- Medical Devices

- Insulin Delivery Device Market

Insulin Delivery Device Market Size, Share, and Growth Forecast, 2025 - 2032

Insulin Delivery Device Market By Device Type (Insulin Pens, Insulin Pumps, Insulin Pen Needles, Insulin Syringes, Other Delivery Devices), Disease Type (Type 1 Diabetes, Type 2 Diabetes), End-user (Hospitals & Clinics, Homecare), and Regional Analysis for 2025 - 2032

Insulin Delivery Device Market Share and Trends Analysis

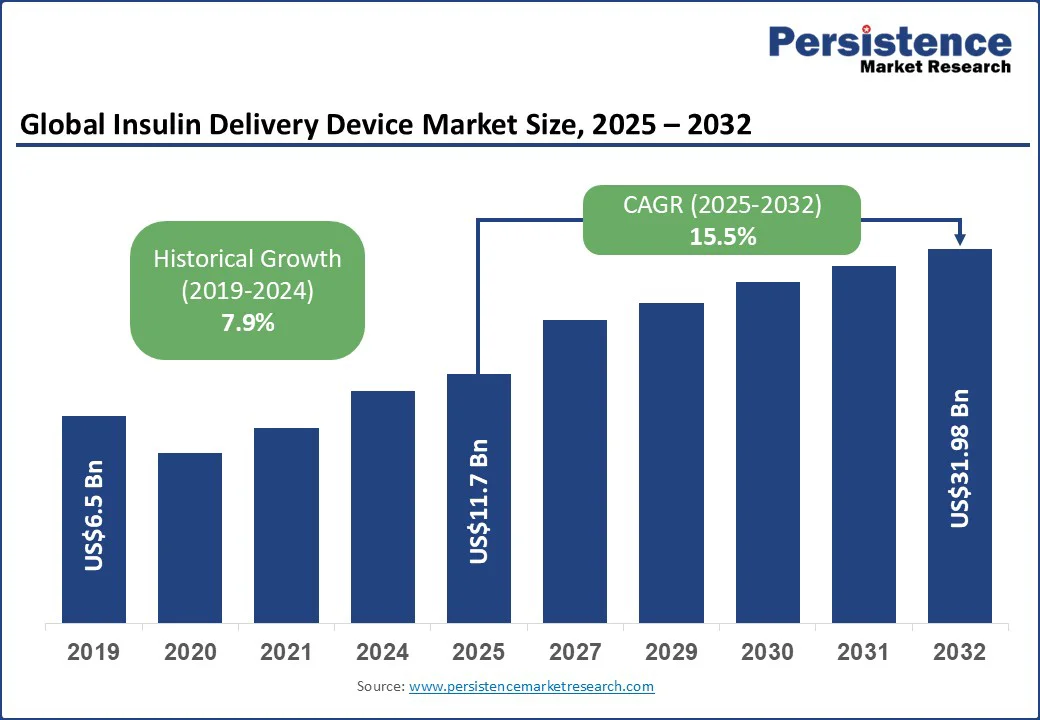

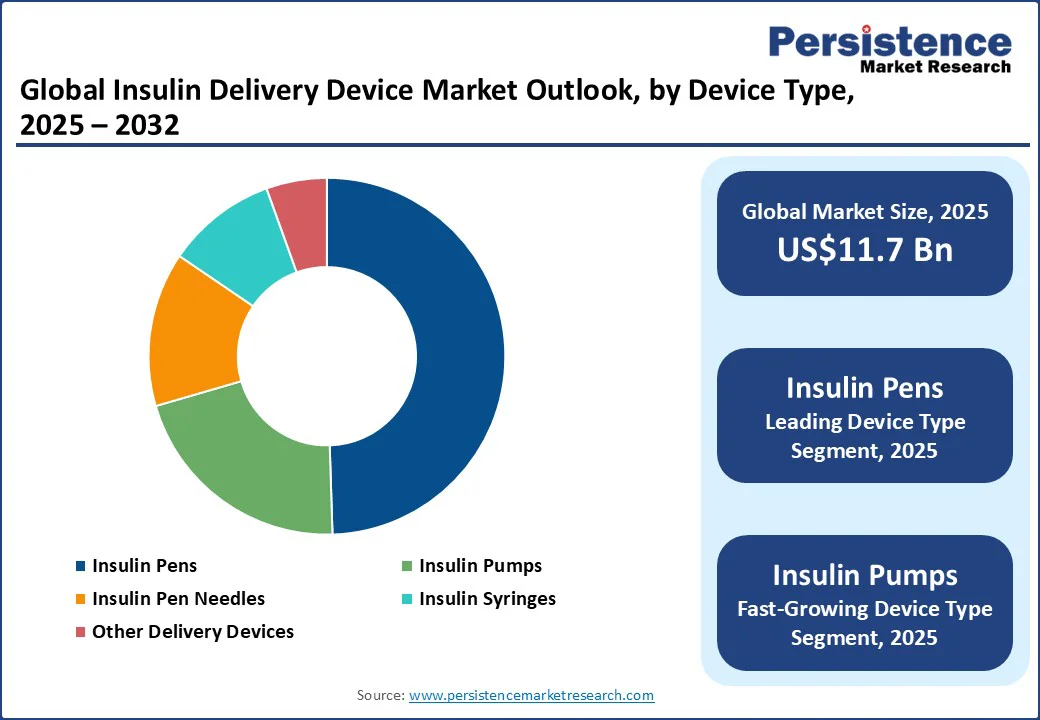

The global insulin delivery device market size is likely to be valued at US$11.7 Bn in 2025 and reach US$31.98 Bn by 2032, growing at a CAGR of 15.5% during the forecast period from 2025 to 2032.

The insulin delivery device industry is growing, driven by the rising global burden of diabetes, innovations in automated insulin delivery, and the increasing adoption of connected smart pens and wearable pumps.

Insulin is a hormone essential for regulating blood sugar levels, particularly among individuals with type 1 and type 2 diabetes. Insulin delivery devices, which include pens, pumps, syringes, and smart patch systems, deliver precision and ease of use to diabetics.

Recent developments by both public and private players signal a marked shift toward AI-powered, app-integrated insulin technologies. Opportunities are also emerging in underserved markets as companies such as Novo Nordisk phase out human insulin pens, creating a sizeable demand for affordable alternatives.

The introduction of Bluetooth-enabled insulin pens and tubeless patch pumps, along with improved access to advanced insulin delivery systems through expanding insurance coverage for diabetic patients, is paving new pathways for stakeholders.

Key Industry Highlights:

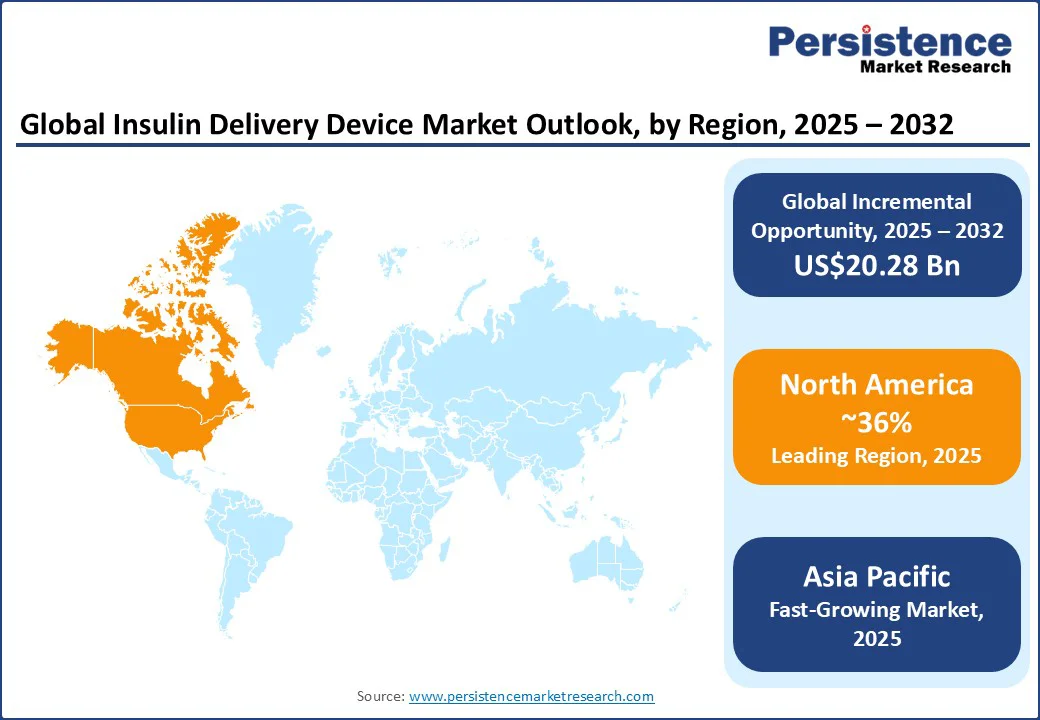

- Leading Region: North America is projected to hold a 36% share in the insulin delivery device market in 2025, driven by the widespread prevalence of diabetes and its anticipated continued growth in the coming years.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing market through 2032, driven by a surging diabetes incidence in India and China, along with active healthcare digitization and improved affordability through government-led initiatives.

- New Product Launches: The introduction of advancements such as closed-loop systems, smartphone-integrated insulin trackers, and patient-friendly patch pumps is enhancing user experience and driving the market toward greater automation.

- Leading End-user: The homecare segment is anticipated to hold the largest revenue share of approximately 51% in 2025, primarily driven by a shift toward self-administered insulin therapies and digital health integration in insulin delivery devices.

- Dominant Device Type: Insulin pens are projected to dominate the device type segment in 2025, capturing nearly 50% of market share, owing to their ease of use, precision, and wide availability across emerging and developed markets.

|

Global Market Attribute |

Key Insights |

|

Insulin Delivery Device Market Size (2025E) |

US$11.7 Bn |

|

Market Value Forecast (2032F) |

US$31.98 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

15.5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

7.9% |

Market Dynamics

Driver - Rising Prevalence of Diabetes Worldwide and the Advent of Digital Therapies

The insulin delivery device market is growing on account of the surge in diabetes prevalence worldwide and the convergence of digital therapeutics with insulin administration. As per the International Diabetes Federation (IDF), the number of diabetics worldwide is set to reach over 643 million by 2030, with the sharpest spike likely to be observed in low- and middle-income countries.

This epidemiological analysis is forcing a shift from conventional insulin syringes to more advanced, connected insulin delivery devices such as smart pens and automated insulin pumps. Two notable examples reflecting this shift include the 2024 rollout of hybrid closed-loop artificial pancreas systems by the National Health Service (NHS) in the U.K. and Insulet’s global expansion of its wearable Omnipod 5, which is FDA approved for both type 1 and type 2 diabetes.

Restraint - Inherent Device Complexities and Limited User Proficiency

Even though insulin delivery devices are becoming increasingly sophisticated, the learning curve for patients, particularly elderly users or those with limited exposure to new technologies, is steep and has emerged as a significant barrier to the adoption of these devices. For example, studies published in Diabetes Technology & Therapeutics show that more than 40% of geriatric adults experience difficulties managing insulin pumps and connected pens due to digital interface fatigue, dexterity issues, or a lack of caregiver support.

While companies such as Medtronic and Novo Nordisk are taking substantial efforts in developing user-centric insulin pen designs and simplified hybrid closed-loop systems, many patients still report anxiety over setting basal rates, interpreting continuous glucose monitor (CGM) data, or managing device alarms.

This usability gap has slowed the acceptance of such technologies in both high- and middle-income economies, despite their growing availability, and has led to the underutilization of advanced diabetes management solutions such as smart insulin pens, automated insulin delivery systems, and patch-based pumps.

Opportunity - Rising Demand for AI-Integrated, Tubeless Insulin Delivery in Emerging Markets

AI-enabled dosing technologies, combined with growing demand for tubeless, wearable insulin pumps in emerging markets, present highly attractive opportunities for insulin delivery device makers. With the incidence of diabetes soaring in large economies (India alone projected to be home to over 100 million diabetic patients by 2045 (IDF)), these regions are moving on from traditional insulin administration methods in favor of compact, discreet solutions such as patch pumps and smart insulin pens with dose-tracking apps.

Insulet’s Omnipod 5, the first FDA-cleared tubeless hybrid closed-loop system, for instance, is now being piloted for type 2 diabetes management and provides a scalable model for health systems with poor infrastructure. Simultaneously, firms such as Biocorp and Novo Nordisk are partnering to integrate connected pen technology with AI-based insulin titration platforms, paving the way for adaptive, personalized care.

With smartphone penetration and telehealth access rapidly expanding in developing economies, manufacturers that localize production, optimize pricing, and bundle connected insulin delivery systems with mobile glucose monitoring tools will be well-positioned to capture untapped market opportunities and improve therapeutic outcomes in previously underserved populations.

Category-wise Analysis

Device Type Insights

Insulin pens are expected to dominate with an estimated 49.4% market share in 2025. The key factors driving the growth of these devices are their ease of use, accurate dosing, and extensive adoption among both type 1 and type 2 diabetes patients. Unlike traditional syringes, insulin pens offer a more convenient and discreet delivery method, significantly improving patient compliance.

The growing interest in smart insulin pens by top medical device manufacturers, such as Medtronic’s InPen and Eli Lilly’s Tempo, puts into the spotlight a broader industry shift toward digitally-enabled diabetes management solutions. These pens are equipped with Bluetooth connectivity, dose tracking features, and real-time integration with CGMs, making them essential tools in personalized insulin therapy.

Insulin pumps are poised to grow the fastest through 2032, fueled by a rising demand for automated and tubeless insulin delivery systems. Both patients and providers are showing an increasing inclination toward hybrid closed-loop pumps that adjust insulin doses based on real-time CGM data, almost eliminating the need for manual insulin management.

End-user Insights

The home care segment is anticipated to hold the largest revenue share of approximately 51% in 2025, primarily driven by a shift toward self-administered insulin therapies and the integration of digital health in insulin delivery devices. The increasing availability of smart insulin pens, wearable patch pumps, and app-enabled glucose monitoring tools has empowered patients to manage diabetes from the comfort of their homes with greater accuracy and convenience.

This adoption is particularly strong in regions with well-developed telehealth infrastructure and higher purchasing power, such as North America and Western Europe. As the demand for AI-enabled insulin devices, remote insulin monitoring, and personalized home insulin delivery systems continues to grow, home care is emerging as a central pillar in the evolving insulin therapy ecosystem.

The hospitals and clinics segment is set to experience the fastest growth rate through 2032, as healthcare facilities increasingly adopt advanced insulin delivery technologies to support inpatient administration and meet the needs of newly diagnosed patients. Hospitals are critical touchpoints for initiating advanced insulin delivery systems, such as hybrid closed-loop insulin pumps, especially for patients with type 1 diabetes who require specialized onboarding.

Government-backed rollouts, such as the NHS’s implementation of artificial pancreas systems in hospitals across the U.K., highlight the central role played by traditional healthcare facilities and institutions in mainstreaming next-generation insulin devices.

Regional Insights

North America Insulin Delivery Device Market Trends

North America is set to lead, accounting for a 36% share in 2025, driven by the widespread prevalence of diabetes in the region. Advanced healthcare infrastructure and high consumer acceptance of digital health technologies are two other important growth determinants. With over 38 million adults in the U.S. living with diabetes, there is a growing reliance on smart insulin delivery solutions, such as connected insulin pens, wearable insulin pumps, and closed-loop systems that integrate with CGMs.

Global players in the medical device industry, such as Medtronic, Insulet, and Tandem Diabetes Care, are investing in AI-powered dosing tools and remote patient management platforms, targeted toward the tech-savvy populations of North America. Furthermore, favorable insurance coverage and early technology adoption are also critical drivers that boost the demand for insulin delivery devices in the region.

Europe Insulin Delivery Device Market Trends

Europe is expected to maintain a strong presence in the insulin delivery device industry in 2025, driven primarily by well-established public healthcare systems and supportive patient reimbursement mechanisms. Countries such as Germany, the U.K., and the Netherlands are actively promoting next-gen technologies, including automated insulin delivery (AID) systems and smart insulin pens.

Public initiatives, such as the NHS’s pioneering introduction of hybrid closed-loop systems across healthcare facilities in the U.K. in 2024, are proving to be indispensable drivers of market growth. Adding to these factors is the region's rising diabetes population.

According to the World Health Organization (WHO), at present, there are 74 million diabetics in Europe, and by 2045, one-tenth of the European population will be suffering from diabetes. As a result, the demand for effective and user-friendly home-based insulin delivery devices is expected to skyrocket in the region over the coming years.

Asia Pacific Insulin Delivery Device Market Trends

Projected to showcase the fastest growth rate through 2032, the market in the Asia Pacific is poised to accelerate at an unprecedented pace, fueled by an increasing burden of diabetes in China and India. Data analysis from the Global Burden of Disease (GBD) 2021 study found that India has the highest diabetes mortality burden, with more than 331,000 deaths, followed by China, where diabetes-related deaths stood at 178,475.

Rapid urbanization and increased access to mobile health technology are driving demand for affordable insulin pumps, Bluetooth-enabled pens, and telehealth-integrated platforms. Recognizing the potential of Asia Pacific, international medical device players are customizing products to fit regional and local preferences, while governments are rolling out nationwide diabetes control programs, such as India’s National Program for Prevention and Control of Non-Communicable Diseases (NP-NCD).

Competitive Landscape

The global insulin delivery device market is highly competitive, driven by intense product innovation among leading players, as well as strategic partnerships and reimbursement strategies. Some of the strongest market competitors differentiate themselves through the development and marketing of hybrid closed-loop systems, smart pen-software integrations, and remote dosing platforms.

For instance, Embecta Corporation’s push to pair Tidepool’s AID algorithm with its syringes and pen needles demonstrates how collaborations can fast-track the shift to automated insulin delivery systems. Other medical device giants such as Medtronic, Insulet, and Tandem Diabetes Care are advancing next-generation pumps such as MiniMed?780G and Omnipod?5. The aim is to weave together CGM-integrated insulin pumps, AI-based insulin dosing, and wearable patch systems to secure the confidence of payers, which in turn will help them strengthen their market position.

Key Industry Developments:

- In July 2025, Medtronic’s MiniMed 780G system received expanded CE mark approval in Europe for use in children aged two years and older, pregnant women, and Type 2 diabetes patients, backed by improved HbA1c and glucose control data.

- In June 2025, Insulet presented new data on its Omnipod 5 AID system at the American Diabetes Association’s Scientific Sessions, noting that over 30% of new users in the first quarter were patients with Type 2 diabetes, following expanded FDA approval and growing provider interest.

- In June 2025, Tandem Diabetes Care partnered with Abbott to integrate its insulin delivery systems with Abbott’s upcoming dual glucose-ketone sensor, aiming to enhance real-time monitoring and prevent diabetic ketoacidosis through earlier ketone detection.

Companies Covered in Insulin Delivery Device Market

- Novo Nordisk A/S

- Medtronic plc

- Sanofi S.A.

- Eli Lilly and Company

- Insulet Corporation

- Tandem Diabetes Care, Inc.

- Ypsomed Holding AG

- Becton, Dickinson and Company

- F. Hoffmann-La Roche Ltd.

Frequently Asked Questions

The insulin delivery device market is projected to reach US$ 11.7 Bn in 2025.

The growing burden of diabetes globally and promising innovations in automated insulin delivery are driving the market.

The insulin delivery device market is anticipated to witness a CAGR of 15.5% from 2025 to 2032.

The increasing preference for compact, discreet solutions such as patch pumps and smart insulin pens with dose-tracking apps in emerging economies and the introduction of AI-powered dosing solutions are key market opportunities.

The key players in the insulin delivery device market include Novo Nordisk A/S, Medtronic plc, and Sanofi S.A.