- Pharmaceuticals

- Lysosomal Storage Disease (LSD) Therapeutics Market

Lysosomal Storage Disease (LSD) Therapeutics Market Size, Share, and Growth Forecast, 2025 - 2032

Lysosomal Storage Disease (LSD) Therapeutics Market by Treatment (Enzyme Replacement Therapy, Hematopoietic Stem Cell Transplant, Small Molecule Therapy, Others), Indication, End-User, and Regional Analysis for 2025 - 2032

Lysosomal Storage Disease (LSD) Therapeutics Market Share and Trends Analysis

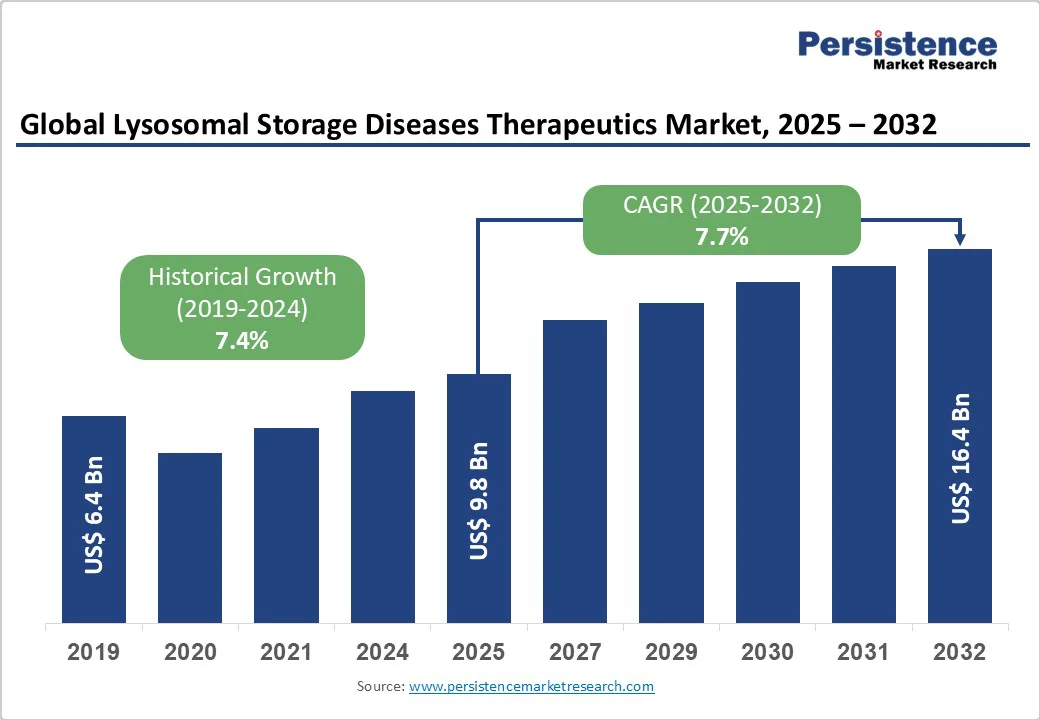

The global lysosomal storage disease (LSD) therapeutics market size is likely to be valued at US$ 9.8 billion in 2025, and is projected to reach US$ 16.4 billion by 2032, growing at a CAGR of 7.7% during the forecast period 2025-2032. Since the characteristics of LSD vary widely due to heterogeneity of substrate types and enzyme deficiencies, they necessitate personalized treatment approaches. Growing advancements in enzyme replacement therapies (ERT), gene therapies, and small-molecule interventions are driving the evolution of the LSD treatment landscape.

Key Industry Highlights

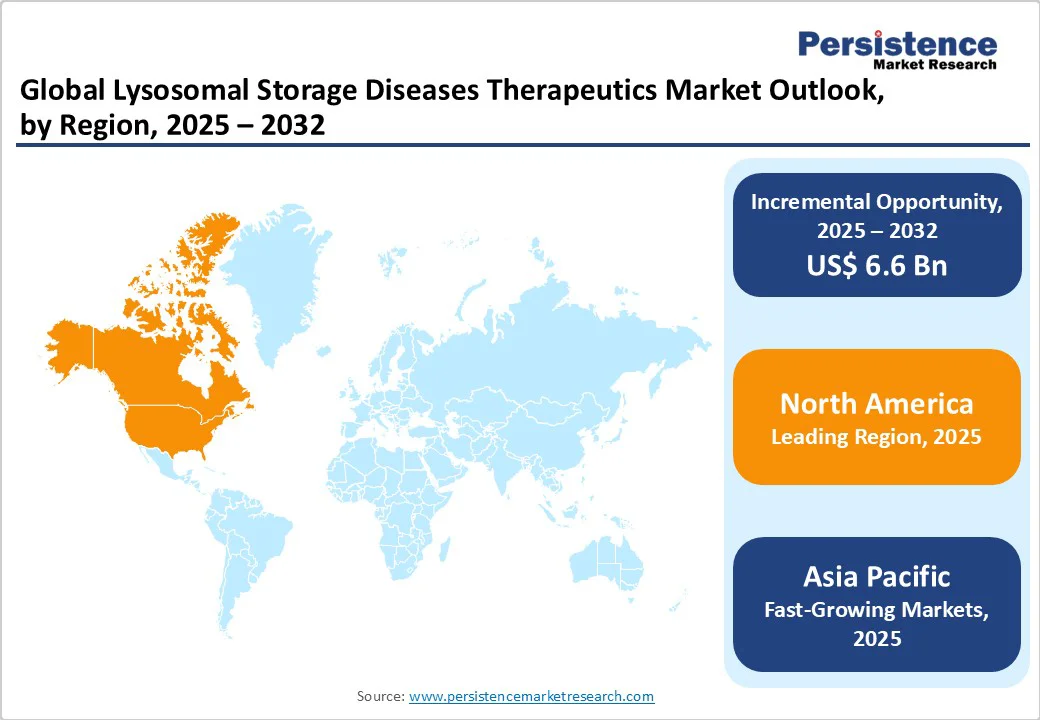

- Leading Region: North America is likely to lead the market share in 2025, supported by advanced healthcare infrastructure, strong regulatory support, and early adoption of innovative rare disease therapies.

- Fastest-Growing Regional Market: Asia Pacific is set to be the fastest-growing regional market, driven by rising awareness, diagnostics expansion, and new government-backed rare disease initiatives.

- Leading Treatment Modality: Enzyme replacement therapy (ERT) is slated to lead, as it is widely established for Gaucher, Fabry, and Pompe diseases with proven efficacy.

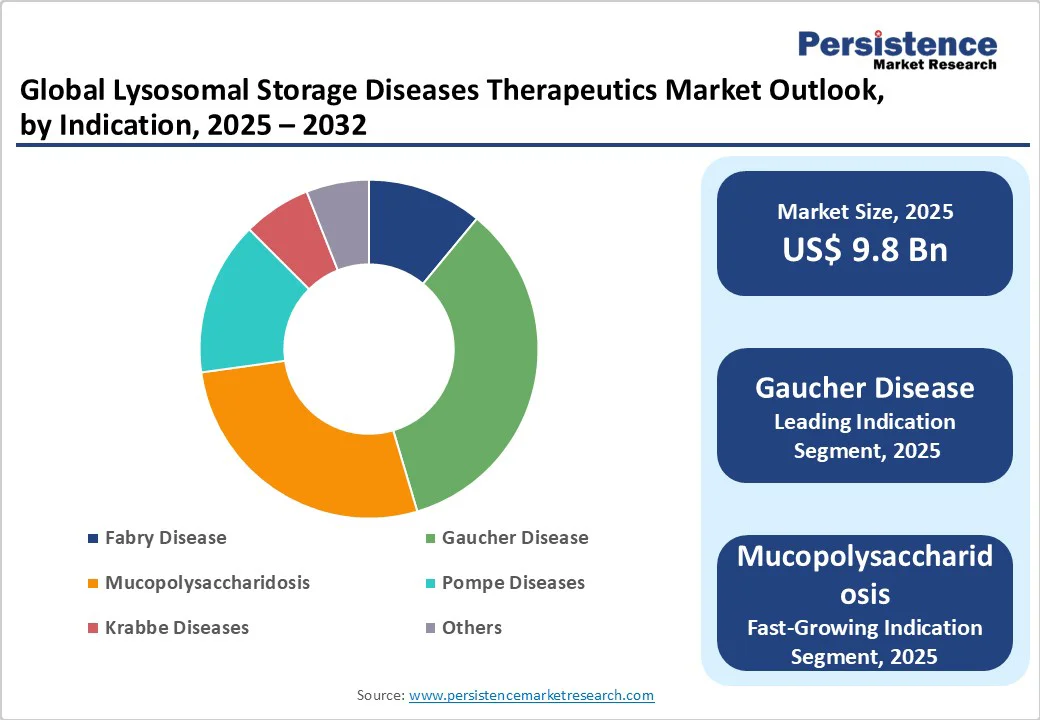

- Leading Indication: Gaucher disease is poised to be the leading indication in 2025, owing to higher prevalence and established therapeutic options across developed markets.

- Fastest-Growing Indication: Mucopolysaccharidoses (MPS) is the fastest-growing indication through 2032, due to expanding clinical trials and greater focus on pediatric patient populations.

- Competitive Environment: Collaborations and licensing deals between pharma companies, academia, and rare disease foundations are increasing, accelerating R&D progress and expanding treatment access across geographies.

- Investment Focus: Expanding pipeline of next-generation ERTs and gene/substrate reduction therapies is advancing LSD treatment with improved stability and broader efficacy.

| Key Insights | Details |

|---|---|

|

Lysosomal Storage Disease therapeutics Market Size (2025E) |

US$ 9.8 Bn |

|

Market Value Forecast (2032F) |

US$ 16.4 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

7.7% |

|

Historical Market Growth (CAGR 2019 to 2024) |

7.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Clinical Need for LSD Therapeutics and Scientific Advancements

The growing prevalence of lysosomal storage disorders across the globe, along with the clinical complexity associated with it is fueling the demand for innovative therapeutic solutions. The combined global incidence of LSD is around 1 in 5000-7500 births, with higher prevalence in specific populations, according to the U.S. National Institutes of Health (NIH). LSDs, caused by enzyme deficiencies or mutations in lysosomal proteins, lead to substrate accumulation in cells, resulting in progressive organ damage, neurological decline, and, in many cases, premature mortality.

Existing treatment options, such as ERT and substrate reduction therapies, address only partial aspects of disease progression, leaving significant unmet medical needs. Growing research and development in the advancements related to mRNA-based approaches, gene therapy, and targeted delivery technologies are expanding the pipeline of next-generation LSD therapeutics. This urgent clinical need, combined with rapid scientific progress and increasing awareness among healthcare providers and patient communities, is driving robust investment and growth in the lysosomal storage disease therapeutics market, making it a high-priority area within rare disease drug development.

Therapeutic Limitations, CNS Delivery Challenges, and Clinical Development Hurdles Restraining Market Growth

The lysosomal storage disease therapeutics market growth faces significant limitations due to the complex biology of these disorders and barriers in drug development. Conventional ERTs have a short half-life, require frequent infusions, variable bioavailability, and limited targeting of organs such as bones, cartilage, and eyes. While its effectiveness is shown in some systemic symptoms, they often fail to cross the blood-brain barrier (BBB), leaving neurological manifestations untreated. On the other hand, variable engraftment in hematopoietic stem cell transplantation (HSCT) limits its applicability and increases morbidity and mortality risks. Gene therapies, though promising, face hurdles such as vector size constraints in AAV (Adeno-Associated Virus)-based approaches, limiting correction of large genes.

Clinical development is further constrained by phenotypic heterogeneity, ultra-rare patient populations, and a lack of robust history data and validated biomarkers. Diagnostic delays exacerbate disease progression before intervention, while high costs and uncertain returns restrict investment. Emerging innovations are addressing these key limitations in LSD therapeutics. Study on JCR’s proprietary J-Brain Cargo® has demonstrated the ability to cross the blood-brain barrier, enabling CNS-targeted drug delivery. Further, approved gene therapy OTL-200 and ongoing AAV-based trials, combined with advanced gene editing tools, offer potential solutions for treating larger genes and expanding therapeutic reach for neuronopathic LSDs.

Strategic Advancements in CNS-Penetrant Therapies and Innovative Platforms

Players active in the lysosomal storage disease therapeutics market have significant opportunities to capitalize on emerging technologies and expanding pipelines. CNS-targeted delivery approaches, such as receptor-mediated transcytosis in clinical trials for MPS II and III, offer a chance to address unmet neurological manifestations. The development of extracellular vesicles (EVs) for delivering functional lysosomal proteins to organs such as the brain, heart, and kidneys allows companies to differentiate their therapies.

Leading firms are also actively expanding pipelines such as Denali Therapeutics has clinically active drug pipeline for MPS I, MPS II, and MPS IIIA, while Sangamo Therapeutics has several gene therapies in clinical development for Fabry disease at present. In parallel with clinical pipeline growth, firms are achieving key regulatory milestones. In September 2024, for instance, GC Biopharma and Hanmi Pharmaceutical achieved Investigational New Drug (IND) clearance for a Phase 1/2 clinical trial from the U.S. Food and Drug Administration (FDA) for their innovative drug - LA-GLA (GC1134A/HM15421), a once-monthly subcutaneous therapy for Fabry disease.

Category-wise Analysis

Treatment Insights

Enzyme replacement therapy (ERT) is expected to maintain the leading share of approximately 75.8% in 2025. Administered intravenously, ERT provides functional, properly glycosylated enzymes that utilize MP6R and endogenous endocytic pathways to reach lysosomes in target cells. Clinically established for nearly two decades, ERT remains the gold standard, demonstrating efficacy in slowing disease progression and improving patient quality of life. Hematopoietic stem cell transplantation (HSCT), indicated for severe MPS I, Krabbe disease, and attenuated metachromatic leukodystrophy, is witnessing rising adoption in pediatric patients diagnosed before 2.5 years, reflecting growing clinical preference for early intervention in select LSD subtypes.

Other emerging segments, including pharmacological chaperones, substrate reduction therapy (SRT), autophagy regulators, and gene therapies (both ex-vivo and in-vivo), are gaining traction by targeting enzyme stabilization, substrate clearance, and molecular pathways. These innovative approaches are expanding treatment options and are poised to drive growth in the market alongside established ERT therapies.

Indication Insights

Gaucher Disease is projected to remain the leading indication segment in 2025 with one-third of the lysosomal storage disease market revenue share. Its dominance is driven by well-established clinical guidelines for the disease, and the long-standing availability of ERTs effectively managing systemic symptoms and improving patient quality of life. The extensive clinical experience with ERTs in Gaucher disease reinforces physician confidence and supports consistent treatment uptake.

On the other hand, Fabry disease and MPS are showing significant growth potential due to expanding awareness, late-stage pipeline therapies, and novel treatment modalities, including CNS-penetrant ERTs, gene therapies, and substrate reduction therapies. These emerging segments are gaining traction as innovative approaches address unmet needs, particularly neurological and multi-organ involvement, offering substantial opportunities for market players.

Regional Insights

North America Lysosomal Storage Disease Therapeutics Market Trends

The North America LSD therapeutics market is expanding rapidly and is projected to account for 37.1% of the global market share by 2025, with the United States being the key contributor. Regional growth is driven by the presence of well-established clinical programs, advanced healthcare infrastructure, and strong research initiatives in rare diseases. Some of the top programs and initiatives for LSD therapeutics, such as the UF Lysosomal Storage Disease Program and Atlantic Health System, provide comprehensive, multi-disciplinary care, combining diagnosis, management, treatment, and monitoring of LSD patients. These programs integrate multiple therapeutic modalities, including ERT, HSCT, and small molecule therapy, alongside innovative clinical trials exploring next-generation therapies.

U.S.-based LSD programs emphasize personalized approaches to address the multi-systemic nature of these disorders, which manifest in neurological, renal, cardiovascular, gastrointestinal, musculoskeletal, ophthalmologic, and respiratory complications. The integration of clinical research with patient care accelerates access to cutting-edge therapeutics and promotes rapid adoption of novel treatment modalities. Moreover, collaborations between research centers, hospitals, and biotech companies facilitate the evaluation of advanced therapies in diverse patient populations.

Europe Lysosomal Storage Disease Therapeutics Market Trends

Europe represents a key regional market for lysosomal storage disease therapeutics, projected to hold approximately 29.4% of the total market share by 2025. This prominence is attributed to advanced healthcare infrastructures, specialized treatment centers, and robust government and industry support for rare disease research. The U.K. LSD therapeutics market is set to experience notable growth from 2025 to 2032, as organizations such as the UK LSD Patient Collaborative, Niemann-Pick UK, and Krabbe UK are actively involved in raising awareness, providing support, and advocating for improved treatment options for individuals affected by LSDs.

These efforts are complemented by initiatives such as Chiesi Global Rare Diseases' "Find For Rare" Research Grant Initiative launched in September 2024, which offers grants up to € 50,000 to encourage innovative studies on LSDs, including Fabry disease, alpha-mannosidosis, and cystinosis. Such initiatives foster cross-disciplinary and transnational collaboration, aiming to expand understanding and improve patient management.

Asia Pacific Lysosomal Storage Disease Therapeutics Market Trends

Asia Pacific is anticipated to witness rapid growth with an estimated CAGR of 9.5% over the forecast period 2025-2032. The regional lysosomal storage disease therapeutics market growth is being driven by increasing awareness, evolving healthcare infrastructure, and government-led initiatives across key countries. In India, LSDs are recognized as multi-systemic disorders, with neurological involvement reported in approximately 70% of cases. Studies indicate Gaucher disease as the most prevalent (32%) among North Indian cohorts, followed by mucopolysaccharidoses (MPS) at 20%, while GM2 gangliosidosis is more frequent in southern India.

Recognizing the unmet need, the Indian Council of Medical Research (ICMR) and Department of Health Research (DHR) established a task force in 2015, leading to characterization of common LSDs, founder variants, and genotype–phenotype correlations. Government initiatives, including multicenter collaborative research projects and the drafting of the National Policy for Treatment of Rare Diseases, aim to improve diagnosis, management, and access to therapies.

In China, the LSD therapeutics landscape is advancing with domestically developed enzyme replacement therapies. In November 2024, CANbridge Pharmaceuticals’ CAN103 (velaglucerase-beta) received NDA acceptance from the Chinese NMPA for Gaucher disease types I and III. Branded as Gaurunning, it represents the first locally developed ERT, now clinically available for adolescents and adults, providing a long-term treatment option with broader indications compared to existing therapies.

Competitive Landscape

The global lysosomal storage disease therapeutics market is highly competitive, with key players including Shire, Sanofi, Takeda, Chiesi, Denali Therapeutics, Sangamo Therapeutics, JCR Pharma, and Azafaros, actively engaged in enzyme replacement, gene therapy, and innovative CNS-targeted solutions. The presence of multiple regional players, research collaborations, and orphan drug developers further intensifies competition, reflecting a market driven by innovation and niche specialization.

Key Industry Developments

- In September 2025, Medipal and JCR co-develop JR-479 for GM2 gangliosidosis via J-Brain Cargo platform; Medipal handles global development (excluding Japan) while JCR leads commercialization in Japan.

- In July 2025, Azafaros initiates two global Phase 3 trials with Nizubaglustat for Niemann-Pick Type C and GM1/GM2 gangliosidoses, first patient dosed in pivotal studies for rare LSDs.

- In May 2025, Azafaros raises €132M Series B to fund Nizubaglustat Phase 3 trials and expand its LSD pipeline; asset holds US/Europe Orphan Drug and US Fast-track designations.

Companies Covered in Lysosomal Storage Disease (LSD) Therapeutics Market

- Polaryx Therapeutics

- M6P therapeutics

- Sanofi

- Denali Therapeutics

- ZYTHERA

- BioMarin

- Sangamo Therapeutics, Inc

- JCR Pharmaceuticals Co., Ltd.

- Takeda Pharmaceutical Company Limited

- Azafaros B.V.

- CIBER & JUMISC

- Gain Therapeutics, Inc.

- Chiesi Group

- Amicus Therapeutics

- CANbridge Life Sciences Ltd.

- Beijing GeneCradle Technology Co., Ltd.

- GC Biopharma

Frequently Asked Questions

The global lysosomal storage disease (LSD) therapeutics market is projected to reach US$ 9.8 billion in 2025.

Rising prevalence of LSDs, unmet medical needs, and advancements in enzyme replacement, gene therapies, and CNS-penetrant drug delivery technologies are driving the market.

The market is poised to witness a CAGR of 7.7% between 2025 and 2032.

Expanding LSD pipeline, development of next-generation ERTs, gene therapies, CNS-targeted treatments, and growing research collaborations and grant initiatives across North America, Europe, and Asia Pacific offer lucrative opportunities.

Major market players include Chiesi Group, Takeda Pharmaceutical Company Limited, Polaryx Therapeutics, M6P therapeutics, and Sanofi, among others.