- Pharmaceuticals

- Peanut Allergy Treatment Market

Peanut Allergy Treatment Market Size, Share, and Growth Forecast, 2026 - 2033

Peanut Allergy Treatment Market by Drug Type (Injectable Epinephrine, Antihistamines), Route of Administration (Oral, Injectable), Distribution Channel (Retail Pharmacies, Hospital Pharmacies, Online Pharmacies, Drug Store), and Regional Analysis for 2026 - 2033

Peanut Allergy Treatment Market Size and Trends Analysis

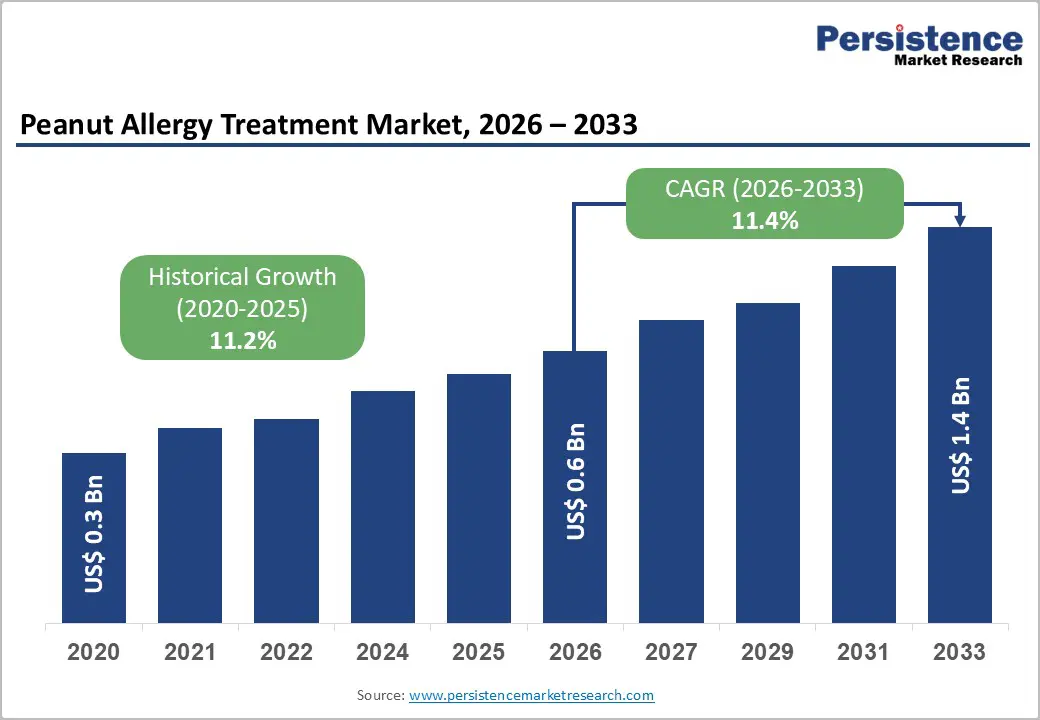

The global peanut allergy treatment market size is likely to be valued at US$0.6 billion in 2026 and is expected to reach US$1.4 billion by 2033, growing at a CAGR of 11.4% during the forecast period from 2026 to 2033, driven by the increasing prevalence of peanut allergies, particularly among children, and the growing recognition of food allergies as a significant public health concern.

Rising awareness among patients, caregivers, and healthcare professionals has led to improved diagnosis rates and early intervention, thereby expanding the patient pool requiring treatment. The market is evolving from traditional emergency management approaches, such as the use of epinephrine and antihistamines for acute allergic reactions, toward more advanced and disease-modifying therapies. Innovations in immunotherapy, including oral and epicutaneous approaches, are gaining traction as they aim to reduce sensitivity and provide long-term protection rather than just symptom control. Advancements in biologics targeting immune pathways are transforming the treatment landscape. Distribution channels are also adapting, with increased availability through retail and online pharmacies improving patient convenience and adherence.

Key Industry Highlights:

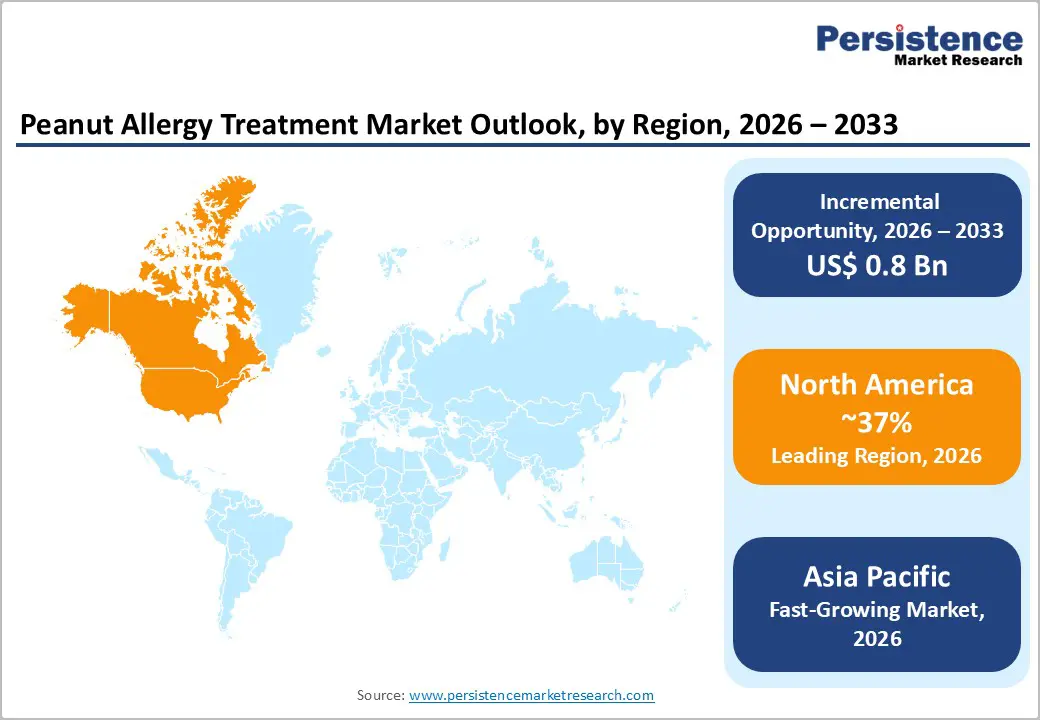

- Leading Region: North America is anticipated to be the leading region, accounting for 37% market share in 2026, driven by strong healthcare infrastructure, high awareness, and continuous innovation in allergy therapeutics.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, supported by expanding healthcare access, rising awareness, and strong regional manufacturing capabilities.

- Leading Drug Type: Injectable epinephrine is projected to be the leading drug type in 2026, accounting for 46% of revenue share, driven by its role as the primary life-saving treatment for severe allergic reactions and its widespread clinical adoption.

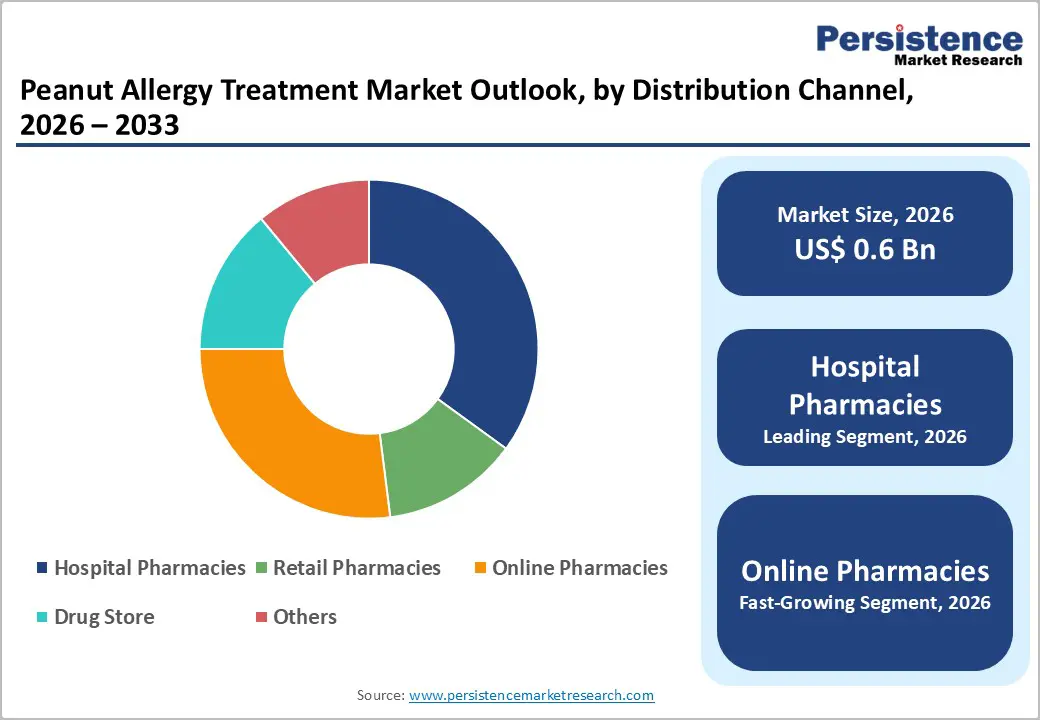

- Leading Distribution Channel: Hospital pharmacies are expected to be the leading application, accounting for over 55% of revenue in 2026, supported by their critical role in managing severe cases and providing supervised access to treatment.

| Key Insights | Details |

|---|---|

|

Peanut Allergy Treatment Market Size (2026E) |

US$0.6 Bn |

|

Market Value Forecast (2033F) |

US$1.4 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

11.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

11.2% |

DRO Analysis

Driver - Rising Prevalence of Peanut Allergies and Improved Diagnosis Rates

The increasing incidence of peanut allergies, particularly among children, is a major factor driving increased treatment demand. Changes in dietary habits, environmental factors, and genetic predisposition have all contributed to higher allergy rates. Improved awareness among parents and healthcare providers has led to earlier recognition of symptoms and increased clinical consultations. A larger patient population is being diagnosed and managed, creating sustained demand for both emergency and long-term therapeutic solutions in clinical and home care settings.

Advancements in diagnostic technologies and standardized clinical guidelines have strengthened early detection and accurate classification of allergy severity. Skin prick tests, blood-based IgE testing, and oral food challenges are increasingly accessible, especially in urban healthcare systems. Government initiatives and awareness campaigns have also encouraged routine screening in high-risk populations. This growing diagnostic infrastructure not only supports timely intervention but also enables better patient monitoring, thereby driving consistent demand for treatment products and improving overall disease management outcomes across healthcare systems.

Advancements in Therapeutic Options and Product Pipeline

Continuous innovation in treatment approaches is significantly transforming the landscape of peanut allergy management. Traditional therapies focused on emergency symptom control, but recent developments emphasize long-term desensitization and immune modulation. Oral immunotherapy and emerging epicutaneous treatments are designed to gradually increase tolerance, reducing the severity of allergic reactions. These advancements provide patients with improved quality of life and reduced anxiety associated with accidental exposure, thereby increasing acceptance and adoption of newer therapeutic options.

A strong and evolving product pipeline is supporting market growth, with ongoing clinical trials exploring biologics and targeted immune therapies. These next-generation treatments aim to modify the immune response at a molecular level, offering more effective and personalized care. Increased investment from pharmaceutical and biotechnology companies, along with favorable regulatory pathways, is accelerating product approvals. This innovation-driven environment is fostering competition and expanding available treatment choices, ultimately strengthening the overall therapeutic ecosystem and addressing unmet clinical needs.

Restraint - Complex Clinical Monitoring and Safety Management

Management of peanut allergy treatments, particularly immunotherapies, requires careful clinical supervision due to potential adverse reactions. Patients undergoing desensitization therapies must be closely monitored during dose-escalation phases, often in controlled healthcare settings. This complexity increases the burden on healthcare providers and may limit patient access in regions with limited medical infrastructure. Strict adherence to treatment protocols is essential to ensure safety, but this requirement makes the process time-intensive and challenging for both patients and clinicians.

Safety concerns about allergic reactions during treatment can also affect patient confidence and compliance. Even minor deviations in dosage or exposure can trigger symptoms, underscoring the need for emergency preparedness at all times. Healthcare professionals must provide extensive patient education and continuous follow-up, which can strain resources. These factors contribute to slower adoption of advanced therapies in certain regions and highlight the need for simplified treatment protocols and improved safety profiles to enhance patient accessibility and overall treatment effectiveness.

Limited Shelf Life and Stability Issues in Plant-Based Formulations

Certain peanut allergy therapies, particularly those involving biologically derived or plant-based components, face challenges related to stability and shelf life. These formulations require specific storage conditions, such as controlled temperatures, to maintain their effectiveness. Any deviation from recommended storage guidelines can compromise product quality and reduce efficacy. This creates logistical challenges in distribution, especially in regions with limited cold-chain infrastructure, thereby affecting the consistent availability of treatments.

A short shelf life also increases the risk of product waste and raises overall healthcare costs. Pharmacies and healthcare providers must carefully manage inventory to avoid expired products, which can complicate supply chain operations. Patients may find it inconvenient to maintain proper storage conditions at home. Addressing these stability concerns through improved formulation technologies and packaging solutions is essential to ensure reliable treatment delivery and broader accessibility across diverse geographic and economic settings.

Opportunity - Expansion of Immunotherapies into Broader Age Groups and Indications

Immunotherapy is increasingly being explored beyond pediatric populations, creating opportunities for expansion into adolescent and adult patient groups. Historically, treatment approaches have focused on children due to the early onset of peanut allergies, but growing clinical evidence supports the effectiveness of therapies across wider age ranges. This expansion significantly increases the addressable patient population and enhances market potential by providing solutions tailored to different life stages.

Ongoing research is evaluating the application of immunotherapy for multiple food allergies and related conditions, broadening its therapeutic scope. This diversification allows healthcare providers to adopt more comprehensive treatment strategies that address co-existing allergies in a single approach. Increased regulatory approvals and clinical validation of these extended indications are expected to drive adoption, improve patient outcomes, and strengthen immunotherapy's role as a cornerstone in allergy management.

Integration of Biologics and Personalized Treatment Pathways

The integration of biologic therapies into peanut allergy treatment represents a significant advancement toward precision medicine. Biologics target specific immune pathways involved in allergic reactions, offering more effective and tailored treatment options. These therapies can be used alone or in combination with immunotherapy to enhance safety and efficacy. By addressing the underlying immune response, biologics provide long-term benefits and reduce the frequency and severity of allergic episodes.

Personalized treatment approaches are gaining importance as patient variability in allergy severity and response to therapy becomes better understood. Advances in biomarker identification and genetic profiling enable clinicians to design customized treatment plans that optimize outcomes. This shift toward individualized care improves patient adherence and satisfaction while minimizing risks. As healthcare systems increasingly adopt precision medicine frameworks, the integration of biologics and personalized pathways is set to unlock new growth opportunities and redefine the future of peanut allergy management.

Category-wise Analysis

Drug Type Insights

Injectable epinephrine is expected to lead the peanut allergy treatment market, accounting for approximately 46% of revenue in 2026, driven by its rapid onset of action and life-saving capability, making it indispensable for individuals diagnosed with peanut allergies. Clinical guidelines strongly recommend that at-risk patients carry epinephrine auto-injectors at all times, ensuring consistent demand across both hospital and retail settings. Healthcare providers prioritize its prescription due to proven efficacy and regulatory approvals supporting its widespread use. For example, products such as EpiPen are commonly prescribed and widely recognized as essential first-line treatments, highlighting the critical role of injectable epinephrine in managing acute allergic emergencies.

Antihistamines are likely to represent the fastest-growing segment, supported by their supportive role in managing mild to moderate allergic symptoms and their increasing use alongside advanced therapies. While they do not replace emergency treatments, their inclusion in comprehensive allergy management plans has expanded significantly. Growing awareness about early symptom control and preventive care has encouraged patients to adopt antihistamines as part of routine treatment strategies. For example, commonly used antihistamines such as cetirizine are widely utilized to relieve symptoms such as itching and swelling, supporting their role in day-to-day allergy management.

Distribution Channel Insights

Hospital pharmacies are projected to lead the market, capturing around 55% of revenue in 2026, supported by their central role in managing severe allergic reactions and initiating advanced therapies under medical supervision. These facilities are closely integrated with emergency departments and allergy specialists, enabling immediate access to critical treatments such as epinephrine during life-threatening situations. For example, patients experiencing severe allergic reactions are typically treated in hospital emergency units, where epinephrine is administered promptly.

Online pharmacies are likely to be the fastest-growing distribution channel, driven by increasing digital adoption and the convenience of accessing medications from home. Patients managing chronic conditions such as peanut allergies often require repeat prescriptions, making online platforms an efficient option for purchasing essential treatments. The rise of e-commerce in healthcare, coupled with improved logistics and doorstep delivery services, has significantly enhanced accessibility. For example, platforms such as PharmEasy allow patients to order epinephrine auto-injectors and antihistamines conveniently, reducing dependency on physical pharmacy visits.

Regional Insights

North America Peanut Allergy Treatment Market Trends

North America is projected to lead the peanut allergy treatment market, accounting for 37% of global share in 2026, supported by high prevalence rates, advanced healthcare infrastructure, and strong awareness across the U.S. and Canada. According to the Centers for Disease Control and Prevention and Food Allergy Research & Education, peanut allergy affects approximately 1–2% of the U.S. population. Overall, more than 32 million Americans have food allergies, including nearly 6 million children, sustaining demand for both emergency and long-term treatments.

The region also benefits from early diagnosis, widespread access to allergists, and advanced diagnostic tools such as IgE testing and oral food challenges. Clinical guidelines from the American College of Allergy, Asthma & Immunology ensure standardized and effective treatment protocols. North America also leads in innovation, with the U.S. Food and Drug Administration enabling faster approvals of therapies such as oral immunotherapy, accelerating the shift toward disease-modifying treatments. Epinephrine auto-injectors remain the primary solution for acute reactions, while immunotherapies and biologics are gaining adoption for long-term desensitization. Strong reimbursement systems and expanding online pharmacy channels further enhance treatment access and adherence, reinforcing the region’s market leadership.

Europe Peanut Allergy Treatment Market Trends

Europe is likely to be a significant market for peanut allergy treatment, driven by increasing prevalence, expanding clinical awareness, and strengthened regulatory frameworks that enable access to structured therapies. While emergency treatments such as epinephrine auto-injectors remain widely used, immunotherapy approaches targeting desensitization are gaining relevance as part of long-term management strategies. For example, DBV Technologies, a French biotech developing Viaskin Peanut, a skin patch immunotherapy designed to help patients gradually build tolerance by delivering controlled exposure to peanut protein through the skin.

Growth is also supported by pan-European clinical guidelines and allergy support networks that improve the detection and monitoring of peanut allergy cases. Integration of allergists into care pathways enhances treatment personalization, while insurance and reimbursement mechanisms in many EU countries facilitate access to both acute and chronic care solutions. Collaborative efforts between healthcare providers and industry players are expanding distribution channels and bolstering patient education initiatives.

Asia Pacific Peanut Allergy Treatment Market Trends

The Asia Pacific region is likely to be the fastest-growing region in 2026, driven by rising diagnosis rates, expanding healthcare infrastructure, and increasing awareness of food allergies across countries such as China, India, and Australia. While peanut allergies have historically been under-reported in parts of the region, improved clinical recognition and enhanced diagnostic capabilities are driving demand for both emergency treatments such as epinephrine and structured management approaches, including immunotherapy.

A notable development supporting regional growth is Teva Pharmaceutical Industries Ltd.’s increased focus on expanding access to epinephrine auto-injectors and allergy management solutions in Asia Pacific markets, reflecting manufacturers’ strategic initiatives to strengthen distribution and awareness in high-growth areas. This involvement from established pharmaceutical companies helps improve the availability of essential emergency care and supports broader adoption of treatments.

Competitive Landscape

The global peanut allergy treatment market exhibits a moderately fragmented structure, driven by a mix of established pharmaceutical leaders and innovative biotechnology firms that are shaping treatment modalities from emergency intervention to long-term desensitization solutions. Major players are investing heavily in research and development to expand product pipelines, particularly in immunotherapy and biologics, while also leveraging regulatory approvals and strong clinical evidence to secure market positions.

With key leaders including Aimmune Therapeutics with its FDA-approved oral immunotherapy PALFORZIA, DBV Technologies developing Viaskin Peanut epicutaneous therapy, and Sanofi (with a broad allergy emergency treatment portfolio), the market is characterized by both innovation and legacy pharmaceutical strength. These players compete through product differentiation, expansive clinical data, strategic alliances, and robust distribution networks to enhance treatment adoption and patient outcomes.

Key Industry Developments:

- In February 2026, DBV Technologies S.A. presented additional positive clinical data from its Phase 3 VITESSE trial of the VIASKIN® Peanut Patch, the epicutaneous immunotherapy designed for peanut-allergic children aged four to seven years. The data showed a statistically significant treatment effect, with a higher proportion of responders in the VIASKIN Peanut group compared with placebo, reinforcing the potential of this non-invasive immunotherapy to desensitize patients and reduce allergic reactions.

- In January 2026, Novartis agreed to acquire U.S. biotech Excellergy, Inc. in a deal valued at up to US$2 billion, strengthening its position in allergy and IgE-driven disease treatment by adding Excellergy’s next-generation anti-IgE asset Exl 111 to its portfolio. The acquisition is designed to complement Novartis’s allergy offerings with a differentiated mechanism that may enhance symptom control across food allergy and other allergic conditions.

- In December 2025, Swiss biotech Mabylon AG initiated the first clinical trial of its novel tri-specific monoclonal antibody therapy MY006 for peanut allergy, dosing the first participant in a Phase I study designed to assess safety, tolerability, and immune response. This innovative biologic combines three antibodies into a single molecule that targets multiple major peanut allergens simultaneously, aiming to neutralize them before they trigger an allergic cascade and offering the potential for fewer injections per year compared with existing treatments.

Companies Covered in Peanut Allergy Treatment Market

- Mylan N.V.

- Sanofi

- Pfizer Inc.

- Kaleo, Inc.

- DBV Technologies

- Cambridge Peanut Allergy Clinic

- Regeneron

- ANAPTYSBIO, INC.

- ALK

- Stallergenes Greer

- Astellas Pharma Inc.

- Immunomic Therapeutics, Inc

- HAL Allergy B.V.

- Aravax

- Aimmune Therapeutics

- Prota Therapeutics Pty Ltd

- Nestlé Health Science

- Viatris

Frequently Asked Questions

The global peanut allergy treatment market is projected to reach US$0.6 billion in 2026.

The peanut allergy treatment market is driven by the rising prevalence of peanut allergies, increasing diagnosis rates, and growing adoption of immunotherapies and advanced emergency treatments.

The peanut allergy treatment market is expected to grow at a CAGR of 11.4% from 2026 to 2033.

Key market opportunities lie in the expansion of immunotherapies, the development of next-generation biologics, and personalized treatment approaches for broader age groups.

Mylan N.V., Sanofi, Pfizer Inc., Kaleo, Inc., DBV Technologies, Cambridge Peanut Allergy Clinic, and Regeneron are the leading players.