- Specialty & Fine Chemicals

- 1,4 Butanediol Market

1,4 Butanediol Market Size, Share, and Growth Forecast, 2025 - 2032

1,4 Butanediol Market by Production Process (Reppe Process, Davy Process, Butadiene-Based Process, Propylene Oxide-Based Process, Bio-fermentation Route), Derivative (Tetrahydrofuran, Polybutylene Terephthalate, Gamma-Butyrolactone, Polyurethane, Other Derivatives), End-use, and Regional Analysis for 2025 - 2032

1,4 Butanediol Market Size and Trends Analysis

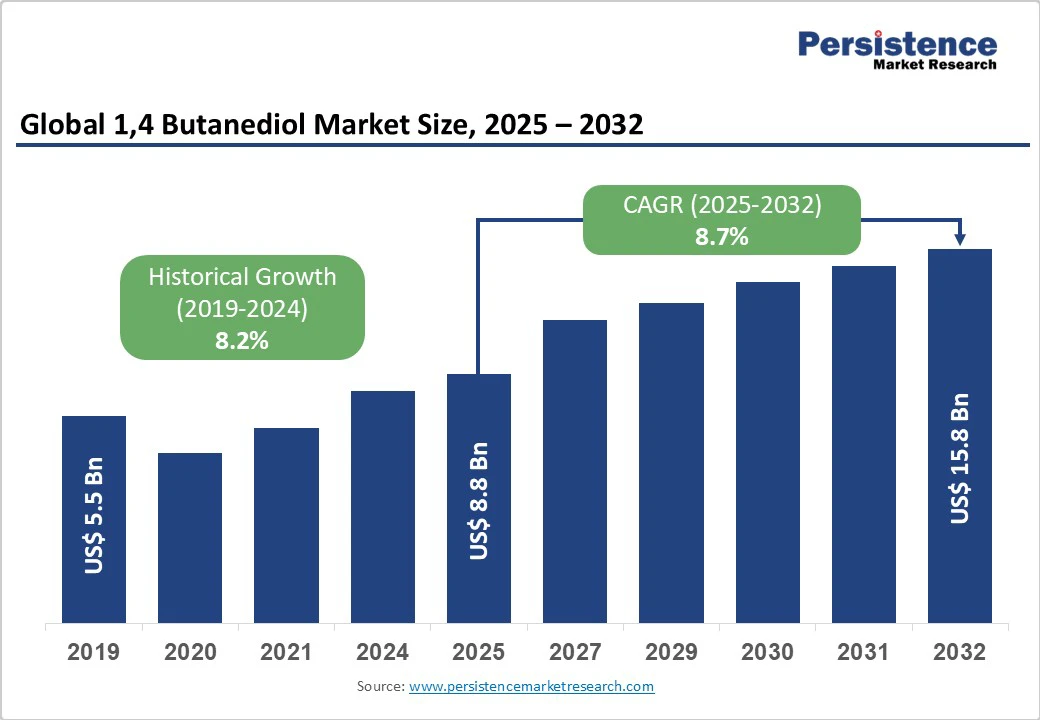

The global 1,4 butanediol market size is likely to be valued at US$ 8.8 Bn in 2025 and is expected to reach US$ 15.8 Bn by 2032, growing at a CAGR of 8.7% during the forecast period from 2025 to 2032. The 1,4 butanediol market has witnessed steady growth, driven by increasing demand for high-performance chemicals across industries such as automotive, textiles, and healthcare, coupled with advancements in production technologies.

Key Industry Highlights:

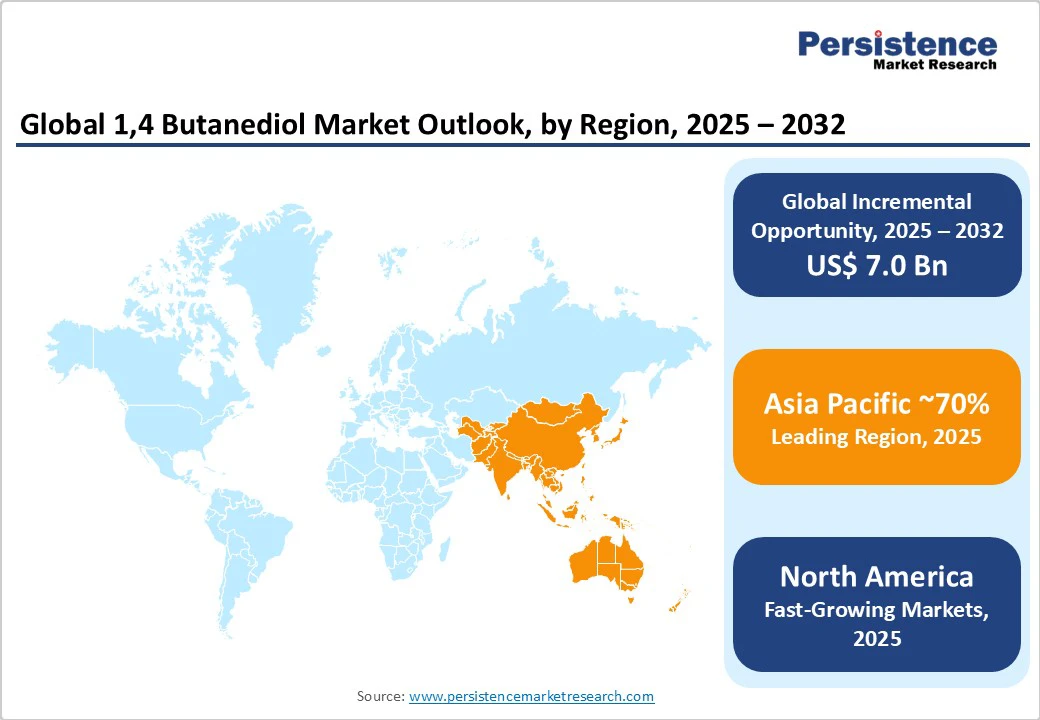

- Leading Region: Asia Pacific accounts for a 70% share in 2025, driven by robust industrial growth, large-scale manufacturing hubs in China and India, and increasing demand for BDO derivatives in automotive and textile sectors.

- Fastest-growing Region: North America, fueled by advancements in bio-fermentation technologies, increasing investments in sustainable chemical production, and growing applications in healthcare and electronics.

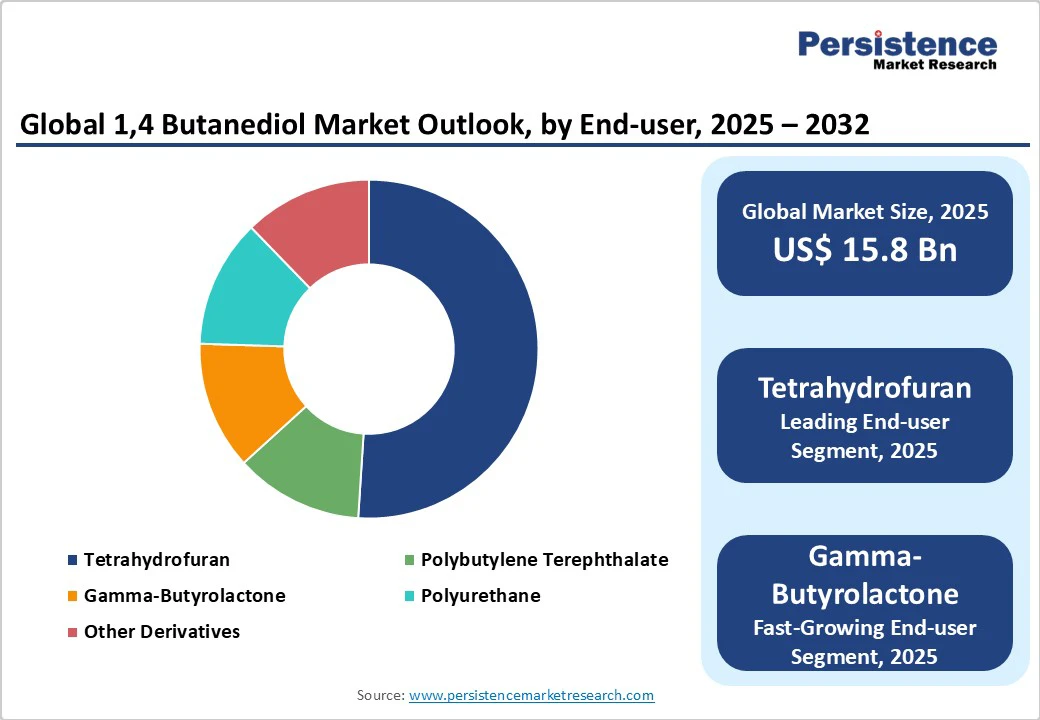

- Dominant Derivative: Tetrahydrofuran (THF), commanding nearly 50% market share, due to its widespread use in producing spandex fibers and as a solvent in pharmaceutical applications.

- Leading End-use: Automotive, accounting for over 40% of market revenue, driven by the need for high-performance polyurethanes in vehicle manufacturing.

| Key Insights | Details |

|---|---|

|

1,4 Butanediol Market Size (2025E) |

US$ 8.8 Bn |

|

Market Value Forecast (2032F) |

US$ 15.8 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

8.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

8.2% |

Market Dynamics

Driver - Increasing Demand for Polyurethane in Automotive and Construction Industries

The growth of the 1,4-Butanediol (BDO) market is driven by the increasing demand for polyurethane in the automotive and construction industries. Polyurethane, derived from BDO and its intermediates, is widely utilized due to its versatility, durability, and lightweight properties. In the automotive sector, the growing emphasis on vehicle weight reduction to improve fuel efficiency and comply with stringent emission standards has significantly boosted the use of polyurethane foams, coatings, adhesives, and sealants. These materials not only enhance vehicle performance but also contribute to passenger comfort and safety through superior insulation and cushioning. In the construction industry, polyurethane has become a preferred material owing to its excellent thermal insulation, energy efficiency, and structural benefits.

Rapid urbanization, infrastructure development, and increasing demand for sustainable building materials are fueling polyurethane adoption in insulation panels, sealants, flooring, and protective coatings. Additionally, government initiatives promoting energy-efficient construction further support market growth. The expanding role of polyurethane across these critical industries directly translates into higher consumption of BDO, as it serves as a crucial raw material in polyurethane production. This rising demand strongly underpins the sustained growth trajectory of the global BDO market.

Restraint - High Production Costs and Regulatory Challenges

The high costs associated with the production and regulatory compliance of 1,4 Butanediol disturb market growth. The conventional production of BDO often relies on petrochemical-based feedstocks and energy-intensive processes, which significantly raise manufacturing expenses. Fluctuating crude oil prices further cut cost volatility, making it difficult for manufacturers to maintain stable profit margins. Even with advancements in bio-based production methods, the initial investment requirements for technology development, infrastructure, and scaling remain substantial, limiting widespread adoption.

High costs and regulatory pressures present another critical challenge. Many governments have introduced strict environmental regulations aimed at reducing carbon emissions and promoting sustainable chemical manufacturing. Producers of BDO must comply with rigorous standards related to emissions, waste management, and product safety. Meeting these requirements often necessitates additional investments in cleaner technologies, advanced monitoring systems, and compliance procedures, thereby further increasing operational costs. These combined factors create barriers for new entrants and pose profitability challenges for existing players. While the demand for BDO continues to grow across industries, the financial and regulatory burdens may hinder market expansion, especially in regions with highly stringent environmental policies.

Opportunity - Advancements in Bio-based BDO Production

Advancements in bio-fermentation routes for 1,4 Butanediol production present a significant growth opportunity. Traditional BDO manufacturing relies heavily on petrochemical feedstocks, which are not only subject to price fluctuations but also contribute significantly to carbon emissions. In response, the development of bio-based BDO, produced from renewable resources such as sugars and biomass through advanced fermentation technologies, has emerged as a sustainable alternative.

Bio-based BDO offers several benefits, including reduced environmental footprint, lower greenhouse gas emissions, and alignment with global sustainability goals. Recent technological progress in metabolic engineering, enzyme optimization, and large-scale fermentation has improved production yields and efficiency, making bio-based BDO increasingly competitive with conventional processes. Several companies and research institutions are investing heavily in scaling up commercial production facilities to meet the growing demand from industries such as automotive, textiles, packaging, and electronics. Moreover, supportive government policies promoting bio-based chemicals, along with rising consumer preference for eco-friendly products, are accelerating market adoption. As industries transition toward circular and sustainable practices, advancements in bio-based BDO production present a significant growth avenue, positioning it as a critical driver of long-term market transformation.

Category-wise Analysis

Production Process Insights

The reppe process dominates the 1,4 Butanediol market and is expected to register approximately 55% share in 2025. Its dominance stems from established infrastructure, high yield efficiency, and widespread adoption by major players such as BASF SE and Dairen Chemical Corporation. The process’s ability to produce high-purity BDO for applications in polyurethane and THF makes it a preferred choice for large-scale manufacturers. Its scalability and compatibility with existing production facilities further drive its adoption in regions such as the Asia Pacific and North America.

The bio-fermentation route is the fastest-growing segment, driven by increasing demand for sustainable chemical production. This process leverages renewable feedstocks and advanced biotechnologies, offering a lower environmental impact compared to traditional methods. Companies such as Genomatica and Mitsubishi Chemical are investing heavily in bio-fermentation, with North America leading the adoption due to strong R&D capabilities and government support for green technologies. The segment is expected to witness significant growth, particularly in eco-conscious markets such as Europe and North America.

Derivative Insights

Tetrahydrofuran (THF) leads the derivative segment, holding a 50% share in 2025. THF’s dominance is driven by its critical role in producing spandex fibers for textiles and as a solvent in pharmaceutical manufacturing. The global textile industry, particularly in the Asia Pacific, relies heavily on THF for producing elastic fibers, with China accounting for over 60% of global spandex production in 2024. THF’s versatility and high demand in healthcare applications further strengthens its market position.

The polyurethane is the fastest-growing segment fueled by increasing use in automotive, construction, and electronics industries. Polyurethane’s lightweight and durable properties are ideal for automotive components and insulation materials. The rise in electric vehicle production and sustainable construction practices is accelerating the adoption of polyurethane, driving demand for BDO as a key raw material.

End-use Insights

The automotive sector holds the largest market share, accounting for approximately 40% of revenue in 2025. The sector’s dominance is driven by the widespread use of BDO-derived polyurethane in vehicle manufacturing, including seats, interiors, and coatings. Companies such as BASF and LyondellBasell provide tailored BDO solutions for automotive applications, supporting lightweight and durable material needs. The segment benefits from strong demand in the Asia Pacific, where automotive production is booming.

The healthcare and pharmaceuticals segment is the fastest-growing, driven by the increasing use of THF as a solvent in drug manufacturing and BDO in medical-grade polymers. The global pharmaceutical market is driving demand for high-purity BDO, particularly in North America and Europe. The rise in biocompatible materials for medical devices and drug delivery systems is further accelerating adoption in this segment.

Regional Insights

North America 1,4 Butanediol Market Trends

North America is emerging as one of the most significant regions in the 1,4-Butanediol (BDO) market, supported by strong technological innovation and a shift toward sustainable chemical production. The region is witnessing notable advancements in bio-fermentation technologies, which enable the production of BDO from renewable resources. This not only reduces dependency on petrochemical feedstocks but also aligns with stringent environmental regulations and the growing demand for greener alternatives across industries.

Rising investments from leading chemical companies and research institutions are further accelerating the adoption of sustainable manufacturing practices. Many U.S.-based and Canadian firms are focusing on scaling bio-based BDO production to meet increasing demand across diverse sectors. One of the key growth drivers in the region is the expanding application of BDO in healthcare, particularly in the production of pharmaceuticals, medical devices, and specialty polymers used in drug delivery systems. The growing electronics industry is fueling demand for BDO derivatives such as polybutylene terephthalate (PBT), which is widely used in connectors, switches, and casings due to its durability and resistance. Together, these factors position North America as a dynamic market with strong growth prospects in the global BDO landscape.

Europe 1,4 Butanediol Market Trends

Europe is a significant player in the 1,4 Butanediol market, supported by strong regulatory frameworks and investments in sustainable chemical production. Leading countries such as Germany, France, and the Netherlands drive market growth, with Germany hosting major players such as BASF SE and Evonik Industries. The region’s focus on sustainability, driven by the EU’s Green Deal, has accelerated the adoption of bio-based BDO, particularly in textiles and automotive applications.

Germany’s chemical industry, valued in 2024, is a key consumer of BDO for polyurethane and THF production. France and the Netherlands are also investing in bio-fermentation technologies, with companies such as Sipchem expanding their presence. The growing demand for eco-friendly materials in construction and healthcare, coupled with stringent environmental regulations, ensures steady market growth in Europe.

Asia Pacific 1,4 Butanediol Market Trends

Asia Pacific is projected to dominate the global 1,4 butanediol market, capturing nearly 70% of the overall share. This remarkable dominance is largely attributed to the region’s robust industrial expansion and the presence of large-scale manufacturing hubs, particularly in China and India. Both countries have emerged as global production centers, offering cost-effective raw materials, skilled labor, and favorable government policies that encourage investment in chemical and industrial manufacturing.

The demand for BDO and its derivatives, such as tetrahydrofuran (THF), polybutylene terephthalate (PBT), and gamma-butyrolactone (GBL), is rapidly increasing due to their extensive applications in the automotive and textile sectors. For the automotive industry, the rising need for lightweight materials, coatings, and polymers is boosting BDO consumption, while in the textile sector, BDO derivatives are widely used for producing spandex fibers and other performance-enhancing fabrics.

Asia Pacific benefits from its expanding infrastructure, growing domestic consumption, and increasing exports to global markets. Strong investments in research and development, along with government support for sustainable production technologies, further strengthen the region’s leadership position. As a result, Asia Pacific is expected to remain the primary growth engine of the global BDO market throughout the forecast period.

Competitive Landscape

The global 1,4 Butanediol market is highly competitive, featuring a mix of global leaders and regional players. In North America and Europe, companies such as BASF SE, LyondellBasell Industries N.V., Mitsubishi Chemical Corporation, and Dairen Chemical Corporation dominate through large-scale production, advanced R&D capabilities, and extensive distribution networks. In the Asia Pacific region, rapid industrial growth, rising demand for polymers, and increasing adoption of bio-based BDO attract investments from international players as well as regional producers such as Xinjiang Markor and Shanxi Sanwei.

Market competition is driven by innovations in bio-based and high-purity BDO, along with the development of derivatives such as THF, PBT, GBL, and PU. Companies are increasingly pursuing sustainability initiatives, strategic collaborations such as BASF’s partnership with Genomatica for bio-BDO expansion, and acquisitions to strengthen regional footprints, including Evonik’s expansion in Asia. Digital supply chain optimization, modular production facilities, and process efficiency improvements further enhance competitiveness. While global giants occupy the top tier, numerous niche and regional players continue to serve cost-sensitive and specialized markets, maintaining a dynamic and fragmented industry landscape.

Key Developments:

- In September 2023, BASF announced a long-term supply agreement with Qore LLC (a joint venture of Cargill and HELM AG) to access their bio-based 1,4-BDO, QIRA, produced via fermentation of plant-based sugars. This agreement includes the expansion of BASF’s BDO derivative portfolio with bio-based variants.

- In December 2023, BASF announced that from early 2024, it will start offering its 1,4-BDO and PolyTHF with significantly lower product carbon footprints, compared to the global average for fossil-based counterparts.

Companies Covered in 1,4 Butanediol Market

- BASF SE

- Dairen Chemical Corporation

- LyondellBasell Industries N.V.

- Mitsubishi Chemical Corporation

- Genomatica, Inc.

- Ashland

- Evonik Industries AG

- Sinopec

- Sipchem

- Xinjiang Markor

- Xinjiang Tianye Group

- Inner Mongolia Dongyuan Technology

- Nan Ya Plastics

- Shanxi Sanwei

- Others

Frequently Asked Questions

The global 1,4 Butanediol market is estimated at US$ 8.8 Bn in 2025.

The increasing demand for polyurethane in the automotive and construction industries is a key driver.

The 1,4 Butanediol market is poised to witness a CAGR of 8.7% from 2025 to 2032.

Advancements in bio-based BDO production are a key opportunity.

BASF SE, Dairen Chemical Corporation, LyondellBasell Industries N.V., Mitsubishi Chemical Corporation, and Genomatica, Inc. are key players.