ID: PMRREP4148| 200 Pages | 29 Oct 2025 | Format: PDF, Excel, PPT* | Healthcare

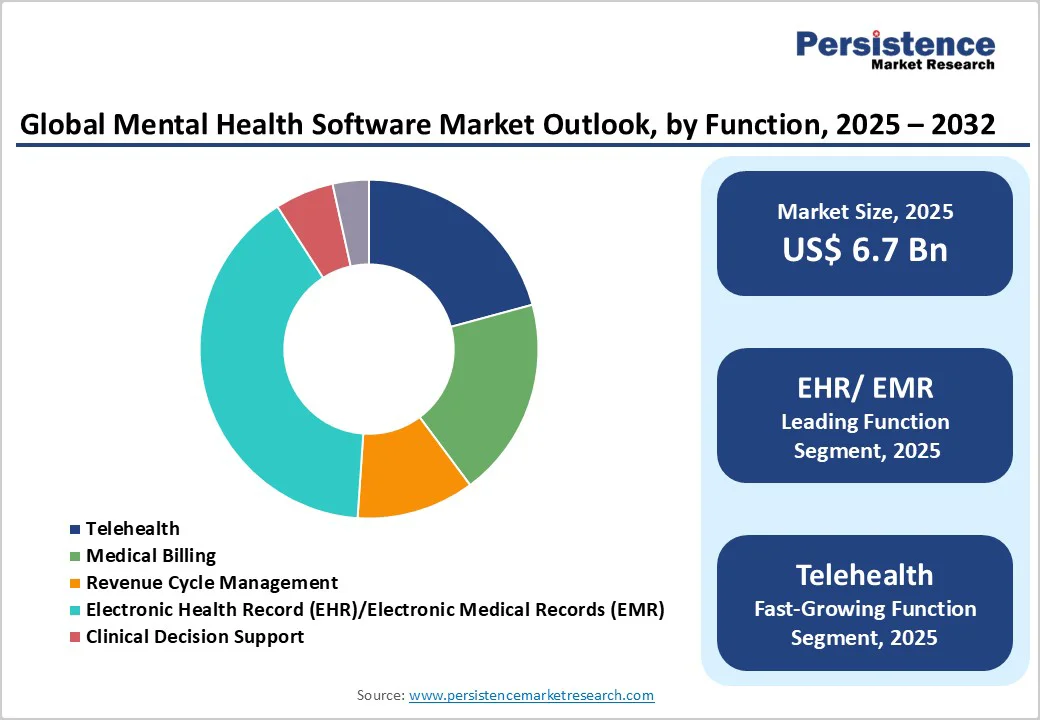

The global mental health software market size is likely to value US$ 6.7 billion in 2025 and is projected to reach US$ 19.4 billion by 2032, growing at a CAGR of 16.4% between 2025 and 2032. Mental health software is a digital solution, available as applications, websites, or both, designed to help clinics and healthcare professionals manage and monitor patient care efficiently. These platforms enable tracking of patient progress, mood fluctuations, and provide emergency support, while streamlining treatment workflows.

| Key Insights | Details |

|---|---|

|

Global Mental Health Software Market Size (2025E) |

US$ 6.7 billion |

|

Market Value Forecast (2032F) |

US$ 19.4 billion |

|

Projected Growth (CAGR 2025 to 2032) |

16.4% |

|

Historical Market Growth (CAGR 2019 to 2024) |

15.9% |

The global mental health software market is being propelled by rising awareness of mental well-being, increasing digital adoption, and the growing burden of mental health disorders worldwide. According to the World Health Organization (WHO, 2025), nearly 1 billion people globally suffer from mental health disorders such as anxiety, depression, addiction, and stress. These conditions represent the second largest cause of long-term disability and impose an estimated US$ 1 trillion annual economic loss, projected to surge to US$ 6 trillion by 2030, surpassing costs linked to cancer, diabetes, and respiratory diseases.

Additionally, the COVID-19 pandemic further accelerated the shift toward digital mental health solutions. As traditional care access was disrupted, tele-mental health and virtual consultations became mainstream by late 2020, with 36% of global mental health and substance-use consultations being conducted virtually (National Institute of Health-NIH, 2020). This transformation enhanced accessibility for patients in rural or underserved regions while normalizing remote therapy. Integrated software platforms offering EHRs, online scheduling, billing, and clinical data management further enable providers to personalize treatment and streamline workflows efficiently.

The global mental health software market faces several restraining factors slowing its expansion. One primary challenge is the high cost of installation and maintenance of digital mental health platforms, which can be prohibitive for small clinics and emerging healthcare providers. Only a small proportion of practitioners possess the necessary expertise to operate and manage these systems efficiently, creating an additional barrier.

The shortage of qualified mental health professionals further compounds the problem. According to a 2022 AAMC (Association of American Medical Colleges) article, the global mental health system is projected to face a deficit of 14,280 to 31,109 psychiatrists by 2025, with over 150 million people living in areas designated as having insufficient mental healthcare coverage.

Another limiting factor is the cost of software development. Entry-level mental health solutions typically range from $12,000 to $30,000, while platforms with advanced features such as AI-guided therapy, telehealth integration, and secure data storage can cost $32,000 to over $250,000, depending on complexity, platform, and development location. Ongoing expenses for maintenance, regulatory compliance, and periodic upgrades further increase the financial burden.

The global mental health software market presents substantial opportunities driven by technological innovation, AI integration, and the growing demand for scalable, accessible behavioral and mental healthcare solutions. Digital platforms enable real-time monitoring of patient health, streamlining administrative tasks, and improving communication between patients and providers, thereby enhancing the overall efficiency of mental health services.

Several landmark implementations illustrate this potential such as in July 2025, Qualifacts launched iQ Assistant across its EHR platforms, delivering AI-driven clinical support in 120+ languages and easing administrative burdens. Similarly, in June 2025, AI developer Nabla raised $70 million to scale ambient scribe technology for clinical notetaking and billing, reflecting growing investor confidence.

Studies, such as the August 2024 Journal of Clinical Medicine publication, confirm that AI-enabled care models like Sword Health’s AI Care help expand clinician capacity, improve patient engagement, and maintain outcomes. By bridging the gap between demand and available mental health resources, AI and advanced software solutions offer a transformative opportunity to increase accessibility, efficiency, and quality of care globally.

The subscription-based (cloud) deployment segment is projected to dominate the mental health software market in 2025, capturing a 74.8% share. This preference is driven by the flexibility, scalability, and cost-effectiveness offered by cloud-based solutions, allowing healthcare providers to access software anytime, anywhere, without investing heavily in on-premise infrastructure.

Subscription models also simplify updates, maintenance, and security management, while supporting remote and hybrid care delivery. In contrast, on-premise solutions require higher upfront investment and dedicated IT resources, making them less attractive for small and medium-sized practices seeking rapid adoption and minimal operational burden.

The mental health software market is segmented by desktops/laptops and tablets/smartphones, with tablets and smartphones projected to hold 68.1% of the global market share in 2025. Their dominance is supported by widespread internet penetration, high adoption rates, and the increasing number of mobile device users, making mental health solutions more accessible anytime, anywhere.

The convenience of on-the-go access, combined with intuitive mobile interfaces, enhances patient engagement and adherence to therapy. These factors collectively ensure that tablets and smartphones remain the preferred mode of access, driving sustained growth in the mental health software market over the next decade.

EHR/EMR are expected to hold the dominant share of the global mental health software market in 2025, enabling providers to securely manage patient records, track treatment progress, and streamline billing and scheduling. Custom mental health EHRs offer tailored treatment planning, in-app telehealth sessions, and advanced convenience features.

Integration with revenue cycle management (RCM), practice management, customer relationship management (CRM), and health information exchange (HIE) software enhances operational efficiency, improves patient engagement, and ensures seamless coordination with other healthcare providers. Patient portals and telehealth apps further facilitate easy access to records, treatment plans, and mental health recommendations, reinforcing the central role of EHR/EMR in modern mental health care delivery.

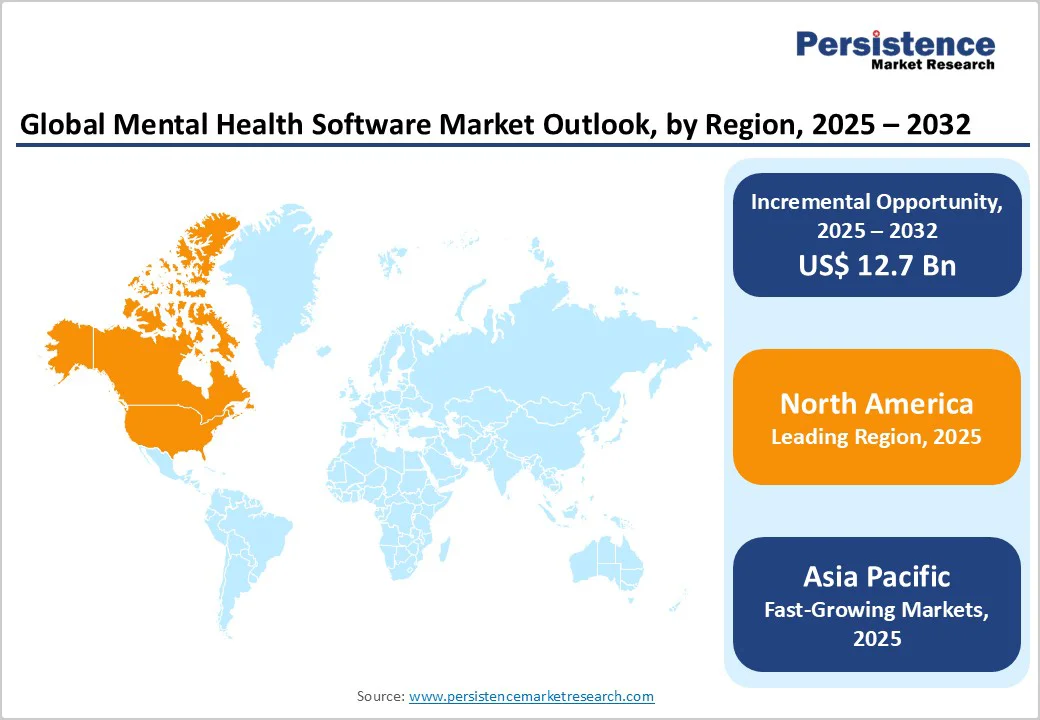

The North American market is expanding rapidly, projected to capture nearly 44.7% of the global share by 2025. The U.S. remains the primary growth driver, supported by advanced healthcare infrastructure, growing insurer participation, and widespread adoption of digital and AI-based solutions.

Increasing smartphone penetration and rising acceptance of mobile mental health apps are further transforming how patients and providers manage behavioral/mental conditions. AI-driven systems, in particular, are revolutionizing care delivery by enabling early intervention, continuous monitoring, and relapse prevention support within both community and hospital settings.

Reflecting this trend, several key initiatives highlight the region’s momentum. In October 2024, MassMutual became the first U.S. insurer to offer policyowners free access to Wysa Assure, an AI-guided mental health app developed by Wysa and Swiss Re. This partnership exemplifies the growing integration of AI into mainstream wellness programs, providing users with 24/7 access to clinically validated chat support and over 150 evidence-based tools for managing stress, anxiety, and sleep.

Similarly, In May 2025, Qualifacts partnered with Greenspace Health to integrate Measurement-Based Care (MBC) technology directly into its Credible and CareLogic EHR platforms. The collaboration streamlines clinical workflows, supports accreditation standards (Commission on Accreditation of Rehabilitation Facilities - CARF and Joint Commission), and strengthens data-driven decision-making illustrating the region’s commitment to outcome-based, technology-enabled mental healthcare delivery.

Europe remains a pivotal market for mental health software, projected to capture 24.2% of the global market share by 2025, driven by government-backed initiatives, digital health integration, and increasing public awareness.

Rising mental health concerns highlighted by the June 2023 Eurobarometer survey, where 46% of Europeans reported experiencing emotional or psychosocial distress have accelerated the adoption of technology-driven solutions aimed at improving care coordination, patient participation, and overall healthcare efficiency.

Complementing these findings, a global study co-led by The University of Queensland and Harvard Medical School (2001–2022) revealed that one in two people worldwide is expected to develop a mental health disorder by age 75, emphasizing the scale and urgency of mental health challenges within Europe and beyond.

To strengthen mental health infrastructure, the European Commission launched several landmark initiatives. The EU-PROMENS project (January 2024), funded with €9 million under EU4Health, provides multidisciplinary training and exchange programs for health professionals, while an additional €31.2 million supports displaced Ukrainians through trauma and psychological care in partnership with the International Federation of Red Cross.

Asia Pacific is expanding rapidly, projected to grow at a positive CAGR in the forecast period, driven by government-backed mental health action plans, data-driven initiatives, and regional collaborations. The region’s momentum is reinforced by the Mental Health Innovation Network (MHIN Asia), which fosters collaboration among researchers, policymakers, educators, and advocates to advance evidence-based practices. MHIN Asia emphasizes knowledge synthesis, evidence dissemination, and the translation of regional insights into practical policies, thereby enhancing visibility and engagement across Asian countries.

In May 2024, the WHO South-East Asia Region reaffirmed its commitment to community-based mental healthcare through the Paro Declaration and the Regional Mental Health Action Plan 2023–2030, aimed at expanding integrated, people-centered care.

Together with the Regional Roadmap for Results and Resilience (2024–2029), these initiatives underscore Asia Pacific’s growing emphasis on technology-enabled, community-based, and data-driven solutions to bridge mental health care gaps and strengthen regional resilience.

The global mental health software landscape witnessed rapid innovation and expansion, with new digital platforms, tele-mental health services, and collaborative programs enhancing accessibility, early intervention, operational efficiency, and integrated care delivery across communities and healthcare settings globally.

The global market is projected to be valued at US$ 6.7 billion in 2025.

Rising awareness, AI integration, and digital adoption drive global mental health software growth.

The global mental health software market is poised to witness a CAGR of 16.4% between 2025 and 2032.

AI-powered solutions and scalable digital platforms create key opportunities in mental health care delivery.

Major players in the global are Qualifacts, NXGN Management, LLC, Wysa Ltd, Greenspace Mental Health Ltd, Woebot Health, Lyra Health, Inc. and others.

| Report Attribute | Details |

|---|---|

|

Historical Data/Actuals |

2019 - 2024 |

|

Forecast Period |

2025 - 2032 |

|

Market Analysis |

Value: US$ Mn |

|

Geographical Coverage |

|

|

Segmental Coverage |

|

|

Competitive Analysis |

|

|

Report Highlights |

|

By Deployment Mode

By Mode of Access

By Function

By End-user

By Region

Delivery Timelines

For more information on this report and its delivery timelines please get in touch with our sales team.

About Author