- Automotive

- U.S. Agricultural Tractor Market

U.S. Agricultural Tractor Market Size, Share, and Growth Forecast, 2026 - 2033

U.S. Agricultural Tractor Market by Engine power (Less than 40 HP, 40-100 HP, 100-200 HP, More than 200 HP), Driveline Type (2WD (Two-Wheel Drive), 4WD (Four-Wheel Drive / Front-Wheel Assist)), Fuel Type (Diesel, Gasoline, Electric), Tractor Type (Compact, Utility, Row Crop, High-Horsepower, Orchard / Vineyard) and Regional Analysis for 2026 - 2033

U.S. Agricultural Tractor Market Size and Trends Analysis

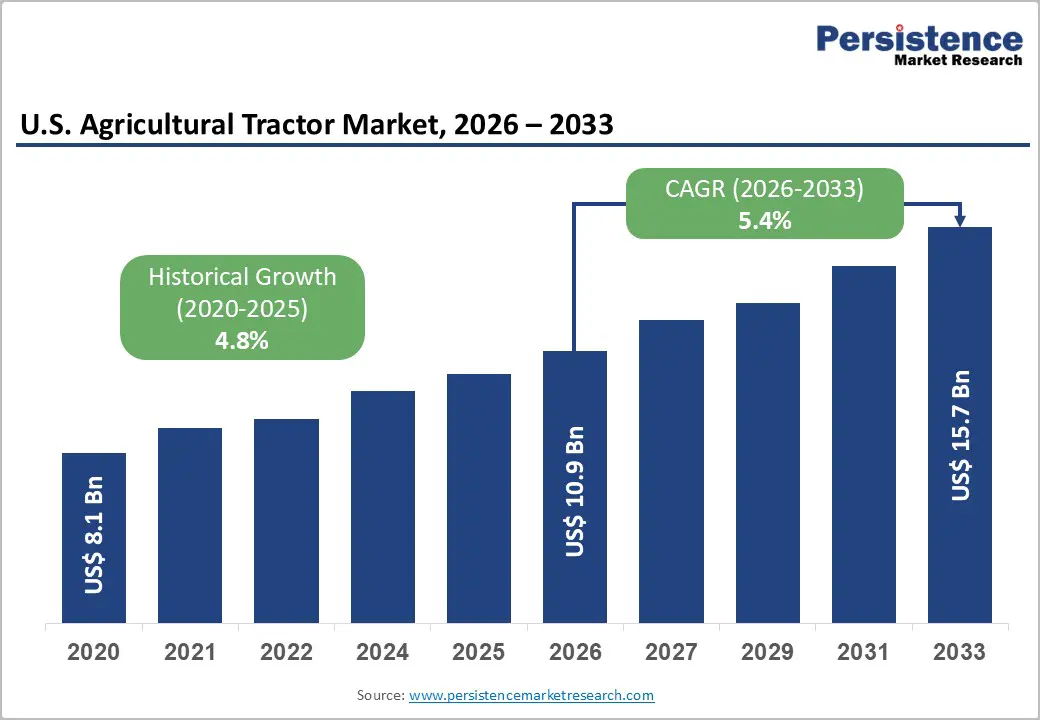

The U.S. agricultural tractor market size is likely to be valued at US$ 10.9 billion in 2026 and is projected to reach US$ 15.7 billion by 2033, growing at a CAGR of 5.4% between 2026 and 2033. The market recorded a historical CAGR of 4.8% between 2020 and 2026, advancing from a base of US$ 8.1 Bn in 2020. This forward momentum is underpinned by sustained farm mechanisation, escalating labour shortages across U.S. agricultural regions, and the accelerating integration of precision agriculture technologies.

Federal farm support programs and USDA-backed conservation financing continue to strengthen farmers' capacity to invest in equipment. Despite short-term headwinds, including a 4.7% decline in total tractor sales reported by the Association of Equipment Manufacturers (AEM) for January 2026, long-term structural demand remains firmly supported by the modernisation imperative across mid-to-large-scale U.S. farming operations.

Key Industry Highlights

- 100-200 HP Leads Demand: The 100-200 HP segment dominates with 38% market share in 2026, driven by its versatility across grain, hay, and mixed-crop farming in the Midwest and Great Plains.

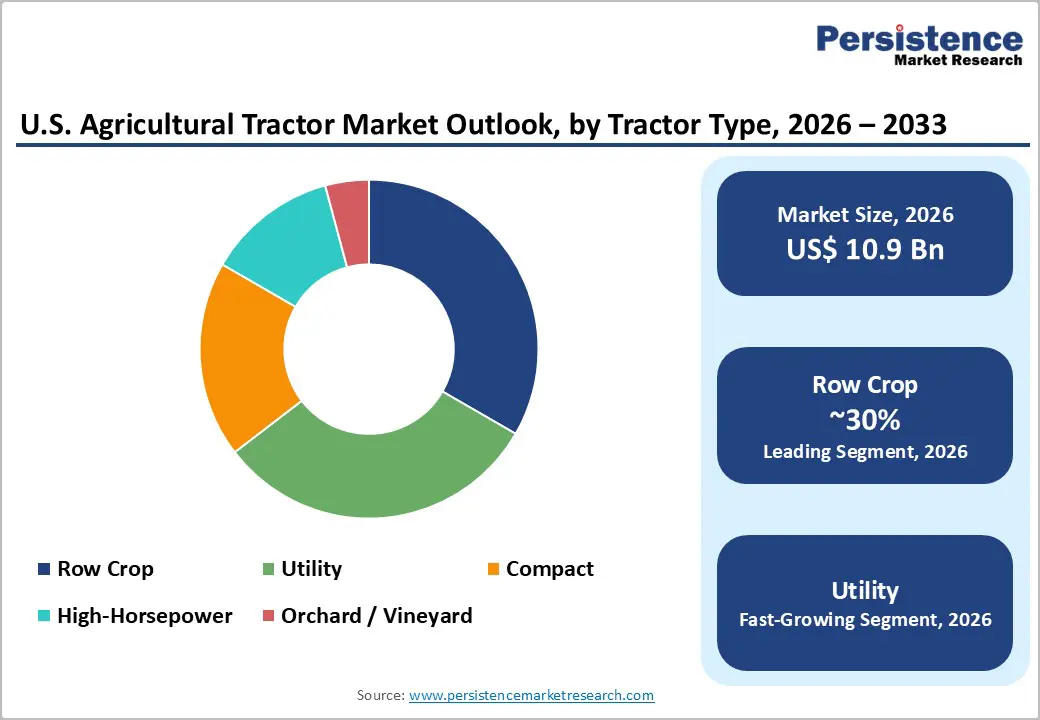

- Dominant Tractor Type: Row Crop tractors hold 32% of the market, supported by strong corn and soybean production across major U.S. grain-producing states.

- Leading Fuel Type: Diesel-powered tractors account for 82% of total sales, underpinned by high torque efficiency and well-established rural fuel infrastructure.

- Fast-growing Engine Power: The 40-100 HP category is expanding steadily, supported by speciality crop farms, livestock operations, and rising rural property ownership.

- Precision Technology: Over 50% adoption in key grain states is accelerating replacement cycles, with OEMs such as John Deere integrating advanced guidance, telematics, and automation systems into new platforms.

- Labour Shortage-Driven Automation: Acute farm labour constraints are accelerating demand for autonomous and semi-autonomous tractors, exemplified by innovations from Kubota Corporation and other leading OEMs.

- Electrification & Sustainability Opportunity: Electric and low-emission tractors, including platforms introduced by AGCO Corporation, represent a high-growth frontier aligned with U.S. conservation incentives and long-term decarbonisation goals.

| Key Insights | Details |

|---|---|

| U.S. Agricultural Tractor Market Size (2026E) | US$ 10.9 Bn |

| Market Value Forecast (2033F) | US$ 15.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.8% |

Market Dynamics

Drivers - Acute Farm Labour Shortages Catalysing Tractor Adoption Across U.S. Farming Operations

Farm labour scarcity has emerged as one of the most persistent structural forces propelling tractor adoption across the United States. The USDA consistently identifies labour availability as a critical constraint on farm productivity, particularly for medium and large-scale operations. As manual operations become economically unsustainable, operators in the U.S. Agricultural Tractor Market are prioritising mechanical and autonomous solutions. Kubota's M7004 Autonomous concept, introduced at Agritechnica in November 2025, is designed to automate up to 80% of field operations, directly addressing labour displacement concerns.

The Kubota Agtonomy collaboration, announced in June 2025, integrates automation sensors and data platforms for speciality crop farms across California, Oregon, and Washington regions, where labour constraints are particularly acute. These developments illustrate that OEM investment in autonomy is directly calibrated to the real-world labour supply challenge confronting U.S. agriculture.

Precision Agriculture Technology Integration: Accelerating Equipment Upgrade Cycles

The deepening penetration of precision agriculture technologies is driving a sustained replacement cycle in the U.S. Agricultural Tractor Market, as older equipment becomes incompatible with modern farm management systems.

According to the USDA's America's Farms and Ranches at a Glance: 2024 Edition, 68% of large-scale crop farms now utilise decision-support technologies such as yield monitors, yield maps, and soil maps compared to just 13% of small-scale farms. Variable-rate technology (VRT) is deployed on 45% of large-scale farms, and auto-steer systems are in use on approximately 70% of large farms nationwide. John Deere's newly launched 8R and 8RX series tractors (March 1, 2026) integrate AutoTrac™, AutoPath™, and JDLink™ Boost precision systems into machines delivering up to 540 HP. Nationally, 27% of all farms used precision agriculture tools in 2023, with adoption exceeding 50% in major grain-producing states, confirming a broad-based demand impulse for technologically advanced tractors.

U.S. Federal Agricultural Policy and Investment Frameworks Supporting Farm Equipment Procurement

Federal policy frameworks play a direct role in stimulating capital expenditure within the U.S. Agricultural Tractor Market. The USDA's Farm Service Agency (FSA) Operating and Ownership Loan programs provide subsidised financing for farm machinery purchases, reducing acquisition costs for qualifying operators.

The Inflation Reduction Act (IRA) of 2022 directed over US$ 19.5 billion toward USDA conservation programs over five years, including the Environmental Quality Incentives Program (EQIP), which incentivises the adoption of fuel-efficient, precision-capable equipment. These policy-backed financial instruments mitigate capital expenditure barriers, sustaining demand even during periods of soft commodity prices. Deere & Company's raised full-year net income guidance of US$ 4.5-5.0 billion reflects manufacturer confidence underpinned in part by the structural stability provided by federal agricultural investment frameworks.

Restraint - Elevated Capital Investment Requirements and Tighter Farm Financing Conditions

The high unit cost of modern agricultural tractors represents a significant procurement barrier, particularly among small and mid-sized operations. High-horsepower models command premium price points that require multi-year financing arrangements, and tighter credit conditions are visibly affecting purchasing behaviour.

AEM data from January 2026 reveals a 25.9% year-over-year decline in 100+ HP tractor sales and an 18.8% drop in 4WD tractor units directly reflecting the postponement of large capital expenditures amid margin compression. Dealer inventory levels stood at 88,482 units at the beginning of January 2026, exerting additional downward pressure on pricing and production scheduling decisions by manufacturers.

Opportunity - Electrification of Farm Equipment: Opening a New Technology Frontier in the U.S. Agricultural Tractor Market

The electrification of agricultural tractors represents a transformative opportunity for manufacturers and operators in the U.S. Agricultural Tractor Market, driven by tightening emission standards, rising diesel fuel costs, and an industry-wide pivot toward sustainable farming. Battery-powered and hybrid tractors are transitioning from concept phases into commercially viable products, with notable momentum from major OEMs.

AGCO Corporation's debut of the Fendt e100 Vario® battery-powered tractor at the World Ag Expo in Tulare, California, marked the first North American introduction of a fully electric utility tractor from a major global manufacturer signaling that electric drivetrains are no longer confined to niche or experimental platforms. Furthermore, CNH Industrial's multi-year licensing collaboration with Monarch Tractor to co-develop fully electric, low-horsepower autonomous tractors underscores the strategic significance that leading manufacturers place on electrification. As USDA conservation programs under the IRA continue to incentivise environmentally sound farming practices, electric tractor adoption is positioned to receive additional policy tailwinds and financial incentives in the near term.

Autonomous and Semi-Autonomous Technology Addressing Labor and Productivity Gaps in Tractor Operations

Autonomous tractor technology presents a highly actionable opportunity within the U.S. Agricultural Tractor Market, as farm labor availability worsens and operators seek cost-efficient productivity solutions. Autonomous systems enable extended operational hours, GPS-precise field coverage, and reduced reliance on skilled operators, delivering measurable improvements in cost-per-acre metrics for large and mid-scale farms.

Kubota's M7004 Autonomous concept, unveiled at Agritechnica in November 2025, is designed to handle up to 80% of field tasks autonomously, targeting speciality and mixed-crop operations where labour dependency is highest. John Deere's 8R/8RX tractor lineup launched in March 2026 with up to 540 HP integrates AutoPath™ and AutoTrac™ precision guidance for fully automated tillage, planting, and field operations. The USDA reports that precision agriculture adoption rates exceed 50% in major grain states, confirming that the digital and connectivity infrastructure required for autonomous tractor functionality is already deeply embedded across large portions of the U.S. farming sector.

Digital Connectivity Platforms Strengthening Dealer-Farmer Relationships and Aftermarket Revenue

The emergence of digital ownership and connectivity platforms is creating a new value-creation layer within the U.S. Agricultural Tractor Market, enabling OEMs to deepen customer relationships beyond the point of sale and generate recurring aftermarket revenue streams. These platforms integrate equipment monitoring, service scheduling, financing management, and operational analytics into unified user-facing applications.

KIOTI Tractor's KIOTI Connect 2.0, launched February 11, 2026, delivers end-to-end support from equipment selection and customisation to financing, maintenance, and real-time connected machine monitoring, exemplifying the commercial potential of this model. Kubota Tractor Corporation's implementation of Syncron Retail Inventory further illustrates the strategy by optimising parts availability and inventory replenishment efficiency across U.S. dealer networks. As the USDA reports that 27% of all U.S. farms have adopted precision agriculture tools a figure expected to climb as digital literacy among operators matures, OEMs that invest in robust digital ecosystems are positioned to capture greater lifetime customer value and strengthen supply chain competitiveness.

Category-wise Analysis

Engine Power Insights

The 100-200 HP segment commands the largest share of the U.S. Agricultural Tractor Market in 2026, accounting for approximately 38% of total market revenue. This horsepower range provides the optimal balance between operational versatility and cost efficiency, making it the preferred configuration for grain cultivation, hay operations, and mid-to-large-scale general farming across the Corn Belt, Great Plains, and Southeast regions. These tractors are broadly compatible with planters, sprayers, and front-end loaders and align closely with USDA-defined mid-to-large farm typologies where mechanisation investment delivers the strongest economic return. Sustained capital allocation toward this segment reflects the structural role it plays in the day-to-day productivity of U.S. commercial agriculture.

The 40-100 HP segment is the fastest-growing engine power category, supported by Association of Equipment Manufacturers (AEM) January 2026 data showing an 8.8% year-over-year increase in 2WD tractor sales in this horsepower class, a notable contrast to declines recorded across all other power bands during the same period. This resilience reflects continued activity among medium-sized and speciality crop farmers requiring versatile, cost-effective equipment for planting, cultivation, and material-handling tasks.

Diesel Type Insights

Diesel-powered tractors retain a dominant position in the U.S. Agricultural Tractor Market, accounting for approximately 82% of the fuel-type segment in 2026. Diesel's supremacy is rooted in its superior torque output at low RPMs, fuel efficiency under heavy load conditions, and the established rural diesel supply infrastructure across U.S. farming regions. High-horsepower platforms including Case IH's Optum® series (360-435 HP, featuring the Cursor 9 diesel engine and John Deere's 8R/8RX lineup (up to 540 HP) are both engineered on diesel drivetrains, reinforcing the segment's structural importance for large-scale row crop, planting, and heavy tillage applications in the near-to-medium term.

Gasoline-powered tractors, primarily deployed in sub-compact and compact utility applications, represent the fastest-growing fuel-type segment. This momentum is driven by expanding hobbyist farming, rural estate management, and small-property-maintenance markets, where gasoline-powered compact tractors offer cost-effective, low-maintenance solutions for landscaping, snow removal, and light field work. The relative affordability and mechanical simplicity of gasoline-powered models make them accessible entry-level products, serving a customer base that overlaps with the broader demand dynamics observed in the 40-100 HP horsepower band.

Tractor Type Insights

Row Crop tractors lead the tractor type segmentation, capturing approximately 32% of the U.S. Agricultural Tractor Market in 2026. These tractors are purpose-built for planting, cultivating, and harvesting corn, soybeans, cotton, and other row-planted crops the foundational commodities of U.S. agriculture. Their adjustable wheel spacing, high ground clearance, and compatibility with precision farming implements make them indispensable across the Midwest, Great Plains, and Southern states. John Deere's 8R and 8RX tractor series, launched at Commodity Classic in March 2026 with up to 540 HP and fully integrated precision guidance, are engineered specifically for high-intensity row crop environments, underscoring continued OEM investment in this dominant category.

Utility tractors are the fastest-growing tractor type, driven by their application versatility across livestock operations, hay production, small-grain farming, and general-purpose rural property maintenance. Unlike specialised row crop or high-horsepower tractors, utility models serve a broader customer base from family farms and hobby operations to mid-scale commercial producers. The growing rural homesteading trend and expanding non-traditional agricultural user base are key demand vectors. AGCO's updated Massey Ferguson equipment lineup and KIOTI's KIOTI Connect 2.0 digital platform both address the utility segment, confirming its commercial attractiveness for leading manufacturers.

Competitive Landscape

The U.S. Agricultural Tractor Market is largely consolidated, dominated by a few major global and domestic players who control significant market share and influence technology adoption and dealer networks. Leading companies like John Deere, Case IH, and AGCO Corporation offer a wide range of high-horsepower tractors, precision agriculture solutions, and advanced automation technologies for large-scale row-crop and speciality farms. Kubota and Mahindra & Mahindra have strengthened their presence through compact tractors, autonomous concepts, and connected solutions targeting small- to mid-size farms and speciality crops.

CNH Industrial is advancing electrification and autonomous tractors in collaboration with U.S. AgTech startups, highlighting the focus on sustainable and precision farming. While these key players dominate the market, smaller manufacturers continue to innovate in niche segments, keeping competitive pressure high. Overall, the market is consolidated but technology-driven, with success strongly tied to product differentiation, dealer networks, and after-sales support.

Key Industry Developments

- In March 2026, John Deere launched six new 8R and 8RX tractor models at Commodity Classic in Olathe, Kansas, featuring up to 540 horsepower, redesigned chassis, and advanced Intelligent Power Management for peak performance. These tractors include precision agriculture technologies such as AutoTrac™, AutoPath™, and JDLink™ Boost, enhancing productivity, efficiency, and versatility for planting, tillage, and heavy-duty field operations.

- In February 2026, AGCO Corporation showcased innovations at the World Ag Expo in Tulare, California, including the North American debut of the Fendt e100 Vario® battery-powered tractor and updated Massey Ferguson equipment. These launches emphasise high-efficiency, electrification, and precision agriculture technologies, reflecting AGCO’s commitment to resource conservation and enhanced productivity for U.S. farmers.

Companies Covered in U.S. Agricultural Tractor Market

- Deere & Company

- AGCO Corporation

- Kubota Corporation

- CNH Industrial N.V.

- Mahindra Group

- Kioti Tractor

- Yanmar

- Argo Tractors S.p.A.

- New Holland

- Case IH

- Massey Ferguson

Frequently Asked Questions

The U.S. Agricultural Tractor Market is projected to be valued at US$ 10.9 Bn in 2026.

The 100-200 HP segment is expected to account for approximately 38% of the U.S. Agricultural Tractor Market by Engine Power in 2026.

The market is expected to witness a CAGR of 5.4% from 2026 to 2033.

The U.S. Agricultural Tractor market growth is driven by acute farm labour shortages, accelerating mechanisation and autonomy adoption, rising precision agriculture integration prompting equipment upgrade cycles, and supportive federal financing and conservation incentives that reduce capital barriers and sustain farm machinery investment.

Key market opportunities in the U.S. Agricultural Tractor Market lie in electrification of farm equipment, expansion of autonomous and semi-autonomous tractor technologies to address labour and productivity gaps, and the growth of digital connectivity platforms that enhance precision farming integration, aftermarket revenue, and long-term dealer-farmer engagement.

Key players in the Agricultural Tractor Market include Deere & Company, CNH Industrial N.V., AGCO Corporation, and Kubota Corporation.