (SAE) notes a significant shift towards low-viscosity engine oils that reduce friction and improve engine longevity. Industrial applications, including compressor oils, turbine oils, and hydraulic fluids, have similarly contributed to robust market growth, with industrial synthetic lubricant consumption expanding in developed and emerging economies. These synthetic base stocks offer superior thermal stability, viscosity indices, and performance at extreme temperatures compared to mineral oils.

Market Restraints

Volatility in Raw Material Prices and Supply Chain Disruptions

The linear alpha olefin market faces significant challenges from fluctuating crude oil and ethylene prices, which directly impact production costs and profit margins for market participants. Ethylene, the primary feedstock for oligomerization-based linear alpha olefin production, exhibits price volatility influenced by global crude oil dynamics, regional naphtha versus ethane feedstock cost differentials, and supply disruptions from geopolitical events or production accidents. The recent volatility in energy markets and petrochemical feedstock costs has created uncertainty in the market, with crude oil price swings of 20-30% observed within short periods.

Geopolitical tensions and supply chain disruptions often lead to sharp spikes in feedstock costs, which can erode profit margins for manufacturers. For instance, data from the U.S. Energy Information Administration (EIA) illustrates historical variances in petrochemical feedstock prices, creating uncertainty for producers in long-term pricing strategies. This volatility forces companies to continuously adjust product pricing, potentially dampening demand from cost-sensitive downstream industries.

Stringent Environmental Regulations and Emissions Compliance Requirements

Increasing global emphasis on environmental sustainability and emissions reduction has imposed stringent regulatory requirements on linear alpha olefin production facilities. Regulatory bodies like the European Chemicals Agency (ECHA) under the REACH framework have imposed strict guidelines on the registration and safety assessment of chemical substances. While Linear Alpha Olefins themselves are intermediates, their primary end-use in single-use plastics places them under scrutiny.

Compliance with these regulations requires substantial capital investments in advanced catalytic systems, process modifications, and emission control technologies, which significantly increase operational costs for manufacturers. Environmental regulations restricting single-use plastics and mandating higher recycling standards have also dampened growth in certain packaging applications, particularly in developed regions.

Market Opportunities

Expansion of Bio-Based and Sustainable Linear Alpha Olefin Production

The development of bio-based linear alpha olefins presents a significant growth opportunity, driven by regulatory incentives and consumer demand for sustainable chemical products. Major chemical manufacturers, including Shell, BASF, and emerging biotech companies, are investing in alternative production pathways utilizing renewable feedstocks such as bio-ethanol and algae-derived ethylene. Bio-based linear alpha olefins offer substantially lower carbon footprints and reduced environmental impact compared to petroleum-derived alternatives.

Researchers and companies are exploring pathways to derive alpha olefins from renewable feedstocks such as plant oils or biomass, rather than fossil fuels. This shift aligns with the growing Functionalized Polyolefins Market trends where sustainable polymer modifiers are gaining traction. Establishing a foothold in bio-based production technologies can allow companies to charge a green premium and cater to the environmentally conscious consumer base, effectively future-proofing their product portfolios against fossil fuel volatility.

Growth in Advanced Polymer Applications and High-Performance Specialty Chemicals

Emerging applications within specialized polymer markets, such as functionalized polyolefins for automotive components, advanced packaging materials, and high-performance elastomers, are creating significant growth prospects for linear alpha olefins. The automotive industry’s transition toward lightweight materials to enhance fuel efficiency and reduce emissions has amplified the demand for customized polyethylene grades incorporating specific linear alpha olefin comonomers.

Furthermore, advanced applications in medical device packaging, which necessitate compliance with ISO 13485 standards, and specialized barrier films for protective purposes are expanding at an estimated annual rate of 6.8%. The development of specialty polyalphaolefins for precision engineering and high-temperature lubricant formulations in aerospace and industrial sectors represents an emerging segment with considerable value potential. Market participants that prioritize application-specific product innovation and provide comprehensive technical support are well-positioned to capitalize on substantial growth opportunities within these niche segments.

Category-wise Insights

Product Type Analysis

The 1-Hexene segment is expected to remain a dominant category within the product type landscape, accounting for approximately 28% of the market share. This leadership is primarily driven by its extensive use as a comonomer in the production of LLDPE and HDPE. Manufactured through ethylene trimerization and oligomerization processes, 1-Hexene is widely recognized as the preferred comonomer for LLDPE due to its optimal molecular structure, which ensures superior film properties at competitive cost levels.

Its excellent sealing capability and impact strength make it the material of choice for premium packaging films. Industry reports confirm that recent capacity expansions by leading players such as Chevron Phillips Chemical and Shell Chemicals have focused on 1-Hexene and 1-Octene technologies, reinforcing the segment’s strong growth trajectory.

Application Analysis

LLDPE represents the largest application segment for linear alpha olefins, commanding approximately 58% of total market share due to widespread utilization across flexible packaging, agricultural films, and specialized coating applications. The sustained growth in LLDPE demand is driven by e-commerce expansion, rising packaged food consumption, and increasing adoption of flexible plastic packaging across consumer goods industries globally. The material's high tensile strength and puncture resistance, derived from the incorporation of Linear Alpha Olefins, make it indispensable in the food packaging and construction industries.

Polyalphaolefin (PAO) applications in synthetic lubricants constitute the second-largest segment, supported by automotive industry requirements and industrial equipment maintenance standards. Detergent applications utilizing detergent-range linear alpha olefins for surfactant synthesis and biodegradable detergent alcohol production, with growth momentum driven by regulatory emphasis on biodegradable cleaning products.

Regional Insights

North America Linear Alpha Olefin Market Trends

North America continues to serve as a key global hub for linear alpha olefin production, with the U.S. Gulf Coast emerging as the primary manufacturing center due to its integrated petrochemical infrastructure and cost-efficient ethylene feedstock availability. Leading producers, including Chevron Phillips Chemical Company LLC, Shell Chemicals, and ExxonMobil Chemical Company, operate large-scale facilities in Texas and Louisiana, leveraging shale gas-derived ethane for competitive advantages.

The region benefits from strong domestic demand in packaging applications and significant export flows to the Asia-Pacific and Europe. Recent developments include Chevron Phillips Chemical’s completion of the world’s largest on-purpose hexene unit in Old Ocean, Texas (2023), and ExxonMobil’s polyalphaolefin capacity expansion at Baytown. Market growth, projected at 4.2% annually, is supported by sustainability-driven investments, regulatory compliance, and technological advancements.

Europe Linear Alpha Olefin Market Trends

The European linear alpha olefin market is defined by mature demand patterns and stringent environmental regulations that promote sustainable and bio-based production methods. Major consuming nations include Germany, France, Italy, and the United Kingdom, supported by established polyethylene processors and automotive lubricant manufacturers. Regulatory frameworks such as REACH compliance, Ecolabel certification for detergents, and mandatory emissions reduction standards have driven investments in sustainable technologies and bio-based feedstocks.

Demand for biodegradable surfactants in cleaning and cosmetic applications continues to grow, with detergent-range alpha olefins commanding premium prices over commodity grades. Although annual growth is projected at 3.8%, expansion is constrained by mature LLDPE consumption and demographic trends. Nevertheless, opportunities exist in specialty applications, sustainability-focused product development, and integration with functionalized polyolefins, particularly in Benelux and Central European industrial hubs.

Asia Pacific Linear Alpha Olefin Market Trends

Asia-Pacific is projected to be the fastest-growing regional market for linear alpha olefins, driven by rapid industrialization, expansion of the packaging sector, and significant polyethylene capacity additions across China, India, and Southeast Asia. China’s commissioning of approximately 11.5 million tonnes per year of new polyethylene capacity during 2025–2026 will substantially increase demand for alpha olefins in comonomer applications, with domestic producers pursuing import substitution strategies to enhance self-sufficiency.

India’s petrochemical growth, supported by government initiatives such as PCPIRs and major investments by Reliance Industries Limited and Indian Oil Corporation Limited, is further accelerating LLDPE production and downstream olefin requirements. The region’s annual growth rate of 6.2% surpasses global averages, supported by rising consumer goods consumption, e-commerce expansion, and automotive development, while Japan and South Korea maintain technology-driven markets emphasizing advanced polymers and synthetic lubricants.

Competitive Landscape

The global linear alpha olefin market exhibits moderate consolidation, with a significant share concentrated among integrated petrochemical companies possessing ethylene production capabilities, advanced oligomerization technologies, and established downstream relationships. Leading players such as ExxonMobil Chemical Company, Chevron Phillips Chemical Company LLC, Shell Chemicals, and SABIC collectively account for nearly 42–45% of global production capacity, leveraging technology leadership and integrated platforms. Mid-tier competitors, including INEOS Oligomers, Sasol Limited, and Evonik Industries AG, maintain strong positions through specialized technologies and regional optimization strategies. Competitive differentiation increasingly focuses on selective oligomerization processes to enhance yield and product quality, sustainable and bio-based production pathways, and robust technical support for downstream applications. Recent trends highlight digital process optimization, AI-driven plant control systems, and strategic partnerships promoting circular economy initiatives and polymer recycling technologies.

Key Market Developments

- February, 2025: Chevron Phillips Chemical revealed a partnership to develop bio-based alpha olefins using algae-derived ethylene, aligning with global sustainability goals.

- August 2023: Chevron Phillips Chemical Company LLC completed construction of the world's largest on-purpose 1-hexene production unit in Old Ocean, Texas, with operational commencement scheduled for September 2023, significantly expanding capacity for LLDPE comonomer supply to North American and export markets.

Top Companies in Linear Alpha Olefin Market

Shell Chemicals (U.K.) is a global leader with massive integrated production sites, particularly in Geismar, Louisiana. The company leverages its proprietary Shell Higher Olefin Process (SHOP) to produce a wide range of alpha olefins and is aggressively expanding capacity to meet North American demand.

Chevron Phillips Chemical Company LLC (U.S.) holds a dominant position, especially in the production of 1-Hexene via its proprietary on-purpose technology. The company acts as a critical supplier to the global polyethylene industry and maintains a strong export network from its US Gulf Coast facilities.

Sasol Ltd. (South Africa) is a key player known for its unique coal-to-liquids technology that yields alpha olefins. Sasol has a strong presence in the comonomer market and has successfully internationalized its operations with significant investments in North America, focusing on 1-Octene and 1-Hexene production.

Companies Covered in Linear Alpha Olefin Market

- ExxonMobil Chemical Company

- Chevron Phillips Chemical Company LLC

- SABIC

- INEOS Group

- Shell Chemicals

- Sasol Ltd.

- Evonik Industries AG

- Dow Chemical Company

- Linde Plc

- Qatar Chemical Company Ltd.

- Reliance Industries Ltd.

- Indian Oil Corporation Ltd.

Frequently Asked Questions

The global Linear Alpha Olefin market is projected to reach US$ 14.2 Bn by 2033, growing at a CAGR of 4.8% from 2026 to 2033, driven by expanding polyethylene production, synthetic lubricants demand, and specialty chemical applications.

The market is primarily driven by escalating demand for LLDPE and HDPE as co-monomers in polyethylene production for packaging and construction applications, coupled with rapid expansion of high-performance PAO-based synthetic lubricants in automotive and industrial sectors requiring superior thermal stability and viscosity characteristics.

The LLDPE (Linear Low-Density Polyethylene) segment is the dominant application, accounting for the largest share of global consumption.

North America is the leading region, largely due to its massive production capacity supported by advantaged shale gas feedstocks.

Developing bio-based Linear Alpha Olefins to meet the rising consumer and regulatory demand for sustainable chemicals presents a major opportunity.