- Off-Road Equipment & Machinery

- Agricultural Mowers Market

Agricultural Mowers Market Size, Share, and Growth Forecast, 2026 - 2033

Agricultural Mowers Market by Product Type (Disc, Sickel Bar, Drum, Flail), Power (Gasoline, Diesel, Electric), End-Use (Garden, Farm), and Regional Analysis for 2026-2033

Agricultural Mowers Market Share and Trends Analysis

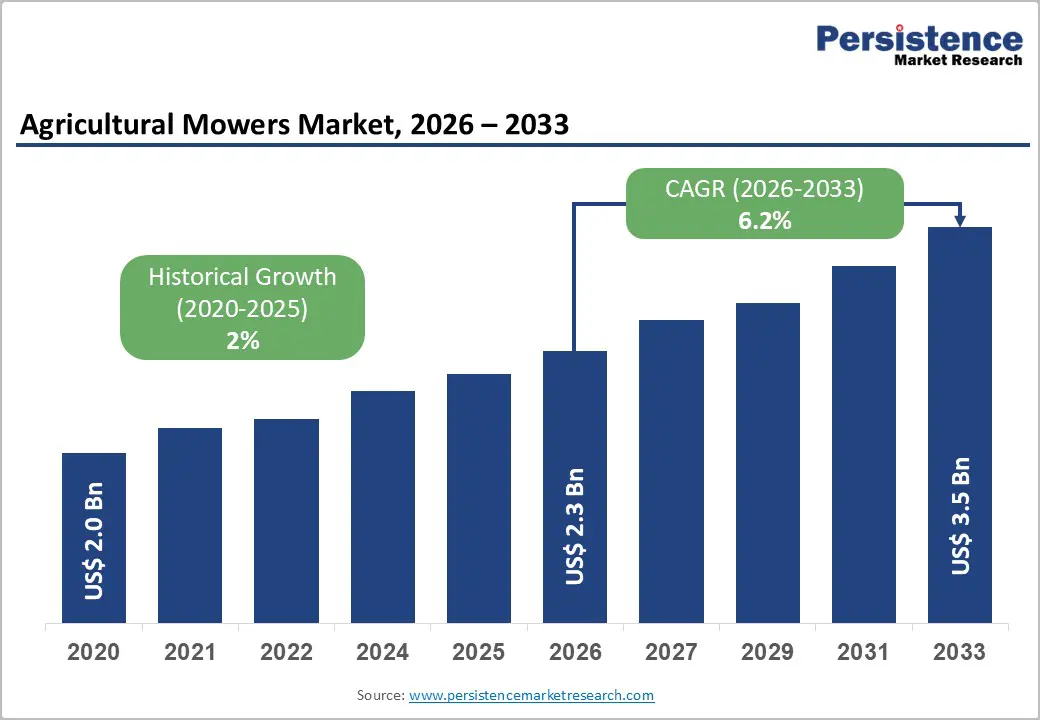

The global agricultural mowers market size is likely to be valued at US$ 2.3 billion in 2026, and is projected to reach US$ 3.5 billion by 2033, growing at a CAGR of 6.2% during the forecast period 2026−2033. The market is being propelled by the twin forces of global food security imperatives and progressive mechanization of farming practices across developing economies. Rising labor costs in developed markets and growing farmland under cultivation in the Asia Pacific and Latin America are compelling farmers to adopt more efficient grass and crop-cutting solutions.

Key Industry Highlights

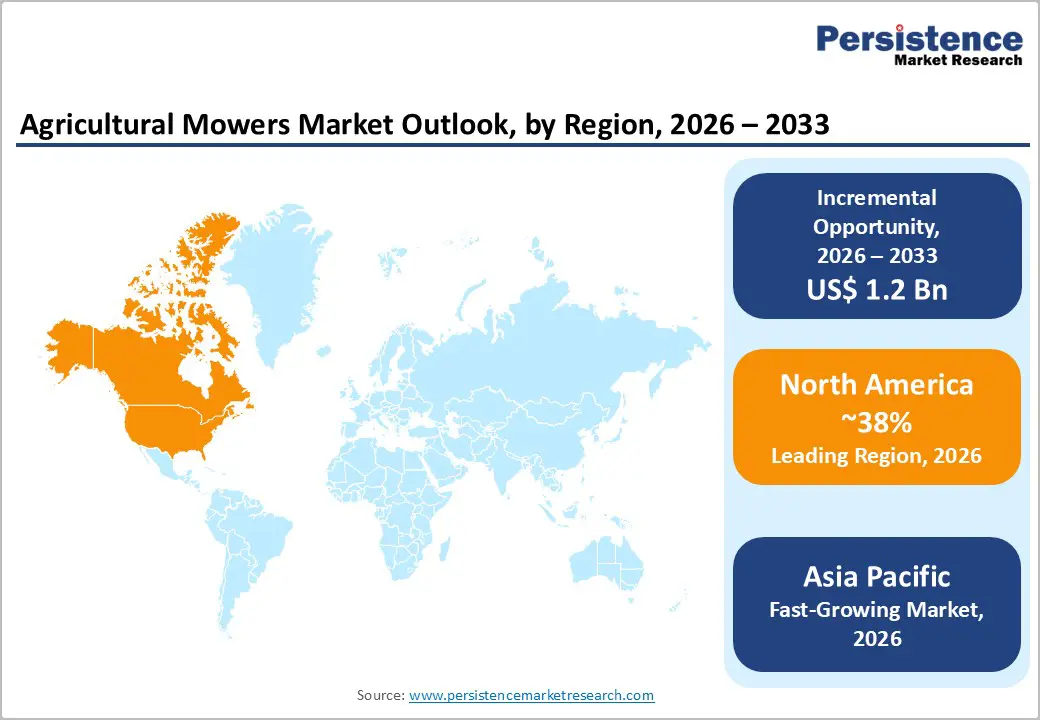

- Dominant Region: North America is likely to hold around 38% market share in 2026, supported by high adoption of advanced agricultural machinery and the presence of large-scale farming operations.

- Fastest-growing Market: The Asia Pacific market is poised to be the fastest-growing from 2026 to 2033, driven by increasing mechanization in agriculture and government initiatives to support modern farming practices.

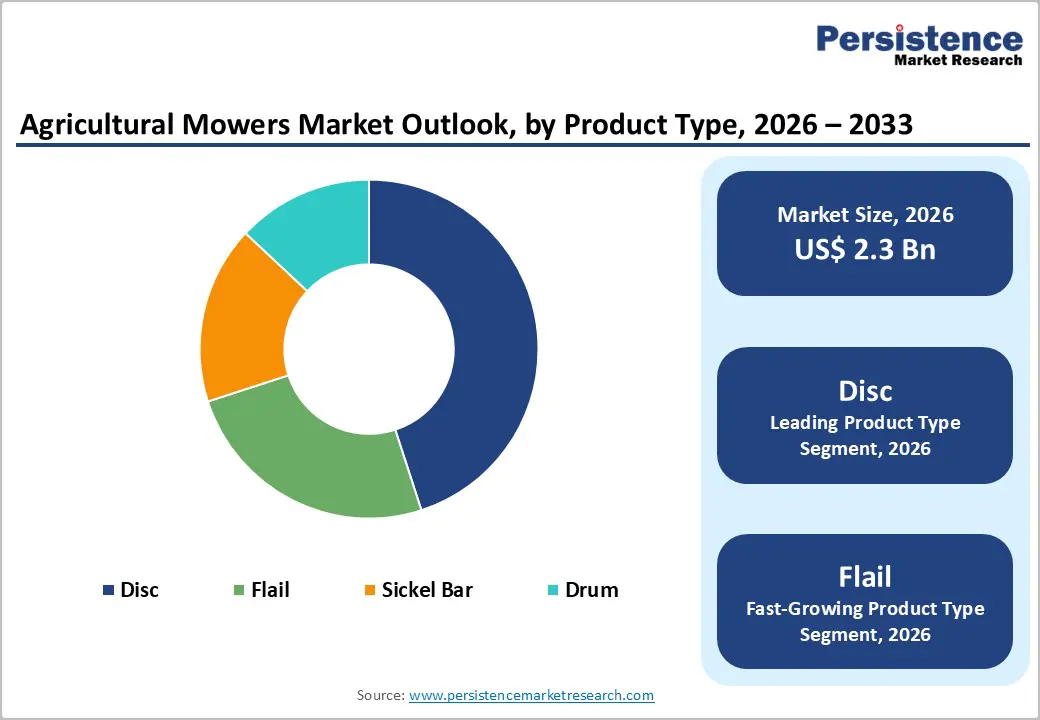

- Leading & Fastest-growing Product Type: Disc mowers are set to dominate by commanding approximately 45% revenue share, while flail mowers are likely to be the fastest-growing segment during the 2026-2033 forecast period.

- Leading & Fastest-growing Power: Diesel mowers are slated to lead with 75% market revenue share in 2026, with electric mowers posting the highest CAGR for the 2026-2033 forecast period.

- April 2025: Yamaha Motor acquired New Zealand-based Robotics Plus, a specialist in agricultural automation, to establish Yamaha Agriculture, Inc. in the U.S.

| Key Insights | Details |

|---|---|

| Agricultural Mowers Market Size (2026E) | US$ 2.3 Bn |

| Market Value Forecast (2033F) | US$ 3.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Accelerating Farm Mechanization in Emerging Economies

Agricultural mechanization is accelerating across the Asia Pacific, Latin America, and Sub-Saharan Africa. Farmers are adopting mowing equipment to manage expanding farmland efficiently and reduce labor dependence. Public policy is reinforcing this transition. India, for example, is implementing the Sub-Mission on Agricultural Mechanization (SMAM), which is offering financial assistance of about 40–50% for machinery purchases. Comparable programs in China and Brazil are also encouraging equipment ownership and improving farm productivity. These initiatives are strengthening the demand for both ride-on and walk-behind mowers.

Product segmentation is aligning with farm structure. Ride-on mowers are serving large estates that require high-capacity coverage, while walk-behind models are addressing small and fragmented plots. Manufacturers are expanding production capacity and strengthening regional distribution to capture emerging demand. Several firms are establishing local assembly facilities to reduce costs and shorten delivery cycles. Farmers are gaining access to equipment that operates effectively across varied crops and terrain conditions. Governments are expanding mechanization incentives, encouraging manufacturers to develop durable and user-friendly designs. As rural economies strengthen, the sector will favor versatile machinery that supports year-round agricultural activity and long-term operational efficiency.

Precision Agriculture Adoption and Smart Equipment Integration

Digital technologies are redefining agricultural mowing systems. Manufacturers are embedding Internet of Things (IoT) sensors, Global Positioning System (GPS) guidance, and telematics to improve precision and operational control. Farmers are monitoring equipment performance in real time through connected platforms, which are enabling faster responses to operational issues. Predictive maintenance alerts are identifying potential faults before equipment failure occurs, with original equipment manufacturers (OEMs), such as John Deere and AGCO, integrating connectivity into standard equipment models to expand functionality and increase product value.

Operational benefits are further reinforcing uptake. Telematics data is providing detailed insights that guide scheduling decisions and resource allocation. Operators are improving efficiency across different terrain conditions and crop environments through route optimization and fuel management features. Producers are upgrading fleets to capture measurable productivity gains, while OEMs are developing recurring revenue streams through software subscriptions and data-driven services. Farmers are adopting connected ecosystems that reduce downtime and simplify equipment management. The industry is progressing toward autonomous mowing capabilities, while new market entrants companies are introducing cost-efficient connectivity solutions for small-scale farms.

High Capital Costs and Limited Financing in Smallholder Markets

Although the World Bank (WB) acknowledges smallholder farms as the foundation of agricultural production, high acquisition costs are limiting the adoption of mechanized and autonomous mowing equipment in regions dominated by smallholder agriculture. Farmers in South Asia and Sub-Saharan Africa are facing difficulty purchasing ride-on mowers and robotic systems because these machines require significant upfront investment. Typical farm budgets in these areas are remaining constrained, which is restricting equipment ownership. Limited access to formal credit is further restricting purchases, resulting several farmers relying heavily on manual techniques or basic walk-behind equipment.

Market responses are emerging to address this affordability gap. Governments are introducing subsidy programs, although administrative delays are limiting their reach. Financial institutions are developing microfinance and small-loan products to expand credit availability. Leasing models are also gaining traction because they reduce initial capital requirements. Equipment manufacturers are designing modular platforms that allow farmers to upgrade features gradually. Cooperative ownership structures are enabling shared access to machinery among small producers. The sector is therefore evolving toward a segmented structure in which large commercial farms are adopting advanced technologies while smallholders are prioritizing cost-efficient tools.

Regulatory Compliance Costs and Emission Standards

Stricter emission standards for non-road mobile machinery (NRMM) are increasing regulatory pressure on agricultural equipment manufacturers in the European Union (EU) and the U.S. The EU is enforcing Stage V standards that are tightening emission limits for diesel engines used in mowing equipment. Similarly, the U.S. Environmental Protection Agency (EPA) is implementing Tier 4 Final regulations with comparable technical thresholds. These frameworks are requiring advanced exhaust aftertreatment systems and cleaner fuel technologies. The Association of Equipment Manufacturers (AEM) has also been reporting rising compliance costs across the sector, with mid-sized manufacturers are facing the greatest pressure due to limited research & development (R&D) resources.

Compliance costs are influencing market structure and product strategy. Manufacturers are transferring part of the additional expense to equipment buyers, which is affecting adoption in price-sensitive segments. Large firms are investing in hybrid and low-emission solutions to maintain regulatory alignment and strengthen competitive positioning. Smaller companies are consolidating operations or exiting markets where compliance investment remains prohibitive. Governments are tightening emission policies to reduce pollution from agricultural machinery, which is accelerating engineering innovation. Equipment manufacturers are adopting shared platforms to distribute research and development costs more efficiently. The industry is also expanding investment in electric drivetrains that eliminate diesel-related regulatory constraints through strategic partnerships that are enabling joint testing and certification processes.

Robotic and Autonomous Mower Adoption

Autonomous mowing technology is emerging as a major innovation pathway in the agricultural mowers market. Developers are designing systems that operate with minimal human intervention across large pastures and managed turf areas. Companies such as Husqvarna are advancing the exact positioning operating system (EPOS) technology to enable centimeter-level navigation accuracy. These systems are navigating obstacles and uneven terrain while performing routine mowing tasks. Farmers are reallocating labor toward supervisory and planning roles while automated equipment is handling repetitive operations. Improvements in battery technology are reducing operating costs, while advanced sensors are ensuring reliable performance under dusty, humid, or wet conditions.

Manufacturers are strengthening system intelligence through artificial intelligence (AI)-driven algorithms that optimize mowing patterns and reduce redundant coverage. Operators are supervising equipment fleets remotely through mobile applications that provide real-time operational data. As production volumes expand, declining unit costs are making autonomous systems accessible to mid-sized farms. Equipment manufacturers are offering modular autonomy packages that upgrade conventional mowers without full equipment replacement. Cooperative ownership models are allowing rural communities to share advanced machines and distribute investment risk. Governments are supporting digital agriculture through grants and incentive programs for smart farming tools. Buyers are prioritizing systems that support over-the-air software updates and seamless integration with crop monitoring platforms. These developments are shifting agricultural labor toward higher-value activities while improving operational consistency across growing seasons.

Contract Mowing and Farm Services Economy

Service-oriented agricultural models are opening alternative avenues for agricultural mower adoption. Providers are offering contract mowing, equipment-as-a-service (EaaS), and rental platforms that accommodate farms of different sizes. Farmers are selecting these options to avoid large upfront capital expenditure. Service hubs in countries such as India are linking machinery owners with nearby users through organized hiring networks. Providers are maintaining equipment fleets and managing repairs, which ensures dependable access to operational tools. This structure is serving operators who require mowing equipment during specific agricultural cycles without bearing ownership costs. Even digital aggregators are developing platforms that match service providers with farm clients in real time.

Utilization-based models are also reshaping revenue structures across the sector. Recurring service contracts are generating predictable income streams for both operators and equipment suppliers. Governments are supporting custom hiring frameworks to accelerate mechanization while limiting direct subsidy expenditure, while technology providers are integrating telematics systems that track equipment usage and improve scheduling efficiency. These service-led approaches are reducing entry barriers, supporting higher equipment utilization rates, and strengthening mechanization access for both smallholder farms and large commercial agricultural operations.

Category-wise Analysis

Product Type Insights

Disc mowers are anticipated to lead with an estimated 45% of the agricultural mower market revenue share in 2026. Their dominance is reflecting strong performance in dense forage crops and high operating speeds that support large-scale harvesting. These machines operate efficiently on uneven terrain, making them highly suitable for extensive hay production systems. Modular cutter bars and quick-change blade mechanisms are reducing downtime during narrow harvest windows. Manufacturers are integrating hydraulic float systems that protect turf surfaces and optimized drivetrains that improve fuel efficiency. As a result, commercial producers managing large acreages are prioritizing disc mowers for consistent field performance and reduced maintenance requirements.

Flail mowers are projected to register the fastest growth during the 2026–2033 forecast period. These machines are proving effective in heavy vegetation management, orchard maintenance, and roadside verge applications. Their mulching mechanism is shredding crop residues into smaller fragments that support faster soil integration. Operators are switching between hammer blades and Y-blades to adapt to varying vegetation density. Reinforced housing structures are protecting equipment from impacts caused by stones and debris in rough terrain. Municipal agencies and land management contractors are consciously selecting flail mowers as they operate safely near obstacles such as tree stumps or roadside litter.

Power Insights

Diesel-powered mowers are poised secure roughly 75% of the agricultural mower market share in 2026. These machines deliver strong performance in heavy-duty agricultural environments where durability and continuous operation are essential. Established supply networks are ensuring consistent availability of components and service support across major farming regions. Farm operators are relying on diesel systems due to long-standing operational familiarity and dependable performance during extended harvesting seasons. Diesel equipment is therefore remaining the preferred option for commercial farms and large-scale operations that prioritize reliability.

Electric mowers are projected to record the fastest growth between 2026 and 2033. Adoption is accelerating in environments where low-noise output and zero on-site emissions are important operational requirements. Landscaped estates, gardens, and environmentally sensitive areas are benefiting from these characteristics. Operators are valuing quiet performance that supports early-hour operations while maintaining improved air quality in managed landscapes. Advancements in battery energy density are extending runtime and improving operational reliability, aided by smart charging systems that are optimizing power use by aligning energy cycles with daily workloads.

Regional Insights

North America Agricultural Mowers Market Trends

North America is forecast to hold about 38% of the agricultural mowers market value in 2026. The United States is drives regional demand due to extensive farmland and a well-developed commercial turf management sector. OEMs are maintaining strong market presence through established dealer and service networks that support large-scale agricultural operations. Farmers in the region are adopting advanced technologies such as precision guidance systems and robotic mowing platforms to improve operational efficiency. These solutions are supporting both commercial turf maintenance and large agricultural fields that require reliable equipment performance across varied crops and terrain conditions. Canada is also contributing significant demand through its expansive pasturelands and structured landscaping services sector.

A stable regulatory environment is reinforcing technological advancement in the region. The U.S. EPA is enforcing Tier 4 Final emission standards, pushing manufacturers to develop cleaner and more efficient powertrain technologies. Investment is increasing in electrification, autonomous operation, and telematics systems that enable remote equipment monitoring. Farm operators are upgrading machinery fleets to capture productivity gains from connected platforms and data-driven management tools. Equipment manufacturers are introducing hybrid solutions that balance operational power with sustainability objectives. As a result, market growth in North America is likely to be steady through premium equipment replacement cycles and rapid technology integration.

Europe Agricultural Mowers Market Trends

Europe claims the second-largest share in the global market for agricultural mowers. Germany spearheads the regional market due to advanced farm mechanization and its role as a major manufacturing base for OEMs. The U.K. is generating strong demand through a well-established turf management sector that includes numerous golf courses and managed landscapes. France and Spain are contributing steady demand from vineyard and orchard farming, where specialized mowing equipment is essential for vegetation management between narrow crop rows. Farmers in these countries are relying on disc and flail mowers that deliver precise cutting performance in dense undergrowth and uneven terrain.

Policy frameworks across the region are shaping equipment purchasing decisions. The EU Farm to Fork Strategy and the European Green Deal are encouraging sustainable agricultural practices and cleaner machinery adoption. Governments are providing grants and tax incentives to support the transition toward electric and low-emission agricultural equipment. EU Stage V emission standards require manufacturers to redesign engine platforms for lower pollutant output. In response, OEMs are integrating precision technologies that optimize fuel efficiency and reduce operational waste, with farmers also adopting connected systems to support environmentally responsible operations.

Asia Pacific Agricultural Mowers Market Trends

The agricultural mowers market growth in Asia Pacific is expected to be the fastest through 2033, headlined by China on account of its vast agricultural land and strong government support through the Agricultural Machinery Purchase Subsidy Program. These incentives are lowering acquisition costs and accelerating equipment adoption among farmers. Domestic manufacturers are producing cost-efficient models tailored to local terrain and crop conditions. India is also strengthening mechanization through the SMAM program and the expansion of custom hiring centers that provide shared access to equipment. Rising rural incomes are enabling farm operators to invest in mechanized solutions that improve productivity and crop yields.

Mechanization is also accelerating across the ASEAN bloc. Farmers here are transitioning from manual vegetation control to powered equipment for pasture maintenance and crop residue management. Manufacturers are leveraging competitive production costs in China and India to supply both domestic markets and international exports. Governments are also investing in rural infrastructure improvements, widening the use of larger agricultural machinery across expanding road networks. Service networks are expanding to provide maintenance support and operator training, with farmers prioritizing fuel-efficient machinery as energy transitions reshape operating costs.

Competitive Landscape

The global agricultural mowers market exhibits a moderately consolidated structure, led by Deere & Company, Husqvarna, AGCO, CNH Industrial, and Kubota Corporation. These companies collectively account for roughly 35–40% of total market share. Their scale, engineering capabilities, and established distribution networks enable strong positioning in both agricultural and commercial turf segments. Beyond these leaders, the mid-tier and regional supplier landscape remains fragmented. Numerous local and specialized manufacturers compete by offering cost-efficient equipment and responsive service support tailored to regional farming conditions.

Competitive dynamics reflect a clear strategic divide within the industry. Premium OEMs are prioritizing technological differentiation through automation, connectivity, and data-driven farm management features. In contrast, regional manufacturers are focusing on affordability, simplified maintenance, and designs adapted to specific crops or terrain conditions. Buyers in emerging agricultural markets are often prioritizing equipment with accessible spare parts and rapid service turnaround. As a result, premium suppliers are pursuing higher-margin innovation strategies, while volume-focused producers are expanding geographic reach through practical and cost-competitive machinery solutions.

Key Industry Developments

- In October 2025, Kubota launched the RTV-X series of mowers, featuring enhanced diesel utility vehicles with variable hydraulic transmission, larger radiators, and improved suspension for better performance. These additions target farmers seeking reliable tools with ergonomic upgrades and expanded cargo options.

- In August 2025, Pandag Tech debuted its G1 robotic mower at Australia's AgQuip and Dowerin Field Day events, attracting strong interest from commercial operators, municipalities, and land managers. The wire-free model impressed with RTK and AI vision navigation, 78% slope handling, 25-acre coverage per charge, and modular electric design for easy maintenance.

- In May 2025, Vermeer expanded its hay equipment lineup with new triple mowers, rakes, and tedders. These additions target higher efficiency in forage operations, complementing earlier launches such as mower-conditioners.

Companies Covered in Agricultural Mowers Market

- Deere & Company

- Husqvarna Group

- AGCO Corporation

- CNH Industrial

- Kubota Corporation

- CLAAS KGaA mbH

- Krone

- Alamo Group Inc.

- MTD Products

- Briggs & Stratton Corporation

- Bosch

- AL-KO Gardentech

- Stiga Group

- Emak Group

- Textron Inc.

Frequently Asked Questions

The global agricultural mowers market is projected to reach US$ 2.3 billion in 2026.

Surge in farm mechanization to address labor shortages and boosts efficiency in forage management is primarily driving the market.

The agricultural mowers market is poised to witness a CAGR of 6.2% from 2026 to 2033.

Major opportunities lie in developing electric/autonomous mowers that can tap into the massive demand for low-emission, smart farming solutions.

Deere & Company, Husqvarna Group, AGCO Corporation, CNH Industrial, and Kubota Corporation are some of the key players in the market.