- Pharmaceuticals

- Hemoglobinopathy Market

Hemoglobinopathy Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Hemoglobinopathy Market by Diagnostic Test (Routine Red Blood Cell (RBC) Count, Genetic Testing, Hemoglobin by High Performance Liquid Chromatography, Hemoglobin Isoelectric Focusing (Hb IEF), Hemoglobin Electrophoresis (Hb ELP), Hemoglobin Solubility Test), Indication, End-user, and Regional Analysis from 2026 - 2033

Hemoglobinopathy Market Share and Trends Analysis

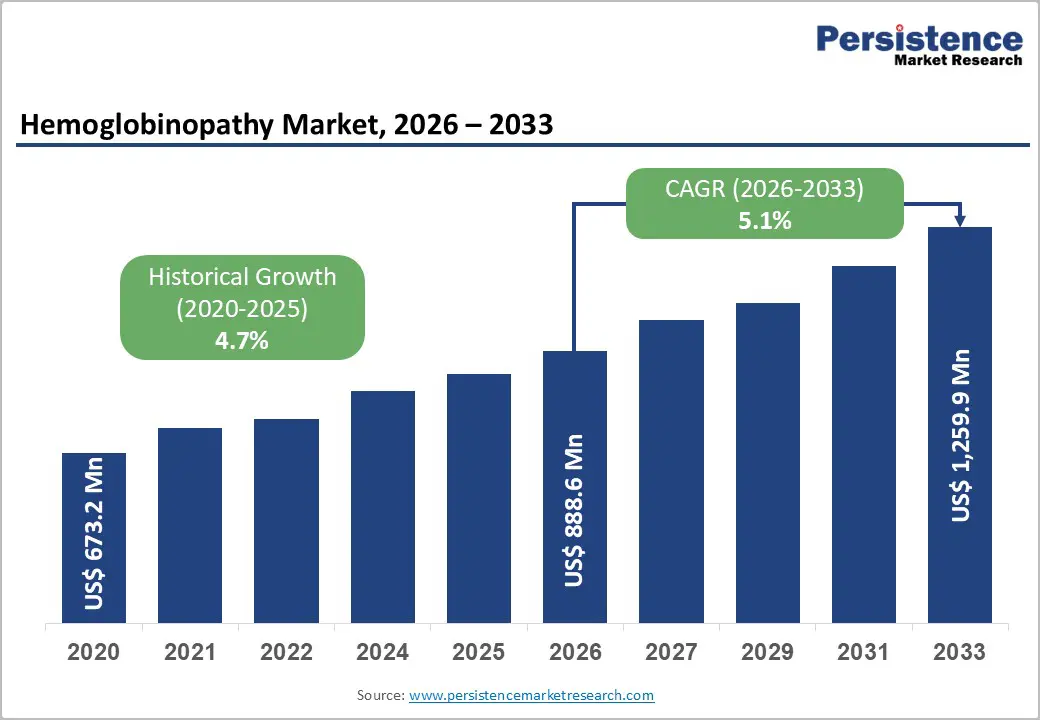

The global hemoglobinopathy market size is likely to value at US$ 888.6 million in 2026 and is projected to reach US$ 1,259.9 Million by 2033, growing at a CAGR of 5.1% between 2026 and 2033. The global market is expanding steadily, driven by the high prevalence of inherited blood disorders such as sickle cell disease, thalassemia, and other hemoglobin variants.

Rising adoption of newborn and prenatal screening programs, coupled with growing awareness of early detection benefits, is fueling demand for advanced diagnostic solutions. Techniques such as high-performance liquid chromatography (HPLC), electrophoresis, molecular genetic testing, and point-of-care assays are being increasingly deployed in hospitals, specialty labs, and research centers. With a focus on accuracy, rapid results, and early intervention, diagnostics play a critical role in guiding treatment decisions, reducing disease burden, and improving patient outcomes globally.

Key Industry Highlights:

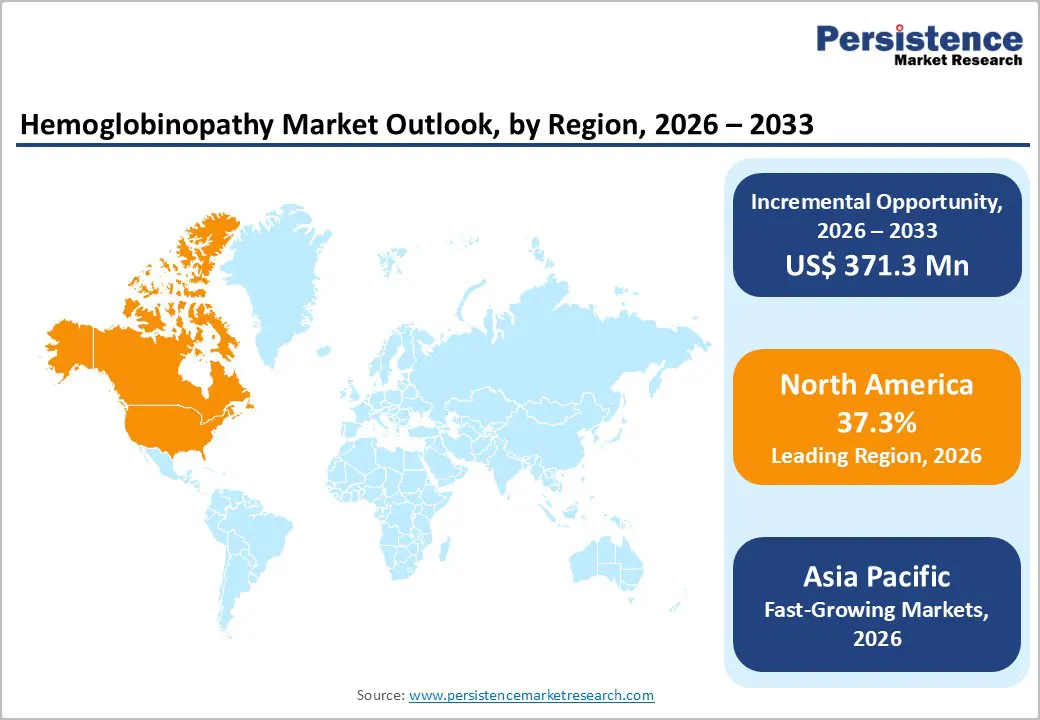

- Leading Region: North America dominates the global market with 37.3%, driven by advanced healthcare infrastructure, widespread newborn screening programs, strong reimbursement policies, and high adoption of molecular diagnostic technologies.

- Fastest-Growing Region: Asia Pacific market is expected to grow rapidly with a CAGR of 6.6% in forecast period, fueled by rising prevalence of hemoglobinopathies, improving diagnostic infrastructure, and increasing government-led screening initiatives.

- Leading Diagnostic Test: Routine Red Blood Cell (RBC) Count lead with 34.4% share, supported by its affordability, simplicity, widespread availability, and essential role in initial hemoglobinopathy detection and monitoring.

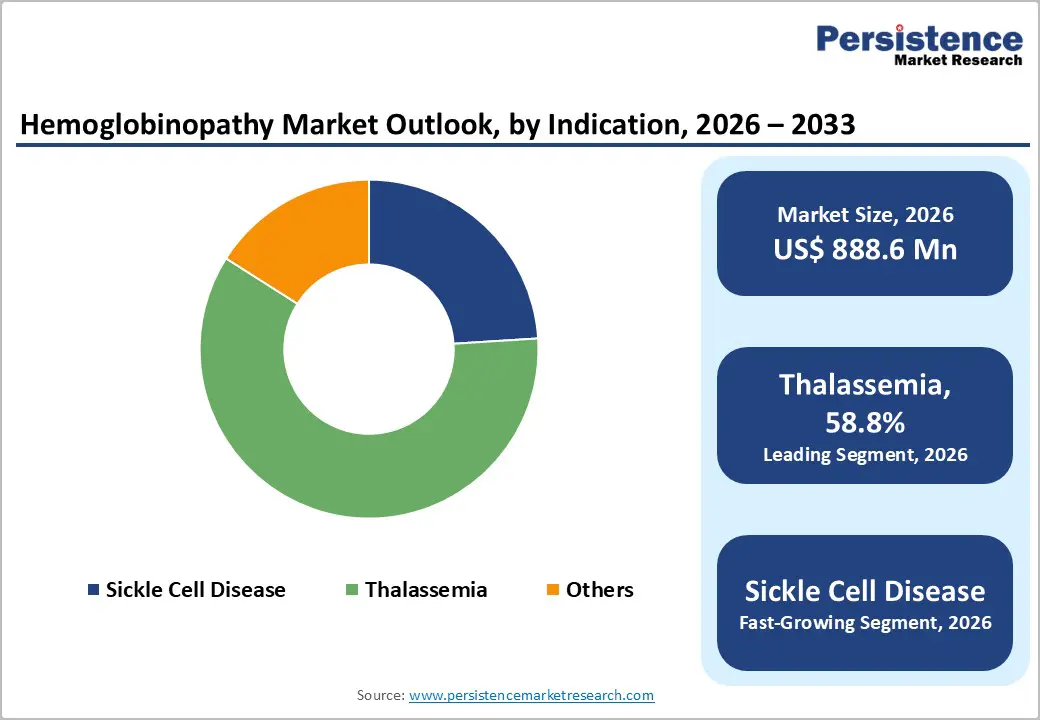

- Leading Indication: Thalassemia remains dominant with 58.8%, driven by high incidence in endemic regions, growing awareness of early diagnosis, and the critical need for timely management to prevent complications.

- Leading End-user: Hospitals & Clinics lead with 47.3% share, due to their advanced lab facilities, high patient volumes, skilled hematology specialists, and integration of diagnostics into comprehensive treatment pathways.

- Early detection initiatives across developed and emerging countries drive demand, enabling timely intervention and reducing long-term complications in hemoglobinopathy patients.

- Portable and rapid POC devices are gaining traction, improving accessibility in remote and resource-limited settings.

- Policies supporting mandatory newborn and school screening programs directly increase demand for hemoglobinopathy diagnostics.

| Key Insights | Details |

|---|---|

|

Global Hemoglobinopathy Market Size (2026E) |

US$ 888.6 Million |

|

Market Value Forecast (2033F) |

US$ 1,259.9 Million |

|

Projected Growth (CAGR 2026 to 2033) |

5.1% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.7% |

Market Dynamics

Driver - Rising Global Prevalence and Early Screening Programs

Hemoglobinopathies are among the most prevalent inherited disorders worldwide, with approximately 7% of the global population as carriers and 2.7‰ of births affected. Traditionally endemic to Southern Europe, Africa, the Middle East, and Asia, these disorders now occur globally due to population migration. Clinical severity ranges from mild microcytosis to life-threatening conditions such as sickle cell disease (SCD) and Hb Bart’s hydrops fetalis, often necessitating lifelong transfusions. Early and accurate diagnosis is essential, relying on hemoglobin electrophoresis and quantification of Hb A2, enabling timely interventions such as blood transfusions and hydroxyurea therapy, which significantly improve survival and quality of life.

Specific phenotypes-Hb SS, Hb SC, Hb SDPunjab, Hb Sβ thalassemia, Hb SOArab, and Hb S/HPFH-benefit most from early screening. To enhance care and awareness, the Thalassaemia International Federation (TIF) launched the Pan American Network for Haemoglobin Disorders (PANHD), fostering collaboration among patient associations, healthcare professionals, and stakeholders across the Americas.

This unified approach facilitates knowledge sharing, standardizes diagnostic practices, and strengthens patient management, positioning early and widespread screening programs as a pivotal driver of global hemoglobinopathy diagnostics market growth.

Restraints - Cardiovascular Complications and Limited Access to Advanced Diagnostics

Cardiovascular complications remain a major concern for patients with hemoglobinopathies, contributing to morbidity and mortality despite advances in therapy. Conditions such as ventricular dysfunction, pulmonary hypertension, pericarditis-myocarditis, arrhythmias, strokes, and thromboembolic events are prevalent, particularly in patients with severe anemia or iron overload from repeated transfusions.

While improved diagnostic tools and therapeutic strategies exist, detecting these complications early can be challenging, particularly in low-resource settings where access to advanced imaging, laboratory testing, and specialist care is limited. Additionally, variability in clinical presentation and overlapping with other comorbidities delay diagnosis, complicating timely intervention. These challenges underscore the need for continuous medical innovation, enhanced patient education, and expanded access to high-quality diagnostics.

The reliance on specialized equipment, trained personnel, and infrastructure in certain regions increases operational complexity and limits adoption, restraining market growth. Thus, while hemoglobinopathy diagnostics offer clear clinical benefits, barriers such as disease complexity, variable presentation, and healthcare accessibility continue to slow market penetration globally.

Opportunity - Advancements in Point-of-Care, Rapid, and High-Accuracy Diagnostic Technologies

Advancements in hemoglobinopathy screening and diagnostics are creating significant opportunities for market expansion. Traditional techniques such as hemoglobin electrophoresis are being complemented by high-accuracy methods including capillary electrophoresis (CE), high-performance liquid chromatography (HPLC), and LC-MS/MS, which provide precise detection of hemoglobin variants.

Point-of-care tests (POCT) and rapid diagnostic tests (RDTs), such as Sickle SCAN, have enhanced accessibility, particularly in resource-limited settings. In June 2024, BioMedomics announced a three-year Independent Research Grant to advance SCD diagnostics and management in Sub-Saharan Africa, coinciding with World Sickle Cell Disease Day.

Additionally, clinical studies presented at the Academy for Sickle Cell and Thalassemia (ASCAT) 19th Annual Scientific Conference in October 2024 demonstrated that the Gazelle™ Hb Variant Test enables rapid, cost-effective newborn and premarital screening in regions disproportionately affected by hemoglobin disorders, including Ghana and Türkiye. These innovations support universal screening programs, improve early detection, and facilitate timely interventions, such as transfusions or hydroxyurea therapy. Increasing adoption of accessible, accurate, and affordable diagnostic technologies, combined with government initiatives and global health programs, positions the hemoglobinopathy diagnostics market for accelerated growth and broader impact on patient outcomes worldwide.

Category-wise Analysis

By Diagnostic Test: Routine Red Blood Cell (RBC) Count Dominate Due to Simplicity, Accessibility, and Early Detection Capability

Routine Red Blood Cell (RBC) count is expected to capture 34.4% of the global hemoglobinopathy market by 2026. This test remains widely used due to its affordability, simplicity, and availability in most clinical laboratories. It serves as a critical first-line screening tool for detecting anemia, abnormal hemoglobin levels, and microcytosis associated with hemoglobinopathies. Its ability to provide rapid results enables early identification of at-risk patients, guiding subsequent confirmatory tests such as hemoglobin electrophoresis or molecular analysis. The widespread adoption of RBC counts, especially in newborn and prenatal screening programs, reinforces its dominance in the market.

By Indication: Thalassemia Lead Owing to High Prevalence and Need for Early Diagnosis and Management

Thalassemia is projected to hold nearly 58.8% of the global hemoglobinopathy market by 2026, driven by its high prevalence in regions such as Southeast Asia, the Mediterranean, and the Middle East. Early diagnosis is crucial for initiating timely interventions like regular blood transfusions, iron chelation therapy, and genetic counseling to prevent severe complications. Newborn and prenatal screening programs are increasingly implemented to identify at-risk infants, further boosting diagnostic demand. The growing awareness of thalassemia’s health impact, combined with government-supported screening initiatives and specialized clinical infrastructure, positions it as the leading indication in the global hemoglobinopathy diagnostics market.

By End-user: Hospitals & Clinics Lead Owing to Advanced Infrastructure and High Patient Volumes

Hospitals and clinics are projected to account for nearly 47.3% of the global hemoglobinopathy market by 2026. These facilities offer advanced laboratory infrastructure, skilled hematology specialists, and integrated care pathways, enabling accurate diagnosis and follow-up of hemoglobin disorders. High patient volumes, particularly in urban centers, further increase the demand for routine and confirmatory tests. Hospitals and clinics are also central to newborn and prenatal screening programs, allowing early identification and intervention for conditions like sickle cell disease and thalassemia. Their role in patient management, comprehensive testing, and treatment coordination makes them the dominant end-user segment in the market.

Regional Insights

North America Hemoglobinopathy Market Trends

North America is projected to capture 37.3% of the global hemoglobinopathy market by 2026, driven by well-established newborn screening programs and advanced diagnostic infrastructure. Sickle cell disease (SCD) affects over 100,000 individuals in the U.S., and early detection via newborn screening enables timely interventions such as blood transfusions and hydroxyurea therapy, improving patient outcomes and reducing complications.

The New York State Newborn Screening Program, housed at the Wadsworth Center, was the first in the U.S. to implement SCD screening in 1975. In October 2025, the program celebrated its 50th anniversary, promoting awareness through community engagement and highlighting the impact of early diagnostics.

Additionally, the integration of interdisciplinary education initiatives, such as the Interprofessional Education (IPE) event held in November 2025 at the University at Albany’s College of Integrated Health Sciences (CIHS), underscores the region’s focus on collaborative approaches to follow-up care. Coupled with ongoing clinical trials evaluating gene therapy for transfusion-dependent β-thalassemia and SCD, these initiatives solidify North America’s leadership in hemoglobinopathy diagnostics and reinforce early detection as a key market growth driver.

Europe Hemoglobinopathy Market Trends

Europe is expected to account for 24.8% of the global hemoglobinopathy market by 2026, supported by the expansion of neonatal screening programs and specialized diagnostic infrastructure. Hemoglobinopathies, including thalassemia and sickle cell disease (SCD), are increasingly observed due to migration and historical genetic patterns.

Many European countries have implemented systematic newborn and prenatal screening programs, enabling early detection of high-risk cases and timely interventions. National registries and multinational collaborations improve patient monitoring, evidence-based care, and access to treatment, although disparities persist across regions.

Innovative therapies, including gene-editing approaches, are being piloted, but accessibility is limited by high costs and infrastructure constraints. Targeted control programs for at-risk couples, particularly for β-thalassemia, combined with prenatal diagnostics, have successfully lowered the incidence of transfusion-dependent cases when effectively executed.

Countries such as Italy exemplify effective prenatal prevention and neonatal screening programs. The presence of expert centers, trained healthcare professionals, and standardized diagnostic protocols in many European nations positions the region as a key driver for the hemoglobinopathy diagnostics market, enabling early diagnosis, improved patient management, and long-term reduction in disease burden.

Asia Pacific Hemoglobinopathy Market Trends

The Asia Pacific hemoglobinopathy diagnostics market is rapidly expanding, projected to grow at a CAGR of 6.6%, driven by high prevalence of disorders like sickle cell disease (SCD) and thalassemia, particularly in India, which accounts for over 50% of global SCD cases.

Approximately 2,00,000 babies are born annually with SCD in India, highlighting the critical need for widespread screening. Early diagnosis through population screening for sickle cell trait (SCT) and hemoglobinopathies enables timely interventions, reducing complications and improving patient outcomes.

In June 2025, the National Institute of Immunohaematology (NIIH), under the Indian Council of Medical Research (ICMR), launched a national Rare Donor Registry to support patients requiring repeated transfusions. The Union Health Ministry’s plan to integrate the Rare Donor Registry with the e-Rakt Kosh platform will enhance access to rare blood types, streamline transfusion management, and improve coordination among hospitals and blood banks.

These initiatives, combined with growing government focus on neonatal screening and infrastructure expansion, position Asia Pacific as a key growth driver for hemoglobinopathy diagnostics, facilitating early detection, improved patient care, and scalable solutions for high-risk population.

Competitive Landscape

The global hemoglobinopathy diagnostics market is highly competitive, driven by innovations in point-of-care testing, high-accuracy molecular diagnostics, and electrophoresis platforms. Market players focus on expanding newborn and prenatal screening programs, enhancing test accuracy, and improving accessibility in resource-limited regions. Strategic partnerships, research grants, and regional pilot programs further intensify competition and accelerate adoption globally.

Key Industry Developments:

- In October 2025, The New York State Newborn Screening Program celebrated 50 years of sickle cell disease screening, highlighting early diagnosis benefits, community awareness initiatives, and commemorative events during National Sickle Cell Awareness Month.

- In June 2024, BioMedomics launched a three-year Independent Research Grant to advance Sickle Cell Disease testing and management in Sub-Saharan Africa, coinciding with World Sickle Cell Disease Day.

Companies Covered in Hemoglobinopathy Market

- Bio-Rad Laboratories, Inc.

- Abcam Limited (Danaher)

- Revvity

- HiMedia Laboratories

- Sebia

- Hemex Health

- ShanMukha Innovations Pvt Ltd

- Trivitron Healthcare

- TrueHb

- SYnAbs S.A.

- Alpine Biomedicals Pvt. Ltd.

- BIOSENSE SRL

- Bio Lab Diagnostics (I) Private Limited

- Trinity Biotech

- BIOMEDOMICS INC.

Frequently Asked Questions

The global hemoglobinopathy market is projected to be valued at US$ 888.6 Million in 2026.

Rising global prevalence of hemoglobinopathies and expanding newborn and prenatal screening programs drive market growth.

The global market is poised to witness a CAGR of 5.1% between 2026 and 2033.

Advancements in point-of-care, rapid, and high-accuracy diagnostic technologies present major growth opportunities.

Major players in the global hemoglobinopathy market include Bio-Rad Laboratories, Inc., Abcam Limited (Danaher), Revvity, HiMedia Laboratories, Sebia, and others.