- Processed Food

- Soups and Broths Market

Soups and Broths Market Size, Share, and Growth Forecast, 2025 - 2032

Soups and Broths Market By Product Type (Canned, Dehydrated, Others), Ingredient (Vegetable, Chicken, Others), Sales Channel (Wholesales/Distributor/Direct, Supermarket/Hypermarket, Convenience Store, Online Retailers, Others), and Regional Analysis for 2025 - 2032

Soups and Broths Market Size and Trends Analysis

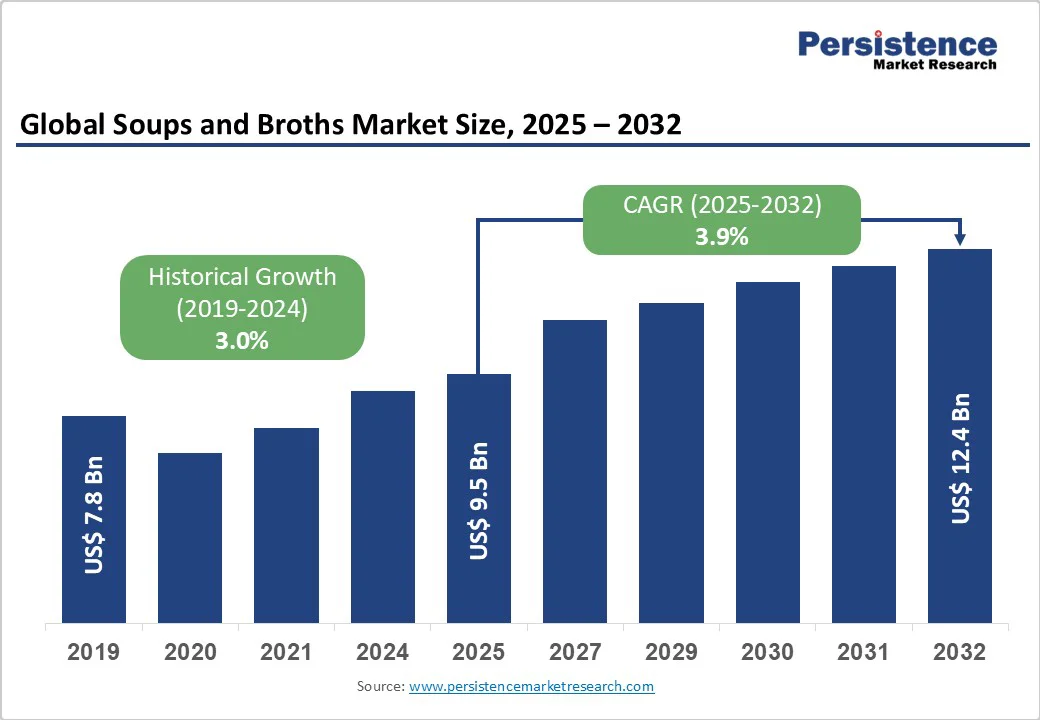

The global soups and broths market size is likely to be valued at US$9.5 Billion in 2025 and is expected to reach US$12.4 Billion by 2032, growing at a CAGR of 3.9% during the forecast period from 2025 to 2032, driven by rising demand for convenient, healthy, and ready-to-serve meals.

Key Industry Highlights

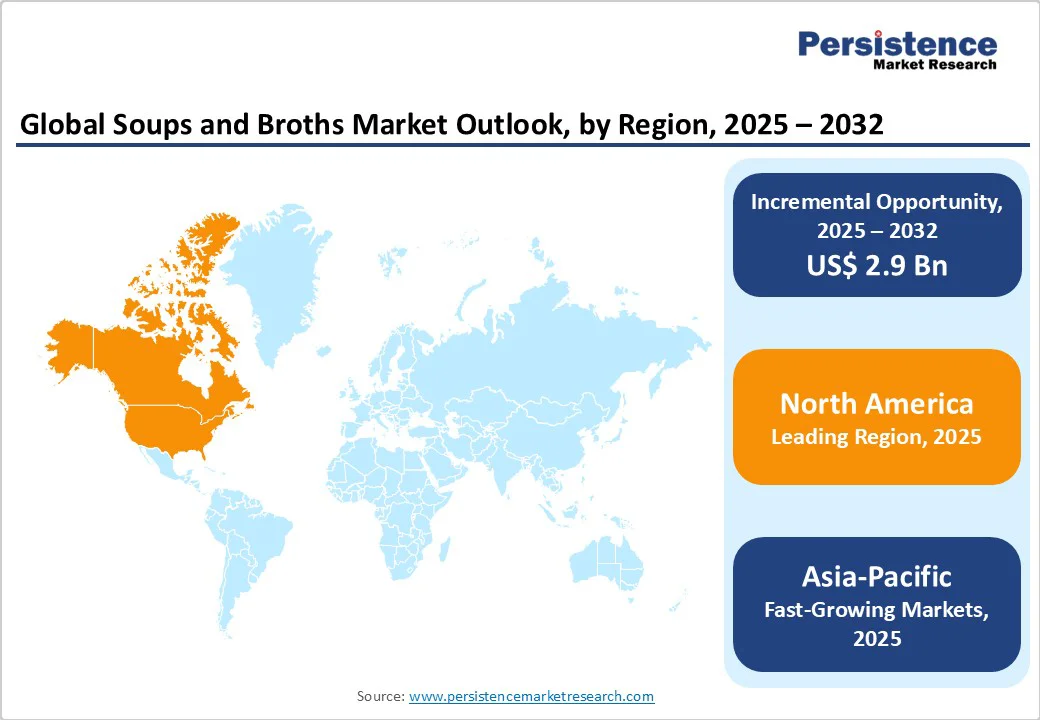

- Leading Region: North America, holding nearly 32.5% share in 2025, driven by high consumption of ready-to-serve soups, strong presence of major brands, and growing demand for convenient, healthy, and low-fat meal options across retail and foodservice sectors.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, supported by rising urbanization, increasing disposable incomes, rapid expansion of modern retail, and growing adoption of Western-style convenience foods among younger consumers.

- Investment Plans: Europe is investing heavily in organic, plant-based, and clean-label soups and broths, emphasizing sustainable sourcing, eco-friendly packaging, and R&D in low-sodium and additive-free formulations to meet evolving consumer preferences.

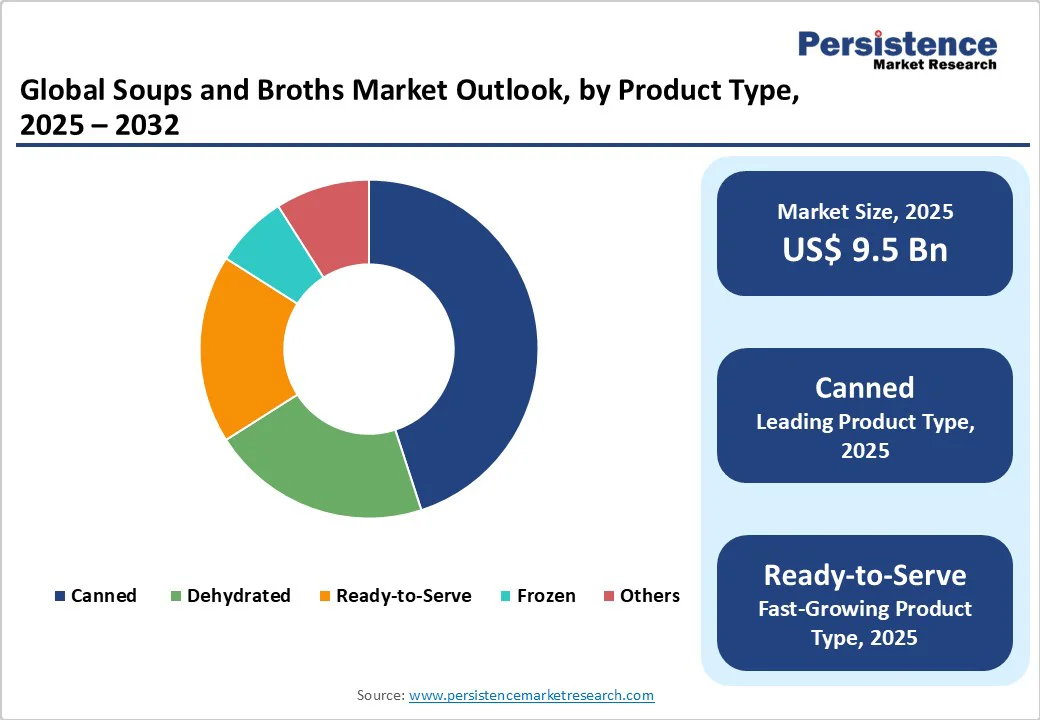

- Dominant Product: Canned Soups lead the market, capturing nearly 45.5% share, due to their long shelf life, variety in flavors, and strong distribution across supermarkets, convenience stores, and online platforms.

| Key Insights | Details |

|---|---|

| Soups and Broths Market Size (2025E) | US$9.5 Bn |

| Market Value Forecast (2032F) | US$12.4 Bn |

| Projected Growth (CAGR 2025 to 2032) | 3.9% |

| Historical Market Growth (CAGR 2019 to 2024) | 3.0% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Demand for Convenient and Ready-to-Serve Foods

The growing demand for convenient and ready-to-serve foods is a key market driver. With increasingly busy lifestyles, consumers are opting for meal options that save time while offering balanced nutrition. Ready-to-serve soups and broths cater to this need by providing quick, wholesome, and easily accessible meals suitable for all age groups.

The rise in dual-income households, urbanization, and changing eating habits has made convenience a top priority in daily food choices. Technological advances in packaging and preservation have also improved product shelf life and quality, making soups and broths more appealing for on-the-go consumption. This shift toward convenience-based nutrition continues to shape global food preferences, driving steady market growth.

Health Concerns, Especially Sodium and Preservatives

Health concerns related to sodium and preservatives are significant restraints. Excessive sodium intake is linked to increased blood pressure, raising the risk of heart disease and stroke. The U.S. Food and Drug Administration (FDA) notes that most dietary sodium comes from packaged and prepared foods, with over 70% of sodium intake attributed to these sources. The Centers for Disease Control and Prevention (CDC) reports that the average American consumes more than 3,300 milligrams of sodium daily, exceeding the recommended limit of less than 2,300 milligrams per day.

Preservatives used in soups and broths, such as sodium benzoate, have raised health concerns. Studies indicate that sodium benzoate may have adverse effects on human health, especially with long-term exposure. The FDA has also issued public health alerts for ground cinnamon products containing elevated levels of lead, highlighting potential contamination risks in food products. These health concerns have led to increased consumer demand for low-sodium and preservative-free options, influencing market trends and product development.

Demand for Plant-Based and Organic Products

The market is witnessing a growing opportunity driven by rising demand for plant-based and organic products. Consumers are increasingly prioritizing health, sustainability, and ethical production practices in their food choices. According to the U.S. Department of Agriculture (USDA), demand for organic products has consistently grown since the 1990s, reflecting a long-term shift in consumer behavior. In the soups and broths segment, this trend translates into increased interest in plant-based and organic variants that offer cleaner ingredients, lower additives, and environmentally responsible sourcing.

Manufacturers are responding by innovating recipes, incorporating organic vegetables, legumes, and plant-based proteins, and promoting sustainable packaging. This meets consumer expectations and differentiates brands in a competitive market. Capitalizing on this trend can drive higher sales, expand market share, and build loyalty among health-conscious and environmentally aware consumers, positioning plant-based and organic soups and broths as a key growth segment.

Category-wise Analysis

Product Insights

Canned Soups dominate the market with approximately 45.5% share in 2025, due to their convenience, long shelf life, and ease of storage. Unlike fresh or frozen varieties, canned products can be stored at room temperature, making them accessible for households, restaurants, and institutions without specialized refrigeration. They also offer consistent taste and quality, which appeals to consumers seeking reliable and ready-to-use meal options.

Canned soups are widely distributed through supermarkets, convenience stores, and online channels, ensuring broad availability. Their portability, minimal preparation requirements, and ability to retain nutrients during processing further strengthen their preference among consumers, making canned soups and broths the dominant product type in the market.

Ingredient Insights

Chicken dominates due to its affordability, versatility, and consumer preference. In 2025, broiler meat accounted for 44.8% of total per capita red meat and poultry consumption in the U.S., with an average of 101.1 pounds per person. This trend reflects a long-standing shift toward chicken as the most consumed meat in the U.S., driven by factors such as lower production costs and versatility in cooking.

Chicken's mild flavor and nutritional profile make it a preferred base for soups and broths, catering to a broad consumer base seeking healthy and convenient meal options. The USDA's Economic Research Service also notes that broiler meat accounted for 46% of all red meat and poultry consumption by volume in 2023, underscoring its dominance in the market.

Regional Insights

North America Soups and Broths Market Trends

North America dominates the global market with a 32.5% share in 2025, due to a combination of high consumer demand, developed retail infrastructure, and strong preference for convenient and ready-to-serve foods. Busy lifestyles and urbanization have increased reliance on packaged soups and broths, while the availability of diverse product formats, canned, frozen, and ready-to-serve, meets varying consumer needs.

The U.S. Department of Agriculture (USDA) reports that household consumption of packaged and processed foods has steadily risen, reflecting this trend. Institutional programs such as school meal initiatives and food assistance programs often include soups and broths, further boosting demand (fns.usda.gov). Combined with strong retail penetration and consumer awareness about health and convenience, these factors make North America the leading region in the market.

Europe Soups and Broths Market Trends

Europe is a significant player in the market due to several key factors. The European Union (EU) has a strong tradition of soup consumption, with various countries having their own unique soup recipes and preferences. For instance, in 2020, the EU's processed fruit and vegetable sector, which includes soups, was valued at €47 billion, accounting for 6.7%. This indicates a substantial demand for processed soup products within the region.

The EU also has stringent food safety regulations and quality standards, ensuring the production of safe and high-quality soups and broths. The European Commission's Rapid Alert System for Food and Feed (RASFF) reported in 2020 that soups and sauces accounted for 44 food safety nonconformities, highlighting the importance of maintaining high standards in the industry.

Furthermore, the EU's emphasis on sustainability and clean-label products has led to an increase in consumer demand for soups and broths made with natural ingredients and minimal additives. This shift in consumer preferences is driving innovation and growth in the European soups and broths market.

Asia Pacific Soups and Broths Market Trends

The Asia Pacific region is witnessing rapid growth in the soups and broths market due to several interrelated factors. Urbanization is a significant driver; for instance, Central Asia's urban population surged from approximately 25 million in 2000 to over 35.5 million by 2019, accounting for nearly half of the region's total population. This urban expansion leads to increased demand for convenient, ready-to-eat food options such as soups and broths.

Economic growth in countries such as the Philippines has also bolstered consumer spending power, with the retail sector projected to grow by 5%. However, challenges remain, as the Asia Pacific continues to represent half of the global total of undernourished individuals, with 370.7 million people affected. Despite these challenges, the combination of urbanization, economic growth, and evolving dietary preferences positions the Asia Pacific region as a rapidly expanding market for soups and broths.

Competitive Landscape

The global soups and broths market is growing as producers adopt advanced processing, fortification, and value-addition techniques. Leading companies focus on quality, flavor retention, and shelf life, while emerging players target organic and specialty segments. Strategic partnerships, sustainable sourcing, and traceability enhance competitiveness, boosting consumption and market expansion globally.

Key Industry Developments:

- In July 2025, Unilever unveiled its new Korean-inspired soup and noodle brand, Namdong, marking its entry into the premium instant soups and broths segment. Namdong offers consumers rich, complex flavors, with recipes designed to provide a thicker, stew-like broth that delivers a deeper, more satisfying noodle experience, catering to growing demand for authentic, convenient Asian-style meals.

- In December 2024, Unilever announced the sale of its food brands, Unox and Zwan, to Zwanenberg Food Group. The transaction marked Unilever’s strategic move to streamline its portfolio, while Zwanenberg aimed to expand its presence in the European processed foods market, strengthening its product offerings in soups, broths, and other ready-to-eat segments.

- In December 2024, Campbell Soup Company introduced a new range of soups and cooking broths with a spicy twist. The launch aimed to cater to consumers seeking bold flavors and diverse culinary experiences, enhancing its product portfolio in the ready-to-eat soups and broths segment and responding to growing demand for flavorful, convenient meals.

Companies Covered in Soups and Broths Market

- Campbell Soup Company

- Kraft Heinz Company

- Nestlé S.A.

- Unilever PLC

- B&G Foods, Inc.

- Conagra Brands Inc.

- Amy's Kitchen

- The Hain Celestial Group, Inc.

- Baxters Food Group Ltd.

- Blount Fine Foods

- Del Monte Foods Corporation Inc.

- Kettle & Fire Inc.

- Nissin Foods

- Uptons Naturals

- Ottogi Corporation

- Bes'Dam Soup

- Aylmer Soups

- Mitchell's Soup Co.

- Pacific Foods of Oregon

Frequently Asked Questions

The soups and broths market is projected to be valued at US$9.5 Billion in 2025.

Rising demand for convenient, healthy meals, urbanization, economic growth, and preference for organic, ready-to-eat products.

The market is poised to witness a CAGR of 3.9% between 2025 and 2032.

Expansion of organic, specialty, and fortified soups, innovative packaging, and growth in emerging Asia Pacific markets are the key market opportunities.

Major players in the soups and broths market are Campbell Soup Company, Kraft Heinz Company, Nestlé S.A., Unilever PLC, B&G Foods, Inc., and Conagra Brands Inc.