- Pharmaceuticals

- Biosimilar Insulin Market

Biosimilar Insulin Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Biosimilar Insulin Market by Type of Synthesis (Insulin Glargine, Insulin Analog, Others), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), and Regional Analysis from 2026 to 2033

Biosimilar Insulin Market Size and Share Analysis

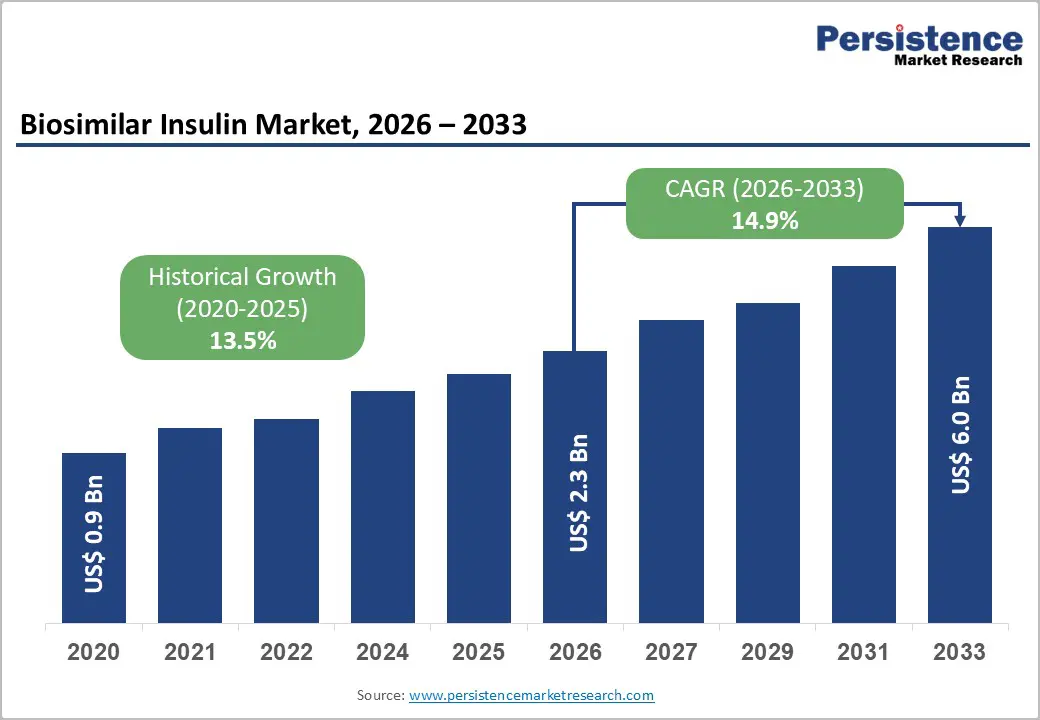

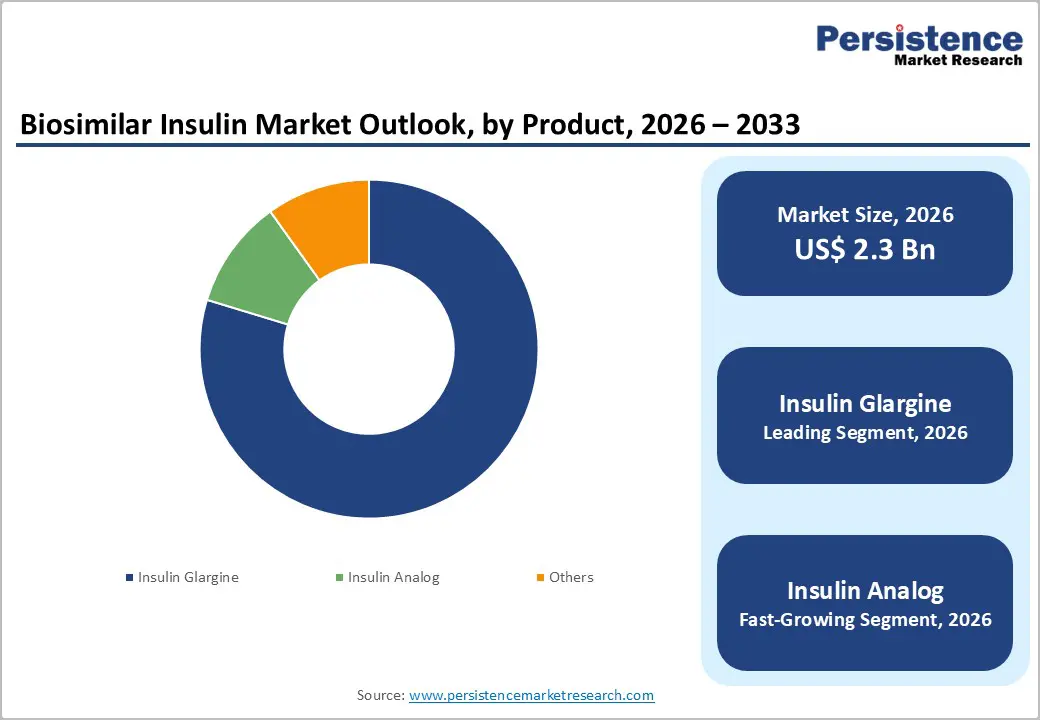

The global biosimilar insulin market is estimated to grow from US$ 2.3 Bn in 2026 to US$ 6.0 Bn by 2033. The market is projected to grow at a CAGR of 14.9% from 2026 to 2033.

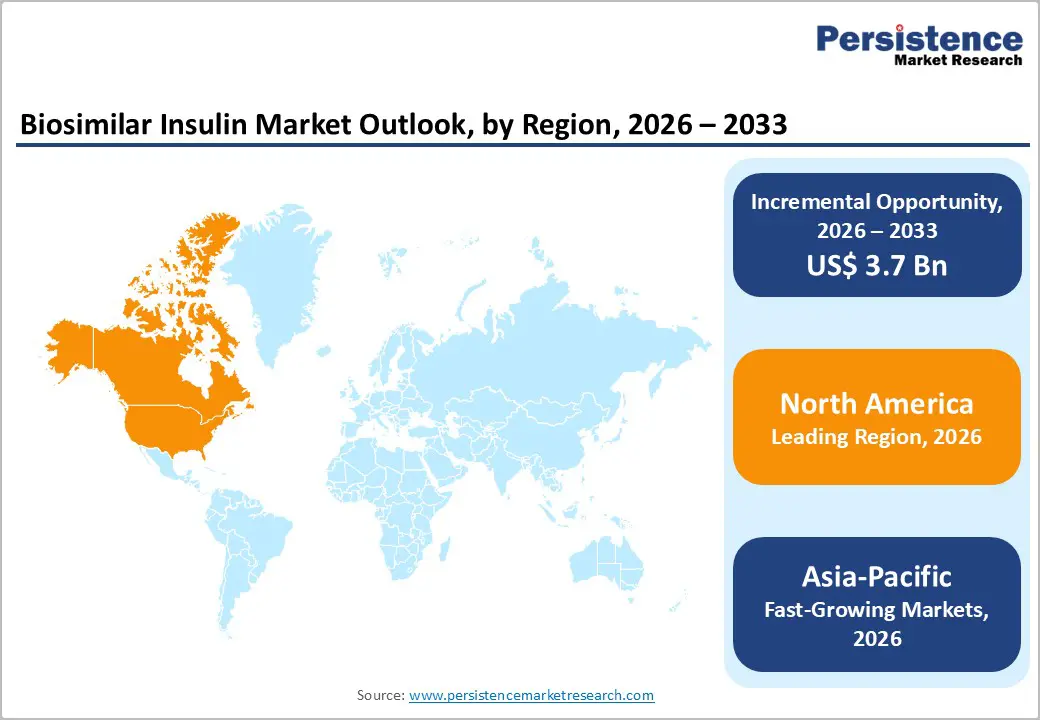

The global biosimilar insulin market is expanding steadily, driven by rising demand for generics, increased pharmaceutical production, and growing outsourcing. North America leads with advanced manufacturing, stringent regulations, and strong R&D investment. Asia-Pacific is the fastest-growing region, driven by cost advantages, expanding production capacity, government initiatives, and rising healthcare access and diabetes prevalence.

Key Industry Highlights

- Dominant Segment: Insulin Glargine led the biosimilar insulin market with a 79.7% share in 2025, driven by high demand for long-acting basal insulin in diabetes management, cost-effective alternatives to branded products, and the growing global prevalence of diabetes. Scalable manufacturing, regulatory-compliant production, and consistent efficacy enhanced adoption in hospitals, clinics, and retail pharmacies, supporting chronic disease treatment and market growth.

- Dominant Region: Europe held a significant share in the biosimilar insulin market, driven by advanced pharmaceutical manufacturing, supportive regulatory frameworks, strong healthcare infrastructure, increasing biosimilar adoption, and investments in R&D and production capacity.

- Market Drivers: Growth is driven by rising chronic disease prevalence, increased use of generics, outsourced API manufacturing, patent expirations, and demand for high-quality, regulatory-compliant APIs.

- Market Opportunities: Expansion in biologic and high-potency APIs, contract manufacturing, localized production, continuous manufacturing adoption, and rising demand from emerging pharmaceutical markets.

| Report Attribute | Details |

|---|---|

|

Biosimilar Insulin Market Size (2026E) |

US$ 2.3 Bn |

|

Market Value Forecast (2033F) |

US$ 6.0 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

14.9% |

|

Historical Market Growth (CAGR 2020 to 2025) |

13.5% |

Market Dynamics

Driver: Growing demand for cost-effective insulin therapies

The global diabetes burden is a major driver of demand for cost-effective insulin therapies. More than 537 million adults worldwide live with diabetes, a number projected to reach 643 million by 2030, placing immense pressure on healthcare systems to manage treatment costs. Biosimilar insulins are typically priced significantly lower than originator biologics; modeling studies estimate biosimilar insulin analogues could cost ≤$78–133 per patient annually, compared with much higher current retail prices. Reducing costs is crucial, as studies have documented that insulin treatment expenses in the United States can exceed $6,000 per person per year for branded analogues, contributing to affordability barriers.

Lower prices enhance access and adherence, particularly in publicly funded systems and low to middle-income countries, accelerating biosimilar adoption in clinics and pharmacies globally.

Restraints: Stringent regulatory approvals and complex compliance requirements

Despite policy advances, regulatory approval remains a key restraint for biosimilar insulin. Biosimilars must demonstrate high similarity to reference biologics in terms of safety, purity, and potency, which requires extensive analytical comparability and clinical data. Regulatory agencies such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) maintain rigorous standards that can lengthen development timelines. Although harmonized pathways have reduced average approval times by roughly 40% since 2018, significant scientific and regulatory hurdles persist.

These requirements increase development cost and complexity for manufacturers, particularly smaller firms, and contribute to slower market entry compared with small-molecule generics. Additionally, interchangeability and substitution policies vary by jurisdiction, which can limit the use of biosimilars in clinical practice even after regulatory approval.

Opportunity: Development of high-potency and long-acting insulin biosimilars

The development of high-potency and long-acting insulin biosimilars presents a significant opportunity to expand treatment options and reduce overall diabetes care costs. Long-acting analogues such as insulin glargine are widely used; Europe has approved multiple biosimilar glargine products, which have contributed to price reductions of up to ~21.6% across 28 countries following biosimilar entry.

New biosimilar products, including the first rapid-acting insulin aspart biosimilar approved in the U.S. in 2025, reflect expanding therapeutic categories and potential for broader clinical adoption.

As diabetes prevalence continues to rise globally, demand for efficacious, convenient dosing regimens and cost reductions will incentivize more manufacturers to develop potent and long-acting biosimilar analogues, improving access and competitive dynamics.

Category-wise Analysis

By Product, Insulin Glargine Dominates the Biosimilar Insulin Market

Insulin Glargine holds a 79.7% share of the global market in 2025, as it is the most widely prescribed basal insulin for diabetes management. Long-acting analogues comprise the majority of basal insulin use, and biosimilar glargine has rapidly expanded in both hospital and retail settings. Real-world data show that biosimilar glargine prescriptions accounted for a large share of long-acting insulin dispensing in community pharmacies by 2020, with some sites reporting biosimilars in up to 89% of insulin glargine dispensed in selected settings. This reflects strong uptake where biosimilars are established and trusted.

Hospitals in multiple countries have also increasingly adopted biosimilar glargine in formularies. The consistent need for basal insulin in type-1 and type-2 diabetes and cost pressures on healthcare systems further reinforce glargine’s leading position.

By Distribution Channel, Hospital pharmacies lead biosimilar insulin distribution through bulk procurement, clinical programs, cost control, and patient education

Hospital pharmacies dominate biosimilar insulin distribution because they serve as primary points of care for acute and complex diabetes management, ensuring timely access to insulin for both inpatient and early outpatient care. Hospital pharmacy channels often account for the largest share (around 50% or more of biosimilar insulin dispensed globally), driven by centralized procurement and bulk purchasing that enhances affordability and supply reliability. These pharmacies also support structured diabetes programs in which clinicians initiate and adjust insulin therapy, reinforcing biosimilar use through formal hospital treatment protocols.

In many regions, government and public health systems prioritize hospital procurement of biosimilars to contain costs and improve access. Additionally, hospital pharmacists play a key role in educating healthcare teams and patients about biosimilar safety and effectiveness, increasing confidence and prescription rates in clinical settings.

Regional Insights

Europe Biosimilar Insulin Market Trends

Europe has emerged as a dominant region in the global biosimilar insulin market, thanks to well-established regulatory frameworks and widespread support from healthcare systems that encourage biosimilar adoption. The European Medicines Agency (EMA) provides clear scientific guidance for biosimilar approval, facilitating market entry and clinician confidence in prescribing alternatives to originator insulins. In 2024, Europe accounted for about 29–35% of the global biosimilar insulin market share, driven by strong uptake in countries such as Germany, France, and the United Kingdom.

Hospitals and national health systems promote biosimilar prescribing to contain public healthcare costs and expand access; for example, biosimilar insulin glargine has been widely reimbursed under national formularies with active physician incentives. Additionally, price-containment policies and formal substitution guidelines in several EU member states have accelerated uptake and strengthened Europe’s leadership position.

North America Biosimilar Insulin Market Trends

North America remains a critically important region for biosimilar insulin because it combines a high diabetes burden with strong regulatory and payer frameworks that support biosimilar use. According to U.S. Centers for Disease Control and Prevention data, over 37 million Americans live with diabetes, creating significant demand for insulin therapies and cost-saving alternatives. The U.S. Food and Drug Administration (FDA) has established a biosimilar approval pathway, enabling multiple insulin biosimilars and interchangeable products to enter the market, including long-acting and rapid-acting analogues, which increases competition and affordability.

Public insurance programs like Medicare and Medicaid actively reimburse biosimilars and, through policies such as insulin cost caps for beneficiaries, reduce out-of-pocket expenses. Canada also contributes through provincial formulary decisions that prioritize biosimilars, thereby enhancing the regional market's importance. These factors position North America as both a high-value and rapidly expanding biosimilar insulin hub.

Asia-Pacific Biosimilar Insulin Market Trends

The Asia-Pacific region is the fastest-growing market for biosimilar insulin, underpinned by a rapidly rising prevalence of diabetes and expanding healthcare access. Countries such as China and India have some of the largest diabetic populations globally, fueling demand for affordable treatment options. In 2024, Asia-Pacific accounted for the fastest-growing region with growth outpacing other regions due to increasing local production capacity and supportive government policies aimed at improving drug affordability and access. Healthcare infrastructure improvements, expanding public health insurance coverage, and a growing middle class with better access to chronic disease care also accelerate uptake.

Local manufacturers in India and China are increasingly entering the biosimilar insulin market, boosting supply and driving competitive pricing across urban and rural markets. As regulatory frameworks mature and awareness grows, this region continues to attract investment and drive rapid adoption of biosimilar insulins.

Market Competitive Landscape

The biosimilar insulin market is highly competitive, led by key players such as Eli Lilly, Sanofi, Biocon, and Wockhardt. Companies focus on biosimilar insulin development, regulatory approvals, cost-effective manufacturing, and strategic collaborations to expand global reach, enhance market share, and meet rising demand in hospitals, retail, and emerging markets.

Key Industry Developments:

- In October 2025, Adocia and its partner Tonghua Dongbao announced that the Phase III clinical trial of BioChaperone® Lispro (THDB0206 injection) in adults with type 1 diabetes in China produced positive topline results. The randomized, multicenter study met its primary endpoint by showing that BioChaperone Lispro achieved non-inferior HbA1c reduction over 26 weeks compared with the standard therapy Humalog®

- In October 2025, Biocon Biologics Ltd. and U.S. nonprofit Civica, Inc. expanded their strategic collaboration to launch a private-label version of Insulin Glargine aimed at broadening treatment options for the 38.4 million Americans living with diabetes.

- In June 2025, Biocon Biologics’ Malaysian subsidiary, Biocon Sdn. Bhd., surpassed a major milestone by supplying over 100 million cartridges of recombinant human insulin to the Malaysian Ministry of Health, significantly expanding insulin access nationwide. This achievement enabled treatment for more than 345,000 diabetes patients and reinforced the company’s long-term commitment to affordable diabetes care in the country.

Companies Covered in Biosimilar Insulin Market

- Tonghua Dongbao

- Biocon Ltd.

- Julphar

- Denver Farma S.A.

- Eli Lilly and Company

- WOCKHARDT

- SEDICO Co.

- Sanofi SA

- Polfa Tarchomin S.A.

- Aristopharma Ltd.

- BIOTON S.A.

- Popular Pharmaceuticals Ltd

- Advanced Chemical Industries Limited

- Others

Frequently Asked Questions

The global biosimilar insulin market is projected to be valued at US$ 2.3 Bn in 2026.

Rising diabetes prevalence, demand for affordable insulin, patent expirations, and expanding biosimilar manufacturing drive growth.

The global biosimilar insulin market is poised to witness a CAGR of 14.9% between 2026 and 2033.

Opportunities include high-potency and long-acting insulin biosimilars, contract manufacturing, localized production, and emerging market demand.

Tonghua Dongbao, Biocon Ltd., Julphar, Denver Farma S.A., Eli Lilly and Company, WOCKHARDT.