- Hardware & Software IT Services

- Public Cloud Service Market

Public Cloud Service Market Size, Share, and Growth Forecast 2026 - 2033

Public Cloud Service Market by Service Model (Infrastructure as a Service, Platform as a Service, and Software as a Service), Enterprise Type (Large Enterprise and Small & Medium Enterprise), Application (Government, BFSI, Healthcare, Telecommunication, Energy & Utilities, Retail/ Wholesale, Manufacturing, Transportation, and Others), and Regional Analysis 2026 - 2033

Public Cloud Service Market Size and Share Analysis

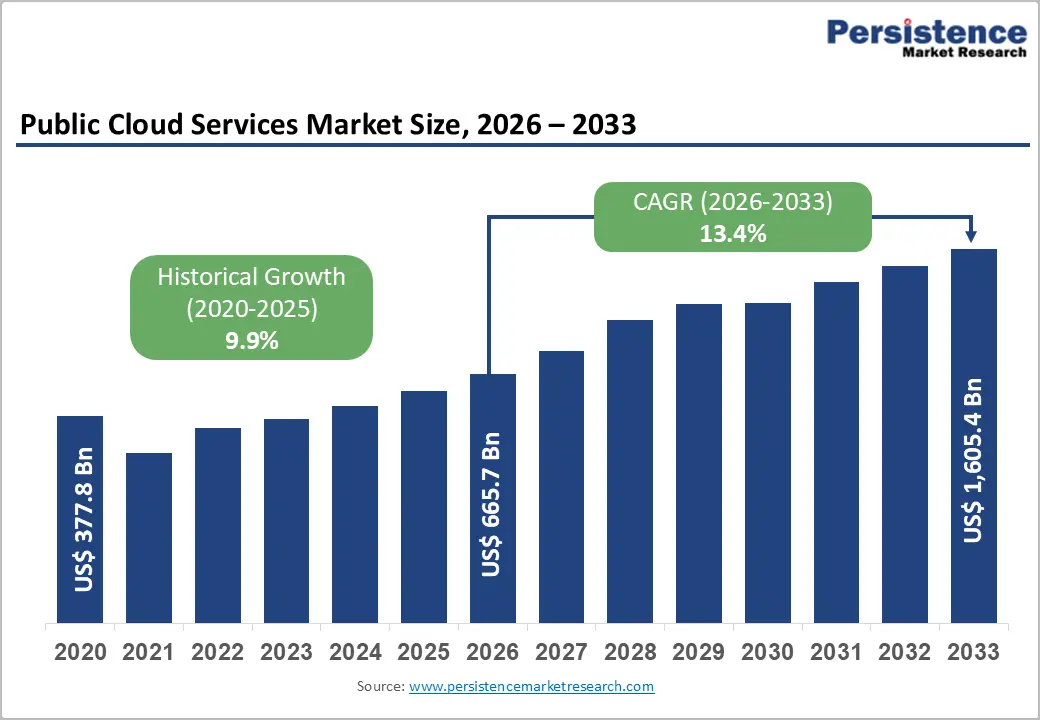

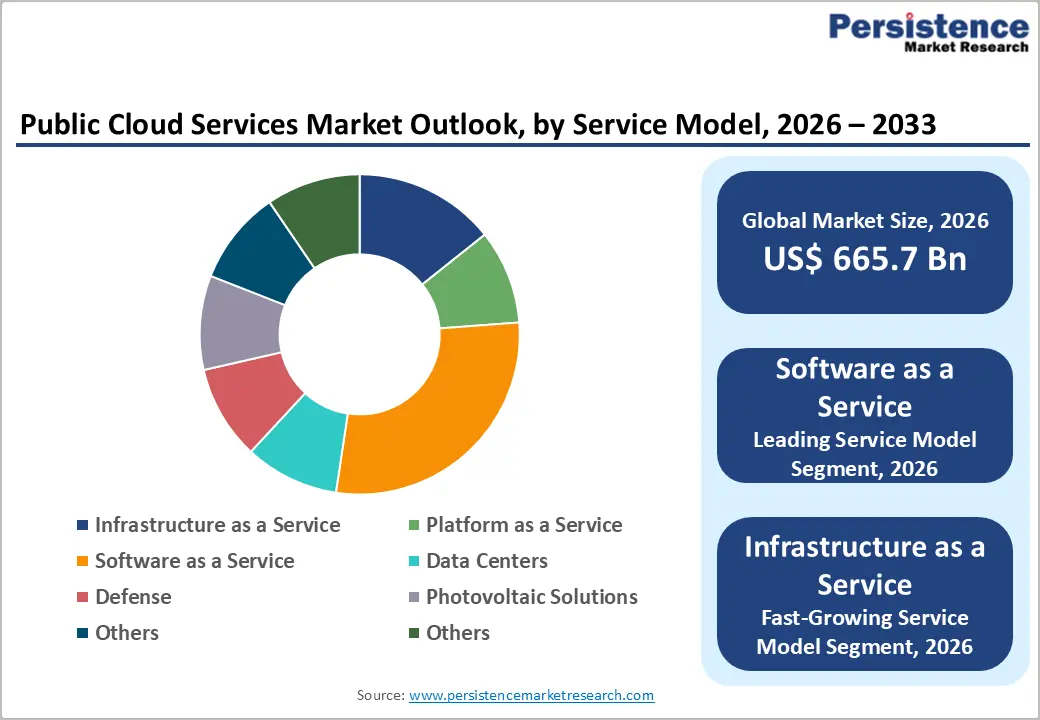

The global Public Cloud Service market size was valued at US$ 665.7 billion in 2026 and is projected to reach US$ 1,605.4 billion by 2033, growing at a CAGR of 13.4% between 2026 and 2033.

The market's expansion reflects accelerating digital transformation initiatives, widespread cloud-first organizational strategies, and unprecedented demand for scalable computing infrastructure driven by artificial intelligence and machine learning applications. The growing demand for cost-efficient IT infrastructure, remote workforce enablement, and data-intensive applications across sectors such as BFSI, healthcare, retail, and manufacturing, is further accelerating public cloud spending.

Key Market Highlights

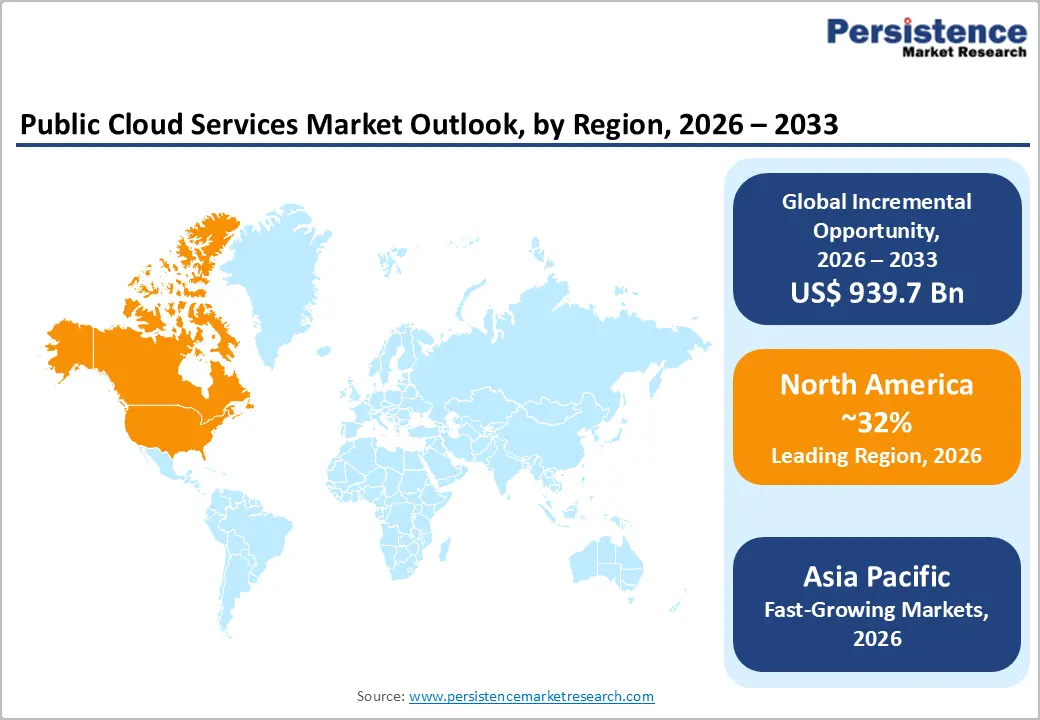

- Leading Region: North America dominates with 32% global market share, United States technology vendor concentration, federal government cloud modernization initiatives, and enterprise cloud adoption leadership at 94% organizational penetration establish North America as primary market driver through 2033.

- Fastest Growing Region: Asia Pacific is the fastest-growing region at 14.5% CAGR Massive digital transformation initiatives across China, India, Japan, and Southeast Asia, coupled with emerging market digitalization, establish Asia Pacific as the highest-growth opportunity zone through 2033.

- Dominant Service Model: Software as a Service (SaaS) dominates with 53% market share. Comprehensive enterprise functionality, subscription-based pricing models, and accessibility for small to medium enterprises drive SaaS market dominance across enterprise segments.

- Growing Application: Infrastructure as a Service (IaaS) is the fastest growing at 24.8% annual expansion. Artificial intelligence infrastructure requirements, hyperscale data center deployment, and machine learning application development accelerate IaaS adoption, driving segment expansion.

- Key Market Opportunity: Artificial Intelligence and Machine Learning integration represents major market opportunity, 72% organization AI adoption rate, large language model training requirements, and generative AI application development create unprecedented demand for cloud computing infrastructure and services.

| Key Insights | Details |

|---|---|

|

Global Public Cloud Service Market Size (2026E) |

US$ 665.7 Bn |

|

Market Value Forecast (2033F) |

US$ 1,605.4 Bn |

|

Projected Growth CAGR (2026-2033) |

13.4% |

|

Historical Market Growth (2020-2025) |

9.9% |

Market Dynamics

Market Growth Drivers

Accelerating Adoption of Artificial Intelligence and Machine Learning Applications

The accelerating adoption of artificial intelligence (AI) and machine learning (ML) applications is a major driver fueling growth in the global public cloud service market. Modern AI and ML workloads require vast computational power, high-performance storage, and advanced data-processing capabilities, which are often impractical or prohibitively expensive to deploy and maintain on traditional on-premises infrastructure. Public cloud platforms address these challenges by offering elastic compute resources, specialized processors such as GPUs and TPUs, and scalable data lakes that can support large-scale model training and real-time inference. As organizations increasingly rely on AI-driven use cases, such as predictive analytics, natural language processing, computer vision, recommendation engines, and autonomous systems, the need for flexible and on-demand cloud infrastructure continues to intensify.

Public cloud providers are rapidly expanding their portfolios of AI-as-a-service and ML-as-a-service offerings, enabling enterprises to accelerate innovation without deep in-house expertise. These services lower entry barriers for small and mid-sized enterprises while allowing large enterprises to shorten development cycles and improve time to market. The integration of AI into core business processes, including customer experience management, fraud detection, supply chain optimization, and intelligent automation, further reinforces cloud dependency. As data volumes grow exponentially and AI models become more complex, public cloud environments remain the preferred foundation for scalable, secure, and cost-efficient AI deployment, making AI and ML adoption a critical long-term growth catalyst for the market.

Enterprise Digital Transformation and Cloud-First Organizational Strategies

Enterprise digital transformation initiatives and the widespread adoption of cloud-first organizational strategies are another fundamental driver of the global public cloud service market. Across industries, organizations are modernizing legacy IT systems to improve operational efficiency, agility, and competitiveness in an increasingly digital economy. Cloud-first strategies prioritize the use of public cloud platforms for new applications and system upgrades, enabling enterprises to rapidly deploy digital services, streamline workflows, and enhance collaboration across distributed teams. Public cloud services support this transformation by offering scalable infrastructure, platform services, and software solutions that reduce capital expenditure and shift IT spending toward flexible operating models.

Cloud-based architecture enables faster innovation through DevOps practices, microservices, and containerization, allowing businesses to respond quickly to changing market demands. The rise of remote and hybrid work models has further reinforced cloud adoption, as organizations require secure, accessible, and resilient environments to support a geographically dispersed workforce. Public cloud platforms also play a critical role in enabling data-driven decision-making by providing integrated analytics, automation, and interoperability with emerging digital technologies. As enterprises continue to prioritize resilience, business continuity, and long-term scalability, cloud-first strategies are becoming deeply embedded in corporate IT roadmaps, positioning public cloud services as a foundational pillar of global digital transformation efforts.

Market Restraints

Security Vulnerabilities and Regulatory Compliance Complexity

Security vulnerabilities and regulatory compliance complexity remain significant restraints for the global public cloud service market, particularly for organizations operating in highly regulated industries. While public cloud providers invest heavily in advanced security frameworks, the shared responsibility model often creates ambiguity around accountability for data protection, identity management, and application security. Misconfigurations, inadequate access controls, and insufficient monitoring can expose sensitive data to breaches, cyberattacks, and unauthorized access. These risks are amplified as enterprises migrate critical workloads, confidential customer information, and intellectual property to cloud environments. In parallel, regulatory compliance requirements are becoming increasingly complex and region-specific, covering data privacy, residency, and governance mandates.

Organizations must comply with evolving regulations across multiple jurisdictions, which can complicate cloud deployment strategies and increase legal and operational risks. Ensuring compliance often requires additional investments in security tools, audits, and specialized expertise, raising overall deployment costs and slowing cloud adoption. For multinational enterprises, managing compliance across geographically distributed cloud infrastructures adds further complexity, as data localization and cross-border transfer restrictions can limit flexibility.

Cost Overruns and FinOps Complexity Limiting Budget Predictability

Cost overruns and the growing complexity of financial operations (FinOps) pose another key restraint on the global public cloud service market, limiting budget predictability and financial control. Although public cloud services are often promoted as cost-effective alternatives to traditional IT infrastructure, their consumption-based pricing models can lead to unexpected expenses if usage is not carefully managed. Dynamic scaling, on-demand resources, and a wide array of service offerings make it challenging for organizations to accurately forecast costs, especially in multi-cloud or hybrid environments. Without robust cost governance frameworks, enterprises may experience “cloud sprawl,” where idle or underutilized resources accumulate unnoticed, driving up operational expenses.

Implementing effective FinOps practices requires cross-functional collaboration between finance, IT, and engineering teams, as well as investment in specialized tools and skilled personnel. For small and mid-sized enterprises, this added complexity can strain limited budgets and delay cloud optimization initiatives. Even large organizations may struggle to balance performance, scalability, and cost efficiency across diverse workloads. As a result, concerns about unpredictable spending, limited cost transparency, and the administrative burden of cloud financial management can slow adoption and encourage cautious or selective use of public cloud services.

Market Opportunities

Emerging Edge Computing and 5G Infrastructure Integration

The integration of emerging edge computing architectures with rapidly expanding 5G infrastructure presents a significant growth opportunity for the global public cloud service market. As latency-sensitive applications such as autonomous systems, smart manufacturing, real-time video analytics, and immersive AR/VR experiences gain traction, centralized cloud models alone are often insufficient to meet performance requirements. Edge computing extends public cloud capabilities closer to data sources by enabling localized processing, reducing latency, bandwidth consumption, and response times. When combined with 5G’s ultra-low latency, high bandwidth, and massive device connectivity, public cloud providers can deliver distributed computing environments that support next-generation digital use cases.

Cloud vendors are increasingly partnering with telecom operators and investing in edge-native platforms to offer seamless orchestration between central cloud data centers and edge nodes. This convergence allows enterprises to deploy scalable, secure, and resilient applications across geographically dispersed environments while maintaining centralized management and analytics. Moreover, edge-cloud integration supports data sovereignty and compliance requirements by enabling localized data processing where regulations restrict data movement. As industries such as healthcare, logistics, energy, and smart cities accelerate digital adoption, the demand for cloud-enabled edge solutions is expected to grow rapidly, positioning edge computing and 5G integration as a transformative opportunity for public cloud service providers.

Serverless Computing and Container-Based Application Development

Serverless computing and container-based application development represent a high-impact opportunity, driving innovation and adoption in the global public cloud services market. This architecture fundamentally changes how applications are built, deployed, and scaled by abstracting infrastructure management and enabling developers to focus on code and functionality. Serverless computing allows applications to run in response to events, automatically scaling resources up or down based on demand, which significantly improves cost efficiency and operational agility. In parallel, containerization and microservices architectures enable applications to be modular, portable, and highly resilient across cloud environments. Public cloud platforms provide managed container orchestration, continuous integration and delivery pipelines, and native support for DevOps practices, accelerating application modernization initiatives.

These capabilities are particularly valuable for enterprises migrating legacy systems, launching digital-native products, and supporting continuous innovation cycles. Additionally, serverless and container-based models enhance deployment consistency across hybrid and multi-cloud environments, reducing vendor lock-in concerns. As organizations increasingly prioritize faster time to market, scalability, and operational efficiency, the adoption of cloud-native development frameworks is expected to accelerate. This shift not only drives higher consumption of platform and compute services but also strengthens long-term reliance on public cloud ecosystems, creating substantial growth opportunities for cloud service providers.

Category-wise Insights

Service Model Analysis

Software as a Service (SaaS) maintains market dominance with approximately 53% market share, making it the largest and most accessible cloud service category for the enterprise and small- to medium-sized business segments. SaaS applications deliver comprehensive enterprise functionality spanning customer relationship management, enterprise resource planning, human resources management, financial planning, and collaboration tools through subscription-based licensing models, eliminating capital infrastructure investments and IT management complexity. The SaaS market is expanding at 15.9% annually, with enterprises focusing on vertical-specific solutions tailored for healthcare, financial services, retail, supply chain management, and manufacturing.

Infrastructure as a Service (IaaS) accounts for approximately 26% of the market, expanding at 24.8% annual growth driven by artificial intelligence infrastructure requirements, hyperscale data center deployments, and hybrid cloud adoption. IaaS providers, including Amazon Web Services, Microsoft Azure, and Google Cloud, maintain competitive positions through comprehensive service portfolios, pricing optimization capabilities, and emerging integration with artificial intelligence and machine learning.

Enterprise Type Analysis

Large Enterprises command approximately 62% market share, reflecting substantial information technology budgets, complex infrastructure requirements, and organizational capacity for sophisticated cloud architecture implementation. Large multinational organizations demonstrate the highest cloud service adoption rates at 94%, with 94% of enterprises exceeding 5,000 employees implementing multi-cloud strategies combining diverse cloud providers. Fortune 500 enterprises allocate average annual cloud spending exceeding US$ 12 million, reflecting comprehensive enterprise resource planning, customer relationship management, business intelligence, and infrastructure transformation initiatives.

Small and Medium Enterprises (SMEs) represent approximately 38% market share, expanding at an accelerating 10.07% annual growth rate, driven by cost-effective cloud access, democratizing enterprise software capabilities traditionally accessible exclusively to large organizations. SMEs demonstrate enthusiasm for SaaS solutions, eliminating capital infrastructure investments and enabling rapid deployment of competitive business applications. Cloud-based marketplace solutions including Shopify, Squarespace, and HubSpot provide SMEs with enterprise-grade capabilities supporting global commerce, marketing automation, and customer relationship management at affordable subscription pricing.

Application Analysis

The BFSI (Banking, Financial Services, and Insurance) segment accounts for approximately 18% of application deployments, significantly driving demand for advanced cloud-based analytics, risk assessment, and regulatory compliance solutions. Financial institutions are increasingly leveraging public cloud platforms to modernize customer relationship management systems, streamline transaction processing, and enhance regulatory reporting capabilities. This shift supports the expansion of open banking frameworks, real-time digital payment ecosystems, and data-driven financial services, enabling BFSI organizations to improve operational efficiency, strengthen compliance readiness, and deliver more personalized customer experiences.

Public cloud adoption in the BFSI sector is enabling scalable fraud detection, real-time credit scoring, and AI-driven customer insights, which are critical for managing growing transaction volumes and evolving cybersecurity threats. Cloud-based platforms also support faster product innovation through API-driven architectures and secure data sharing, allowing financial institutions to collaborate with fintech partners, improve service agility, and maintain business continuity while adhering to stringent data security and governance standards.

Regional Insights

North America Public Cloud Service Trends

North America maintains established market leadership with approximately 32% global market share, anchored by United States dominance representing approximately 28% of worldwide public cloud services spending. United States benefits from exceptional technology vendor concentration including Amazon Web Services, Microsoft, Google, and Salesforce alongside robust venture capital funding supporting cloud-native startup ecosystem development. Federal Government cloud modernization initiatives including FedRAMP compliance requirements and Department of Defense cloud infrastructure development drive public sector adoption, establishing baseline infrastructure requirements cascading through contractor supply chains.

United States enterprises demonstrate highest global cloud adoption rates at 94%, with 72% of cloud spending decisions controlled by information technology departments establishing organizational strategic alignment around cloud-first technology strategies. Canada contribute secondary market demand, with Canadian enterprises demonstrating comparable cloud adoption rates for operational efficiency and customer engagement improvements. North American regulatory framework including GDPR compliance for data transfers and emerging artificial intelligence governance requirements create compliance complexity elevating total cost of ownership for multinational organizations operating across North American and international jurisdictions.

Europe Public Cloud Service Trends

Europe represents approximately 24% global public cloud market share, characterized by stringent regulatory frameworks, progressive digital government initiatives, and strong cloud-native enterprise culture particularly in Germany, United Kingdom, France, and Scandinavian nations. European Union General Data Protection Regulation (GDPR) establishes world-leading data protection standards substantially influencing cloud infrastructure design, data governance practices, and compliance requirements adopted globally. European enterprises increasingly adopt sovereign cloud architectures, ensuring data residency compliance through European cloud providers or hyperscaler regional infrastructure, creating differentiated market opportunities for regional cloud service providers and establishing expansion pathways for multinational technology companies.The

United Kingdom post-Brexit regulatory environment creates independent data governance frameworks requiring specialized cloud infrastructure and compliance management capabilities supporting financial services, healthcare, and government applications. Germany maintains exceptional technology maturity and a large-scale manufacturing sector cloud adoption, with industrial enterprise digital transformation initiatives driving demand for advanced analytics, predictive maintenance, and supply chain optimization cloud platforms. France and Spain demonstrate accelerating cloud adoption through digital government programs, financial services innovation, and emerging artificial intelligence ecosystem development, establishing emerging market opportunities for cloud service providers to establish regional presence.

Asia Pacific Public Cloud Service Trends

Asia Pacific represents approximately 29% global public cloud market share, expanding at an accelerating growth rate, positioning the region as the highest-growth market through 2032. China maintains regional dominance through an extraordinary technology ecosystem scale, with domestic cloud providers Alibaba Cloud, Tencent Cloud, and Baidu Cloud capturing substantial domestic market share while expanding international presence. Chinese government digital transformation initiatives, e-commerce infrastructure requirements supporting Alibaba, JD.com, and emerging platforms, and the prioritization of artificial intelligence development drive persistent public cloud adoption.

India demonstrates exceptional cloud adoption growth through massive digital transformation initiatives, the development of its startup ecosystem, and a concentration in information technology services, establishing it as a high-growth opportunity. Government digital transformation programs across Vietnam, Thailand, Indonesia, and Malaysia are establishing foundational cloud infrastructure supporting emerging market digital economies.

Competitive Landscape for the Public Cloud Service Market

The Public Cloud Service market exhibits significant consolidation among dominant hyperscale cloud providers Amazon Web Services, Microsoft Azure, Google Cloud, and Alibaba Cloud collectively commanding approximately 72% aggregated market share through comprehensive service portfolios, continuous innovation, price optimization, and established enterprise customer relationships. Market leaders pursue expansion through strategic acquisition of specialized cloud application providers, infrastructure technology innovators, and artificial intelligence platform capabilities enabling differentiated service offerings.

Mid-sized competitors including Oracle, VMware, Salesforce, and IBM maintain competitive positions through specialization in specific vertical applications, legacy system integration capabilities, and enterprise customer relationships. Red Hat and Platform as a Service specialists provide containerization, Kubernetes orchestration, and cloud-native development tools addressing developer productivity and application modernization requirements.

Key Market Developments

- In September 2025, Amazon Web Services Announces Specialized Quantum Computing as a Service Capability, Amazon Web Services introduced quantum computing as a service enabling enterprise access to quantum computational capabilities without specialized infrastructure investment, establishing emerging market opportunity for quantum-enabled problem solving across pharmaceutical development, financial modeling, and optimization applications.

- In December 2024, Microsoft Azure Launches Advanced AI Copilot Integration for Enterprise Cloud Platforms, Microsoft Corporation unveiled comprehensive AI copilot integration throughout Azure cloud platform, enabling sophisticated natural language-based infrastructure management, automated optimization recommendations, and enterprise application development acceleration supporting enterprise digital transformation initiatives.

- In June 2024, Google Cloud Expands Infrastructure Footprint with Sovereign Cloud Deployments in European Union, Google Cloud announced establishment of sovereign cloud infrastructure meeting GDPR compliance requirements and European data residency mandates, enabling enhanced competitive positioning in European markets while supporting regulatory compliance requirements for multinational enterprises.

Companies Covered in Public Cloud Service Market

- Alphabet, Inc.

- Microsoft Corp.

- International Business Machines Corp.

- Oracle Corp.

- CenturyLink, Inc.

- Amazon Web Services Inc

- Salesforce.com, Inc.

- VMware, Inc.

- Adobe Systems, Inc.

- Red Hat, Inc.

- Alibaba Cloud

- Tencent Cloud

- Dropbox

- Slack Technologies

- Atlassian Corporation

Frequently Asked Questions

The global Public Cloud Service market was valued at US$ 665.7 billion in 2026 and is projected to reach US$ 1,605.4 billion by 2033, expanding at 13.4% CAGR. This exceptional growth trajectory reflects accelerating digital transformation initiatives, widespread cloud-first organizational strategies, and unprecedented demand for artificial intelligence infrastructure supporting machine learning applications globally.

Primary growth drivers include accelerating artificial intelligence and machine learning adoption with 72% of organizations utilizing AI services through cloud platforms, enterprise digital transformation initiatives with 88% of companies identifying cloud adoption as fundamental transformation cornerstone, and cloud-first organizational strategies with 94% enterprise cloud adoption.

Software as a Service (SaaS) dominates with approximately 53% market share, providing comprehensive enterprise functionality through subscription-based licensing models. Infrastructure as a Service (IaaS) represents 26% market share expanding at 24.8% annual growth rates, while Platform as a Service (PaaS) commands 21% market share with accelerating 21.5% annual expansion driven by serverless computing and container adoption.

North America maintains market leadership with approximately 32% global market share anchored by United States technology vendor dominance and 94% enterprise cloud adoption. Asia Pacific emerges as fastest-growing region with 18.5% CAGR, driven by massive digital transformation initiatives across China, India, Japan, and Southeast Asian markets establishing region as highest-growth opportunity zone through 2033.

Artificial intelligence infrastructure development and emerging edge computing integration represent most compelling opportunities, with 72% organization AI adoption driving public cloud infrastructure demand and edge computing achieving 29% enterprise penetration expanding at accelerating rates through 5G deployment and IoT application requirements.

Market leaders include Amazon Web Services commanding 32% market share through comprehensive service breadth, Microsoft Corporation capturing 23% share through enterprise integration advantages, Google Cloud commanding 11% share through artificial intelligence specialization, Alibaba Cloud and Tencent Cloud leading Asia Pacific markets, alongside Oracle, Salesforce, IBM, VMware, Adobe, and Red Hat maintaining specialized competitive positions through vertical applications and developer platform differentiation.