ID: PMRREP8539| 210 Pages | 11 Dec 2025 | Format: PDF, Excel, PPT* | Chemicals and Materials

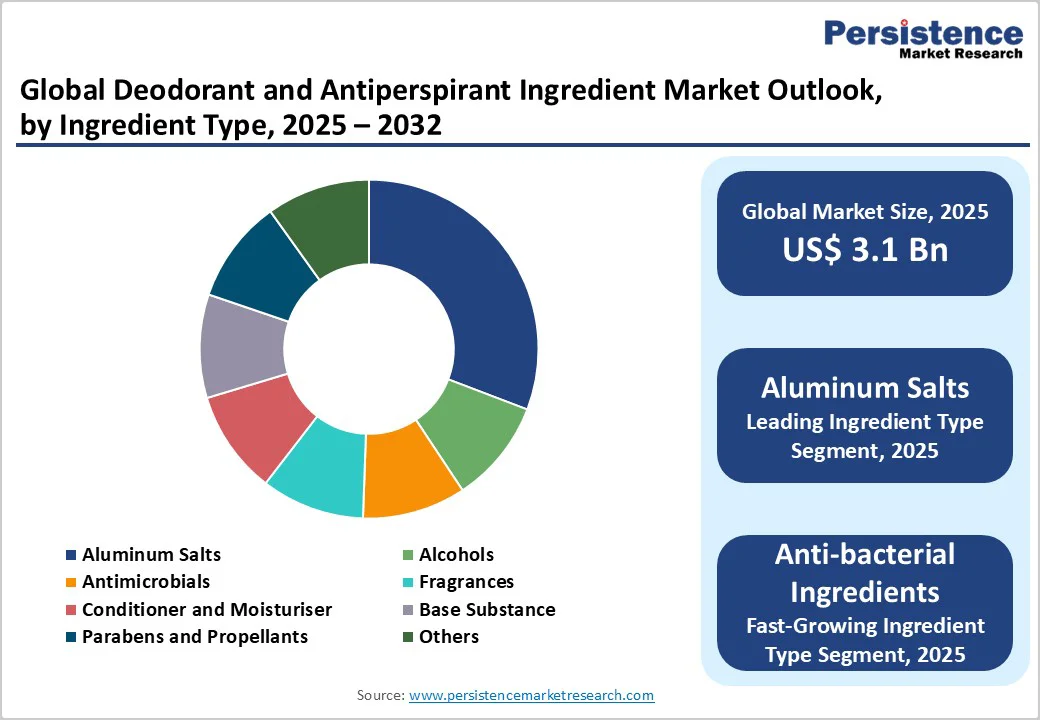

The global deodorant and antiperspirant ingredient market size is valued at US$3.1 billion in 2025 and projected to reach US$4.4 billion by 2032, growing at a CAGR of 5.1% between 2025 and 2032.

Rising consumer awareness about personal hygiene and grooming standards is driving unprecedented demand for advanced deodorant and antiperspirant formulations globally. Increasing urbanization, coupled with higher disposable incomes, is compelling consumers to invest in premium personal care products that offer enhanced protection and sophisticated fragrance profiles. The growing emphasis on professional appearance in corporate environments and expanding participation in fitness activities further amplifies the need for long-lasting, effective odor control solutions.

| Key Insights | Details |

|---|---|

|

Deodorant and Antiperspirant Ingredient Market Size (2025E) |

US$3.1 Billion |

|

Market Value Forecast (2032F) |

US$4.4 Billion |

|

Projected Growth CAGR(2025-2032) |

5.1% |

|

Historical Market Growth (2019-2024) |

4.3% |

The unprecedented surge in personal hygiene awareness, particularly accelerated by global health crises, has fundamentally transformed consumer attitudes toward daily grooming essentials. Urban populations across emerging markets are increasingly prioritizing professional appearance and social confidence, driving demand for sophisticated deodorant formulations. WHO initiatives promoting hygiene practices and government campaigns emphasizing cleanliness have significantly elevated awareness levels globally.

This heightened consciousness extends beyond basic odor control to encompass skin health, long-lasting protection, and premium sensory experiences. Urbanization rates reaching 68% by 2030 according to World Bank projections are creating larger consumer bases with higher spending power for personal care products. The expanding middle-class demographics in countries like China, India, and Indonesia are adopting Western-style grooming routines, substantially increasing market penetration rates for advanced deodorant ingredients.

Consumer preferences are shifting dramatically toward aluminum-free, natural, and organic deodorant ingredients due to growing health and environmental consciousness. The organic deodorant market, reaching US$160.9 million in 2025 with a projected 14.8% CAGR, demonstrates the accelerating transition toward plant-based formulations. The aluminum-free deodorant market is also anticipated to register a 10% CAGR between 2025 and 2032, reflecting consumers' concerns about potential health risks associated with traditional aluminum-based antiperspirants.

Over 65% of consumers are switching to aluminum-free formulations due to skin sensitivity and long-term health concerns. This trend is driving innovation in natural antimicrobial agents, essential oils, and botanical extracts as effective alternatives to synthetic chemicals. Brands are incorporating ingredients like tea tree oil, witch hazel, baking soda, and arrowroot to deliver effective odor control while meeting clean beauty standards.

Stringent regulatory frameworks, particularly EU REACH compliance, are imposing increasingly complex restrictions on chemical ingredients used in deodorant formulations. Recent amendments to the REACH Regulation through Regulation (EU) 2024/1328 have introduced restrictions on octamethylcyclotetrasiloxane (D4), decamethylcyclopentasiloxane (D5), and dodecamethylcyclohexasiloxane (D6) in cosmetic products, limiting concentrations to 0.1% by weight.

These substances, commonly used in deodorants for their silicone properties, face phase-out deadlines by June 2027. The European Chemicals Agency (ECHA) enforcement campaigns have identified over 6% of products containing banned substances, forcing reformulations and supply chain disruptions. Additionally, expanding fragrance allergen disclosure requirements mandate individual labeling of 26 specific allergens when concentrations exceed 0.001% in leave-on products.

The deodorant ingredients market faces significant cost pressures from volatile pricing of key raw materials, particularly natural and organic components. Premium ingredients like essential oils, plant extracts, and sustainable packaging materials command substantially higher prices than conventional synthetic alternatives, creating affordability barriers in price-sensitive markets. Supply chain disruptions affecting imported ingredients and packaging materials have increased production costs and delayed new product launches.

Raw material price volatility remains a key challenge for scalability and affordability, particularly affecting smaller manufacturers and emerging market penetration. This pricing dynamic is especially pronounced in Asia Pacific and Latin America, where cost-conscious consumers prioritize value propositions over premium formulations.

The antibacterial deodorant segments present significant growth opportunities for ingredient suppliers. Rising incidence of skin infections and growing awareness of the need for antimicrobial protection are driving demand for advanced deodorant formulations that incorporate natural and synthetic antibacterial agents. Innovation opportunities exist in developing tea tree oil, triclosan alternatives, silver nanoparticles, and probiotic-based antimicrobial systems that provide long-lasting protection while maintaining skin health. Clinical-strength antibacterial deodorant segments are experiencing notable growth as consumers seek prescription-level efficacy for persistent odor management. Companies can capitalize on this trend by developing antimicrobial formulations that leverage natural compounds while delivering superior performance compared to traditional chemical-based systems.

The global deodorant and antiperspirant ingredients market is poised to benefit from rapid expansion in roll-on and stick product formats, driven by evolving consumer preferences for convenient, skin-friendly, and sustainable solutions. The global deodorant roll-on market is projected to reach USD 12.22 billion by 2033, while the deodorant stick market is anticipated to reach USD 19.4 billion by 2033, reflecting growing demand for solid and liquid application systems. This surge is likely to create significant opportunities for ingredient manufacturers to develop multifunctional actives, emulsifiers, and carriers that enhance texture, absorption, and long-lasting odor protection. Innovation in aluminum-free, alcohol-free, and natural-derived formulations is further accelerating ingredient diversification, as brands seek to differentiate through performance, sensory appeal, and environmental sustainability across both product categories.

Aerosol formats dominate the deodorant and antiperspirant ingredient market with 68% market share in 2025, driven by consumer preference for convenience, quick-drying properties, and even application coverage. The popularity of aerosol deodorants stems from their ability to provide instant freshness and superior distribution of active ingredients across larger skin areas.

Aerosols accommodate diverse ingredient formulations including volatile alcohols, propellants, and fragrance compounds that create immediate sensory impact. The segment benefits from continuous innovation in propellant technologies, including eco-friendly alternatives that address environmental concerns while maintaining performance standards. However, environmental regulations and sustainability trends are driving the development of gas-free and eco-friendly propellant systems to maintain aerosol advantages while reducing environmental impact.

Aluminum salts maintain the leading position with 31% share in 2025, representing the cornerstone of antiperspirant efficacy through their sweat-blocking properties. Aluminum chlorohydrate, aluminum zirconium compounds, and related salts work by forming gel-like plugs within sweat ducts, temporarily preventing perspiration from reaching the skin surface.

Despite growing consumer concerns about potential health risks, aluminum-based antiperspirants remain widely used due to their unmatched effectiveness in high-performance and clinical-strength formulations. The segment is evolving to address consumer concerns through the development of low-residue, buffered aluminum complexes and mineral-blend hybrids that enhance skin compatibility while maintaining antiperspirant efficacy.

North America maintains its position as a mature but innovation-driven market, with the United States holding more than 75% share of the regional deodorant market in 2025. The region demonstrates sophisticated consumer preferences for premium formulations, natural ingredients, and advanced delivery systems. The North America aerosol market size is predicted to reach US$ 28.4 billion by 2032 from US$ 20.3 billion in 2025, registering a CAGR of around 4.9% during the forecast period, reflecting strong demand for convenient application formats, with rising consumption of deodorants and hair sprays serving as crucial market drivers.

Consumer awareness initiatives and FDA regulatory frameworks are compelling manufacturers to invest in safer, more transparent ingredient formulations while maintaining efficacy standards. The region leads in natural and organic deodorant adoption, with North America representing one of the largest markets for aluminum-free alternatives as consumers prioritize health-conscious formulations. E-commerce platforms and direct-to-consumer brands are reshaping distribution strategies, enabling specialty ingredient suppliers to reach niche segments seeking customized solutions.

Canada shows strong environmental consciousness with preferences for natural and organic products and increasing demand for sustainable packaging solutions. The regulatory landscape emphasizes ingredient transparency and environmental responsibility, creating opportunities for suppliers offering biodegradable and eco-friendly formulation components. Both countries demonstrate premium pricing acceptance for innovative ingredients that deliver superior performance, skin-friendly properties, and environmental benefits.

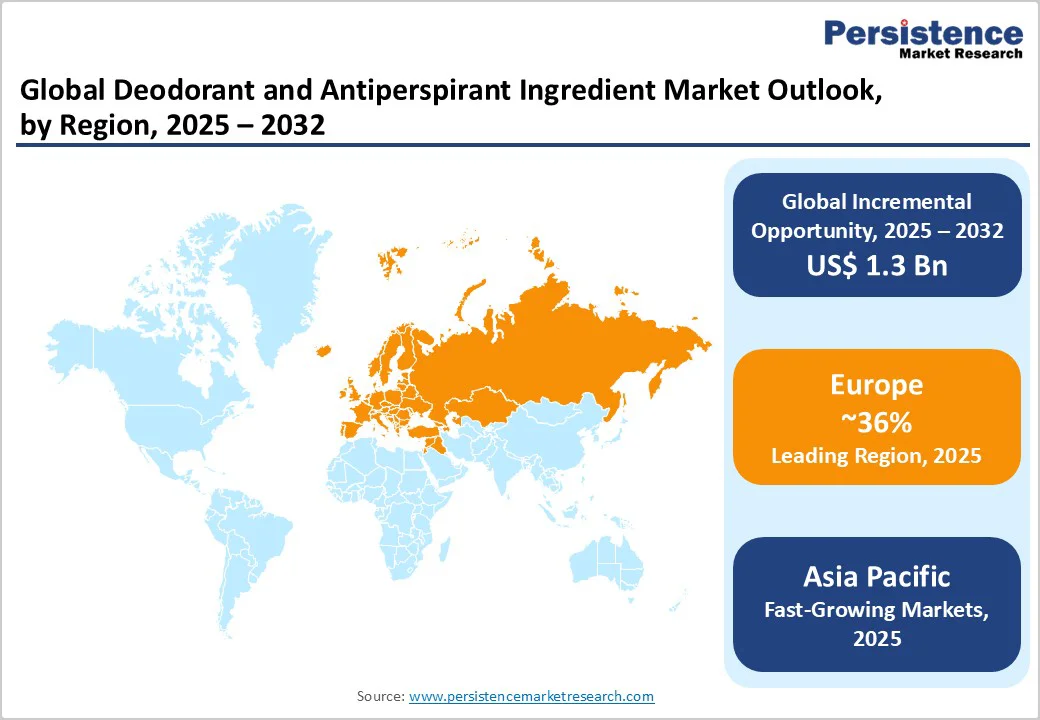

Europe commands 36% market share in 2025 as the leading regional market, characterized by stringent regulatory standards and sophisticated consumer preferences for quality formulations. Germany emerges as the largest individual market, driven by increasing demand for personal care products and growing female labor force participation creating sustained demand for professional grooming solutions. The region leads globally in regulatory harmonization through EU REACH compliance, creating standardized ingredient safety requirements across member states. France is expected to emerge as a key growth region due to scientific research advances in deodorant formulation and major market players introducing innovative formats.

European consumers demonstrate strong preferences for dermatologically tested products, skin-friendly formulations, and sustainable packaging solutions. The region's emphasis on natural ingredients and environmental responsibility is driving innovation in botanical extracts, organic compounds, and biodegradable packaging materials.

Asia Pacific represents the fastest-growing regional market with 6% CAGR from 2025-2032, driven by rapid urbanization, rising disposable incomes, and expanding middle-class demographics. China leads regional growth with its cosmetics and personal care sector anticipated to constitute about 70% of the Asia Pacific beauty market share until 2025. The market benefits from rising disposable income in the countries like India and southeast Asia. India shows exceptional growth potential with deodorant market projected to grow at CAGR of 7.5% between 2025 and 2032, driven by hot and humid climate conditions that create sustained demand for effective sweat control.

Regional preferences create opportunities for customized formulations. Japan and South Korea favor minimalist, fast-drying formulations while Southeast Asia demands strong odor protection for humid climates. The region demonstrates growing adoption of waterless beauty products and refillable deodorant systems to address sustainability concerns while meeting performance expectations. E-commerce platforms and digital marketing strategies are enabling ingredient suppliers to reach diverse demographic segments across urban and emerging rural markets, accelerating market penetration rates for premium formulations.

The global deodorant and antiperspirant ingredients market exhibits moderate consolidation with major chemical and personal care companies maintaining dominant positions while numerous regional suppliers and specialty ingredient manufacturers compete across diverse application segments. BASF leads the global market by leveraging its comprehensive portfolio of aluminum salts, mineral complexes, and encapsulation technologies alongside strategic partnerships with leading personal care brands.

The competitive landscape features Unilever, Procter & Gamble, and Henkel as key market players, collectively commanding significant market influence through their extensive distribution networks and brand portfolios. Market concentration allows established players to invest heavily in research and development, sustainable formulations, and advanced delivery systems while smaller specialty suppliers focus on natural ingredients, niche applications, and regional customization. Strategic expansion approaches include product diversification, mergers and acquisitions, and geographical market penetration to strengthen competitive positioning in high-growth segments and emerging markets.

The global Deodorant and Antiperspirant Ingredient Market is projected to reach US$ 4.4 billion by 2032, growing from US$ 3.1 billion in 2025 at a CAGR of 5.1%.

Key demand drivers include rising consumer awareness about personal hygiene, increasing urbanization, growing disposable incomes, and the expanding trend toward natural and organic formulations as consumers seek aluminum-free and environmentally sustainable deodorant ingredients.

Aerosol formats dominate the market with 68% share in 2025, driven by consumer preference for convenience, quick-drying properties, and superior distribution of active ingredients across application areas.

Europe maintains market leadership with 36% share in 2025, supported by stringent regulatory standards, sophisticated consumer preferences for quality formulations, and robust personal care industry infrastructure.

The natural and organic ingredient formulations segment presents significant growth opportunities, with the aluminum-free deodorant market expanding from USD 3.4 billion in 2025 to USD 6.2 billion by 2035, reflecting increasing consumer health consciousness and environmental awareness.

Major market players include BASF SE, Unilever Company, Procter & Gamble, Givaudan, Henkel AG & Company KGaA, Beiersdorf AG, LOreal Company, Symrise AG, Dow Chemical Company, and International Flavors & Fragrances Inc. (IFF), among others.

| Report Attribute | Details |

|---|---|

|

Historical Data/Actuals |

2019 - 2024 |

|

Forecast Period |

2025 - 2032 |

|

Market Analysis |

Value: US$ Mn/Bn, Volume: As Applicable |

|

Geographical Coverage |

|

|

Segmental Coverage |

|

|

Competitive Analysis |

|

|

Report Highlights |

|

By Product Type

By Ingredient Type

By Regions

Delivery Timelines

For more information on this report and its delivery timelines please get in touch with our sales team.

About Author