- Inks, Coatings, Adhesives & Sealants (ICAS)

- Algae Ink Market

Algae Ink Market Size, Share, and Growth Forecast, 2026 - 2033

Algae Ink Market by Application (Food Packaging, Beverage Packaging, Others), Ink Type (Flexographic Ink, UV Screen Ink, Others), End-use Industry, and Regional Analysis for 2026 - 2033

Algae Ink Market Size and Trends Analysis

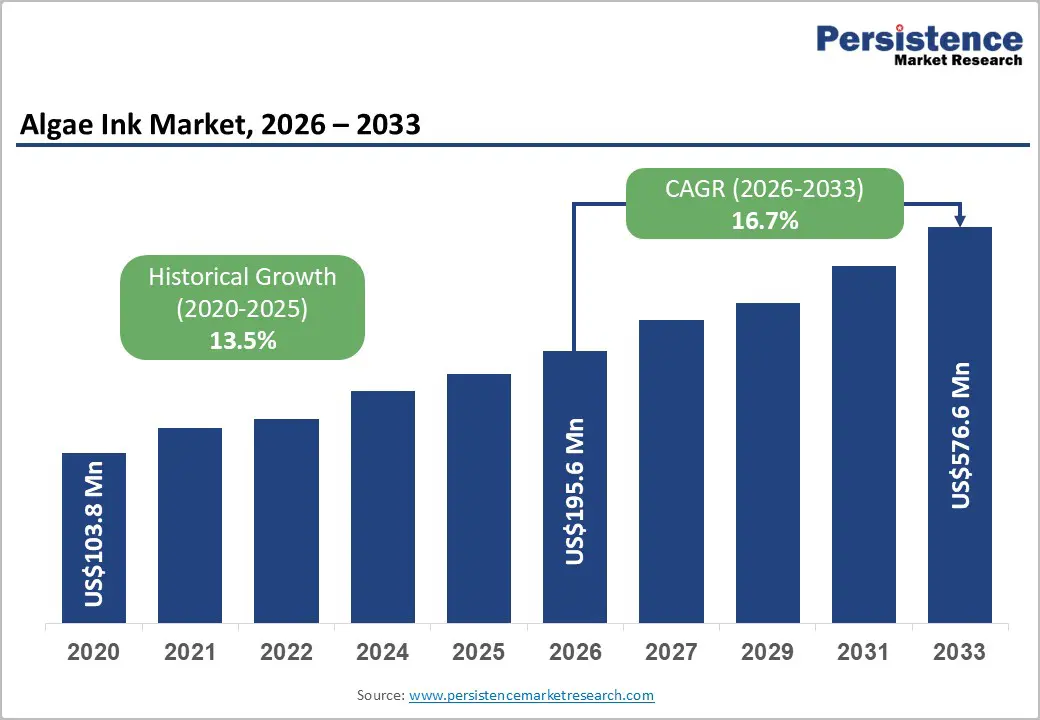

The global algae ink market size is likely to be valued at US$195.6 million in 2026 and is expected to reach US$576.6 million by 2033, growing at a CAGR of 16.7% between 2026 and 2033, driven by the increasing adoption of bio-based pigments across packaging and textile applications, tightening regulatory pressure on volatile organic compounds (VOCs) and petroleum-derived colorants, and the rapid commercialization of algae-based pigment technologies.

Demand remains concentrated in packaging and food & beverage applications, where sustainable sourcing and recyclability requirements are most stringent. Continued improvements in algal cultivation efficiency, pigment-extraction yield, and compatibility with mainstream printing technologies are expected to further accelerate market expansion.

Key Industry Highlights:

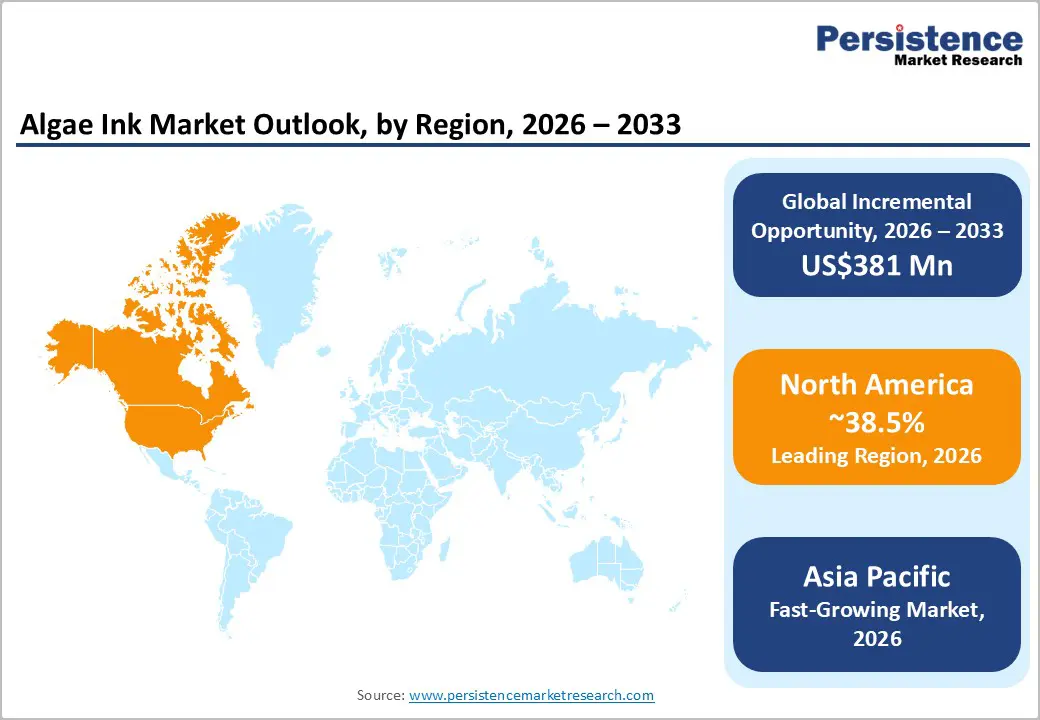

- Leading Region: North America is projected to dominate the market, accounting for approximately 38.5% of the market share, supported by early commercialization, strong R&D infrastructure, and brand-led sustainability adoption.

- Fastest-growing Region: Asia Pacific is the fastest-growing region, driven by large-scale packaging manufacturing, export-oriented production, and rising sustainability compliance across China, Japan, India, and ASEAN economies.

- Investment Plans: Strategic investments focus on scaling algae cultivation, improving pigment-extraction yields, and expanding water-based and UV-compatible formulations. Venture funding and corporate partnerships in North America and Europe are accelerating pilot-to-commercial transitions, while Asia Pacific is emerging as a potential low-cost production hub.

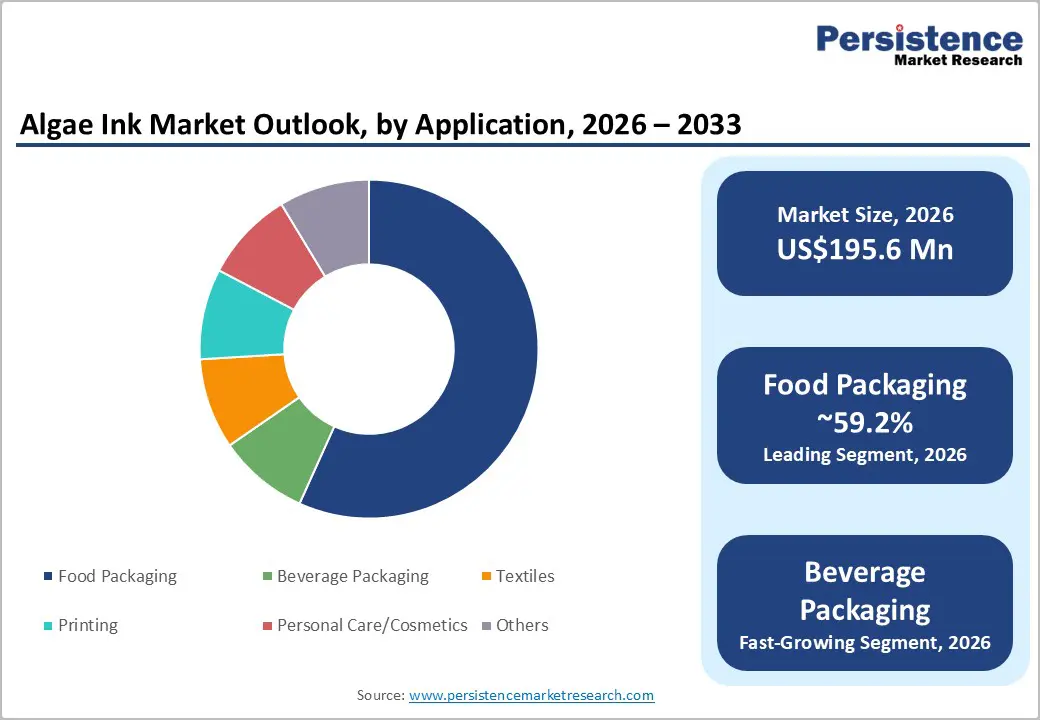

- Dominant Application: Food packaging is expected to lead the market, accounting for approximately 59.2%, driven by stringent food-safety regulations, recyclability mandates, and rising demand for low-migration, bio-based inks.

- Leading Ink Type: Flexographic water-based ink is estimated to account for approximately 46.3% of the market, reflecting its strong compatibility with packaging printing processes and its established use in corrugated board and labeling applications.

| Key Insights | Details |

|---|---|

|

Market Size (2026E) |

US$195.6 Mn |

|

Market Value Forecast (2033F) |

US$576.6 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

16.7% |

|

Historical Market Growth (CAGR 2020 to 2025) |

13.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Regulatory and Sustainability Mandates Accelerating Substitution of Petroleum-Based Pigments

Global regulatory frameworks and corporate sustainability mandates increasingly restrict VOC emissions, hazardous additives, and carbon-intensive raw materials in packaging and textile production. Extended producer responsibility (EPR) policies, packaging waste directives, and stricter chemical disclosure requirements are compelling brands to re-evaluate ink formulations across supply chains. Major consumer brands and retailers now embed bio-based content targets into procurement standards, creating measurable demand for renewable pigment alternatives. Algae-based inks exhibit lower carbon intensity and improved recyclability than conventional petroleum-derived inks. As labeling regulations tighten and sustainability reporting becomes mandatory in several jurisdictions, procurement budgets are increasingly being reallocated toward certified bio-based inks. This regulatory and compliance-driven demand forms a structural growth foundation for the algae ink market.

Technological Improvements in Algae Pigment Yield and Formulation Compatibility

Advancements in algae cultivation systems, including controlled photobioreactors and optimized strain selection, have significantly enhanced pigment yield and consistency. Improvements in extraction technologies and solvent-free processing methods have enhanced pigment concentration, stability, and lightfastness. These developments enable algae-derived pigments to meet industrial performance requirements for viscosity, adhesion, cure speed, and substrate compatibility. Water-based flexographic and screen-printing formulations are increasingly compatible with existing packaging and textile production lines, reducing conversion barriers for manufacturers. Even incremental gains in extraction yield and process efficiency materially improve unit economics, moving algae inks from niche applications toward broader commercial viability. Continued R&D investment is expected to enhance performance parity with conventional inks.

Brand and Consumer Demand for Verifiable Carbon-Sensitive Sourcing

Brand-driven sustainability strategies are significantly influencing material selection across the packaging and apparel sectors. Consumer-facing industries increasingly prioritize traceable and measurable reductions in environmental impacts associated with raw material sourcing. High-visibility collaborations between algae pigment developers and global fashion, outdoor, and consumer goods brands demonstrate the commercial and marketing value of renewable inks. Institutional investors and ESG-focused funds are also integrating sustainable material usage into risk assessments and portfolio decisions. This financial and reputational pressure incentivizes brands to adopt low-carbon inputs such as algae-based pigments. As lifecycle assessment methodologies mature and carbon accounting becomes standardized, suppliers capable of quantifying environmental impact will gain a competitive advantage and accelerate long-term adoption.

Barrier Analysis - Unit Cost and Scale Economics

Despite technological advancements, algae-based inks generally carry a price premium compared to petroleum-derived alternatives. Limited feedstock scale, capital-intensive cultivation systems, and supply chain inefficiencies contribute to higher production costs in several regions. If algae pigments maintain a 20–60% cost premium relative to conventional inks, adoption may remain concentrated in premium, regulated, or sustainability-driven segments rather than mass-market packaging. Achieving cost parity depends on scaling cultivation infrastructure, improving yield efficiency, and optimizing logistics. Until production volumes increase substantially, cost sensitivity among high-volume converters may constrain rapid penetration into commoditized markets.

Technical Compatibility across Printing Technologies

Not all algae ink formulations currently meet the full spectrum of technical specifications required across digital, offset, gravure, and high-speed flexographic processes. Performance variables such as drying time, substrate adhesion, color consistency, and curing compatibility can present operational challenges. Converters operating high-throughput production lines require minimal disruption and precise performance benchmarks. Any deviation from established production parameters increases validation costs and slows procurement decisions. Furthermore, food-contact certifications and textile washfastness standards require additional testing, which extends commercialization timelines. Broader technical standardization will be critical to unlocking large-scale adoption.

Opportunity Analysis - Expansion in Food Packaging and Certified Food-Contact Applications

Food packaging represents both the largest current application and the most immediate growth opportunity. Regulatory emphasis on recyclability, compostability, and reduction of chemical migration aligns closely with the attributes of algal ink. If algae-based formulations secure food-contact approvals at competitive price points, even modest substitution, such as 5–10% of global food packaging ink demand, could translate into substantial incremental revenue potential over the coming decade. Improved compatibility with paper-based and recyclable substrates further strengthens the value proposition. Early adoption by consumer packaged goods (CPG) companies indicates scalable commercial potential as certifications expand.

Textile Printing and Premium Fashion Integration

The textile and fashion industries exhibit strong growth potential owing to rising demand for sustainable dyeing and printing alternatives. Apparel brands frequently pilot innovative materials in limited runs before scaling to larger collections. Algal inks offer compelling environmental narratives, particularly when life-cycle analyses demonstrate reduced water use or carbon intensity relative to synthetic pigments. Textile applications also tolerate higher price points, allowing suppliers to refine formulations before targeting high-volume packaging markets. Successful multi-season partnerships can convert pilot projects into recurring supply agreements, supporting predictable revenue growth.

Category-wise Analysis

Application Insights

The food packaging segment is anticipated to account for approximately 59.2% of the market in 2026, making it the dominant application segment. Its leadership is driven by stringent regulatory oversight of food-contact materials, rising corporate sustainability targets, and growing demand for low-migration, non-toxic formulations. Water-based flexographic algae inks are increasingly used for corrugated shipping boxes, folding cartons, paper-based trays, and product labels, particularly in organic foods, plant-based products, and premium private-label categories where environmental positioning is central to brand identity.

The segment benefits from relatively higher value-added margins, enabling converters and brand owners to absorb incremental costs associated with bio-based inputs. For example, several sustainable snack and beverage brands have piloted the use of algae-based black and cyan pigments in secondary packaging to reduce petroleum-derived carbon content. Alignment with circular-economy goals, recyclability mandates, and compostable-substrate initiatives further strengthens adoption. As regulatory scrutiny of mineral-oil-based inks and synthetic pigments intensifies, penetration into both primary and secondary food packaging formats is expected to expand steadily.

Beverage packaging is expected to be the fastest-growing application segment within the algae ink market. Premium beverage manufacturers, particularly in craft beer, functional drinks, organic juices, and plant-based dairy alternatives, actively incorporate sustainability messaging into packaging design, accelerating demand for renewable ink technologies. Compared to primary food packaging, beverage labels and shrink sleeves typically have shorter development and qualification cycles, enabling faster commercialization of innovative ink formulations.

Improvements in drying speed, color vibrancy, and substrate adhesion have strengthened compatibility with pressure-sensitive labels, aluminum cans, glass bottles, and PET containers. For instance, limited-edition sustainable packaging campaigns by craft beverage brands have utilized algae-based pigments to highlight carbon-reduction initiatives. As sustainability-driven SKU transitions continue and multinational beverage companies expand ESG-aligned procurement standards, this segment is projected to sustain above-average growth over the forecast period.

Ink Type Insights

Flexographic water-based algae inks are anticipated to account for 46.3% of the global market in 2026, positioning flexography as the leading ink type segment. Flexographic printing remains the dominant process for corrugated packaging, flexible packaging, and labels worldwide, particularly in high-volume food and beverage applications. Algae pigments integrate relatively efficiently into existing water-based flexographic systems, minimizing equipment modification requirements for converters.

The widespread installed base of flexographic presses across North America, Europe, and Asia Pacific further supports this dominance. For example, sustainable e-commerce packaging and retail-ready display cartons are increasingly printed using water-based systems compatible with renewable pigment inputs. Operational advantages such as fast changeovers, lower solvent emissions, and established supply chains reduce conversion risks. As packaging remains the primary demand driver for algae inks, flexographic formulations are expected to retain leadership throughout the forecast period.

UV-curable algae inks are projected to be the fastest-growing segment of the ink type. UV systems provide rapid curing, high color density, superior abrasion resistance, and reduced solvent emissions, making them particularly attractive for specialty packaging, premium labels, and textile printing applications. Advancements in algal pigment stabilization and photoinitiator compatibility are improving performance under UV-curing conditions.

This progress enables application across shrink sleeves, cosmetic packaging, promotional materials, and short-run customized prints. For example, sustainable apparel brands experimenting with algae-based screen printing inks for limited collections demonstrate the segment’s expansion beyond traditional packaging. As converters increasingly adopt high-speed UV lines to improve efficiency and reduce energy consumption, demand for UV-curable algae formulations is expected to accelerate, particularly in premium and specialty markets.

Regional Insights

North America Algae Ink Market Trends - R&D-Driven Commercialization and Brand-Led ESG Adoption of Algae-Based Inks

North America is expected to lead the market, accounting for approximately 38.5% of market share in 2026, supported by advanced R&D ecosystems, early commercialization pipelines, and strong brand-driven sustainability mandates. The U.S. anchors regional growth through innovation clusters in California, Colorado, and the Pacific Northwest, where biotechnology firms and material science startups focus on algae-derived pigments and carbon-negative materials. Companies such as Living Ink Technologies (U.S.) have commercialized algae-based black pigments for packaging and footwear applications, demonstrating the scalability of a petroleum-derived carbon black replacement.

Corporate ESG commitments remain a central catalyst. Major U.S.-based food and beverage companies, including PepsiCo and Coca-Cola, have strengthened packaging sustainability targets tied to recyclable, compostable, and lower-carbon materials. These procurement frameworks indirectly support the adoption of renewable ink across supply chains. Regulatory developments such as California’s SB 54 (Plastic Pollution Prevention and Packaging Producer Responsibility Act) and emerging extended producer responsibility (EPR) programs across multiple states incentivize packaging material transparency and reduced lifecycle emissions.

Venture capital funding in climate-tech and bio-based materials, tracked by organizations such as the U.S. Department of Energy and private investment databases, has expanded pilot-scale algae cultivation and pigment extraction infrastructure. Partnerships between biotechnology firms and established ink manufacturers are improving production yields and color stability, reducing commercial risk for converters.

High-visibility collaborations, including sustainable product launches in athletic footwear and limited-edition packaging campaigns, have accelerated brand confidence and normalized algae-derived pigments in mainstream packaging. As regulatory scrutiny on chemical safety and lifecycle carbon accounting intensifies, North America is expected to maintain leadership in commercialization and premium adoption.

Europe Algae Ink Market Trends - EU Circular Economy Regulation and Certification-Focused Algae Ink Integration

Europe accounts for a significant share of the global algae ink market, driven by comprehensive regulatory harmonization and circular-economy mandates under the European Green Deal. Core markets include Germany, the U.K., France, and Spain, where sustainability performance increasingly influences procurement decisions across packaging and retail sectors. The European Union’s Packaging and Packaging Waste Regulation (PPWR) framework and REACH chemical safety standards have tightened material disclosure and recyclability requirements. These policies encourage converters to evaluate renewable pigment inputs with lower environmental impact profiles.

Germany’s strong flexographic printing base and its leadership in sustainable packaging innovation provide a favorable environment for algae ink testing and commercialization. Companies operating in Germany’s industrial packaging clusters are integrating bio-based pigments into corrugated and folding carton lines to meet recyclability objectives.

European investment trends emphasize the development of certification and traceability infrastructure. Collaborative research initiatives between universities, biotechnology firms, and established ink producers, often supported by EU Horizon Europe funding programs, focus on pigment stability, UV resistance, and compostability verification. These developments enhance technical reliability and regulatory compliance, lowering barriers for converters. As carbon pricing mechanisms and sustainability reporting requirements expand across EU member states, renewable ink technologies are expected to gain incremental traction in both packaging and specialty printing applications.

Asia Pacific Algae Ink Market Trends - Manufacturing-Scale Advantages and Export-Driven Sustainability Compliance

Asia Pacific is likely to be the fastest-growing regional market for algae inks, supported by large-scale manufacturing capacity, export-driven packaging production, and tightening sustainability compliance standards across major economies. While the region currently trails North America and Europe in overall adoption rates, its structural manufacturing advantages position it for accelerated scale-up. China leads in printing converter capacity and supply chain integration. As the world’s largest packaging producer, China has increased regulatory focus on environmental compliance through policies aligned with its national carbon neutrality objectives.

Large packaging exporters supplying multinational consumer goods brands are beginning to evaluate renewable ink alternatives to meet international ESG procurement standards. The country’s strong algae cultivation capabilities, supported by industrial biotechnology initiatives, could facilitate localized pigment production, reducing import dependency and improving cost competitiveness.

India and ASEAN countries represent high-growth potential markets as regulatory awareness increases and packaging demand expands alongside urbanization and e-commerce growth. India’s Plastic Waste Management Rules and the implementation of extended producer responsibility are encouraging packaging manufacturers to explore environmentally aligned materials. Regional startups and academic institutions are investigating microalgae cultivation for industrial pigment extraction, which could establish cost-effective regional production hubs.

Export-oriented production models across Southeast Asia, particularly in Thailand, Vietnam, and Indonesia, create downstream incentives to comply with North American and European sustainability requirements. As global brands impose uniform packaging standards across markets, Asia Pacific converters are likely to integrate renewable ink systems to maintain export competitiveness. Over the forecast period, improvements in cultivation efficiency, regional supply chain localization, and regulatory convergence are expected to accelerate algae ink adoption across packaging and specialty applications.

Competitive Landscape

The global algae ink market remains emerging but increasingly structured around a limited number of technology innovators supported by specialized regional formulators. Market concentration is moderate. Early movers with proprietary pigment extraction processes and cultivation technologies maintain a competitive advantage. Competitive differentiation centers on supply security, food-contact certification, recyclability validation, and strategic brand partnerships. While fragmentation exists at the formulation level, technological barriers create defensible positions for leading innovators.

Leading companies focus on vertical integration of algae cultivation and pigment extraction, strategic partnerships with packaging converters, and product differentiation through regulatory certification. Co-development with brand owners and long-term supply agreements remain central to market expansion strategies.

Key Industry Developments:

- In April 2025, Living Ink Technologies announced participation in Cohort 6 of the 100+ Accelerator with global partners such as AB InBev, Coca-Cola, Danone, Colgate-Palmolive, and Unilever to transform brewery and other waste biomass into sustainable pigments, supporting scale-up and supply chain integration.

- In September 2025, Crocs became the first major brand to use algae-based ink in full CMYK packaging for its Jibbitz shoe charm boxes, printing over 3.2 million cartons with renewable pigments in partnership with Living Ink Technologies and EcoEnclose.

Companies Covered in Algae Ink Market

- Living Ink Technologies

- ECKART GmbH

- Sun Chemical Corporation

- Siegwerk Druckfarben AG & Co. KGaA

- Flint Group

- Toyo Ink SC Holdings Co., Ltd.

- Huber Group

- INX International Ink Co.

- Nazdar Ink Technologies

- T&K Toka Co., Ltd.

- DIC Corporation

- Sakata INX Corporation

- Wikoff Color Corporation

- Zeller+Gmelin GmbH & Co. KG

- Royal Dutch Printing Ink Factories Van Son

- FUJIFILM Sericol

- Agfa-Gevaert Group

- ALTANA AG

Frequently Asked Questions

The global market size is projected to be valued at US$195.6 million in 2026.

The algae ink market is expected to reach US$576.6 million by 2033.

Key trends include rising adoption of bio-based and low-VOC inks, expansion of water-based flexographic formulations, increased food-safe and compostable packaging solutions, and strategic partnerships between algae pigment innovators and global apparel and packaging brands.

Food packaging is the leading application segment, accounting for approximately 59.2% of market share, driven by regulatory compliance requirements and strong sustainability mandates in food & beverage packaging.

The algae ink market is projected to grow at a CAGR of 16.7% between 2026 and 2033.

Major players include Living Ink Technologies, ECKART GmbH, Sun Chemical Corporation, Siegwerk Druckfarben AG & Co. KGaA, and Flint Group.