- Technology

- Airborne Intelligence Surveillance Reconnaissance Market

Airborne Intelligence Surveillance Reconnaissance Market Size, Share, and Growth Forecast 2026 - 2033

Airborne Intelligence Surveillance Reconnaissance (ISR) Market by Platform Type (Manned ISR Aircraft, Unmanned Aerial Vehicles (UAVs), Other Airborne Platforms), by Solution (Sensors, Communication Systems, Software & Analytics, Others), by Application (Border & Maritime Security, Battlefield ISR, Search & Rescue (SAR), Critical Infrastructure Protection, Target Tracking, Others), by Regional Analysis, 2026-2033

Airborne Intelligence Surveillance Reconnaissance Market Size and Trend Analysis

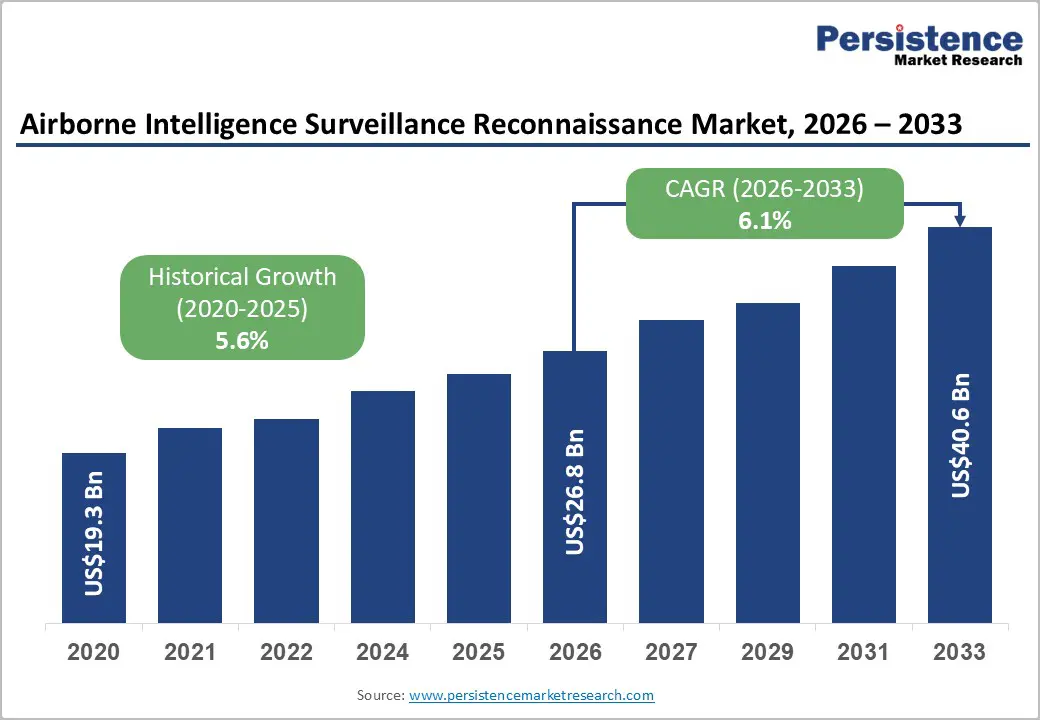

The global airborne intelligence, surveillance, and reconnaissance (ISR) market size is expected to be valued at US$ 26.8 billion in 2026 and is projected to reach US$ 40.6 billion by 2033, growing at a CAGR of 6.1% between 2026 and 2033. This growth is driven by accelerating defense modernization, rapid deployment of unmanned aerial systems, and the rising need for real-time situational awareness across military and homeland security operations. Governments are strengthening their airborne ISR fleets to counter emerging threats, including anti-access strategies, hypersonic weapons, and asymmetric warfare. Simultaneously, advancements in EO/IR sensors, synthetic aperture radar, and AI-enabled analytics are improving multi-domain intelligence fusion, enabling faster, more accurate operational decisions.

Key Market Highlights

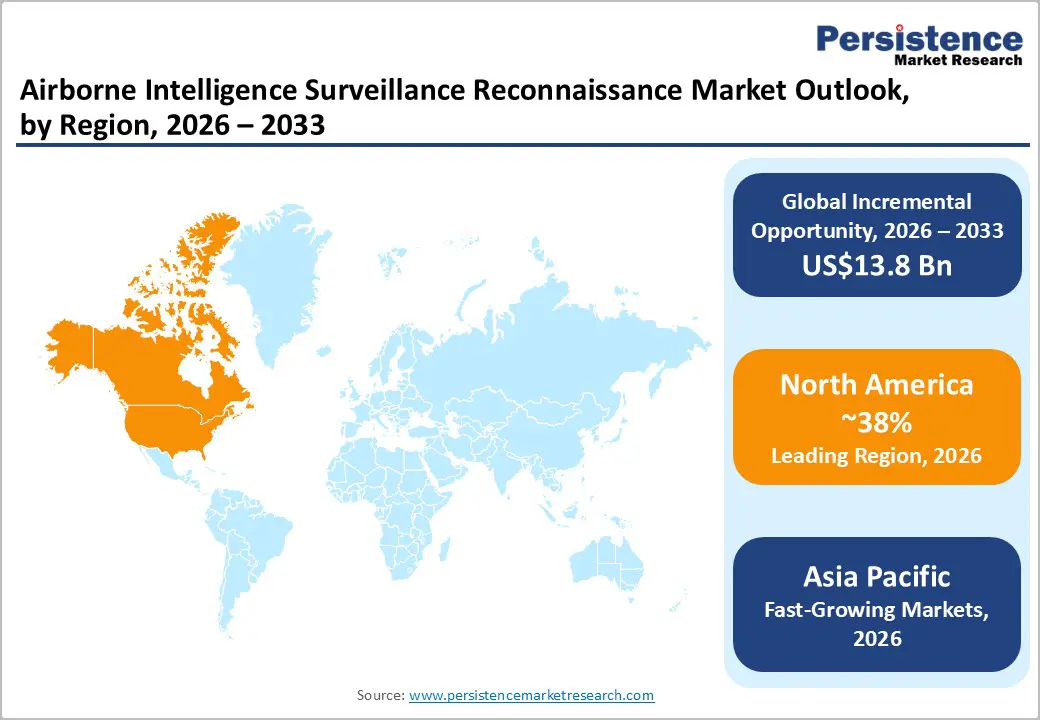

- Leading Region: North America remains the leading region, contributing an estimated 38% share of the airborne ISR market in 2025, driven by high U.S. defense spending, robust innovation ecosystems, and modernization of manned and unmanned ISR fleets.

- Fastest-Growing Region: The Asia Pacific market, with a 30% share, is expected to be the fastest-growing region through 2033, driven by rising defense budgets, expanding maritime security needs, and regional aerospace and UAV industrialization.

- Leading Platform Category: Unmanned Aerial Vehicles (UAVs) dominate the platform segment with around 45% share in 2025, offering persistent surveillance, lower crew risk, and flexible payload integration across defense, border security, and maritime missions.

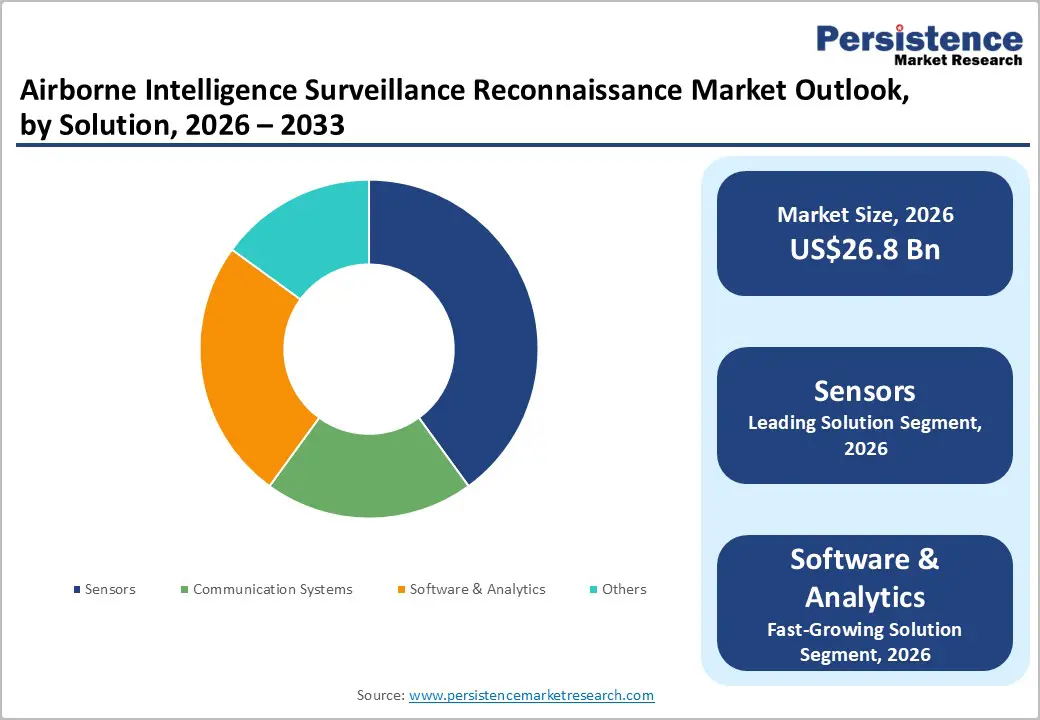

- Leading Solution Category: Sensors, holding ~40% share, form the core solution segment, providing high-resolution EO/IR, radar, and electronic intelligence capabilities.

- Key Market Opportunity: AI-enabled multi-sensor ISR ecosystems present a major opportunity, enabling integrated platforms, modular payloads, and ISR-as-a-Service for defense and civil security missions.

| Key Insights | Details |

|---|---|

| Airborne Intelligence Surveillance Reconnaissance Market Size (2026E) | US$ 26.8 Bn |

| Market Value Forecast (2033F) | US$ 40.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.6% |

Market Dynamics

Market Growth Drivers

Rising Geopolitical Tensions and Defense Modernization

Escalating geopolitical rivalries, border disputes, and regional conflicts are pushing governments to invest heavily in airborne ISR for persistent surveillance and rapid threat detection. Defense budgets across NATO members and key Indo-Pacific and Middle East countries continue to rise, with a growing share allocated to ISR platforms, secure communications, and command-and-control modernization to support joint and coalition operations.

These investments are driving procurement of long-endurance ISR aircraft, advanced sensor payloads, and real-time data-link systems that enhance situational awareness across air, land, and maritime domains. Upgrades of legacy surveillance fleets with modern electro-optical, radar, and electronic intelligence capabilities are further reinforcing sustained market demand for integrated airborne ISR solutions.

Proliferation of UAVs and Multi - domain ISR Concepts

The rapid expansion of unmanned aerial vehicles has become a major growth driver for the airborne ISR market, as militaries increasingly deploy MALE and HALE drones for persistent, wide-area surveillance with reduced operational risk. Networked UAVs now support target detection, tracking, and real-time intelligence dissemination across complex operational environments.

At the same time, defense innovation programs are accelerating the adoption of manned-unmanned teaming, autonomous mission management, and cloud-enabled ISR processing. These multi-domain concepts require advanced sensors, secure communications, and AI-driven analytics, fueling rising demand for next-generation airborne ISR platforms and integrated intelligence architectures.

Market Restraints

High Acquisition and Lifecycle Costs

Airborne ISR platforms, especially manned surveillance aircraft and high-end HALE drones, require significant capital investment and long-term sustainment spending. The integration of advanced radar, EO/IR sensors, electronic intelligence suites, and secure communications can push unit costs into the hundreds of millions of dollars, while ongoing maintenance, crew training, and logistics further raise lifecycle expenses.

For budget-constrained defense forces, these high costs can limit fleet expansion and delay modernization programs. As a result, some countries opt for more affordable ground-based or space-based surveillance alternatives, slowing the adoption of sophisticated airborne ISR systems and extending the operational life of older platforms.

Regulatory and Airspace Integration Challenges

The deployment of ISR-capable UAVs is constrained by strict airspace regulations governing safety, spectrum use, and beyond-visual-line-of-sight operations. Authorities such as the Federal Aviation Administration and the European Union Aviation Safety Agency impose rigorous certification and detect-and-avoid requirements, particularly for flights in non-segregated civilian airspace.

These regulatory hurdles delay approvals for routine UAV operations, limiting the flexibility of ISR missions for homeland security, disaster response, and border surveillance. As a result, integration challenges can slow deployment timelines and restrict the expansion of civil and dual-use airborne ISR applications in densely populated regions.

Market Opportunities

AI-Enabled Multi-Sensor Data Fusion and Analytics

The rapid growth in ISR data volumes is creating strong demand for AI-driven analytics, automated target recognition, and multi-sensor fusion platforms. Defense agencies are investing in edge computing, cloud-based processing, and C4ISR integration to reduce decision cycles and improve real-time intelligence delivery across operational domains.

Vendors that provide interoperable software capable of integrating radar, EO/IR, SIGINT, and open-source intelligence into unified, intuitive dashboards are well-positioned to secure high-value contracts. This opportunity aligns closely with military digital transformation programs prioritizing secure data pipelines, advanced algorithms, and scalable intelligence architectures.

Expansion of ISR for Homeland Security and Civil Applications

Airborne ISR is increasingly being adopted beyond traditional military roles, creating new opportunities across homeland security, maritime safety, and disaster response. Agencies use ISR platforms for border surveillance, anti-smuggling patrols, search and rescue, wildfire detection, and monitoring of critical infrastructure.

Maritime patrol aircraft and UAVs equipped with surface search radar and AIS sensors help protect exclusive economic zones, while disaster management agencies rely on real-time aerial imagery for emergency coordination. This diversification supports growing demand for dual-use platforms, modular payloads, and service-based ISR offerings, expanding the overall customer base.

Category-wise Insights

Platform Type Analysis

Unmanned Aerial Vehicles (UAVs) are the leading platform segment in the airborne ISR market, accounting for around 45% share by 2025, driven by their ability to deliver long-endurance surveillance at lower operational risk and cost. MALE and tactical UAVs are widely deployed for border security, counter-terrorism, and maritime patrol, making them the preferred ISR platform globally.

Manned ISR aircraft are expected to be the fastest-growing platform type as air forces upgrade strategic reconnaissance fleets and integrate advanced sensors, electronic intelligence systems, and secure communications to support high-threat, long-range, and multi-domain missions that require higher payload capacity and survivability.

Solution Analysis

Sensors represent the dominant solution segment, holding approximately 40% share of the airborne ISR market in 2025, reflecting the critical importance of EO/IR, synthetic aperture radar, and electronic intelligence payloads in modern intelligence collection. Continuous investments in high-resolution imaging, wide-area surveillance, and multi-spectral detection are driving strong demand across both manned and unmanned platforms.

Software and analytics solutions are the fastest-growing segment as defense agencies prioritize AI-enabled data fusion, automated target recognition, and cloud-based ISR processing to convert raw sensor data into actionable intelligence faster and support network-centric and multi-domain operational environments.

Application Analysis

Battlefield ISR is the leading application, accounting for about 38% of the airborne ISR market by 2025, driven by the growing need for real-time tracking of enemy forces, electronic emissions, and logistics networks. Airborne ISR supports precision strikes, mission planning, and battle damage assessment, making it central to modern high-intensity and hybrid warfare.

Homeland security and civil applications are the fastest-growing areas as governments increasingly use airborne ISR for border surveillance, maritime security, disaster response, and critical infrastructure protection, expanding ISR usage beyond combat operations into continuous peacetime security and emergency management missions.

Regional Insights

North America Airborne ISR Market Trends and Insights

North America remains the largest airborne ISR market, accounting for around 38% share in 2025, driven primarily by the United States’ extensive defense modernization and multi-domain operations strategy. High investments in ISR aircraft, advanced sensors, and C4ISR integration continue to support strong procurement of both manned and unmanned platforms across air, land, and maritime domains.

The region also benefits from a powerful innovation ecosystem, where prime contractors, startups, and research institutions collaborate on AI, autonomy, and resilient communications. Strong export frameworks allow U.S. and Canadian manufacturers to supply allied forces, reinforcing North America’s leadership in global ISR technology and system integration.

Europe Airborne ISR Market Trends and Insights

Europe represents a technologically advanced and steadily expanding airborne ISR market, supported by rising security concerns and coordinated defense initiatives under NATO and the European Union. The region is projected to grow at a CAGR of about 5.5% through the forecast period, driven by modernization of ISR aircraft, increasing use of MALE UAVs, and cross-border surveillance programs.

Harmonized EASA regulations are enabling wider integration of UAVs into controlled airspace, supporting both military and civil ISR missions. Europe’s strong aerospace and sensor manufacturing base ensures continued innovation, positioning the region as a key supplier of advanced ISR solutions to global defense partners.

Asia Pacific Airborne ISR Market Trends and Insights

Asia Pacific is emerging as one of the most dynamic airborne ISR markets, capturing nearly 30% of global demand by 2025 as countries expand surveillance across vast coastlines and contested maritime zones. Nations such as China, India, Japan, and South Korea are heavily investing in UAVs, maritime patrol aircraft, and airborne early-warning platforms to enhance domain awareness.

Rapid growth in domestic aerospace manufacturing and rising defense budgets are supporting large-scale procurement of sensors, drones, and mission systems. Partnerships with global primes and local firms are accelerating technology transfer, making airborne ISR a cornerstone of national security and regional stability strategies.

Competitive Landscape

The global airborne ISR market is moderately consolidated, dominated by large defense contractors alongside specialized providers of sensors, mission systems, and unmanned platforms. Competition is shaped by long-term government procurement programs, export opportunities, and continuous investment in research and development to integrate open-architecture avionics, advanced payloads, and AI-driven intelligence processing into modern ISR platforms.

Market leaders are increasingly focused on modular system designs, manned-unmanned teaming, and scalable ISR solutions. New business models emphasize service-based offerings, cloud-enabled data processing, and performance-based support, enabling vendors to deliver end-to-end, intelligence-centric ISR ecosystems.

Key Market Developments

- In February 2024, Northrop Grumman Corporation announced enhancements to its HALE UAV ISR platform, introducing upgraded radar and secure communications suites designed to improve maritime domain awareness, long-range target detection, and real-time data sharing for naval forces operating across wide ocean and coastal environments.

- In June 2024, Lockheed Martin Corporation secured a multi-year contract to modernize manned ISR aircraft for a North American customer, integrating open-architecture mission systems, advanced EO/IR sensors, and upgraded data links to improve interoperability, survivability, and real-time intelligence dissemination across joint operations.

- In September 2023, Airbus SE completed successful flight trials of a next-generation maritime surveillance aircraft configuration for European coast guard and border security missions, validating new radar, electro-optical payloads, and mission systems that enhance surface tracking, illegal activity detection, and persistent wide-area maritime monitoring.

Companies Covered in Airborne Intelligence Surveillance Reconnaissance Market

- BAE Systems

- L-3 Technologies Inc.

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- UTC Aerospace Systems

- The Boeing Co.

- General Dynamics Corporation

- Raytheon Company

- Rockwell Collins Inc.

- Thales S.A.

- Others.

Frequently Asked Questions

The global airborne ISR market is expected to reach US$ 26.8 billion in 2026, reflecting continued investments in manned and unmanned surveillance platforms.

Demand is primarily driven by rising geopolitical tensions, defense modernization initiatives, proliferation of UAVs, and the need for real‑time situational awareness

North America, with 38% share in 2025, leads due to high defense spending, ISR fleet modernization, and a strong industrial and R&D base.

AI-enabled multi-sensor ISR ecosystems, modular payloads, and ISR-as-a-Service offerings represent a major opportunity across defense and civil security missions

Prominent players include Northrop Grumman Corporation, Lockheed Martin Corporation, Raytheon Technologies Corporation, L3Harris Technologies, Inc., and BAE Systems plc.