- Medical Devices

- Intraoperative Imaging Market

Intraoperative Imaging Market Size, Trends, Share, Growth, and Regional Forecast, 2026 to 2033

Intraoperative Imaging Market by Component (Systems, Software & Services), Application (Oncology, Neurosurgical Intervention, Orthopedic Procedures, Cardiovascular Intervention, Others), End-user, and Regional Analysis from 2026 to 2033

Intraoperative Imaging Market Share and Trends Analysis

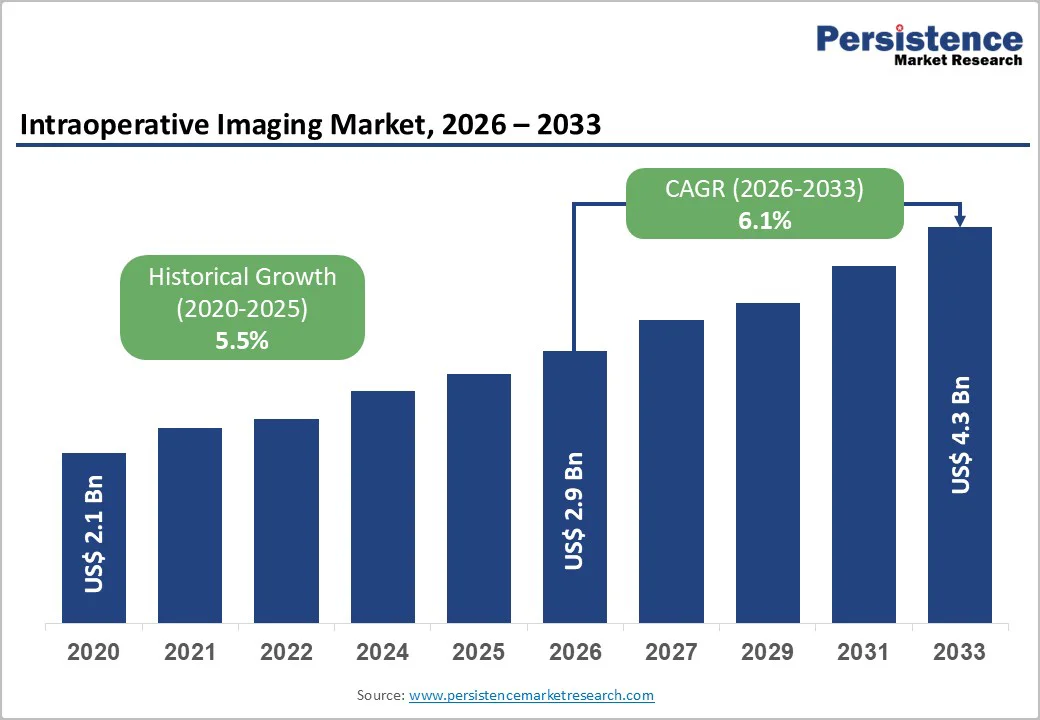

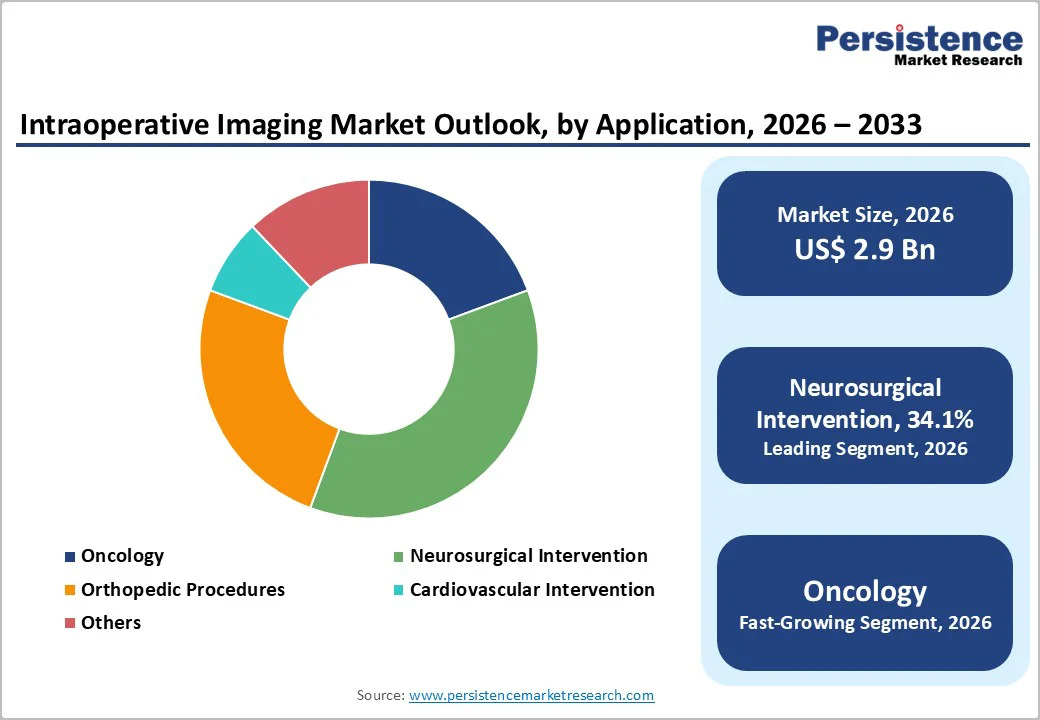

The global intraoperative imaging market size is estimated to reach US$2.9 billion in 2026 and is projected to reach US$ 4.3 billion by 2033, growing at a CAGR of 6.1% between 2026 and 2033.

The global market is witnessing robust growth, driven by increasing demand for real-time imaging during complex surgical procedures. Advanced systems such as intraoperative MRI, CT, ultrasound, and mobile C-arms are being integrated into operating rooms to enhance surgical precision, reduce complications, and improve patient outcomes.

Technological innovations, including AI-assisted navigation, hybrid operating suites, and multi-modality platforms, are expanding clinical applications across neurosurgery, oncology, orthopedics, and cardiovascular interventions. Growing healthcare expenditure, high prevalence of chronic and surgical conditions, and adoption in both developed and emerging markets are further accelerating market expansion worldwide.

Key Industry Highlights:

- Leading Region: North America dominates the global market, accounting for 35.2%, driven by advanced surgical infrastructure, high adoption of image-guided procedures, strong reimbursement, and widespread hybrid OR integration.

- Fastest-Growing Region: The Asia Pacific market is expected to grow rapidly with a CAGR of 7.7% in the forecast period, fueled by rising cancer and trauma surgeries, expanding hospital investments, medical tourism, and rapid adoption of minimally invasive techniques.

- Leading Component: Mobile C-arm lead within the systems category with 31.8% share, supported by versatility, lower cost than fixed systems, high usage in ortho and trauma, and easy integration into existing ORs.

- Leading Application: Neurosurgical Intervention to remain dominant with 34.1%, driven by demand for precision in brain and spine procedures, growing use of iMRI/CT, and navigation-assisted tumor resections.

- Leading End-user: Hospitals lead with a 42.7% share, driven by higher patient volumes, complex surgeries requiring intraoperative imaging, the availability of hybrid ORs, and strong capital budgets for advanced systems.

- AI-integrated intraoperative imaging is growing rapidly as surgeons adopt real-time anatomy mapping, automated margin detection, and workflow optimization to enable precision surgery.

- Hybrid OR expansion accelerates adoption, driven by hospitals integrating imaging with surgical workflows for cardiovascular, neuro, and oncology interventions.

- Ambulatory surgical centers (ASCs) are showing strong uptake of compact imaging systems, driven by increasing orthopedic day surgeries, lower operating costs, and a preference for mobile C-arms.

| Key Insights | Details |

|---|---|

| Global Intraoperative Imaging Market Size (2026E) | US$ 2.9 Billion |

| Market Value Forecast (2033F) | US$ 4.3 Billion |

| Projected Growth (CAGR 2026 to 2033) | 6.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.5% |

Market Dynamics

Driver - Technological Advancements and Integration Boost Global Intraoperative Imaging Adoption

Rapid technological advancements and the growing adoption of advanced imaging systems in surgical procedures are propelling the global intraoperative imaging market. Manufacturers are increasingly focusing on developing systems that are highly mobile, compact, user-friendly, and capable of providing comprehensive coverage. These innovations allow surgeons to perform complex procedures with improved accuracy and reduced operative time.

Additionally, companies are leveraging promotional strategies such as product demonstrations and trial offers to familiarize hospitals with new platforms, thereby driving adoption. Strategic collaborations and partnerships between imaging solution providers and device manufacturers are further enhancing the clinical utility of these systems by integrating complementary technologies.

For example, in February 2024, USA-based IMRIS, Deerfield Imaging, received FDA clearance for its ceiling-mounted InVision 1.5 Surgical Theatre, enabling real-time intraoperative MRI visualization and enhanced neurosurgical precision. In a separate collaboration, IMRIS and Insightec integrated focused-ultrasound systems within the InVision Surgical Theatres, expanding hospital capabilities for neurological interventions such as essential tremor and Parkinson’s disease.

Increasing adoption of intraoperative devices, such as magnetic resonance imaging (MRI), computed tomography (CT), and ultrasound, for tumor resections and other complex surgeries is further driving demand. Overall, ongoing innovation and system integration are expected to continue fueling growth across the intraoperative imaging market.

Restraints - High Costs and Regulatory Challenges Limit Market Expansion

Despite strong growth, the global intraoperative imaging market faces several challenges that could hinder its expansion. The high capital investment required for advanced imaging systems such as ceiling-mounted MRI, mobile C-arms, or integrated hybrid OR suites limits adoption, particularly among small and mid-sized hospitals.

Additionally, operational costs, including maintenance, staff training, and infrastructure upgrades, can be prohibitive. Regulatory approvals for new imaging technologies vary across regions, causing delays in product launches and commercialization. Integration of multiple imaging modalities into existing surgical workflows can also be complex, often requiring extensive staff retraining and temporary workflow disruptions.

Moreover, concerns related to radiation exposure in CT-based intraoperative systems, as well as compatibility issues with certain surgical instruments, may further restrain utilization. In emerging markets, limited healthcare budgets and a lack of insurance coverage for high-end procedures can restrict widespread adoption. Collectively, these financial, operational, and regulatory hurdles pose challenges to market growth, and addressing them will be critical to the sustained expansion of intraoperative imaging technologies.

Opportunity - AI and Real-Time Imaging Enable Enhanced Surgical Precision and Workflow Efficiency

The global intraoperative imaging market presents significant opportunities driven by increasing adoption of AI, real-time imaging, and system integration across diverse surgical procedures. AI-enabled platforms that convert standard 2D fluoroscopic X-rays into high-resolution 3D volumes are enhancing intraoperative visualization and surgical navigation while potentially reducing radiation exposure, costs, and operative time.

Real-time mobile MRI and high-resolution imaging systems are facilitating precise interventions in neurosurgery, orthopedics, and minimally invasive procedures, improving patient safety and surgical outcomes. Lightweight, MR-compatible stabilization devices, such as the DORO LUCENT® iMRI Cranial Stabilization Set, enable flexible coil positioning and compatibility with multiple image-guided systems, streamlining workflow and expanding clinical indications.

In 2025, companies such as See All AI secured funding to scale AI-powered 3D visualization platforms, while Body Vision Medical received regulatory approval in India for its LungVision system, supporting real-time tumor navigation in bronchoscopic procedures. Such innovations provide opportunities for hospitals to improve procedural efficiency, expand service offerings, and adopt precision-guided interventions. Overall, leveraging AI, mobile systems, and integrated imaging solutions represents a promising avenue for growth and enhanced surgical outcomes across the global intraoperative imaging market.

Category-wise Analysis

By Component Insights

Systems dominate the global intraoperative imaging market, with mobile C-arms projected to hold 31.8% of segment share in 2026. Their portability, ease of use, and multi-procedure applicability make them highly preferred across surgical specialties. Intraoperative CT systems are expected to grow the fastest, driven by demand for real-time 3D imaging and accurate tumor localization. Manufacturers are focusing on compact, high-resolution, and AI-enabled platforms to improve workflow efficiency and procedural precision. Continuous technological innovation and integration across imaging modalities are key drivers of the segment’s global dominance.

By Application Insights

Neurosurgical interventions are expected to account for approximately 34.1% of the global intraoperative imaging market in 2026. This dominance is driven by the critical need for real-time visualization during complex brain and spine surgeries. Imaging systems such as intraoperative MRI, CT, and ultrasound enhance surgical accuracy, reduce operative time, and minimize complications. Technological innovations, including AI-assisted navigation and hybrid operating suites, further support precision neurosurgery. The high prevalence of neurological disorders, rising surgical volume, and growing adoption of minimally invasive procedures drive sustained growth in the neurosurgical application segment.

By End-user Insights

Hospitals are projected to account for nearly 42.7% of the global intraoperative imaging market in 2026, driven by their advanced infrastructure, surgical volume, and capability to invest in cutting-edge imaging technologies. They adopt intraoperative MRI, CT, and ultrasound systems to enhance precision in oncology, neurosurgery, and orthopedic procedures. Larger healthcare facilities benefit from integrated hybrid operating suites, AI-enabled workflow management, and multi-modality imaging. Increasing patient demand for minimally invasive surgeries, higher procedural efficiency, and improved outcomes reinforce hospitals as the leading end-users of intraoperative imaging systems globally.

Regional Insights and Trends

North America Intraoperative Imaging Market Trends

North America is poised to dominate the global intraoperative imaging market, capturing 35.2% share by 2026, primarily due to the region’s advanced healthcare infrastructure, strong regulatory support, and high adoption of cutting-edge surgical technologies. Leading hospitals and pediatric health systems are investing heavily in hybrid operating suites. For instance, in March 2023, Children’s Minnesota launched the nation’s first pediatric hybrid intraoperative MRI suite, combining a moving-scanner and a moving-patient MRI system to enable real-time brain and spine imaging. This innovation enhances surgical decision-making, reduces repeat procedures, and improves outcomes in tumor, epilepsy, and trauma surgeries.

Additionally, IMRIS Imaging received FDA 510(k) clearance in August 2025 for its ceiling-mounted InVision 3T Recharge Operating Suite, which offers faster intraoperative scans, AI-enabled protocols, and improved imaging quality. Further, the introduction of new billing and reimbursement codes, such as the CPT Category III code granted to Lumicell’s fluorescence imaging system in 2024, is encouraging broader adoption across surgical oncology procedures. Overall, continuous technological advancements, regulatory facilitation, and infrastructure readiness are driving the robust growth of the North American intraoperative imaging market.

Europe Intraoperative Imaging Market Trends

Europe is expected to hold 28.3% of the global intraoperative imaging market by 2026, driven by technological innovation, high-quality healthcare systems, and increasing adoption of advanced intraoperative imaging devices. Manufacturers are introducing mobile, hybrid, and user-friendly platforms that enable precision-guided surgeries across neurosurgery and endovascular procedures. For example, in February 2025, Germany’s Ziehm Imaging unveiled the Vision RFD Hybrid Edition at a European conference in Austria, integrating CT-based planning, real-time fluoroscopy, and image fusion into a mobile C-arm. This innovation improves surgical accuracy, minimizes radiation exposure, and allows efficient use of OR space.

Additionally, in October 2025, Italy-based Esaote launched its I-Genius intraoperative MRI system at a neurosurgery congress in Vienna. The open-MRI design enables real-time imaging during glioma surgery without moving patients, reducing operating time and improving tumor resection accuracy. Collectively, Europe’s focus on clinical precision, compact system designs, and integration of real-time imaging solutions is accelerating adoption, positioning the region as a key growth hub for intraoperative imaging technologies.

Asia Pacific Intraoperative Imaging Market Trends

Asia Pacific is expanding rapidly, projected to grow at a CAGR of 7.7% over the forecast period. The growth is fueled by rising healthcare expenditure, increasing prevalence of cancer and neurological disorders, and adoption of advanced imaging devices in surgical workflows.

Hospitals in India, China, and other emerging markets are investing in cost-effective and high-precision imaging systems to enhance surgical outcomes. For instance, in June 2024, India’s Tata Memorial Centre installed the country’s first advanced intraoperative ultrasound (bKActiv) system for complex brain-tumor surgeries, providing real-time tumor visualization and navigation support as a resource-efficient alternative to MRI.

IIT Delhi inaugurated a dedicated MRI research facility in July 2025, equipped with a 1.5 Tesla clinical-grade scanner to foster AI-based imaging protocols, device development, and hands-on training with innovative objectives. These initiatives reflect the growing emphasis on integrating intraoperative imaging into routine clinical practice. Overall, the combination of technological advancement, growing clinical need, and infrastructure investment is expected to drive strong market growth in the Asia Pacific region.

Competitive Landscape

The global intraoperative imaging market is highly competitive, characterized by rapid technological innovation, continuous product launches, and integration of AI and multi-modality systems. Market players focus on enhancing imaging precision, mobility, and workflow efficiency while forming strategic collaborations to expand clinical applications. Regional adoption varies based on infrastructure, regulatory support, and healthcare spending, driving both growth and differentiation.

Key Industry Developments:

- In February 2025, A USA-based firm, Grovecourt Capital Partners, announced its acquisition of IMRIS to strengthen the company’s growth trajectory. The deal supports expansion of IMRIS’s intraoperative MRI solutions, enhances technology development for advanced neurosurgical applications, and positions the company for broader global adoption across high-acuity surgical environments.

- In March 2024, Global medical-technology firm Siemens Healthineers unveiled the fully automated self-driving C-arm system CIARTIC Move, cleared by the FDA. The motorized C-arm enables remote-controlled imaging, slashes intraoperative imaging time by about 50%, and reduces staff burden, enhancing workflow efficiency across spine, trauma, pelvic, and general surgeries.

Companies Covered in Intraoperative Imaging Market

- GE Healthcare

- Koninklijke Philips N.V.

- Medtronic PLC

- Siemens Healthineers AG

- IMRIS Imaging, Inc.

- Carl Zeiss Meditec AG

- Activ Surgical

- Serac Imaging Systems Ltd.

- Brainlab SE

- Esaote SPA

- Corin Group

- HYPERFINE, INC.

- Taumedis

- Halomedicals

- 3D Systems, Inc.

- Probo Medical

Frequently Asked Questions

The global intraoperative imaging market is projected to be valued at US$ 2.9 Billion in 2026.

Adoption of advanced imaging systems and AI integration enhances surgical precision and workflow efficiency drive market growth.

The global market is poised to witness a CAGR of 6.1% between 2026 and 2033.

Expansion of real-time imaging, AI-assisted navigation, and hybrid OR solutions across surgical specialties presents major growth opportunities.

Major players in the global are GE Healthcare, Koninklijke Philips N.V., Medtronic PLC, Siemens Healthineers AG, IMRIS Imaging, Inc., Carl Zeiss Meditec AG, and others.