- Beauty & Personal Care

- Refillable Deodorants Market

Refillable Deodorants Market Size, Share, and Growth Forecast 2026 - 2033

Refillable Deodorants Market by Product Type (Stick Refillable Deodorants, Spray or Roll-On Refillable Deodorants), Distribution Channel (Online, Offline), Packaging (Metal, Glass, Plastic, Others), by Regional Analysis, 2026 - 2033

Refillable Deodorants Market Size and Trend Analysis

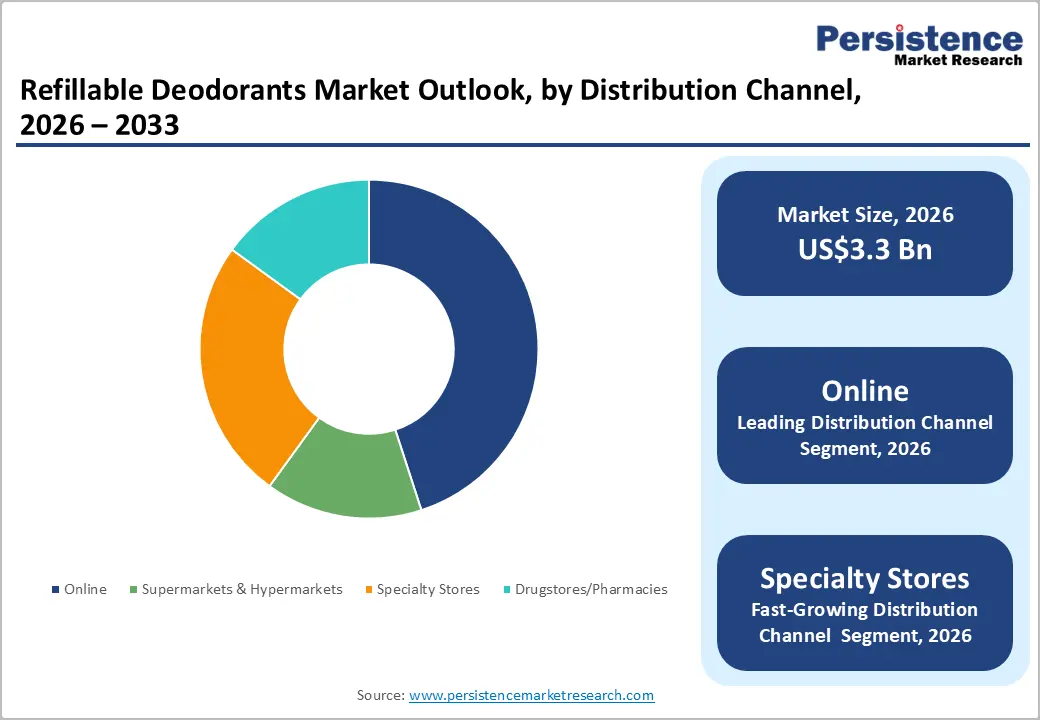

The global refillable deodorants market size is projected to be valued at US$ 3.3 billion in 2026 and reach approximately US$ 5.1 billion by 2033, registering a CAGR of 6.4% between 2026 and 2033.

Growth is shaped by the rise in environmental awareness, with more than 65% of consumers moving away from single-use plastics toward sustainable refill formats. In parallel, stricter regulations, including the EU Packaging and Packaging Waste Regulation (2030 recyclability target) and EU Cosmetics Regulation (2024/996), are accelerating innovation in safer, eco-friendly designs. Additionally, premiumization and increasing disposable incomes are encouraging consumers to adopt higher-quality, refillable personal care solutions.

Key Industry Highlights:

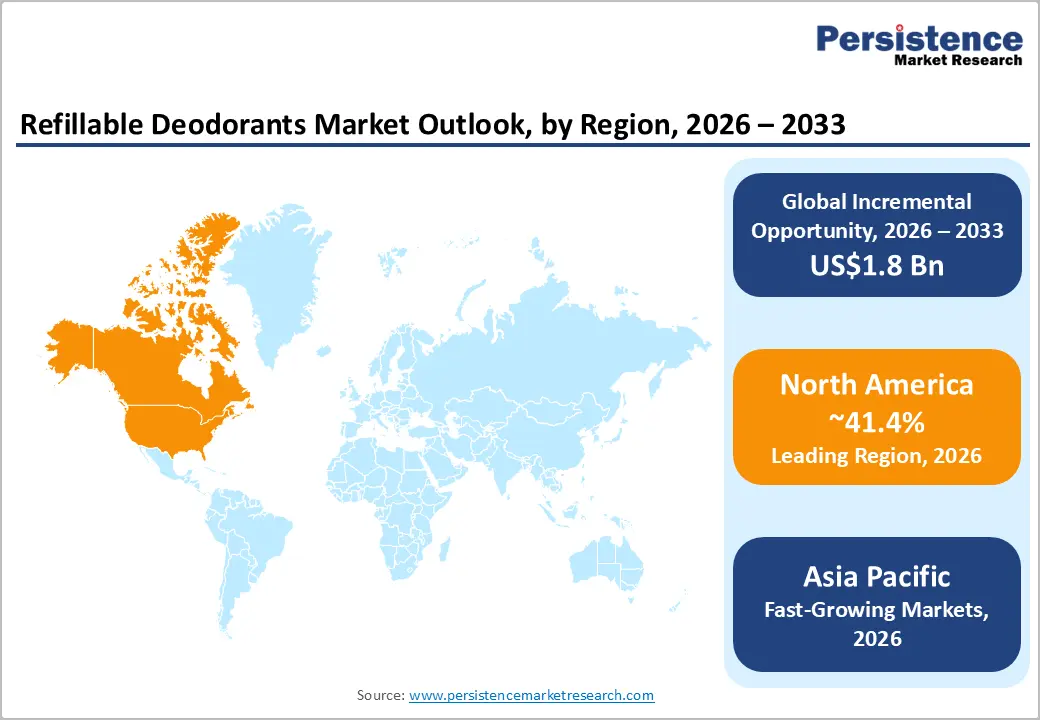

- Leading Region: North America commands refillable deodorants market leadership with 41.4% share, driven by sustainability preferences, mature e-commerce

- Fastest Growing Region: Asia Pacific is the fastest-growing region with 32.3%, fueled by rising disposable incomes, digital commerce penetration (60–70%), and Gen Z/Millennial sustainability awareness.

- Dominant Segment: Stick refillable deodorants lead the market at 62.1% share due to familiarity, superior refill mechanics, and premium positioning in developed markets.

- Fastest Growing Segment: Online distribution channels hold 45+% share through subscriptions, DTC scaling, and consumer preference for online purchasing.

- Key Market Opportunity: Subscription-based refill models drive recurring revenue, personalization, and sustainability alignment, validated by high-value acquisitions and DTC brand scaling.

| Key Insights | Details |

|---|---|

|

Refillable Deodorants Market Size (2026E) |

US$ 3.3 Billion |

|

Market Value Forecast (2033F) |

US$ 5.1 Billion |

|

Projected Growth CAGR (2026-2033) |

6.4% |

|

Historical Market Growth (2020-2025) |

5.7% |

Market Dynamics

Drivers - Sustainability, Circular Packaging, and Plastic Waste Reduction as the Core Momentum Driver

Growing environmental awareness, pressure on brands to reduce plastic waste, and the normalization of circular packaging models are redefining how deodorants are designed and purchased. Consumers now expect durable cases that last, simple refills that generate minimal waste, and credible sustainability claims that feel authentic rather than marketing slogans. Retailers increasingly curate eco-focused assortments, reinforcing these expectations at shelf worldwide.

Regulatory momentum amplifies the shift, pushing companies to rethink materials, refill systems, and lifecycle impacts across portfolios. Leading manufacturers are investing in stainless-steel or aluminum housings, compostable or low-plastic refills, and return programs that keep packaging in circulation. Sustainability has moved from optional differentiator to baseline expectation, shaping product roadmaps, retail strategies, and long-term brand credibility across global markets and future growth.

Health Awareness, Ingredient Transparency, and the Shift Toward Cleaner, Skin-Friendly Formulations

Rising focus on personal wellness and ingredient transparency is transforming deodorant choices. Consumers read labels carefully, avoid confusing chemical lists, and gravitate toward formulas that feel gentle, simple, and trustworthy. This scrutiny has shifted expectations from merely masking odor to supporting skin health, minimizing irritation, and aligning with broader lifestyle preferences around safety and wellbeing. Dermatologist guidance and social conversation reinforce these behaviors.

In response, brands are developing cleaner, plant-inspired formulations using mild antimicrobials, natural fragrances, and fewer synthetic additives while maintaining reliable performance. Transparent sourcing stories, hypoallergenic testing, and minimalist ingredient panels help reassure cautious shoppers. Refillable formats extend this promise, pairing skin-friendly formulas with responsible packaging, and strengthening loyalty by aligning everyday hygiene routines with values of wellness, transparency, and conscious consumption.

Restraints - Premium Positioning, Higher Upfront Costs, and Consumer Price Sensitivity Limiting Broader Adoption

Refillable deodorants often rely on durable, sustainable housings and more complex dispensing systems, which raise development and production costs. This places many products in a premium price tier, creating a noticeable gap versus conventional single-use deodorants. While consumers value sustainability, many still evaluate purchases through a cost-first lens, especially in everyday hygiene categories where frequent replenishment is expected.

As a result, the willingness to “pay extra for eco-friendliness” does not always translate into consistent purchasing behavior. Budget-conscious shoppers may postpone switching or reserve refillable formats for occasional use. This tension is particularly visible in value-driven markets and among younger consumers with limited disposable income, slowing mass penetration and keeping refillable formats concentrated in urban, premium, and specialty retail environments.

Perceived Performance Trade-Offs and Skepticism Toward Natural, Aluminum-Free Formulations

A second restraint stems from consumer perceptions around performance. Many shoppers remain unsure whether natural or aluminum-free deodorants can deliver strong, long-lasting odor and moisture control comparable to familiar antiperspirant systems. When expectations involve strenuous activity, warm climates, or long wear times, doubts about staying power can create hesitation at the point of purchase.

Although new formulations increasingly incorporate advanced botanical antimicrobials, probiotics, and absorbent ingredients, the perception gap persists. Occasional experiences of shorter protection or transitional skin adjustments reinforce skepticism and slow repeat purchase rates. For performance-driven users including athletes, outdoor workers, and highly active consumers reliability still outweighs sustainability, creating a barrier that brands must address through clearer education, transparent testing claims, and continuous formulation improvements.

Opportunity - Subscription-Driven Refill Programs and Direct-to-Consumer Ecosystems as Scalable Growth Engines

Subscription and direct-to-consumer (DTC) refill programs are reshaping how deodorants are purchased, replenished, and experienced. Instead of occasional, irregular purchases through retail shelves, brands use automated refills, doorstep delivery, and personalized communication to build predictable relationships. This model reduces friction, embeds sustainability into daily routines, and normalizes refills as the default behavior rather than an optional alternative.

Category innovators have demonstrated that subscriptions deepen loyalty, strengthen brand communities, and generate reliable recurring revenue. Companies benefit from first-party data, enabling tailored scents, bundle options, and targeted education around usage and sustainability. Strategic acquisitions by major personal-care corporations further validate this channel’s potential, signaling accelerating investment in DTC logistics, digital engagement, and long-term retention strategies across refillable deodorant portfolios.

Asia Pacific Expansion, Urban Affluence, and Sustainability Adoption Among Emerging Consumers

Asia Pacific represents a compelling opportunity as rising urbanization, lifestyle upgrading, and exposure to global beauty trends reshape hygiene and grooming habits. A growing base of aspirational middle-income consumers is increasingly receptive to premium, wellness-aligned products that balance functionality with environmental responsibility. Early-stage penetration of refillable formats leaves substantial headroom for education-driven market development.

Brands that localize pricing, fragrances, packaging design, and cultural messaging can establish credibility before the category fully matures. Digital commerce, influencer-led discovery, and mobile-first shopping journeys enable direct access to young urban consumers, bypassing traditional retail constraints. Companies that pair affordability-minded refill innovations with strong sustainability storytelling are positioned to capture long-term loyalty as refillable deodorants transition from novelty to mainstream personal-care behavior across key Asia Pacific markets.

Category-wise Analysis

Product Type Insights

Stick refillable deodorants hold the leading position in the category, capturing about 62.1% market share. Their dominance is supported by consumer familiarity, solid-format convenience, and efficient refill mechanics that reduce waste and improve portability. Sticks also align well with premium, eco-friendly positioning because durable refill cartridges reduce packaging volume while preserving usability, shelf appeal, and long-standing trust across mature personal-care markets.

The fastest-growing opportunity sits within spray and roll-on refillable formats. These products appeal to consumers prioritizing quick application, lighter textures, and minimal residue. Younger shoppers, highly active lifestyles, and growing adoption in warmer regions support momentum. As brands refine refill mechanisms and enhance sensory performance, spray and roll-on formats are becoming credible alternatives, expanding the addressable base beyond traditional stick loyalists.

Distribution Channel Insights

Online distribution has emerged as the dominant channel for refillable deodorants, approaching 45%+ share as consumers increasingly prefer subscription convenience, comparison shopping, and direct brand access. E-commerce supports premium storytelling around sustainability, transparency, and ingredient safety, while automated replenishment reduces stockouts and minimizes reliance on physical retail networks, particularly in markets where specialty sustainable brands have limited shelf presence.

The fastest-growing channel opportunity lies in digitally enabled, brand-owned platforms and hybrid models linking online ordering with experiential engagement. Direct-to-consumer ecosystems enable personalization, sampling programs, loyalty rewards, and education-led selling strategies. These models help brands nurture long-term relationships, optimize margins, and integrate refills seamlessly into consumer routines - strengthening repeat purchase behavior and accelerating adoption of refillable formats over conventional single-use products.

Packaging Material Insights

Metal packaging, including stainless steel, aluminum, and tinplate leads the refillable deodorant segment, accounting for around 59.2% market share. Its durability, resistance to product degradation, premium aesthetics, and infinite recyclability make it the preferred option for sustainability-focused brands. Metal housings support precise refill mechanisms, withstand temperature fluctuations, and reinforce circular-economy positioning that resonates strongly with eco-conscious consumers.

The fastest-growing opportunity is emerging in biodegradable and next-generation refill systems using paper-based, plant-derived, or compostable materials. These formats appeal to consumers seeking low-waste packaging without the weight or cost of metal. Innovations in structural strength, moisture resistance, and user experience are expanding feasibility, allowing brands to experiment with lighter, more affordable refill solutions while maintaining strong environmental credibility.

Regional Insights

North America Refillable Deodorants Market Trends

North America remains the leading region in refillable deodorants, accounting for about 41.4% of global market share. Growth is driven by sustainability-conscious consumers, expanding subscription programs, and premium natural formulations. State-level extended producer responsibility (EPR) and single-use plastic reduction initiatives, especially in California and New York, are encouraging innovation in refillable packaging, ingredient reformulation, and environmentally responsible manufacturing practices.

The U.S. dominates regional demand, with e-commerce and mass retail channels facilitating broad adoption. Direct-to-consumer storytelling, high awareness of ingredient transparency, hypoallergenic claims, and recyclable packaging reinforce consumer trust. Retailers such as Target, Ulta, and Whole Foods help normalize refillable formats, while subscription models strengthen loyalty, making North America both a mature market and a hub for innovation in sustainable deodorant solutions.

Europe Refillable Deodorants Market Trends

Europe is the second-largest refillable deodorants market, supported by stringent sustainability regulations and highly eco-conscious consumers. Refillable formats benefit from the EU Packaging and Packaging Waste Regulation (PPWR) and evolving cosmetics regulations, which create strong investment confidence. Premium, aluminum-free, and natural deodorants drive consumer preference, while cultural sustainability awareness reinforces adoption across Western European markets.

The region is projected to grow at a CAGR of 7.2–7.5%, outpacing many mature markets. Germany leads adoption via drugstores and natural beauty retailers, while the UK, France, and Spain see growth driven by premiumization, subscription-based models, and online channels. Specialty retail supports curated sustainability offerings, helping brands position refillable deodorants as both aspirational and mainstream personal-care products.

Asia Pacific Refillable Deodorants Market Trends

Asia Pacific is the fastest-growing region, accounting for around 32.3% of global market share, with high long-term potential. Rising urbanization, expanding middle-class incomes, rapid digital commerce growth, and increasing sustainability awareness among younger consumers are transforming deodorant purchasing habits. China, in particular, benefits from strong social-commerce ecosystems and aspirational urban consumers receptive to refillable formats.

India, Japan, and Australia also drive regional growth, with refillables positioned as premium, safe, and aesthetically refined. Influencer marketing, e-commerce, and sustainability storytelling help increase awareness and trial, enabling refillable deodorants to shift from niche to mainstream. The combination of affordability, convenience, and eco-conscious appeal creates strong opportunities across key Asia Pacific urban markets.

Competitive Landscape

The refillable deodorants market is moderately consolidated, with a few major players controlling 60–70% of the market, while emerging direct-to-consumer sustainability-focused brands occupy niche positions. Leading incumbents leverage scale advantages in portfolio management, R&D, sustainability innovation, and omnichannel distribution, enabling broad positioning across premium, masstige, and mass-market segments. Strategic acquisitions and partnerships highlight the importance of digital-first, values-driven brand equity in capturing eco-conscious consumers.

Competitive differentiation focuses on three key dimensions: formulation innovation emphasizing natural, safe ingredients; packaging sustainability and refillable mechanics; and distribution strategy balancing subscription-based direct-to-consumer channels with mainstream retail. Smaller brands use influencer marketing, social commerce, and community-building to achieve rapid customer adoption.

Key Market Developments:

- In April 2025, Unilever Plc completed the acquisition of Wild, the UK-based refillable deodorant brand founded in 2019, for approximately £230 million ($286 million), reflecting strategic recognition of direct-to-consumer sustainability-focused brands' growth trajectory and market leadership positioning within the premium refillable segment.

- In March 2024, Tom's of Maine, Colgate-Palmolive's natural personal care subsidiary, launched deodorant products in 100% recycled plastic containers, advancing sustainability positioning and demonstrating incumbent commitment to refillable and sustainable packaging innovation across portfolio brands.

- In August 2024, Procter & Gamble expanded its Native brand portfolio with the introduction of Whole-Body Deodorant formulations combining 72-hour odor protection with plant-based ingredients, demonstrating innovation velocity within the premium natural segment and validating acquisition synergies from Native integration, supporting multi-category expansion from initial deodorant positioning.

Companies Covered in Refillable Deodorants Market

- Unilever Plc

- Procter & Gamble Company

- L'Oréal Group

- Beiersdorf AG

- Colgate-Palmolive Company

- Myro

- By Humankind

- Wild

- Fussy

- Noniko

- Proverb Skincare

- Helmm

- Asuvi

- Alpine Provisions

- Ethique

Frequently Asked Questions

The global refillable deodorants market is projected to reach US$ 5.1 Billion by 2033, expanding from US$ 3.3 Billion in 2026, representing a CAGR of 6.4% during the forecast period.

Demand is driven by 65%+ consumers seeking sustainable packaging, regulatory mandates such as the EU Packaging Waste Regulation, and premiumization trends supporting eco-conscious, high-efficacy products.

Stick refillable deodorants dominate with 62.1% share, supported by consumer familiarity, superior refill mechanics, compact packaging, and premium positioning in developed markets.

Asia Pacific is the fastest-growing region with 32.3% share, driven by rising disposable incomes, 60–70% digital commerce penetration, and sustainability-focused younger demographics.

Subscription-based refill and DTC models offer highest growth potential, expanding at 7.34% CAGR, enabling recurring revenue, personalized engagement, and alignment with sustainability narratives.