- Pharmaceuticals

- Allergy Shots Market

Allergy Shots Market Size, Share, and Growth Forecast 2026 - 2033

Allergy Shots Market by Product (SLIT Tablets, Oral Immunotherapy, Subcutaneous Injections, Others), by Indication (Allergic Rhinitis, Allergic Asthma, Food Allergy, Atopic Dermatitis, Venom Allergy), by Allergen (Pollen, House Dust Mites, Mold, Animal Dander, Insect Venom), by Distribution Channel (Institutional Sales, Retail Sales, Others), by Regional Analysis, 2026-2033

Allergy Shots Market Size and Trend Analysis

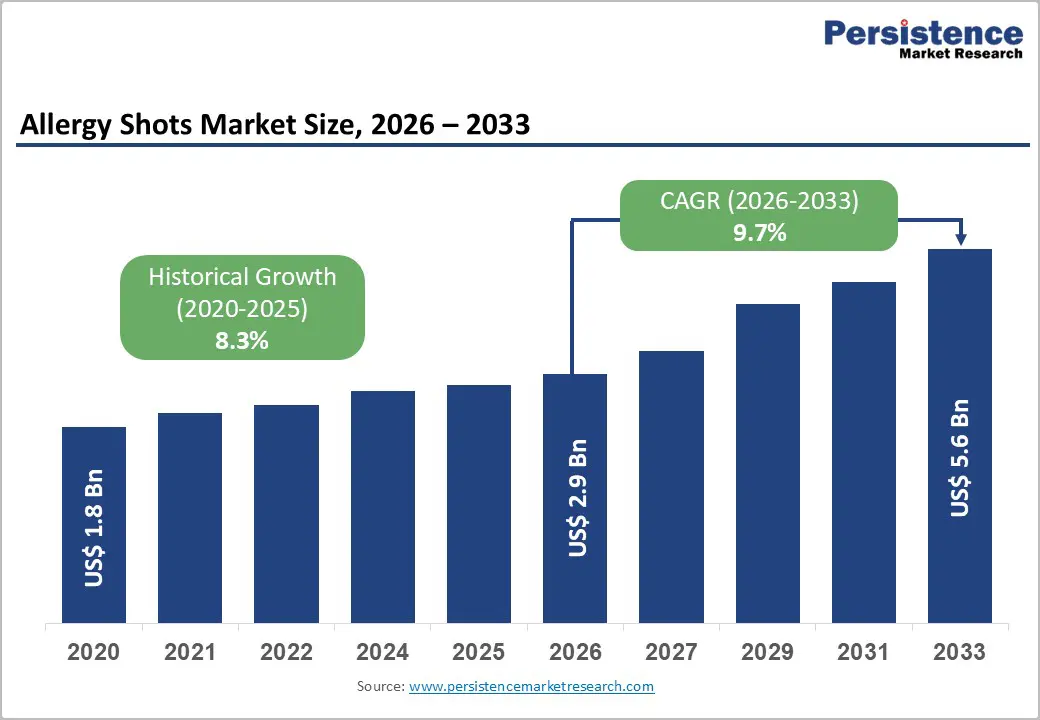

The global allergy shots market size is expected to be valued at US$ 2.9 billion in 2026 and projected to reach US$ 5.6 billion by 2033, growing at a CAGR of 9.7% between 2026 and 2033.

The market expansion is driven by a confluence of three critical factors that strengthen market fundamentals. First, the rising global prevalence of allergic diseases, with allergic rhinitis affecting 15-25% of the population in developed nations creates sustained demand for immunotherapy solutions that offer disease-modifying effects beyond symptomatic relief. Second, regulatory approvals of innovative SLIT tablets and oral immunotherapy products, including FDA-approved formulations like Odactra, Grastek, Ragwitek, Oralair, and Palforzia, have established clinical credibility and expanded treatment accessibility. Third, clinical evidence demonstrating 30% greater symptom reduction and 40% reduction in rescue medication use compared to standard pharmacotherapy provides compelling economic justification for healthcare systems to prioritize immunotherapy adoption.

Key Market Highlights

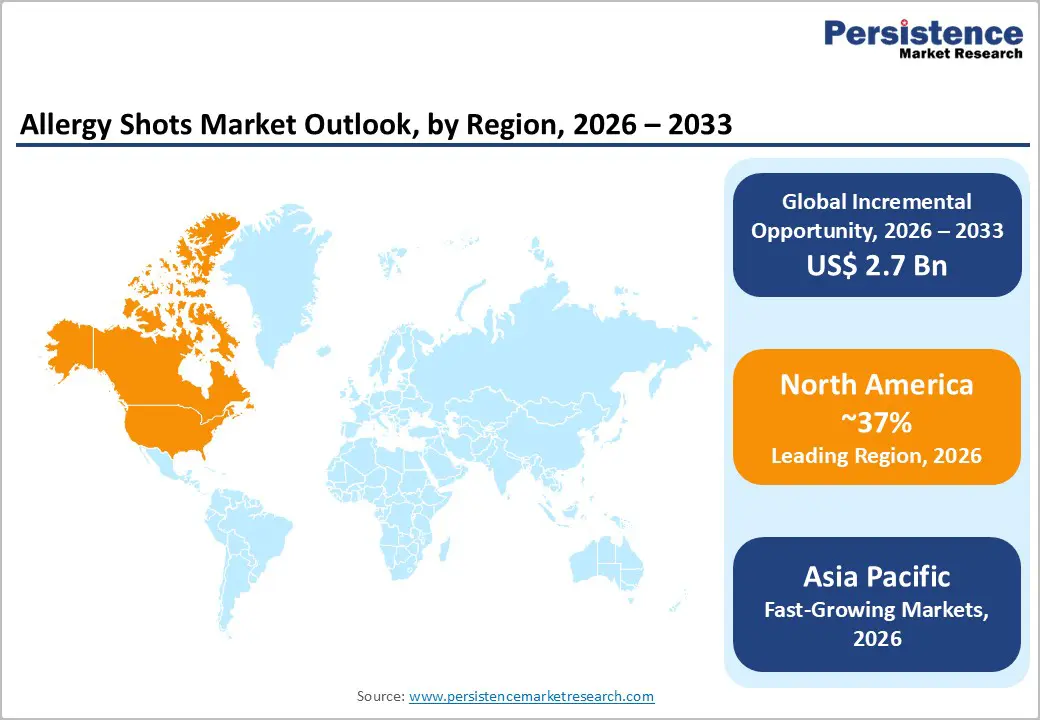

- Leading Region: North America controls 37% global market share in 2025, driven by advanced healthcare infrastructure, 100+ million annually-affected allergy patients, comprehensive FDA-approved immunotherapy product portfolio, and established reimbursement frameworks supporting clinical adoption across specialty allergy centers and multidisciplinary treatment settings.

- Fastest Growing Region: Asia-Pacific demonstrates 12.4% CAGR through 2033, propelled by rapid urbanization, rising allergic disease prevalence across China and India, Japanese government initiatives supporting immunotherapy expansion, and emerging manufacturing capacity establishing regional competitive advantages.

- Dominant Segment: Sublingual immunotherapy tablets command 55% market share in 2025, supported by FDA-approved formulations including Odactra, Grastek, Oralair, and Ragwitek, superior patient preference over injections, clinical efficacy comparable to subcutaneous immunotherapy, and improved treatment adherence in pediatric populations.

- Fastest Growing Segment: Food allergy immunotherapy expands at 12.8% CAGR through 2033, driven by Palforzia FDA approval establishing commercialization precedent, escalating pediatric food allergy prevalence globally, parental demand for anaphylaxis prevention alternatives, and robust clinical pipeline targeting multiple allergens.

- Key Market Opportunity: Epicutaneous immunotherapy platforms validated through Phase 3 clinical success offer non-invasive delivery reducing clinical supervision requirements, enhancing pediatric treatment accessibility, establishing potential home-based administration protocols, and expanding addressable patient populations to previously treatment-refractory groups.

| Global Market Attributes | Key Insights |

|---|---|

| Allergy Shots Market Size (2026E) | US$ 2.9 billion |

| Market Value Forecast (2033F) | US$ 5.6 billion |

| Projected Growth CAGR(2026-2033) | 9.7% |

| Historical Market Growth (2020-2025) | 8.3% |

Market Dynamics

Market Growth Drivers

Increasing Prevalence of Allergic Diseases and Shift Toward Disease-Modifying Therapies

The escalating burden of allergic diseases globally represents the primary growth catalyst for the allergy shots market. According to clinical research, allergic rhinitis prevalence ranges between 15-25% in developed countries, with documented increases in developing regions driven by urbanization and climate change. The World Allergy Organization recognizes allergen-specific immunotherapy as the only form of treatment capable of modifying the natural course of allergic diseases, positioning it as a superior alternative to symptomatic medications. Clinical evidence demonstrates that immunotherapy reduces symptom severity by 30% compared to placebo and decreases rescue medication consumption by 40%, delivering sustained benefits even after treatment cessation. Furthermore, immunotherapy can prevent progression to allergic asthma in allergic rhinitis patients and reduce new allergen sensitization risk, offering long-term disease modification that extends treatment value beyond immediate symptom relief and justifies healthcare investments in allergen-specific approaches.

Regulatory Approvals and Expanding Product Portfolio Driving Clinical Adoption

The regulatory landscape has undergone significant transformation with FDA approval of multiple sublingual immunotherapy tablets, creating validated pathways for market expansion and clinical standardization. Merck's Odactra (house dust mite extract) received FDA approval for patients aged 12-65 years, establishing safety and efficacy standards for sublingual immunotherapy in allergic rhinitis. Similarly, Stallergenes Greer's Grastek (timothy grass), ALK Abello's Oralair (mixed grass pollens), and Merck's Ragwitek (ragweed) have established regulatory precedent and reimbursement frameworks across North America and Europe. Additionally, Aimmune Therapeutics' Palforzia achieved breakthrough status as the first FDA-approved oral immunotherapy for peanut allergy, validating food allergy immunotherapy pathways and generating pediatric market opportunities. The clinical pipeline continues expanding with emerging platforms, including epicutaneous immunotherapy technologies, positioning the market for accelerated growth as regulatory approvals translate into broader healthcare integration and insurance coverage expansion.

Market Restraints

Challenges in Allergen Extract Standardization and Variable Clinical Trial Design Requirements

Despite therapeutic promise, the market faces significant constraints related to allergen standardization and regulatory complexity. The lack of universally accepted standards for allergen extracts, particularly for house dust mite preparations, where extracts are conventionally standardized by skin prick test reactivity rather than allergen content, creates inconsistencies in product potency and clinical efficacy. European Medicines Agency and FDA requirements for clinical development differ substantially across regions, necessitating region-specific trials and increasing development timelines and costs. Additionally, the heterogeneity of patient populations, allergen exposure variability, and complex statistical requirements for clinical trials (requiring 10-15% efficacy above 95% confidence intervals versus 5% for conventional medications) impose substantial regulatory barriers. These factors collectively increase time-to-market and development costs, limiting smaller pharmaceutical companies' ability to bring innovative immunotherapy products to market and restricting therapeutic options in underpenetrated geographic regions.

Adverse Event Profile and Patient Adherence Challenges in Long-Term Immunotherapy

Although sublingual immunotherapy demonstrates superior safety relative to subcutaneous injections, primarily manifesting as local oromucosal reactions, systemic hypersensitivity reactions remain clinically significant concerns limiting broader adoption. Subcutaneous immunotherapy continues to require clinic-based administration and carries documented risks of anaphylaxis at rates of approximately 1 per 2.5 million injections, necessitating clinical supervision and emergency preparedness. Long-term immunotherapy requires sustained patient adherence across 3-5 year treatment protocols, with substantial dropout rates occurring in both subcutaneous and sublingual regimens due to perceived inconvenience, cost barriers, and delayed onset of clinical benefits. These adherence challenges disproportionately affect pediatric populations despite efficacy advantages, ultimately reducing market penetration and treatment success rates even in healthcare systems with favorable reimbursement structures.

Market Opportunities

Expansion of Food Allergy Immunotherapy and Pediatric Treatment Paradigm Shifts

Food allergy immunotherapy represents the market's highest-potential growth segment, driven by escalating pediatric food allergy prevalence and validated clinical evidence from recent regulatory approvals. Aimmune Therapeutics' Palforzia commercialization has established proof-of-concept for oral immunotherapy, with clinical data demonstrating dose-dependent desensitization in 82.7% of treated pediatric patients compared to placebo. The peanut allergy segment alone is projected to expand at 7.5-9.1% CAGR across North America and Europe through 2035, driven by childhood prevalence rates and parental demand for proactive allergy management alternatives to strict avoidance protocols. Pipeline candidates targeting egg, milk, and multi-allergen protocols are advancing through clinical development, with multiple Phase II and Phase III trials underway across North America and Europe. Multidisciplinary care integration—incorporating allergists, pediatric specialists, and immunology experts into coordinated treatment protocols—enhances clinical outcomes and patient adherence, creating institutional revenue opportunities for specialty care providers and establishing sustainable market models for food allergy immunotherapy expansion.

Category-wise Insights

Product Analysis

Sublingual immunotherapy tablets represent the dominant product segment, commanding approximately 55% market share in 2025, reflecting FDA approval of multiple platforms and superior patient preference relative to subcutaneous injections. FDA-approved SLIT tablets including Odactra (house dust mite), Grastek (timothy grass), Oralair (mixed grass pollens), and Ragwitek (ragweed) have established clinical efficacy and reimbursement frameworks across North America. Clinical evidence demonstrates that SLIT offers comparable efficacy to subcutaneous immunotherapy for pediatric allergic rhinitis with significantly superior safety profiles, predominantly manifesting local oromucosal reactions rather than systemic hypersensitivity. The segment's leadership reflects growing demand for home-based administration, elimination of needle-related anxiety in pediatric populations, and improved treatment adherence. Furthermore, expansion into oral immunotherapy formats, exemplified by Palforzia for peanut allergy, is rapidly capturing market share in food allergy indications, positioning oral formulations as the fastest-growing product subcategory with projected 11.2% CAGR through 2033. Institutional and retail pharmacy distribution channels increasingly stock SLIT formulations due to simplified handling requirements and growing specialist-led prescribing patterns, further consolidating product segment leadership.

Indication Analysis

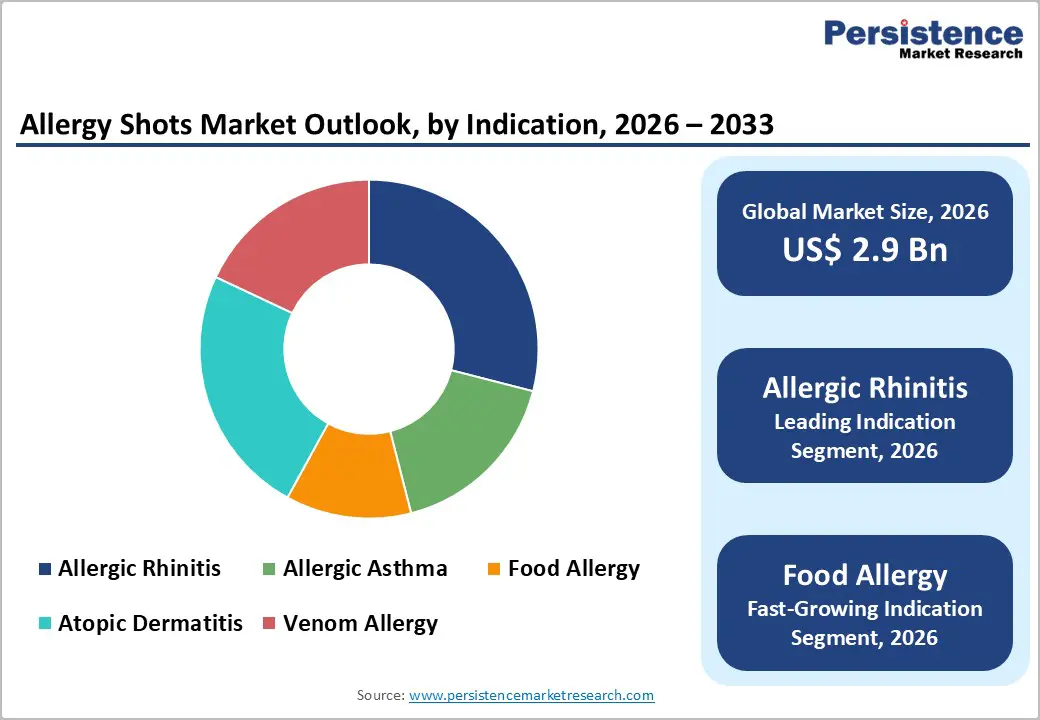

Allergic rhinitis dominates the allergy shots market with 29% market share in 2025, reflecting the condition's high global prevalence (15-25% in developed populations) and established clinical evidence supporting immunotherapy efficacy. This indication benefits from decades of clinical validation, with documented 30% symptom reduction and 40% medication reduction compared to placebo across randomized controlled trials. FDA-approved products specifically targeting allergic rhinitis, including Odactra, Grastek, Oralair, and Ragwitek, have established reimbursement precedent and specialist prescribing patterns across North America and Europe. Healthcare systems recognize cost-effectiveness of immunotherapy relative to 10-15 year lifetime management with intranasal corticosteroids and antihistamines, driving insurance coverage and institutional adoption.

Distribution Channel Analysis

Institutional sales, encompassing specialty allergy clinics, hospital immunotherapy centers, and academic medical centers, represent the dominant distribution channel with approximately 62% market share in 2025, reflecting the clinical supervision and specialized expertise requirements for immunotherapy initiation and maintenance. These channels benefit from established multidisciplinary care protocols, emergency medical support infrastructure, and integrated electronic health records systems facilitating treatment adherence monitoring. Institutional channels provide optimal environments for patient education regarding adverse event management and long-term immunotherapy benefits, resulting in superior treatment persistence relative to retail pharmacy-based dispensing.

Regional Insights

North America Allergy Shots Market Trends and Insights

North America maintains leadership in the allergy shots market with 37% global market share in 2025, driven by advanced healthcare infrastructure, favorable reimbursement mechanisms, and a comprehensive FDA approval landscape. The region benefits from the highest concentration of allergists, immunology specialists, and multidisciplinary allergy care centers globally, facilitating rapid clinical adoption of innovative immunotherapy platforms. FDA-approved SLIT tablets, including Odactra, Grastek, Oralair, and Ragwitek, command significant prescription volumes supported by insurance reimbursement frameworks and clinical guidelines established by the American Academy of Allergy, Asthma & Immunology and Asthma and Allergy Foundation of America.

The United States market specifically commands 64% of North American allergy shots revenues, driven by the region's estimated 100+ million people annually experiencing allergic conditions requiring immunotherapy evaluation.

Asia Pacific Allergy Shots Market Trends and Insights

Asia-Pacific emerges as the fastest-growing regional market with projected 12.4% CAGR through 2033, driven by rapid urbanization, rising allergic disease prevalence, and expanding pharmaceutical manufacturing capacity in key markets. The Japanese government announced strategic initiatives to promote allergen immunotherapy adoption by supporting SLIT utilization expansion, targeting fourfold increase in immunotherapy supply through 2028 and positioning the region as an emerging manufacturing hub for allergen products. China and India represent substantial untapped market opportunities, with rising middle-class populations and improving healthcare infrastructure supporting specialist allergy care expansion and pharmaceutical product accessibility.

Immunotherapy adoption patterns in Asia-Pacific reflect distinct regional dynamics, with Japan demonstrating mature market characteristics comparable to Western Europe, while China, India, and ASEAN countries represent emerging growth markets with nascent immunotherapy infrastructure. Clinical trial expansion across Asia-Pacific, particularly in India and China, is accelerating pharmacokinetic and safety data generation for regional populations, supporting regulatory approval pathways and market entry for Western pharmaceutical manufacturers. Rising air pollution levels in major metropolitan areas across China and India are driving allergic rhinitis prevalence increases, creating sustained demand for disease-modifying immunotherapy approaches. Manufacturing cost advantages and regulatory pathway streamlining in India are attracting investment from multinational pharmaceutical companies developing allergen extract platforms, positioning the region for incremental manufacturing capacity expansion and improved product accessibility across South and East Asia through 2035.

Competitive Landscape

Market Structure Analysis

The competitive landscape of the Allergy Shots Market is moderately concentrated and dynamic. Long-standing immunotherapy innovators compete with specialized biotech firms in developing more effective, standardized treatments and expanding geographic reach. Competition centers on research & development, novel delivery methods, regulatory approvals, and strategic alliances to broaden portfolios and improve patient adherence. Companies are increasingly investing in biologics, recombinant allergen technologies, and digital health integration to differentiate offerings.

Key Market Developments

- In January 2026, UK-listed Allergy Therapeutics announced that its grass pollen allergy treatment, Grassmuno, had received approval in Germany, marking the company’s first commercial market and setting the stage for a launch planned for early the following year. Grassmuno, also known as Grass MATA MPL, became the first subcutaneous grass pollen allergy immunotherapy to be cleared by the Paul Ehrlich Institute (PEI), Germany’s medicines regulator, under the Therapieallergene-Verordnung (TAV) regulatory framework, representing a significant regulatory milestone for the company.

Companies Covered in Allergy Shots Market

- ALK Abello

- Stallergenes Greer

- Allergy Therapeutics

- Aimmune Therapeutics

- Anergis

- Arrayit Corporation

- Biomay AG

- HAL Allergy Group

- DBV Technologies

Frequently Asked Questions

The global allergy shots market is projected to reach US$ 2.9 billion in 2026, growing from US$ 1.8 billion in 2020, representing an 8.3% historical CAGR and validating sustained pharmaceutical investment in immunotherapy innovations and clinical evidence generation across allergen-specific treatment modalities.

The market is driven by three critical factors: escalating global allergic disease prevalence affecting 15-25% of developed populations, FDA and EMA approval of innovative SLIT tablets and oral immunotherapy platforms establishing clinical credibility and reimbursement frameworks.

North America commands 37% global market share in 2025, driven by advanced healthcare infrastructure, the highest concentration of allergist specialists globally.

Epicutaneous immunotherapy platforms, exemplified by DBV Technologies' VIASKIN patch technology, represent transformative opportunities offering non-invasive allergen delivery, reduced clinical supervision requirements, enhanced pediatric treatment accessibility, and home-based administration potential. Phase 3 clinical evidence demonstrates 46.6% response rates with superior safety profiles, with FDA BLA submission planned for the first half 2026.

ALK Abello, Stallergenes Greer, Allergy Therapeutics, Aimmune Therapeutics, etc.