- Pharmaceuticals

- Pulmonary Arterial Hypertension Market

Pulmonary Arterial Hypertension Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Global Pulmonary Arterial Hypertension Market by Drug Class (Endothelin Receptor Antagonists, PDE-5 Inhibitors, Prostacyclin and Prostacyclin Analogs, and SGC Stimulators), by Type (Branded and Generics) by Route of Administration (Oral, Intravenous, and Inhalational), by Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and Online Pharmacies), and Regional Analysis from 2026 to 2033

Pulmonary Arterial Hypertension Market Share and Trend Analysis

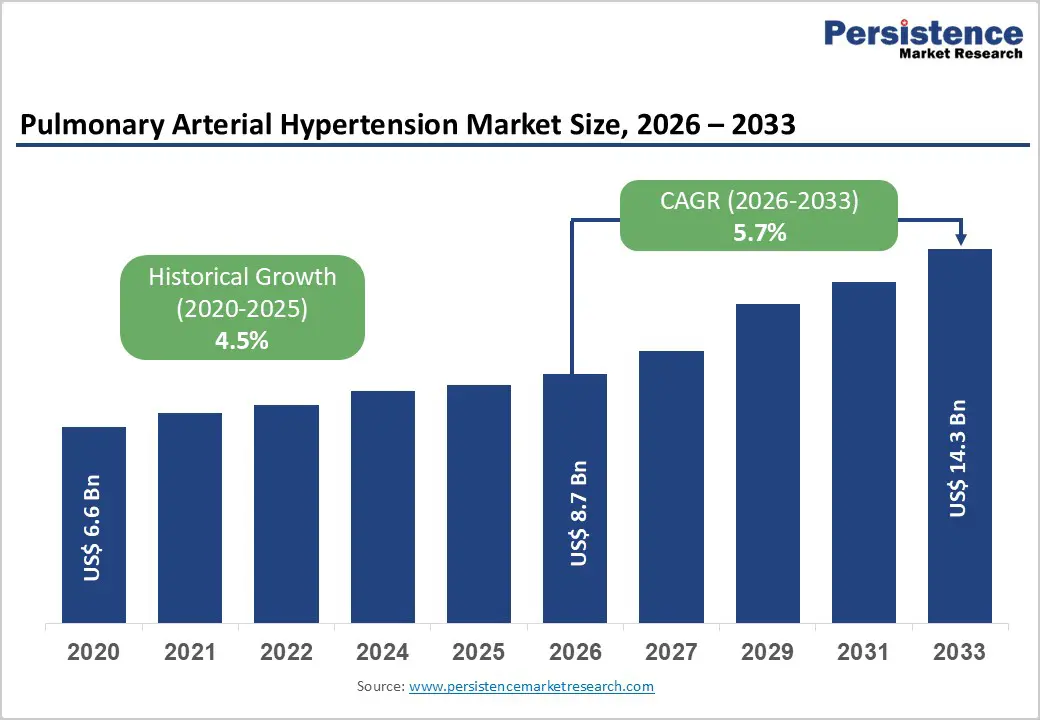

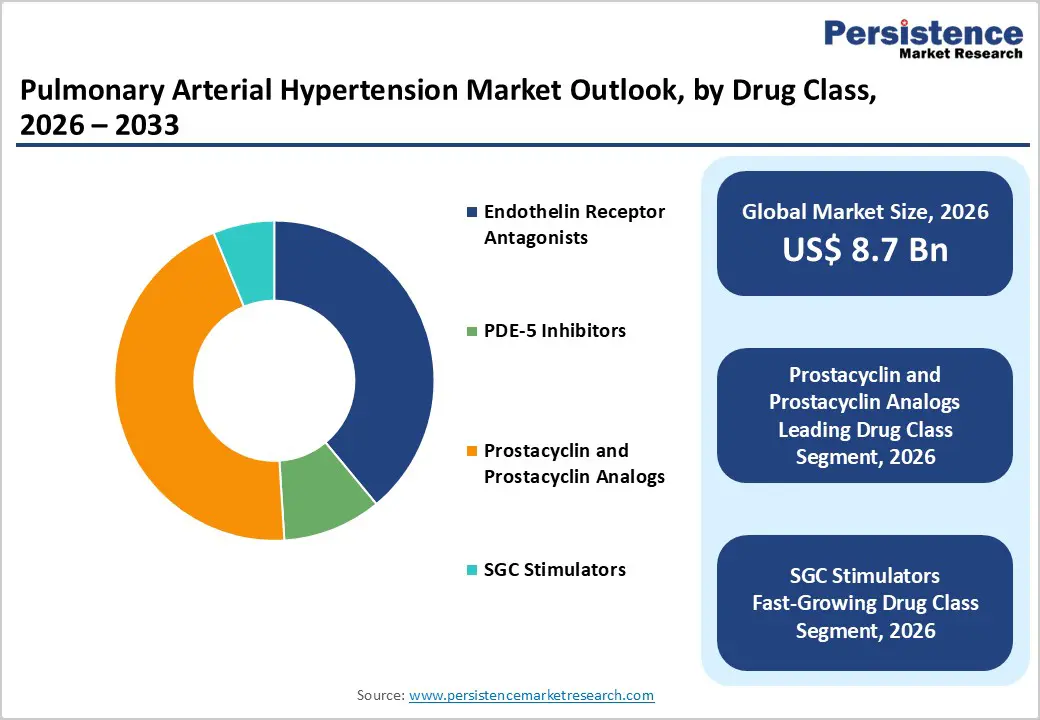

The global pulmonary arterial hypertension market size is estimated to grow from US$ 8.7 Bn in 2026 to US$ 14.3 Bn by 2033. The market is projected to record a CAGR of 5.7% during the forecast period from 2026 to 2033.

Global demand for pulmonary arterial hypertension (PAH) therapies is increasing steadily, driven by improved disease awareness, rising diagnosis rates, and advances in cardiopulmonary diagnostic capabilities. Greater recognition of risk factors such as connective tissue disorders, congenital heart disease, genetic predisposition, and chronic cardiopulmonary conditions has significantly expanded the identified patient population. Wider adoption of advanced diagnostic tools, including echocardiography, right heart catheterization, and biomarker-based risk stratification, enables earlier diagnosis and timely initiation of targeted therapy. PAH drugs are extensively used across hospitals and specialized pulmonary hypertension centers to deliver sustained symptom control, improved functional capacity, and long-term survival benefits. The global shift toward oral therapies, combination regimens, and patient-centric dosing strategies is accelerating adoption by improving adherence and reducing treatment burden compared with complex parenteral regimens. Continuous innovation in prostacyclin formulations, endothelin receptor antagonists, sGC stimulators, and disease-modifying biologics is enhancing clinical outcomes and broadening treatment eligibility. Rising healthcare expenditure, expanding specialty care infrastructure, and improved reimbursement access in emerging economies are reinforcing long-term demand. Additionally, growing clinical awareness, updated treatment guidelines, and favorable reimbursement frameworks in developed regions continue to support sustained global market growth.

Key Industry Highlights

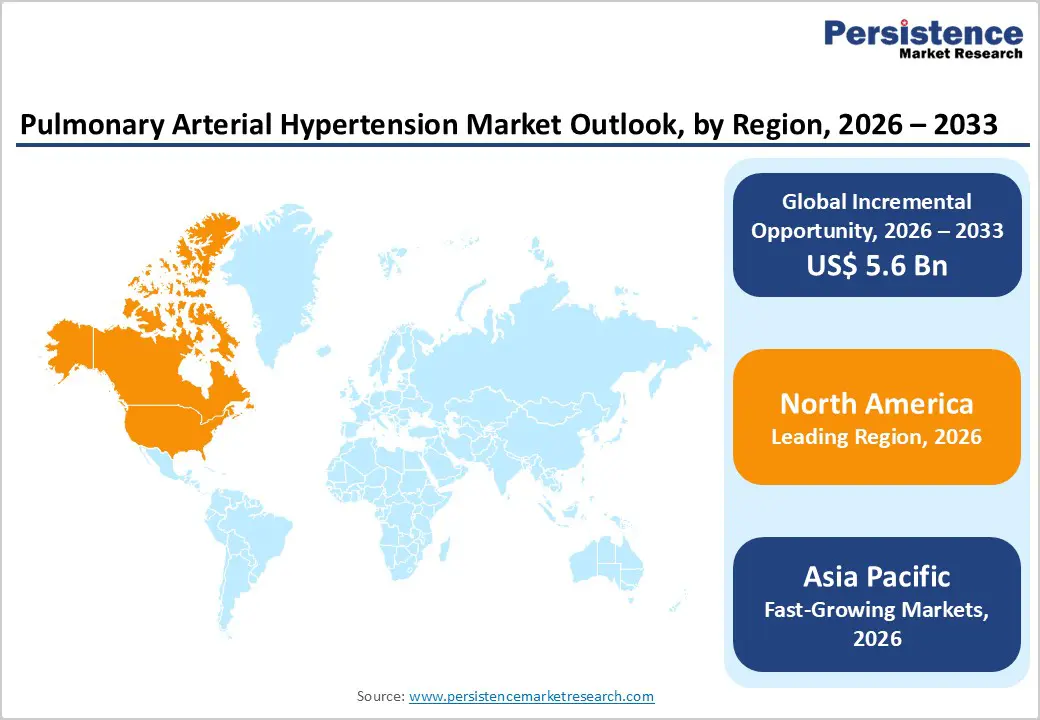

- Leading Region: North America holds the largest share at 47.3%, supported by advanced healthcare infrastructure, high diagnostic penetration, early adoption of novel PAH therapies, strong reimbursement coverage, and the presence of leading pharmaceutical companies.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to rising healthcare expenditure, improving access to specialized cardiopulmonary diagnostics, growing high-risk populations, rapid hospital infrastructure expansion, and increasing adoption of advanced PAH therapies.

- Leading Drug Class Segment: Prostacyclin and prostacyclin analogs dominate the market due to strong clinical efficacy in moderate-to-severe PAH, widespread use in advanced disease management, and continued innovation in delivery systems and formulations.

- Fastest-Growing Drug Class Segment: SGC stimulators are growing steadily as adoption increases for earlier-stage treatment and combination therapy, supported by favorable clinical outcomes and expanding guideline recommendations.

- Leading Route of Administration Segment: Oral remains the top segment, driven by clinical preference for convenient long-term therapy, improved patient adherence, and broad use across early and intermediate PAH stages.

- Fastest-Growing Route of Administration Segment: Intravenous is witnessing renewed growth due to its continued necessity in treating complex MDR/XDR-TB cases, pediatric patients, and patients unable to tolerate oral therapy, particularly in hospital and emergency care settings.

| Report Attribute | Details |

|---|---|

|

Pulmonary Arterial Hypertension Market Size (2026E) |

US$ 8.7 Bn |

|

Market Value Forecast (2033F) |

US$ 14.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.7 % |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.5% |

Market Dynamics

Driver – Growing Disease Awareness and Expanding Use of Targeted Combination Therapies

Growth is strongly supported by increasing awareness, improved diagnosis rates, and wider adoption of guideline-recommended therapies for pulmonary arterial hypertension. Advances in non-invasive screening, echocardiography, and right heart catheterization have improved early identification, particularly among high-risk populations such as patients with connective tissue disorders, congenital heart disease, and hereditary PAH. Clinical guidelines increasingly emphasize early intervention and risk-based treatment escalation, driving demand for targeted drug classes including endothelin receptor antagonists, prostacyclin analogs, PDE-5 inhibitors, and sGC stimulators.

The shift toward combination therapy as a standard of care has significantly increased per-patient treatment value, especially in moderate-to-severe cases. Improved survival outcomes and quality of life associated with newer agents encourage long-term therapy continuation. Additionally, growing physician expertise, patient advocacy initiatives, and specialized PAH treatment centers are strengthening treatment adherence. Favorable reimbursement policies in developed markets and inclusion of PAH under rare disease frameworks further support access to high-cost therapies. Collectively, these factors are accelerating treatment uptake, expanding the diagnosed patient pool, and sustaining long-term demand for advanced pharmacological management.

Restraints – High Treatment Costs, Complex Administration, and Delayed Diagnosis

Market expansion is constrained by the high cost of PAH therapies, particularly branded prostacyclin formulations and combination regimens used in advanced disease stages. Long-term treatment requirements place a substantial financial burden on healthcare systems and patients, especially in regions with limited reimbursement coverage. Parenteral and inhaled therapies involve complex administration, dose titration, and continuous monitoring, which can reduce patient compliance and limit broader adoption.

Delayed diagnosis remains a critical challenge, as early PAH symptoms often overlap with common cardiopulmonary conditions, leading to under-recognition and late-stage presentation. In emerging markets, limited access to specialized diagnostic tools and trained pulmonary hypertension specialists further restrict timely treatment initiation. Adverse effects associated with certain drug classes, such as hypotension, gastrointestinal symptoms, and infusion-site complications, may also impact therapy persistence. Additionally, stringent regulatory requirements and lengthy clinical development timelines increase R&D costs and delay market entry for innovative therapies. These clinical, economic, and systemic barriers collectively temper growth momentum and highlight the need for simplified treatment options and broader diagnostic access.

Opportunity – Innovation in Disease-Modifying Therapies and Expansion in Emerging Regions

Substantial opportunities are emerging from ongoing innovation aimed at addressing the underlying pathophysiology of pulmonary arterial hypertension rather than solely managing symptoms. Development of disease-modifying agents, novel biologics, and next-generation prostacyclin formulations with improved safety and dosing convenience is reshaping the treatment landscape. Oral and inhaled therapies with longer duration of action and reduced side effects are expected to enhance adherence and expand use in earlier disease stages.

Improved genetic testing, biomarker-driven risk stratification, and digital patient monitoring tools enable personalized treatment approaches and earlier intervention. Expanding screening initiatives and referral networks are increasing diagnosis rates, particularly in underpenetrated regions. Emerging markets across Asia Pacific, Latin America, and the Middle East present strong growth potential due to rising healthcare investment, expanding specialty care infrastructure, and improving reimbursement mechanisms. Local manufacturing, introduction of generics, and public–private collaborations are improving affordability and access. Strategic partnerships, accelerated clinical trials, and regulatory support for orphan drugs are expected to fast-track innovation, positioning PAH therapies as a key growth area within the rare cardiovascular disease segment.

Category-wise Analysis

By Drug Class, Prostacyclin and Prostacyclin Analogs Lead Due to Superior Efficacy in Advanced PAH

Prostacyclin and prostacyclin analogs are projected to dominate the global pulmonary arterial hypertension market in 2026, accounting for a revenue share of 44.8%. This leadership is primarily attributed to their proven clinical efficacy in managing moderate-to-severe PAH and improving exercise capacity, hemodynamics, and long-term survival outcomes. These therapies are often prescribed for high-risk and advanced PAH patients, particularly those who show inadequate response to oral monotherapies. Increasing emphasis on early diagnosis, risk stratification, and guideline-driven escalation to combination or parenteral therapy has expanded their adoption. The availability of multiple delivery formats, including intravenous, subcutaneous, inhaled, and oral formulations, further enhances treatment flexibility and patient suitability. Continued innovation in long-acting formulations, improved delivery systems, and next-generation prostacyclin agents is supporting better adherence and safety profiles. Strong clinical guideline endorsement and increasing use in combination regimens ensure sustained dominance of this drug class throughout the forecast period.

By Route of Administration, Oral Therapies Dominate Due to Ease of Use and Long-Term Management

The oral segment is expected to lead the pulmonary arterial hypertension market in 2026, capturing a revenue share of 66.0%. Oral therapies remain the preferred first-line and maintenance treatment option due to their convenience, ease of administration, and suitability for long-term outpatient disease management. They are widely prescribed across early- and intermediate-risk PAH patients, particularly endothelin receptor antagonists, PDE-5 inhibitors, and sGC stimulators. Oral regimens support better patient adherence compared with parenteral therapies, reduce hospitalization requirements, and lower overall treatment burden. Standardized oral combination therapies are increasingly adopted in accordance with evolving PAH treatment guidelines, reinforcing clinical confidence. Ongoing development of once-daily dosing, fixed-dose combinations, and improved safety profiles further boosts uptake. Expanding availability through hospital and retail pharmacies, along with reimbursement coverage in developed markets, continues to support the sustained leadership of oral administration in global PAH treatment.

By Distribution Channel, Hospital Pharmacies Lead Due to Centralized Diagnosis and Specialized Care

Hospital pharmacies are projected to dominate the global pulmonary arterial hypertension market in 2026, accounting for a revenue share of 58.0%. This dominance is driven by the central role hospitals play in PAH diagnosis, risk assessment, treatment initiation, and long-term disease monitoring. PAH management often requires specialized cardiopulmonary centers with access to right heart catheterization, advanced imaging, and multidisciplinary care teams. High-cost therapies such as prostacyclin analogs and combination regimens are typically initiated and managed through hospital settings. Hospital pharmacies also support therapy titration, adverse event monitoring, and patient education programs. Favorable reimbursement frameworks, payer preference for hospital-based dispensing of specialty drugs, and government-supported rare disease programs further strengthen utilization. In addition, tertiary care hospitals frequently participate in clinical trials and early adoption of newly approved PAH therapies, reinforcing hospital pharmacies as the primary distribution channel.

Region-wise Insights

North America Pulmonary Arterial Hypertension Market Trends

North America is expected to dominate the global pulmonary arterial hypertension market with a value share of 47.7% in 2026, led primarily by the United States. The region benefits from advanced healthcare infrastructure, high disease awareness, and widespread access to specialized PAH diagnostic and treatment centers. Early diagnosis is supported by established referral pathways, routine screening in high-risk populations, and strong adherence to international clinical guidelines.

The presence of leading pharmaceutical companies, robust R&D investments, and rapid commercialization of novel therapies accelerates market growth. Favorable reimbursement policies under both public and private insurance plans support access to high-cost branded therapies, including prostacyclin analogs and combination regimens. In addition, strong patient advocacy networks and physician education programs improve treatment adherence and long-term outcomes. North America’s emphasis on personalized therapy selection, digital patient monitoring, and continuous guideline updates is expected to sustain its market leadership throughout the forecast period.

Europe Pulmonary Arterial Hypertension Market Trends

The European pulmonary arterial hypertension market is projected to grow steadily, supported by strong public healthcare systems, well-established hospital networks, and increasing focus on early disease detection. Countries such as Germany, the U.K., France, Italy, and Spain lead adoption due to specialized pulmonary hypertension centers and structured referral systems. National healthcare coverage ensures broad access to both first-line oral therapies and advanced parenteral treatments, supporting consistent treatment adherence. Strict regulatory oversight by European health authorities ensures high-quality drug manufacturing and standardized treatment protocols.

Increasing adoption of combination therapy, growing use of inhaled and oral prostacyclin formulations, and emphasis on risk-based treatment escalation drive market expansion. Collaborative clinical research initiatives and continuous professional training enhance management of complex PAH cases. As awareness improves and diagnostic capabilities expand across Eastern and Southern Europe, the region is expected to maintain stable growth with strong emphasis on patient safety and outcomes.

Asia Pacific Pulmonary Arterial Hypertension Market Trends

The Asia Pacific pulmonary arterial hypertension market is expected to register a higher CAGR of around 7.7% between 2026 and 2033, driven by improving healthcare infrastructure, rising disease awareness, and expanding access to specialized cardiopulmonary care. Countries including China, India, Japan, South Korea, and Australia are witnessing increased diagnosis rates due to better availability of echocardiography and referral to tertiary care centers.

Government investments in hospital infrastructure and rare disease management programs are supporting broader adoption of PAH therapies. Regional pharmaceutical manufacturers are improving affordability through generic and locally produced formulations, enhancing treatment access. Urban hospitals are increasingly implementing standardized PAH treatment protocols aligned with global guidelines. Expansion of physician training programs, digital health platforms, and reimbursement coverage further improves disease management. Growing patient awareness and earlier intervention strategies position Asia Pacific as the fastest-growing regional market during the forecast period.

Market Competitive Landscape

The global pulmonary arterial hypertension market is highly competitive, with strong participation from companies such as United Therapeutics Corporation, Bayer AG, Gilead Sciences, Inc., Merck & Co., Inc., Pfizer Inc., and Johnson & Johnson. These players leverage extensive global distribution networks, strong brand recognition, and diversified cardiovascular and specialty pharmaceutical portfolios to address

Their product offerings focus on targeted drug classes including prostacyclin and prostacyclin analogs, endothelin receptor antagonists, PDE-5 inhibitors, and sGC stimulators, along with combination regimens and patient-centric formulations aimed at improving treatment adherence, clinical outcomes, and long-term disease management. Continuous innovation in drug development, regulatory approvals, clinical efficacy, safety optimization, and compliance with international quality and manufacturing standards remains critical for sustaining competitive positioning in the global pulmonary arterial hypertension market.

Key Industry Developments:

- In June 2024, the FDA approval of sotatercept marked a significant advancement in the treatment of pulmonary arterial hypertension, with UCHealth and the University of Colorado playing a pivotal role in the clinical trials that supported approval of this novel therapy for the debilitating condition.

- In March 2024, Merck announced FDA approval of WINREVAIR™ (sotatercept-csrk) for adults with WHO Group 1 pulmonary arterial hypertension to improve exercise capacity, functional class, and reduce clinical worsening. WINREVAIR, previously granted Breakthrough Therapy Designation, is the first activin signaling inhibitor approved for PAH, targeting abnormal vascular cell proliferation.

Companies Covered in Pulmonary Arterial Hypertension Market

- United Therapeutics Corporation

- Bayer AG

- Gilead Sciences, Inc.

- Merck & Co., Inc.

- Pfizer Inc.

- Johnson & Johnson

- Viatris Inc.

- GSK Plc.

- Sandoz Group AG

- Lupin Pharmaceuticals, Inc.

- Sun Pharmaceutical Industries Ltd

- Teva Pharmaceutical Industries Ltd

- Shubham Pharmachem Pvt Ltd

- Arena Pharmaceuticals

Frequently Asked Questions

The global pulmonary arterial hypertension market is projected to be valued at US$ 8.7 Bn in 2026.

The global pulmonary arterial hypertension market is driven by rising disease awareness and diagnosis rates, expanding use of combination therapies, continuous approvals of innovative targeted drugs, improved survival outcomes, and strong reimbursement support in developed healthcare systems.

The global pulmonary arterial hypertension market is poised to witness a CAGR of 5.7% between 2026 and 2033.

Major opportunities lie in the development of novel disease-modifying therapies, expansion of inhaled and oral prostacyclin formulations, growth of generics in emerging markets, and increasing adoption of digital and home-based PAH management solutions.

United Therapeutics Corporation, Bayer AG, Gilead Sciences, Inc., Merck & Co., Inc., Pfizer Inc., and Johnson & Johnson are some of the key players in the pulmonary arterial hypertension market.