- Semiconductor Electronics

- 5G Enterprise Market

5G Enterprise Market Size, Share, and Growth Forecast, 2026 - 2033

5G Enterprise Market by Access Equipment (Service Node, Radio Node, Small Cells), Core Technology (Network Functions Virtualization, Software-Defined Networking), End-user (Manufacturing, Healthcare & Life Science, Others), and Regional Analysis 2026 - 2033

5G Enterprise Market Size and Trends Analysis

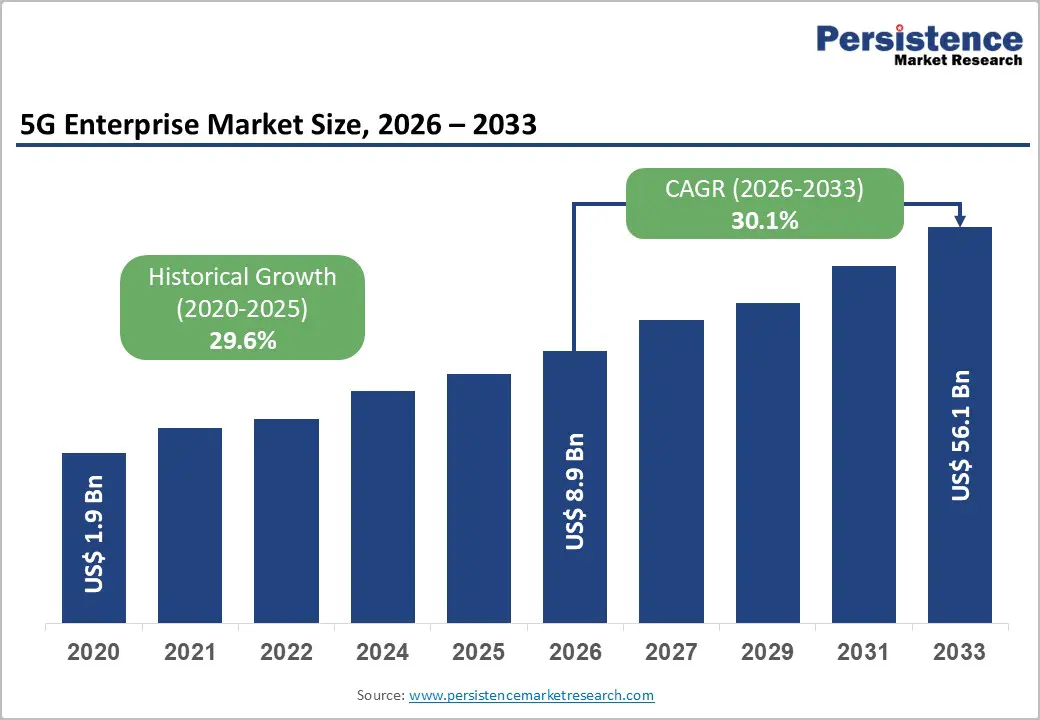

The global 5G enterprise market size is likely to be valued at US$8.9 billion in 2026 and is expected to reach US$56.1 billion by 2033, growing at a CAGR of 30.1% during the forecast period from 2026 to 2033, driven by rapid industrial digitalization and rising demand for low-latency connectivity. Enterprises are adopting private 5G networks to enable real-time automation, particularly in manufacturing.

The integration of edge computing further supports faster data processing and efficient IoT operations. Overall, market expansion is closely tied to the shift toward private, high-performance network architectures for mission-critical applications.

Key Industry Highlights:

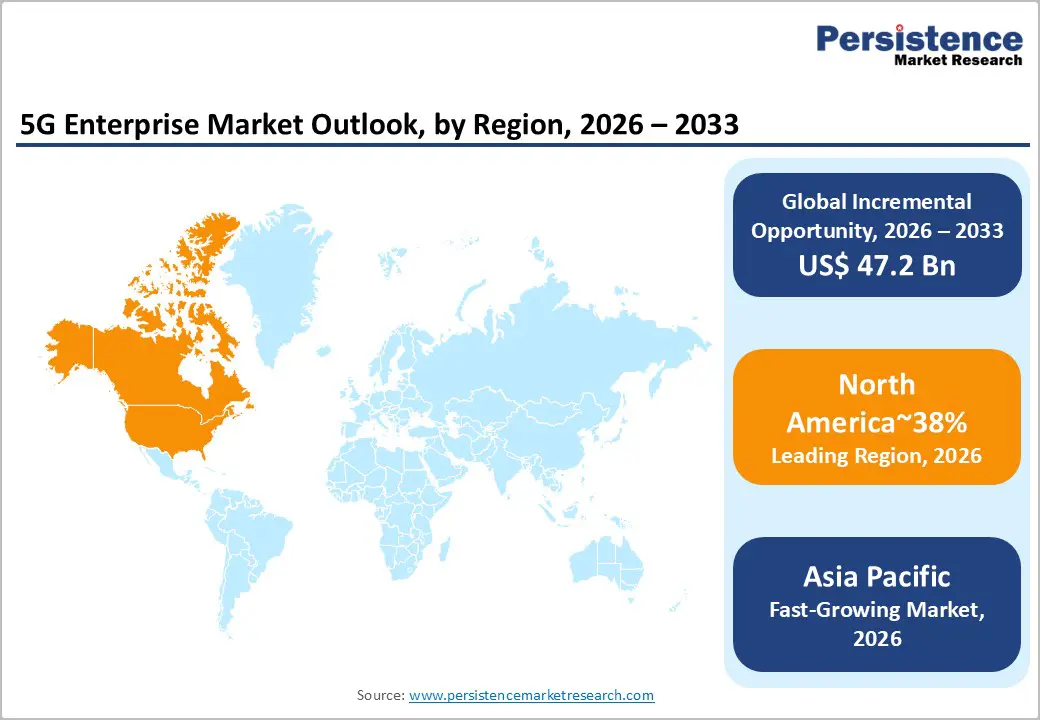

- Leading Region: North America is projected to lead, accounting for approximately 38% share in 2026, supported by mature spectrum allocations, dense industrial clusters, and robust vendor ecosystems.

- Fastest-growing Region: Asia Pacific is anticipated to grow the fastest, driven by rapid infrastructure buildout, manufacturing scale-up, and government-led digitization initiatives.

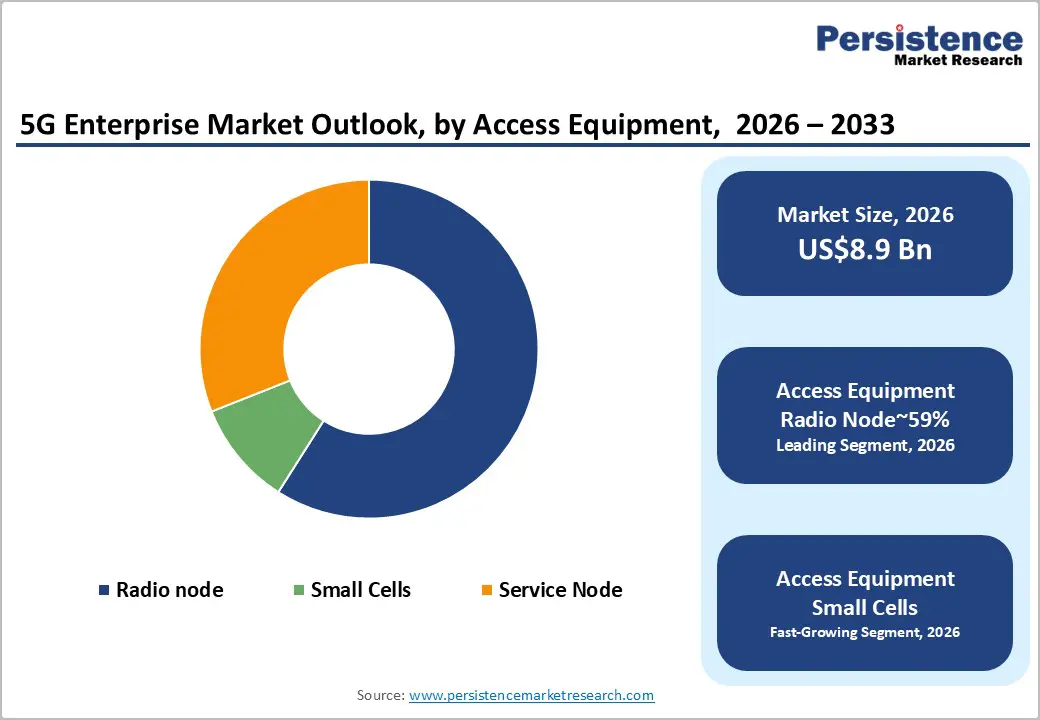

- Leading Access Equipment: Radio node is expected to lead, accounting for approximately 59% share in 2026, anchored by high deployment density in campus networks and seamless integration with existing infrastructure.

- Leading End-user: Manufacturing is projected to dominate, holding approximately 25% share in 2026, driven by Industry 4.0 integration and autonomous robotics requirements.

| Key Insights | Details |

|---|---|

| 5G Enterprise Market Size (2026E) | US$8.9 Bn |

| Market Value Forecast (2033F) | US$56.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 30.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 29.6% |

DRO Analysis

Driver - Industrial Automation Integration

The transition toward Industry 4.0 is generating massive demand for high-reliability wireless backbones. Manufacturers require seamless connectivity to support autonomous mobile robots within complex factory environments. Low-latency performance remains a critical requirement for real-time synchronization across distributed production lines. This shift is set to eliminate physical cabling constraints in modular assembly facilities. Enterprise digitalization strategies prioritize wireless agility to maintain global competitiveness in high-output sectors. Enhanced spectral efficiency underpins the widespread utilization of private cellular networks for mission-critical tasks.

Reliable data transmission protocols ensure consistent performance for high-precision industrial machinery operations. Robust infrastructure investments sustain the momentum toward fully automated and connected factory floors. Nokia, with Digital Automation Cloud, reinforces operational resilience through scalable private network deployments globally. Procurement of high-capacity hardware is positioned to increase as production facilities scale digital operations. Ericsson with Private 5G addresses these requirements by delivering dedicated connectivity for diverse industrial workloads. Integrated software platforms facilitate simplified management of complex device ecosystems across modern enterprises.

Massive IoT Proliferation

The exponential increase in connected devices is necessitating high-density network support for modern enterprises. Scalable connectivity frameworks allow for the simultaneous management of thousands of industrial sensors. Reliable machine-to-machine communication remains fundamental for the success of smart utility monitoring systems. This trend is forecast to drive the adoption of narrowband 5G protocols. Enhanced device battery life underpins the long-term viability of massive IoT sensor deployments. Organizations prioritize network stability to ensure uninterrupted data collection from remote or inaccessible assets.

Standardized connectivity solutions are expected to reduce the complexity of managing global IoT fleets. Improved protocol interoperability facilitates the seamless exchange of data across heterogeneous device categories. Qualcomm’s Snapdragon X80 5G Modem-RF System addresses these requirements through advanced 5G-Advanced technology integration. High-throughput capabilities support the transmission of high-definition video for remote surveillance applications. ZTE with Minimalist Private 5G-A enables efficient broadcasting and media workflows through simplified architecture. This alignment between device density and network capacity fuels industrial monitoring expansion.

Restraint - Security and Privacy Concerns

Expanding attack surfaces in 5G-enabled environments are raising significant cybersecurity alarms for enterprise IT leaders. High-speed connectivity facilitates faster data exfiltration if network defenses are successfully breached by attackers. Privacy risks associated with localized data processing necessitate robust encryption and identity management protocols. These concerns are likely to dampen enthusiasm for 5G among highly regulated sectors. Compliance with evolving data residency laws adds another layer of complexity to network administration. Trust in cloud-managed infrastructure remains a sensitive topic for government and defense agencies.

Heightened vulnerability to sophisticated network-level attacks necessitates continuous investment in advanced security software suites. Organizations must implement zero-trust architectures to safeguard sensitive intellectual property within distributed networks. Palo Alto Networks, with 5G Security, addresses these risks through integrated visibility and threat prevention. Misconfigured network slicing parameters could lead to unintended data leakage between different enterprise departments. Microsoft, with Azure Private 5G Core, focuses on delivering secure and compliant connectivity frameworks. Despite these advancements, the perception of risk continues to influence the pace of adoption.

High Deployment Expenditure

Initial capital requirements for private 5G infrastructure represent a significant barrier for mid-sized enterprises. Procurement of dedicated spectrum and radio hardware necessitates substantial upfront financial commitments from organizations. High engineering costs for customized network design further inflate the total cost of ownership. This financial burden is poised to slow adoption rates among budget-constrained manufacturing firms. Long-term return on investment cycles complicate the justification for rapid technological migration projects. Complexity in integrating legacy systems with new 5G cores adds further implementation costs.

Downstream commercial impacts include delayed modernization plans for facilities requiring extensive infrastructure overhauls. Limited availability of skilled networking personnel increases the reliance on expensive third-party managed services. Dell, with its Private Wireless Program, attempts to mitigate these barriers through standardized deployment models. High licensing fees for proprietary software platforms remain a persistent challenge for many vendors. Samsung with vCore addresses cost concerns by offering flexible and virtualized core network solutions. Nevertheless, the cost of specialized end-user devices continues to constrain market penetration levels.

Opportunity - AI-Native Network Optimization

The integration of artificial intelligence is creating opportunities for self-healing and autonomous network management. AI algorithms can predict traffic patterns and dynamically allocate resources to optimize enterprise performance. Automated fault detection reduces downtime for critical industrial processes by identifying issues before failure. This technological inflection is anticipated to lower operational expenditures for complex 5G network owners. Enhanced network visibility supports more granular service-level agreement monitoring for mission-critical enterprise applications. Intelligent optimization underpins the efficiency of large-scale private deployments in smart cities.

Pursuing this opportunity allows vendors to differentiate through software-defined value-added services and intelligent platforms. Advanced analytics enable enterprises to derive deeper insights from their internal communication traffic patterns. Real-time optimization improves the user experience for mobile workers in data-intensive enterprise environments. Nokia, with MX Workmate, integrates AI to assist industrial workers through real-time data visualization. Strategic focus on AI-driven automation remains a key growth lever for market participants.

Smart Logistics and Warehousing

The demand for fully-automated warehouses is generating significant opportunities for high-capacity 5G network solutions. Autonomous guided vehicles require uninterrupted connectivity to navigate complex and dynamic storage environments safely. Real-time inventory tracking through 5G-connected sensors improves supply chain transparency and operational efficiency. This technology shift is set to redefine the throughput capabilities of global logistics hubs. Enhanced location tracking services support more precise asset management across large-scale distribution centers. Organizations prioritize network densification to eliminate coverage gaps in dense metal-racking warehouse structures.

Strategic partnerships between logistics providers and telecom vendors are accelerating the rollout of smart hubs. Integrated tracking platforms provide end-to-end visibility for high-value goods during transit and storage phases. ZTE with Private 5G as a Service enables logistics firms to deploy flexible network capacity. Lower latency improves the responsiveness of automated sorting systems in high-volume e-commerce facilities. Verizon’s Private 5G for Logistics addresses the connectivity needs of modern port and shipping operations. Ongoing urbanization and e-commerce growth continue to fuel demand for advanced logistics infrastructure.

Category-wise Analysis

Access Equipment Insights

Radio node is expected to dominate, accounting for approximately 59% share in 2026, underpinned by the essential requirement for network densification. Small cell deployments are critical for providing high-capacity coverage within indoor industrial environments and dense urban campuses. Adoption remains anchored in the need for low-latency transmission across numerous end-user devices in factories. Ericsson’s Radio Dot System and Nokia’s AirScale exemplify the hardware standards required for these high-density enterprise environments. Continuous enhancements in MIMO technology further strengthen the signal reliability of modern access equipment platforms. This structural alignment between coverage requirements and hardware capability sustains the segment's leadership.

Small cells are anticipated to be the fastest-growing segment, driven by the increasing demand for localized high-performance connectivity. Conventional macro-cell coverage often fails to penetrate complex industrial structures with significant metal interference or thick walls. Advanced radio architectures enable precise signal targeting to support specific high-bandwidth applications on the factory floor. Samsung’s Link Cell and Huawei’s LampSite address the need for flexible and high-capacity indoor network coverage. Integration of power-efficient designs supports the sustainable scaling of private 5G infrastructure for large enterprises. As organizations prioritize precision and throughput, localized radio nodes are gaining traction across evolving industrial ecosystems.

End-user Insights

Manufacturing is projected to lead, holding approximately 25% share in 2026, driven by the widespread implementation of Industry 4.0. Large-scale production facilities require high-bandwidth and low-latency networks to support autonomous assembly lines and predictive maintenance. This structural demand remains anchored in the necessity for real-time data exchange between millions of industrial sensors. Manufacturers prioritize private 5G to ensure data security and maintain control over critical production uptime. Huawei’s Kite Solution and Ericsson’s Private 5G address these specific industrial connectivity and security requirements. Ongoing digital transformation initiatives in the automotive and electronics sectors further bolster the segment's market position. This alignment between industrial automation goals and 5G capabilities sustains the manufacturing sector's leadership.

Healthcare & life sciences are expected to be the fastest-growing end-user segment, driven by the emerging need for remote surgical assistance and telemedicine. High-resolution medical imaging and real-time robotic surgery require the ultra-reliable and low-latency performance that only 5G can provide. Adoption is accelerating as hospitals seek to modernize diagnostic workflows and enhance patient monitoring through connected devices. Samsung with 5G-powered Medical Devices and NEC with 5G Healthcare Solutions address the stringent reliability needs of medical environments. Integration of 5G into emergency services and ambulances supports faster data transmission during critical patient transit phases. As the healthcare sector prioritizes digital resilience and remote access, 5G adoption is forecast to expand rapidly.

Regional Insights

North America 5G Enterprise Market Trends

North America is expected to remain the leading regional market, accounting for approximately 38% share in 2026, supported by a high concentration of technology vendors and early spectrum availability. The region's dominance is anchored in the rapid adoption of private cellular networks among large-scale industrial and logistics enterprises. Mature digital infrastructure allows for the seamless integration of 5G with existing cloud and edge computing frameworks. High R&D investments by domestic telecommunications giants sustain the momentum of next-generation wireless technology development.

The U.S. is forecast to anchor regional momentum through sustained federal investments in secure and resilient 5G infrastructure for government agencies. Government-led initiatives promoting domestic semiconductor production and advanced networking technologies are anticipated to accelerate adoption among defence and aerospace contractors. Cisco with Private 5G remains positioned to benefit from large-scale enterprise modernization projects across the American manufacturing and healthcare sectors. Regulatory clarity regarding the CBRS band has already facilitated numerous private network deployments in commercial and industrial sites.

Asia Pacific 5G Enterprise Market Trends

Asia Pacific is expected to register the fastest growth trajectory, as rapid industrialization and government-led infrastructure initiatives accelerate market expansion. The region's momentum is anchored in the expansion of massive smart manufacturing clusters requiring high-density wireless connectivity. Dense urban populations and rapid urbanization drive the demand for 5G-enabled smart city and utility management solutions. Strategic focus on becoming a global hub for high-tech production necessitates the deployment of advanced communication networks. Forward-looking regulatory frameworks in several leading economies facilitate the early testing and adoption of 5G-Advanced technologies.

China is anticipated to lead the regional acceleration through its massive national strategy for 5G industrial integration and large-scale factory automation. The government's "5G + Industrial Internet" initiative has already resulted in thousands of private network installations across diverse industrial sectors. Huawei with AI WAN Solution and ZTE with Minimalist Private 5G-A are deeply embedded in these national digitalization projects. Rapid rollout of 5G Standalone networks provides the necessary foundation for advanced network slicing and ultra-low latency enterprise applications. High domestic production of 5G-enabled hardware and sensors further lowers the barrier to entry for local manufacturing firms.

Europe 5G Enterprise Market Trends

Europe is expected to remain a mature and structurally stable regional market, with demand primarily anchored in high-end manufacturing and automotive sectors. The region's market profile is supported by strict data privacy regulations that favor the deployment of secure private 5G networks. Industrial demand is driven by the need for high-precision connectivity in the production of complex machinery and luxury vehicles. Adoption remains anchored in the transition toward green manufacturing and energy-efficient industrial processes enabled by 5G. Collaborative research initiatives between academia and industry reinforce the long-term innovation potential of the regional market.

Germany is set to anchor the European 5G enterprise landscape through its world-leading automotive and industrial engineering base. The localized allocation of the 3.7-3.8 GHz spectrum for industrial use has empowered hundreds of German firms to deploy independent private networks. Nokia with Digital Automation Cloud and Ericsson with Private 5G address the stringent reliability and security needs of German "Mittelstand" and large enterprises. Regulatory focus on industrial sovereignty and data security sustains the procurement of high-performance wireless infrastructure within the country. Sustained investment in autonomous vehicle testing and smart logistics hubs continues to drive demand for low-latency communication solutions.

Competitive Landscape

The global 5G enterprise market is moderately consolidated, led by Ericsson, Nokia, and Huawei, supported by strong IP portfolios, scale, and standardized architectures. Their influence is reinforced through interoperability, long-term contracts, and advanced capabilities such as network slicing and low-latency performance.

Competition is driven by open architectures and cloud-native deployments. Players such as Cisco are expanding core and analytics capabilities, while partnerships with Amazon Web Services and Qualcomm enable hybrid ecosystems. The market is shifting toward platform-based competition, with AI-driven optimization emerging as a key differentiator in edge-focused enterprise deployments.

Key Industry Developments:

- In February 2026, Industrial AI, NTT DATA, and Ericsson teamed up to scale Private 5G and physical AI for global enterprises. This partnership focuses on combining private cellular infrastructure with "Physical AI" (robotics/drones) to automate complex logistics and manufacturing environments at scale.

- In November 2025, Nokia reorganized into two primary segments (Network & Mobile Infrastructure) to capture the AI super cycle. By streamlining around AI-driven data centers and mobile standards, Nokia aims to accelerate R&D in AI-native 6G and premium 5G-Advanced performance.

Companies Covered in 5G Enterprise Market

- Ericsson

- Nokia

- Huawei

- Cisco

- Samsung

- Qualcomm

- Amazon Web Services

- Microsoft Azure

- Google Cloud

- ZTE

- NEC Corporation

- Fujitsu

- Hewlett-Packard Enterprise

- Dell Technologies

- Intel

- VMware

Frequently Asked Questions

The global 5G enterprise market is likely to be valued at US$ 8.9 billion in 2026. It is expected to reach US$ 56.1 billion by 2033.

Growth is primarily driven by industrial automation and the integration of Industry 4.0 technologies. Demand for low-latency connectivity for autonomous robotics and IoT sensors remains a critical structural force.

The 5G enterprise market is expected to grow at a CAGR of 30.1% during the forecast period from 2026 to 2033.

North America is expected to lead the market, accounting for approximately 38% share in 2026. This leadership is supported by mature technology ecosystems and early 5G spectrum allocation for enterprises.

Major participants include Ericsson, Nokia, Huawei, Samsung, Cisco, ZTE, NEC, and Qualcomm. These firms provide the critical RAN and core technology required for private 5G deployments.